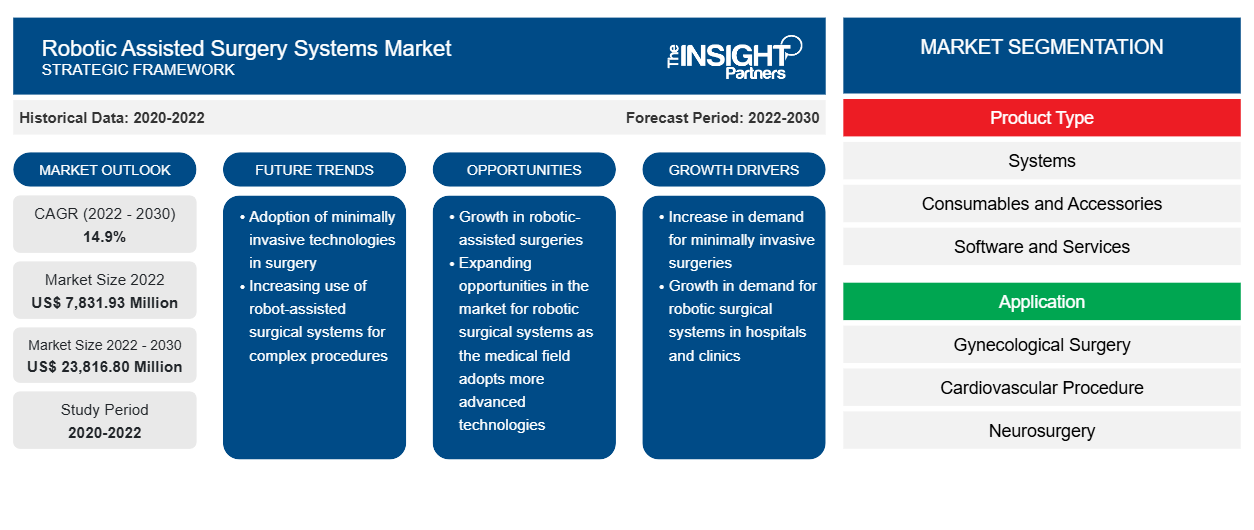

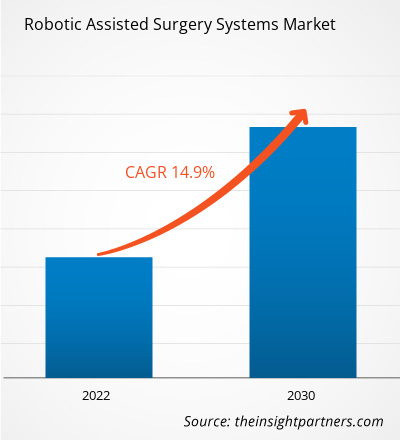

[تقرير بحثي] من المتوقع أن ينمو حجم سوق أنظمة الجراحة بمساعدة الروبوتات من 7،831.93 مليون دولار أمريكي في عام 2022 إلى 23،816.80 مليون دولار أمريكي بحلول عام 2030؛ ومن المتوقع أن يسجل السوق معدل نمو سنوي مركب بنسبة 14.9٪ من عام 2022 إلى عام 2030.

رؤى السوق ووجهة نظر المحلل:

يشتمل سوق أنظمة الجراحة بمساعدة الروبوتات على مجموعة من المنصات الجراحية المتقدمة تقنيًا والتي تدمج الروبوتات وأنظمة التصوير والملاحة لمساعدة الجراحين في إجراء العمليات الجراحية الأقل توغلاً بدقة وتحكم متزايدين. تم تصميم هذه الأنظمة لتعزيز القدرات الجراحية وتحسين نتائج المرضى وتقليل تدخل التقنيات الجراحية التقليدية. تشمل الفوائد الجديرة بالملاحظة لأنظمة الجراحة بمساعدة الروبوتات تحسين البراعة والتصور ثلاثي الأبعاد وتصفية الرعشة، مما يسمح للجراحين بإجراء عمليات معقدة بدقة فائقة وسهولة في المناورة. غالبًا ما تمكنهم هذه الأنظمة من الوصول إلى المناطق التشريحية التي يصعب الوصول إليها، مما يؤدي إلى تقليل الصدمات وأوقات تعافي المريض بشكل أسرع. بالإضافة إلى ذلك، يقلل دمج الروبوتات في العمليات الجراحية من خطر حدوث المضاعفات ويقلل من الحاجة إلى نقل الدم، مما يساهم في النهاية في تحسين نتائج ما بعد الجراحة.

