铝模板市场规模、份额、增长、趋势分析及预测(2031年)

铝模板市场规模和预测(2021-2031 年)、全球和区域份额、趋势和增长机会分析报告范围:按产品(解决方案、服务)、类型(板模板、墙模板、角模板、梁模板、其他)、应用(工业、商业、住宅)和地理区域(北美、欧洲、亚太地区、中东和非洲、南美和中美)

- 状态 : 已发布

- 报告代码 : TIPRE00041003

- 类别 : 制造和建筑

- 页数 : 230

- 可用报告格式 :

- 最后更新日期 : November 26, 2025

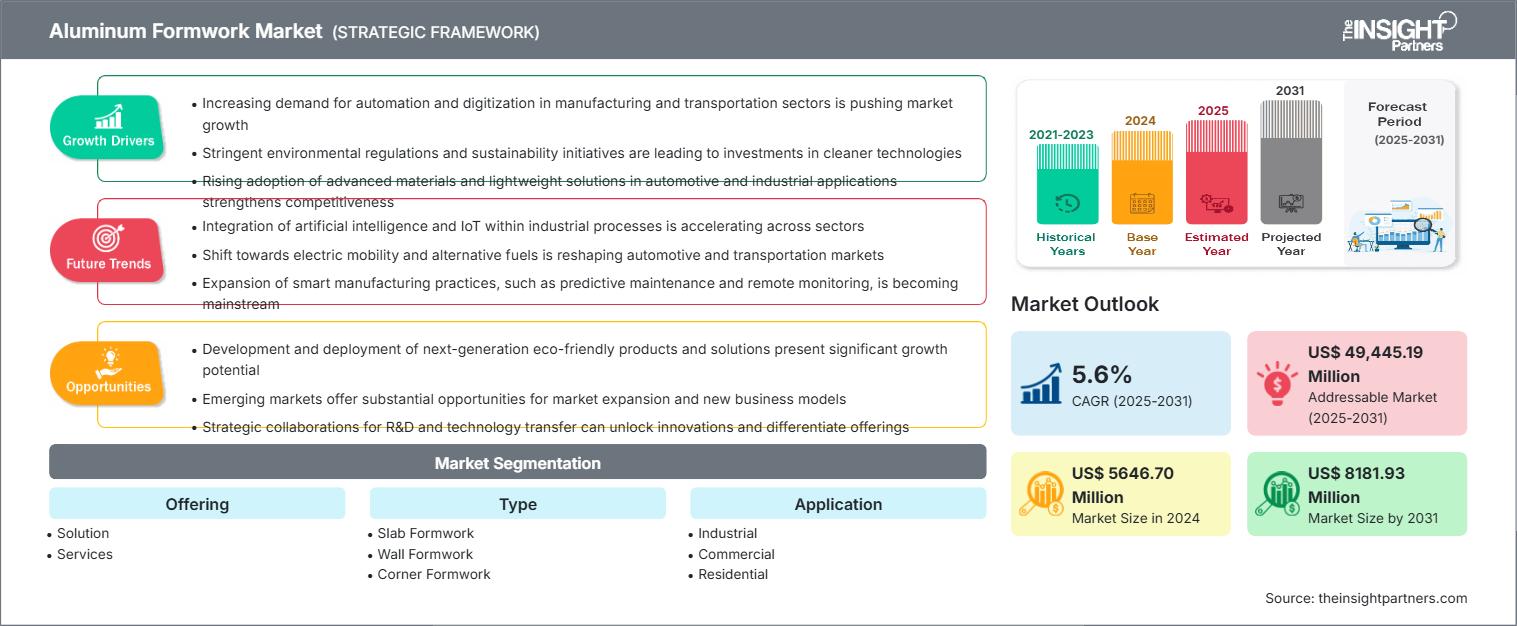

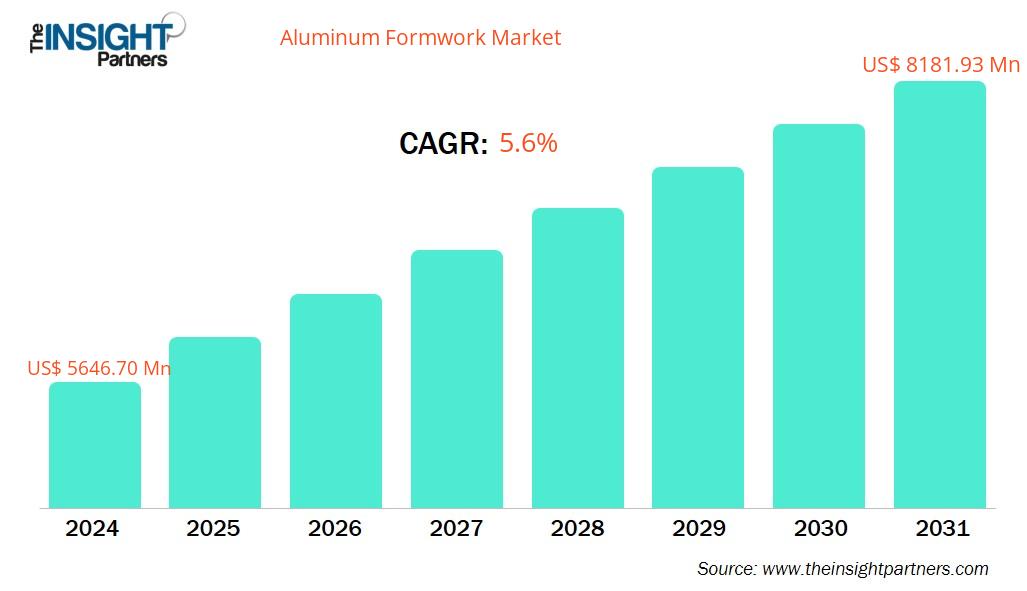

铝模板市场规模预计将从 2024 年的 56.467 亿美元增至 2031 年的 81.8193 亿美元。预计 2025-2031 年期间该市场的复合年增长率为 5.6%。

铝模板市场分析

在当前市场中,建筑商和承包商面临着使用先进建筑材料的压力,以保持竞争优势。这部分包括安装价格合理的脚手架和模板方案,同时提高工人安全、建筑材料质量和施工效率。除了模板解决方案外,服务还包括维护和检查、改造、远程支持和热线套餐、维修和备件以及咨询。墙体、楼板支撑平台、艺术石纹理面板、梁、水下柱、混凝土房屋/泳池建造以及水中柱重建只是模板解决方案众多用途中的一小部分。

铝模板市场概况:

建筑承包商在现场制作结构模具的常用技术是模板。现代模板系统在建筑中的应用得益于技术发展以及对高效、经济解决方案的需求。模板是一种低成本的解决方案,但需要大量的安装和组装时间,因为需要使用胶合板或木材来制作模具,并在现场根据特定需求进行准备。另一方面,模板系统使用金属或金属和木材的组合来构建框架,从而最大限度地减少了复杂性并节省了组装时间。该系统易于组装,减少甚至消除了现场材料切割的需要。模板系统为工人提供了更简单的解决方案,并提高了建筑工地的安全性。由于表面采用框架结构构建,易于连接和安装,因此其生命周期成本较低。如果维护和保养得当,模板系统可提供最大的可重复使用性。

您将获得任何报告的免费定制,包括本报告的部分内容、国家级分析、Excel 数据包,以及为初创企业和大学提供优惠和折扣

铝模板市场:战略洞察

-

获取此报告的顶级关键市场趋势。此免费样品将包括数据分析,从市场趋势到估计和预测。

铝模板市场驱动力和机遇formwork Market Drivers and Opportunities

市场驱动因素:

-

铝模板系统日益受到青睐:Formwork Systems:

铝模板系统因其经济实惠、可持续性和实用性,在全球范围内越来越受欢迎。铝合金密度低、耐腐蚀性强、延展性优异,是简单和复杂建筑环境中模板应用的理想选择。铝板可重复使用200至300次而不会失去其完整性,与钢材或木材替代品相比,这降低了生命周期成本并符合绿色建筑标准。在大型或高层项目中,其轻量化设计使其操作更安全、更简便,组装更快捷,这对于工人安全和劳动效率至关重要。随着环境法规和绿色建筑实践的日益严格,使用可回收材料符合全球可持续发展目标。得益于自动化和数字化设计等先进的制造技术,可定制的铝模板系统在各个市场中都更具吸引力。

-

工业部门的发展:

在全球范围内,工业部门的扩张是铝模板市场增长的关键催化剂,这与印度的类似趋势相符。随着各国工业化和经济多元化发展,大规模建设制造设施、物流中心、能源基础设施和商业设施成为必然。在东亚、北美和欧洲等国家,由于支持先进制造业、扩大出口和增强供应链韧性的政策,工业部门在GDP中的占比正在上升。受中国“中国制造2025”、美国两党合作的基础设施规划以及欧洲对绿色产业的关注推动,专用建筑、仓库和装配厂的需求也在增长。

市场机会:

-

扩大基础设施和商业建筑:铝模板市场增长的关键驱动力:

大规模基础设施建设是推动铝模板市场扩张的主要因素。铝模板因其安装快捷、精度高、经久耐用等特点,广泛应用于桥梁、隧道、机场、地铁和商业建筑等复杂结构项目。基础设施建设支出的增加,也增加了对高效建筑技术的需求,也促使公共和私营部门的项目更加注重铝模板的多功能性、高可重复使用性和长期成本节约。

铝模板市场报告细分分析

铝模板市场细分为多个细分领域,以便更详细地了解其运营情况、增长机会和新兴趋势。以下是行业报告中使用的标准细分方法:

通过提供:

-

解决方案:

解决方案包括铝模板系统的设计、生产和配送。它们有助于混凝土板、墙、梁和角的施工。由于采用模块化设计,它们易于组装、拆卸和重复使用,从而减少了人工成本和施工时间。由于铝模板具有耐腐蚀、轻质耐用等特点,并且无需额外抹灰即可打造光滑优质的混凝土饰面,因此成为首选。 -

服务:

得益于安装、现场技术支持、维护、翻新和培训服务等增值服务,模板系统在整个施工生命周期内得到部署和优化。安装服务可确保项目按时执行、精确校准并符合安全要求。专业的现场协助可加快施工周期、降低人工成本并最大程度地减少错误。维护和翻新服务可延长铝模板的使用寿命,使其能够多次重复使用,并保护初始投资。

按类型:

-

楼板模板:

楼板模板用于浇筑楼板、天花板和屋面板等大型水平表面。其模块化设计和轻质铝制结构可实现快速安装、高效搬运并降低人工成本。

-

墙体模板:

墙体模板用于垂直建造墙体、柱子和核心筒墙,并在混凝土养护期间提供支撑。铝制墙体模板系统以其精确度、刚性和易用性而闻名,是高层住宅、商业和基础设施项目的首选。

-

角模板

角模板主要用于两块或多块墙板相接处,通常呈90度角。它能保持墙体尺寸的精度和结构强度,尤其适用于多层住宅和商业建筑。

-

梁模板

在混凝土浇筑和养护过程中,梁模板用于定型和支撑梁和大梁等水平结构部件。在住宅和商业建筑中,梁对于荷载分配至关重要。此外,精确的模板可确保最佳的荷载性能和结构完整性。

-

其他的

“其他”部分涵盖了用于弧形墙、阳台、电梯井、楼梯和建筑构件的专用和非标准模板系统。尽管它们的规模比楼板和墙体小,但它们却能应对复杂的现代建筑设计。这些模板系统经过专门设计,以满足项目的特定几何形状和结构需求。

按应用:

- 工业的

- 商业的

- 住宅

按地理位置:

- 北美

- 欧洲

- 亚太地区

- 南美洲和中美洲

- 中东和非洲

铝模板市场区域洞察

Insight Partners 的分析师已详尽阐述了预测期内影响铝模板市场的区域趋势和因素。本节还讨论了北美、欧洲、亚太地区、中东和非洲以及南美和中美洲的铝模板市场细分和地理分布。

