医院缝合线市场规模、趋势及收入预测(至2034年)

全球医院缝合线市场规模及预测(2021-2034 年)、全球及区域份额、趋势和增长机会分析报告涵盖范围:按产品(缝合线、自动缝合器械及其他)、性质(可吸收缝合线和不可吸收缝合线)、类型(单丝和编织缝合线)、应用(普通外科、骨科、心血管外科及其他)

- 状态 : 数据发布

- 报告代码 : TIPRE00027433

- 类别 : 生命科学

- 页数 : 150

- 可用报告格式 :

- 最后更新日期 : July 29, 2026

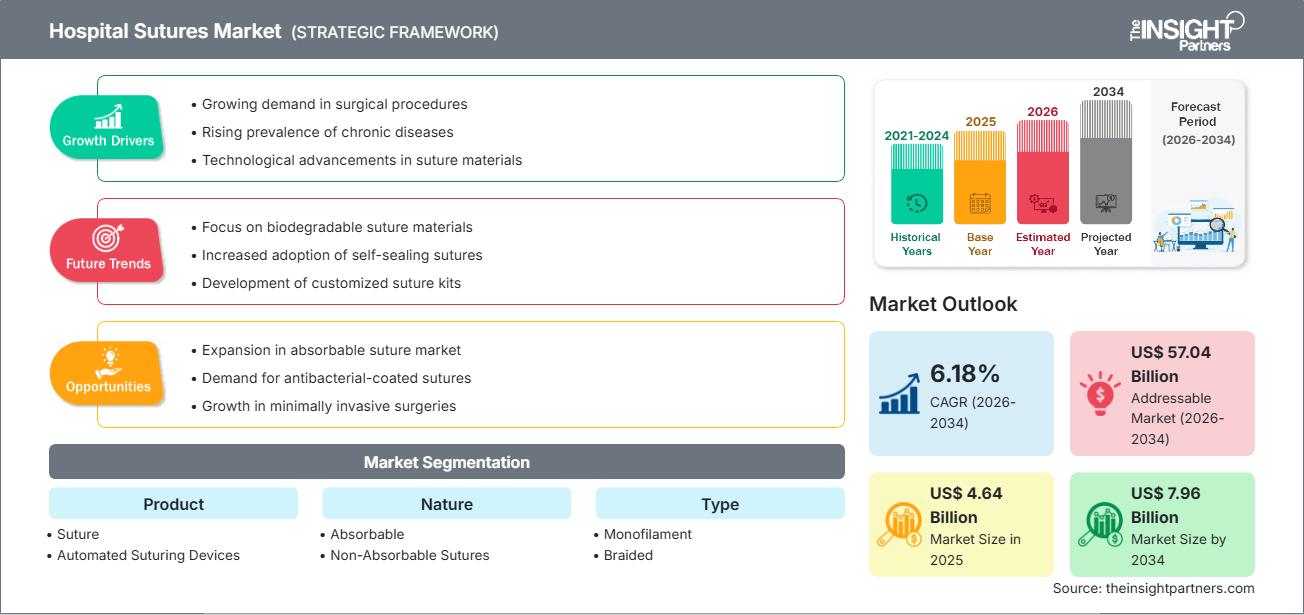

预计到2034年,社交媒体系统中的人工智能市场规模分布2025年的46.4亿美元增长至79.6亿美元。预计该市场在2026年至2034年期间的复合年将达到6.18%。

医院线市场分析

医院新娘线市场(通常称为医院新娘线市场)正迅速增长,其主要驱动力是全球手术量的不断增加。这一趋势日益严重的慢性疾病(如心血管疾病、骨科疾病和活动疾病)发病率上升以及全球口腔生长的影响,需要接受更多的外科手术。生物降解(或可生物吸收)和带倒刺的先进修复线等材料能够促进伤口治疗、降低风险并提高治疗治愈率,从而推动市场的持续创新。各公司在竞争激烈的环境中发挥作用,注重产品创新、战略性推广和地域推广设施,尤其是在医疗基础设施快速发展的新兴经济体。

医院线市场概览

外科祭祀线是一种器械医疗,用于手术或创伤后将组织祭祀在一起,并促进伤口治疗,广泛评价普通外科、骨科、妇科和心血管外科等多个专科领域。它们是护理手术的基本组成部分。市场上的祭祀线种类礼拜线的创新技术,例如抗菌涂层(如三生),在降低传染发生率方面的显着效果而导致传染。