铝模板市场报告范围

| 报告属性 | 细节 |

|---|---|

| 2024年的市场规模 | 56.467亿美元 |

| 2031年的市场规模 | 81.8193亿美元 |

| 全球复合年增长率(2025-2031) | 5.6% |

| 史料 | 2021-2023 |

| 预测期 | 2025-2031 |

| 涵盖的领域 |

通过奉献

|

| 覆盖地区和国家 |

北美

|

| 市场领导者和主要公司简介 |

|

铝模板市场参与者密度:了解其对业务动态的影响

铝模板市场正在快速增长,这得益于终端用户需求的不断增长,而这些需求的驱动因素包括消费者偏好的不断变化、技术进步以及对产品优势的认知度不断提高。随着需求的增长,企业正在扩展产品线,不断创新以满足消费者需求,并抓住新兴趋势,从而进一步推动市场增长。

- 获取铝模板市场主要参与者概览

铝模板市场份额按地区分析

受跨境电商行业蓬勃发展的推动,亚太地区铝模板市场正经历着最快的增长。南美和中美以及中东和非洲等新兴市场为铝模板供应商提供了尚未开发的扩张机会。

受建筑行业增长、制造商规模以及政府举措等因素的影响,各地区铝模板市场的增长情况各有不同。以下是各地区市场份额和趋势的总结:

1. 北美

-

市场份额:

占据全球市场的很大份额 -

关键驱动因素:

- 高昂的劳动力成本推动了对高效、可重复使用的模板系统的需求。

- 基础设施支出和大规模住宅/商业建设,尤其是在美国和加拿大。

- 更严格的绿色建筑标准(LEED、BREEAM)激励可持续的建筑方法。

-

趋势:

- 采用数字工具和人工智能监控来提高精度和生产力。

- 模块化和预制建筑项目中铝模板的使用越来越多。

- 加大对本地制造和材料回收的投资

2.欧洲

-

市场份额:

大量份额,在民用安全、能源基础设施监测和国防方面的大力投资 -

关键驱动因素:

- 采用数字工具和人工智能监控来提高精度和生产力

- 模块化和预制建筑项目中铝模板的使用日益增多

- 加大对本地制造和材料回收的投资

-

趋势:

- 快速采用模块化铝模板进行升级和翻新

- 强调可回收、节能的建筑组件

- 随着基础设施项目的扩大,东欧和南欧市场实现增长

3. 亚太地区

-

市场份额:

增长最快、市场份额占主导地位的地区 -

关键驱动因素:

- 政府对经济适用房、城市化和基础设施的投资

- 本地生产的成本效益——铝模板本地制造成本降低 30-40%

- 中国、印度、越南和印度尼西亚的重大项目燃料采用

-

趋势:

- 扩大培训和技能发展计划。

- 地铁项目逐渐从传统的木材/木料转向先进的铝制系统。

- 增加数字物流、项目管理和物料跟踪的使用

4. 南美洲和中美洲

-

市场份额:

发展中市场,特定领域的认知度不断提高,选择性采用 -

关键驱动因素:

- 基础设施投资、采矿和资源行业

- 本地采用主要集中在高端项目

- 通过跨国承包商引进先进的模板

-

趋势:

- 大型项目的跨境技术转让和技能提升。

- 由于持续的经济不稳定和庞大的非正规部门,选择性采用

5.中东和非洲

-

市场份额:

海湾国家(阿联酋、沙特阿拉伯和卡塔尔)的新兴市场增长迅速;北非较早采用 -

关键驱动因素:

- 需要快速建设和精确度的大型项目(例如迪拜2040计划、沙特2030愿景)

- 石油、天然气、旅游和城镇化项目推动先进建筑系统的使用

- 推动雄心勃勃的新城市的可持续发展和节能实践

-

趋势:

- 增加在高层、复杂建筑开发中的部署。

- 逐步扩大本地制造业和技能发展。

- 泛非洲基础设施协议有望加速发展

铝模板市场参与者密度:了解其对业务动态的影响

市场密度高,竞争激烈

由于 MFE Formwork Technology Sdn Bhd、EFCO Corp、MEVA Schalungs-Systeme GmbH、PERI GmbH 和 Doka GmbH 等老牌企业的存在,竞争非常激烈。