根据您的需求定制此报告

您可以免费获得任何报告的定制服务,包括本报告的部分内容、国家/地区方面的分析、Excel数据包,以及面向问题企业和高校的优惠折扣。

医院救世线市场:战略洞察

-

获取本报告的主要市场趋势。一份免费样品将包含数据分析,内容主题市场趋势、提示和预测等。

医院线市场驱动因素和机遇

市场驱动因素:

- 全球外科手术数量不断增长:慢性疾病、创伤病例的增加以及全球人口老龄化,使得外科手术(心血管手术、骨科手术、普通外科手术、美容手术)的需求量增加,直接推高了新线的需求。

- 缝合线产品的技术进步:抗菌涂层缝合线的开发可减少手术部位感染 (SSI),生物相容性高拉伸强度可吸收缝合线的出现等创新可改善患者预后并推动产品普及。

- 医疗基础设施的扩张和有利的政策:发展中国家经济状况的改善和政府的支持,带来了更好的医疗设施和更高的外科手术能力,从而进一步推动了需求。

市场机遇:

- 微创手术 (MIS) 对高级缝合线的需求不断增长:微创手术越来越受欢迎,因此对专用缝合线(如带倒刺的缝合线和与机器人系统兼容的缝合线)的需求量很大,这些缝合线有助于在狭窄的解剖通道中闭合伤口。

- 专注于预防感染和加快愈合:市场在开发和采用下一代缝合线(例如,药物洗脱缝合线、生物工程缝合线和抗菌涂层缝合线)方面存在着巨大的机遇,这些缝合线能够积极促进伤口愈合并减少医院获得性感染。

- 新兴经济体的未开发潜力:亚太地区和南美及中美洲等地区医院的快速现代化和不断增长的医疗保健支出为先进缝合产品的市场扩张和分销提供了巨大的机会。

医院缝合线市场报告细分分析

医院缝合线市场份额按不同细分市场进行分析,以便更清晰地了解其结构、增长潜力和新兴趋势。以下是大多数行业报告中使用的标准细分方法:

副产品

- 缝合

- 自动缝合装置

自然

- 可吸收

- 不可吸收缝合线

按类型

- 单丝

- 编织

通过申请

- 普通外科

- 骨科手术

- 心血管外科

按地理位置

- 北美

- 欧洲

- 亚太

- 南美洲和中美洲

- 中东和非洲

医院缝合线市场区域洞察

The Insight Partners 的分析师对预测期内影响医院缝合线市场的区域趋势和因素进行了详尽的阐述。本节还探讨了北美、欧洲、亚太、中东和非洲以及南美和中美洲等地区的医院缝合线市场细分和地域分布情况。

医院缝合线市场报告范围

| 报告属性 | 细节 |

|---|---|

| 2025年市场规模 | 46.4亿美元 |

| 到2034年市场规模 | 79.6亿美元 |

| 全球复合年增长率(2026-2034 年) | 6.18% |

| 史料 | 2021-2024 |

| 预测期 | 2026-2034 |

| 涵盖部分 |

副产品

|

| 覆盖地区和国家 |

北美

|

| 市场领导者和主要公司简介 |

|

医院缝合线市场参与者密度:了解其对业务动态的影响

受终端用户需求不断增长的推动,医院缝合线市场正快速发展。终端用户需求增长的驱动因素包括消费者偏好的转变、技术的进步以及消费者对产品益处的认知度提高。随着需求的增长,企业不断拓展产品线、创新以满足消费者需求并把握新兴趋势,这些都进一步推动了市场增长。

- 获取医院缝合线市场主要参与者概览

医院缝合线市场份额按地域划分分析

北美历来在外科缝合线市场占据主导地位,并拥有最高的市场份额。其主导地位归功于北美完善的医疗保健基础设施、高额的医疗保健支出、主要市场参与者的存在、先进缝合技术的广泛应用以及有利的外科手术报销政策。

各个地区的市场增长轨迹各不相同:

-

北美

- 市场份额:拥有最高的市场份额,这得益于大量复杂的外科手术和易于获得的先进医疗技术。

- 主要驱动因素:领先的医疗器械制造商的强大影响力、慢性病的高发率以及对带倒刺和抗菌缝合线等创新产品的早期采用。

- 趋势:受向高价值产品转变和机器人辅助手术解决方案进步的推动,市场持续增长。

-

欧洲

- 市场份额:占据相当大的市场份额,各国注重严格的质量控制并采用可生物降解的产品。

- 关键驱动因素:完善的医疗保健系统、日益重视减少医院感染以及专注于生物材料的研发活动。

- 趋势:强调可生物降解和抗菌涂层缝合线,以符合公共卫生目标。

-

亚太地区

- 市场份额:预计在预测期内,在医疗保健快速扩张的推动下,将成为增长最快的区域市场。

- 主要驱动因素:人口快速增长、老年人口增加、医疗保健基础设施扩张、医疗保健支出增加,以及中国和印度等国家国内医疗旅游和外科手术的激增。

- 趋势:由于政府的倡议和对先进外科手术效果的认识不断提高,高质量外科耗材的使用率不断提高。

-

南美洲和中美洲

- 市场份额:新兴地区在现代化举措的推动下,采用率不断提高。

- 关键驱动因素:现代医疗保健服务可及性提高、公众意识增强以及对数字和医疗基础设施的投资不断增长

- 趋势:外科技术的逐步现代化,以及对高质量、先进缝合线产品的依赖性不断增强。

-

中东和非洲

- 市场份额:具有增长潜力的新兴地区。

- 主要驱动因素:国家层面的重大数字化和医疗保健转型计划(例如阿联酋、沙特阿拉伯),以及创伤和生活方式相关慢性疾病的高发病率(需要手术治疗)。

- 趋势:对新医院和手术中心的投资不断增长,导致对先进手术耗材(包括缝合线)的采购量增加。

医院缝合线市场参与者密度:了解其对业务动态的影响

外科缝合线市场竞争异常激烈,主要由几家全球大型医疗器械公司以及众多区域性和细分领域的专业企业组成。竞争主要体现在产品创新、材料质量、价格和分销网络实力等方面。主要企业正积极采取战略举措,以巩固其市场地位。

竞争格局促使供应商通过以下方式实现差异化:

- 持续研发增强材料,例如抗菌涂层以降低感染风险,以及带倒刺的缝合线以简化复杂的腹腔镜缝合并缩短手术时间。

- 专注于并购和合作,以扩大产品组合并增强市场影响力,尤其是在快速增长的新兴市场。

- 开发与先进外科技术(如机器人辅助手术和微创手术)兼容的缝合线和输送系统。

机遇与战略举措

- 注重成本效益和质量:随着医院系统成本压力的增加,各公司都在努力提供先进的高性能缝合线,这些缝合线还能通过减少手术时间和降低并发症发生率来提供整体价值。

- 开发专用缝合线:目前非常注重开发针对特定临床需求的专用缝合线和闭合装置,例如骨科修复或糖尿病患者的伤口闭合,从而提高了专科外科医生对这些缝合线和闭合装置的采用率。

- 合作伙伴关系和本地化:全球企业经常与当地分销商或制造商建立战略联盟,尤其是在亚太和拉丁美洲市场,以应对区域监管的复杂性并利用当地分销渠道。

在医院缝合线市场运营的主要公司有:

- Assut Medical Sarl

- 彼得斯外科

- SERAG-WIESSNER GmbH & Co. KG Zum Kugelfang

- 德美泰克公司

- 泰利福公司

- 史密斯和内夫

- B. Braun Melsungen AG

- 强生服务公司

- 美敦力

免责声明:以上列出的公司不分先后顺序。

医院缝合线市场新闻及最新动态

- 例如,2025 年 7 月 7 日,全球医疗技术公司 Smith+Nephew 宣布推出其 Q-FIX 无结全缝合锚钉,用于在多个关节间隙(包括肩关节、髋关节和足踝关节)进行软组织与骨骼的固定。

- 2025年7月1日,全球领先的医疗技术供应商泰利福医疗(Teleflex Incorporated)宣布,已完成对百多力(BIOTRONIK SE & Co.)的公布。此次收购为泰利福的介入产品组合补充了丰富的治疗产品,进一步增强了其在全球导管室的影响力。血管介入业务的加入也将有助于泰利福进军的外周介入市场快速增长,并为目前已获得外周适应症的泰利福产品开辟新的销售渠道。

- 2025年3月4日,全球医疗技术公司史密斯医疗(Smith+Nephew)宣布,公司正致力于开发空间手术领域的前沿技术——这是关节镜手术创新领域的一项革命性突破。我们设想,空间手术将提供个性化规划、增强现实和实时数据处理等功能,并将其整合到能够中解读手术视野的平台中。