这种激烈的竞争促使公司通过提供以下产品脱颖而出:

- 公司通过频繁推出新产品以及模块化、可持续性和装配速度的改进来脱颖而出。

- 战略收购和全球扩张,特别是在亚太地区和中东等高增长地区,使企业能够扩大生产规模、获得新的客户群并升级技术。

- 研发投资不断推动轻量但坚固的系统设计、表面处理以及对复杂项目要求的适应性的改进。

机遇与战略举措

- 公司与当地建筑公司、政府和科技初创企业建立合资企业或合作伙伴关系,以促进市场渗透和创新。

- 数字功能的扩展,例如与 BIM(建筑信息模型)、智能传感器以及自动/手动混合装配功能的集成,使产品与众不同。

- 公司通过推出新产品、模块化、可持续性和装配速度的改进来脱颖而出。

- 战略性收购和全球扩张,尤其是在亚太地区和中东等高增长地区,使企业能够扩大生产规模、获得新的客户群并快速升级技术。

- 研发投资推动了轻量化但坚固的系统设计、表面处理以及对复杂项目要求的适应性的改进。

在铝模板市场运营的主要公司有:

- 科斯莫斯建筑机械设备私人有限公司

- 伊日田模板公司

- 克内斯特制造商有限责任公司

- Technokraft工业(印度)私营有限公司

- MFE 模板技术有限公司

- EFCO公司

- MEVA Schalungs-Systeme GmbH

- 派利有限公司

- 多卡有限公司

- PASCHAL-Werk G.

- 迈尔有限公司

免责声明:以上列出的公司没有按任何特定顺序排列。

研究过程中分析的其他公司:

- Kumkang Kind Co., Ltd.(韩国)

- ULMA建筑公司(西班牙)

- Alsina Formwork(西班牙)

- Acrow集团(澳大利亚/全球)

- NOE-Schaltechnik GmbH(德国)

- RMD Kwikform(英国/全球)

- Intek Construction(意大利)

- Pilosio SpA(意大利)

- 德国商业、能源和工业战略部(BEIS)

- Hünnebeck (BrandSafway)(德国/全球)

- 秃鹰(意大利)

- 韦科国际机场(南非)

- 苏州泰康建筑技术有限公司 (中国)

- 忠旺铝业(中国)

- GETO(中国)

- 闽发铝业(中国)

- SNTO(中国)

- 博奥铝模(中国)

- KITSEN(中国)

- 华建铝业(中国)

- AAG(阿拉伯铝业集团)(阿联酋)

- Seobo(韩国)

- 安泰铝业(中国)

- 拉耶尔(土耳其)

- 梅萨黑斑羚(墨西哥)

- 法雷辛(意大利)

- 乌尔蒂姆(土耳其)

- 阿利塔德集团(法国)

铝模板市场新闻及最新发展

- PASCHAL NeoR 轻型模板系列产品线再添新成员。除了目前使用的钢板外,该系列还新增了铝制板。在 2025 年德国宝马展上,PASCHAL 展示了其备受赞誉的 NeoR 轻型模板的扩展:对于注重效率的现场管理人员和团队而言,这款全新铝制板具有革命性的意义,因为它将最高水平的人体工程学设计与 PASCHAL 闻名遐迩的品质完美融合。

- SYFIT 和 PERI 长期以来一直保持着高效的合作。SYFIT 提供识别技术,PERI 子公司可利用该技术定期检查租赁园区内需要检查的设备。此外,SYFIT 拥有丰富的获奖经验,并拥有用于定位和识别不同类型设备的尖端技术。这些专业知识已通过 PERI 应用于建筑行业,并开发了一款先进的设备管理软件程序。

铝模板市场报告覆盖范围和交付成果

《铝模板市场规模和预测(2021-2031)》报告对以下领域进行了详细的市场分析:

- 铝模板市场规模以及涵盖范围内所有关键细分市场的全球、区域和国家层面的预测

- 铝模板市场趋势以及市场动态,例如驱动因素、限制因素和关键机遇

- 详细的 PEST 和 SWOT 分析

- 铝模板市场分析涵盖主要市场趋势、全球和区域框架、主要参与者、法规和最新市场发展

- 行业格局和竞争分析,包括市场集中度、热点图分析、知名企业以及铝模板市场的最新发展

- 详细的公司简介

Nivedita 是一位经验丰富的研究专业人士,在市场研究和商业咨询领域拥有超过 9 年的经验。她目前担任 The Insight Partners 的 ICT 领域项目经理,在管理和执行跨技术领域的联合研究、定制研究、订阅研究和咨询研究方面拥有深厚的专业知识。

Nivedita 在提供数据驱动的分析和切实可行的洞察方面拥有丰富的经验,并已成为多个关键项目的关键贡献者。她的工作涉及端到端的项目执行——从理解客户目标、分析市场趋势到制定战略建议。她与领先的 ICT 公司广泛合作,帮助他们识别市场机遇并引领行业变革。

Nivedita 拥有德拉敦 IMS 的管理学 MBA 学位。在加入 The Insight Partners 之前,她在浦那的 MarketsandMarkets 和 Future Market Insights 积累了宝贵的经验,担任过各种研究职位,并在行业分析和客户互动方面奠定了坚实的基础。

- 全面的市场规模与预测分析

- 详细的细分市场分析

- 深入的市场动态评估

- 区域及国家级洞察

- 竞争格局与企业对标分析

- 战略性商业情报

客户评价

Insight Partners 的 SCADA 系统市场报告内容全面,对当前趋势和未来预测提供了宝贵的见解。该团队始终高度专业、响应迅速且乐于助人。我们非常满意,强烈推荐他们的服务。

兰·凯德姆 伙伴, Reali Technologies LTD我请求一份关于特定软件市场的报告,团队在几天内就完成了。报告信息非常相关,而且呈现得非常出色。之后,我请求对报告进行一些修改和补充。团队再次迅速响应,不到一周我就收到了最终报告。

让-埃尔韦·詹恩 主席, 未来分析公司我们与 Insight Partners 合作进行了一项重要的市场研究和预测。他们清晰地洞察了机遇和风险,帮助我们制定了计划。他们的研究简单易用,数据可靠,帮助我们做出了明智而自信的决策。我们强烈推荐他们。

皮尤什·纳格帕尔 高级副总裁, 远光全球Insight Partners 凭借其深厚的行业专业知识,提供了富有洞察力、结构合理的市场研究。他们的团队始终专业且响应迅速。用户友好的网站让访问行业报告变得顺畅无阻。我们强烈推荐他们可靠、高质量的研究服务。

安达幸彦 首席执行官, 深蓝有限责任公司这是我第一次从The Insight Partners购买市场报告。起初我有些犹豫,但访问了他们的网站后,我更放心地冒险购买市场报告。我对报告的质量和客户服务非常满意。我对最初的报告有一些疑问和意见,但在与他们的分析师通过电子邮件沟通了几次后,我相信这份报告可以作为我们战略规划流程的参考。非常感谢您抽出宝贵的时间,让这次体验如此愉快。我一定会向其他人推荐你们的服务,当我们需要更多市场数据时,你们将是我的首选。

约翰·铃木 总裁兼首席执行官、董事会董事, BK科技感谢您在处理我关于尼日利亚传染病体外诊断市场信息请求的过程中所展现的支持和专业精神。感谢您的耐心、指导,以及您愿意提供的折扣,最终促成了这笔交易。我期待未来与 Insight Partners 继续合作,这一切都要归功于您与我初次接触后留下的良好印象。

奇吉奥克博士 ONYIA 董事总经理, PineCrest 医疗保健有限公司购买理由

- 明智的决策

- 了解市场动态

- 竞争分析

- 客户洞察

- 市场预测

- 风险规避

- 战略规划

- 投资论证

- 识别新兴市场

- 优化营销策略

- 提升运营效率

- 顺应监管趋势