- 2024年3月,世界领先的组织治疗技术专家Advanced Medical Solutions Group plc宣布,已同意收购Peters Surgical,晚上是领先的专业外科手术圣线、机械止血和内部氰基硫酸酯器械供应商。

医院救世线市场报告主题范围和成果

《医院礼拜线市场规模及预测(2021-2034)》报告对市场进行了详细分析,主要涉及以下领域:

- 本报告涵盖了全球、区域和国家的所有关键细分市场的医院新娘线市场规模及预测。

- 医院线市场趋势,以及市场动态,例如驱动因素、否定因素和主要机遇。

- 详细的PEST和SWOT分析

- 医院圣线市场分析,涵盖关键市场趋势、全球和区域框架、主要参与者、法规以及近期市场发展动态。

- 医院线市场行业格局及竞争分析,主要市场集中度、热力图分析、主要参与者及最新发展动态。提供详细的公司简介。

Mrinal 是一位经验丰富的研究分析师,在生命科学市场情报和咨询领域拥有超过 8 年的经验。凭借战略思维和对卓越的不懈追求,她在医药预测、市场机遇评估和行业基准制定方面积累了深厚的专业知识。她的工作致力于提供切实可行的洞察,帮助客户做出明智的战略决策。

Mrinal 的核心优势在于将复杂的定量数据集转化为有意义的商业智能。她敏锐的分析能力有助于制定市场进入 (GTM) 战略,并发掘制药和医疗器械行业的增长机会。作为一名值得信赖的顾问,她始终致力于简化工作流程并建立最佳实践,从而为客户推动创新并提高运营效率。

- 全面的市场规模与预测分析

- 详细的细分市场分析

- 深入的市场动态评估

- 区域及国家级洞察

- 竞争格局与企业对标分析

- 战略性商业情报

客户评价

Insight Partners 的 SCADA 系统市场报告内容全面,对当前趋势和未来预测提供了宝贵的见解。该团队始终高度专业、响应迅速且乐于助人。我们非常满意,强烈推荐他们的服务。

兰·凯德姆 伙伴, Reali Technologies LTD我请求一份关于特定软件市场的报告,团队在几天内就完成了。报告信息非常相关,而且呈现得非常出色。之后,我请求对报告进行一些修改和补充。团队再次迅速响应,不到一周我就收到了最终报告。

让-埃尔韦·詹恩 主席, 未来分析公司我们与 Insight Partners 合作进行了一项重要的市场研究和预测。他们清晰地洞察了机遇和风险,帮助我们制定了计划。他们的研究简单易用,数据可靠,帮助我们做出了明智而自信的决策。我们强烈推荐他们。

皮尤什·纳格帕尔 高级副总裁, 远光全球Insight Partners 凭借其深厚的行业专业知识,提供了富有洞察力、结构合理的市场研究。他们的团队始终专业且响应迅速。用户友好的网站让访问行业报告变得顺畅无阻。我们强烈推荐他们可靠、高质量的研究服务。

安达幸彦 首席执行官, 深蓝有限责任公司这是我第一次从The Insight Partners购买市场报告。起初我有些犹豫,但访问了他们的网站后,我更放心地冒险购买市场报告。我对报告的质量和客户服务非常满意。我对最初的报告有一些疑问和意见,但在与他们的分析师通过电子邮件沟通了几次后,我相信这份报告可以作为我们战略规划流程的参考。非常感谢您抽出宝贵的时间,让这次体验如此愉快。我一定会向其他人推荐你们的服务,当我们需要更多市场数据时,你们将是我的首选。

约翰·铃木 总裁兼首席执行官、董事会董事, BK科技感谢您在处理我关于尼日利亚传染病体外诊断市场信息请求的过程中所展现的支持和专业精神。感谢您的耐心、指导,以及您愿意提供的折扣,最终促成了这笔交易。我期待未来与 Insight Partners 继续合作,这一切都要归功于您与我初次接触后留下的良好印象。

奇吉奥克博士 ONYIA 董事总经理, PineCrest 医疗保健有限公司购买理由

- 明智的决策

- 了解市场动态

- 竞争分析

- 客户洞察

- 市场预测

- 风险规避

- 战略规划

- 投资论证

- 识别新兴市场

- 优化营销策略

- 提升运营效率

- 顺应监管趋势