محركات النمو والتحديات:

من المتوقع أن يؤدي العدد المتزايد من الدراسات البحثية التي تستكشف فوائد وقدرات العمليات الجراحية بمساعدة الروبوتات إلى تعزيز تقدم السوق في السنوات القادمة. في سبتمبر 2022، أجرى فريق من كلية الدراسات العليا للعلوم الطبية بجامعة مدينة ناغويا (NCU)، دراسة قارنت بين الوصول إلى الكلى بمساعدة الروبوتات والموجه بالفلوروسكوب والموجه بالموجات فوق الصوتية لاستخراج حصوات الكلى عن طريق الجلد. توضح نتائج الدراسة سلامة وسهولة استخدام الأجهزة الروبوتية الثورية، والتي قد تخفف من عبء التدريب على الجراحين وتمكن المزيد من المستشفيات من إجراء عمليات PCNL. قد تفتح هذه الطريقة، التي تستخدم الروبوتات التي يقودها الذكاء الاصطناعي ، الباب أمام أتمتة التدخلات الجراحية المماثلة، مما يؤدي بدوره إلى تسريع العملية وتقليل خطر حدوث مضاعفات.

إن ارتفاع حالات الأمراض المزمنة والشعبية المتزايدة للجراحات الأقل توغلاً يعززان سوق أنظمة الجراحة بمساعدة الروبوتات. وفقًا للأخبار التي نشرتها صحيفة The Hindu في أغسطس 2022، أكملت Apollo Health City في حيدر أباد بالهند أكثر من 500 عملية جراحية في أمراض النساء بمساعدة الروبوتات. في نوفمبر 2022، أعلنت India Medtronic Private Limited، وهي شركة تابعة مملوكة بالكامل لشركة Medtronic plc، ومستشفى Venkateshwar في دلهي عن إكمال أول علاج للمسالك البولية في شمال الهند بنظام الجراحة بمساعدة الروبوت Hugo (RAS).

من ناحية أخرى، تعيق التكلفة العالية لأنظمة الجراحة الروبوتية الجدوى المالية والاستدامة التشغيلية لمقدمي الرعاية الصحية. وفي حين توفر هذه الأنظمة مزايا مثل الدقة المحسنة، والحد الأدنى من التدخل الجراحي، وتقليص أوقات تعافي المريض، فإن الاستثمار الأولي الكبير وتكاليف الصيانة المستمرة تتطلب التخطيط المالي الدقيق وتخصيص الموارد لمرافق الرعاية الصحية. بالإضافة إلى ذلك، تضيف الحاجة إلى التدريب المتخصص وإصدار الشهادات للعاملين الجراحيين لتشغيل هذه الأنظمة المزيد من التكاليف التشغيلية، مما يؤثر على القدرة على تحمل التكاليف الإجمالية والعملية لدمج الجراحة الروبوتية في الممارسات السريرية الحالية. إن العبء المالي المرتبط بأنظمة الجراحة الروبوتية لديه القدرة على التأثير على نماذج سداد الرعاية الصحية وقرارات التغطية. قد تختلف معدلات السداد للإجراءات التي يتم إجراؤها بمساعدة الروبوت، وقد تؤثر التغطية من قبل مقدمي التأمين على الأساس الاقتصادي لتبني هذه التقنيات. وهذا يخلق مشهدًا معقدًا حيث تحتاج مرافق الرعاية الصحية إلى موازنة المزايا السريرية للجراحة الروبوتية مقابل العواقب المالية، مما قد يؤثر على وتيرة ونطاق التبني عبر أنظمة الرعاية الصحية المختلفة.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق أنظمة الجراحة بمساعدة الروبوتات:

- احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

تقسيم التقرير ونطاقه:

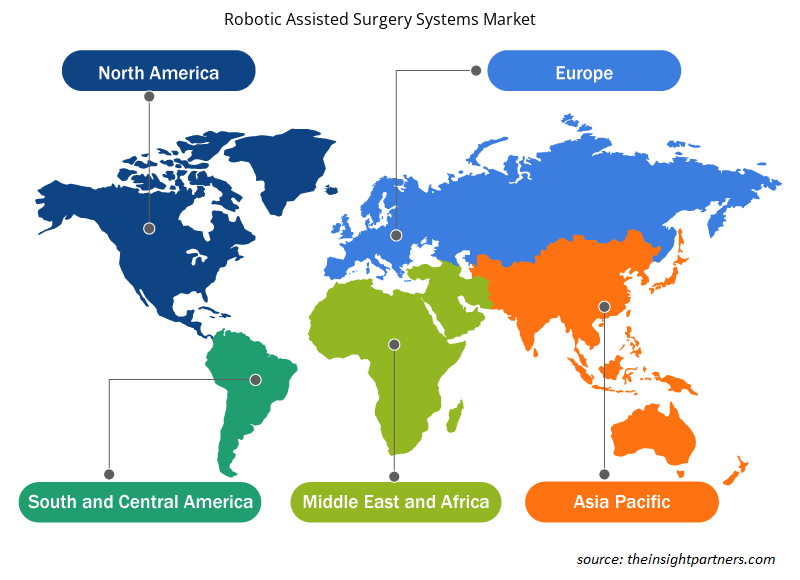

يتم تقسيم سوق أنظمة الجراحة بمساعدة الروبوتات على أساس نوع المنتج والتطبيق والمستخدم النهائي. بناءً على نوع المنتج، يتم تقسيم السوق إلى أنظمة وأدوات وملحقات وخدمات. حسب التطبيق، يتم تقسيم سوق أنظمة الجراحة بمساعدة الروبوتات إلى جراحة أمراض النساء، وأمراض القلب والأوعية الدموية، وجراحة الأعصاب، وجراحة العظام، والتنظير البطني، وجراحة المسالك البولية، والجراحة العامة، وغيرها. يتم تصنيف السوق، بناءً على المستخدم النهائي، إلى مستشفيات ومراكز جراحة العيادات الخارجية ومستخدمين نهائيين آخرين. من حيث الجغرافيا، يتم تقسيم سوق أنظمة الجراحة بمساعدة الروبوتات إلى أمريكا الشمالية (الولايات المتحدة وكندا والمكسيك)، وأوروبا (المملكة المتحدة وألمانيا وفرنسا وإيطاليا وإسبانيا وبقية أوروبا)، وآسيا والمحيط الهادئ (الصين واليابان والهند وكوريا الجنوبية وأستراليا وبقية آسيا والمحيط الهادئ)، والشرق الأوسط وأفريقيا (الإمارات العربية المتحدة والمملكة العربية السعودية وجنوب إفريقيا وبقية الشرق الأوسط وأفريقيا)، وأمريكا الجنوبية والوسطى (البرازيل والأرجنتين وبقية أمريكا الجنوبية والوسطى).

التحليل القطاعي:

استنادًا إلى نوع المنتج، استحوذ قطاع الروبوتات الجراحية على حصة كبيرة من إيرادات سوق أنظمة الجراحة بمساعدة الروبوتات في عام 2022. ومن المتوقع أن تزداد الحاجة إلى الروبوتات الجراحية لإجراء عمليات دقيقة وصحيحة بسبب الارتفاع العالمي في حالات الإصابة بأمراض القلب والأوعية الدموية والسرطان. ومن المتوقع أن تبلغ الولايات المتحدة عن 1.9 مليون حالة إصابة جديدة بالسرطان في عام 2023، وفقًا لإحصاءات السرطان لعام 2023 الصادرة عن الجمعية الأمريكية للسرطان. ووفقًا لتقرير المعهد الأسترالي للصحة والرفاهية لعام 2021، فإن حالات الإصابة الجديدة بالسرطان المقدرة في أستراليا في عام 2021 كانت 150800 حالة. ويذكر تقرير مارس 2022 الصادر عن المكتب الأسترالي للإحصاء أن 4.0٪ من الأستراليين، أو 1.0 مليون شخص، من المقدر أن يكونوا مصابين بأمراض القلب في عام 2021.

بناءً على التطبيق، يتم تصنيف سوق أنظمة الجراحة بمساعدة الروبوت إلى جراحة أمراض النساء، وأمراض القلب والأوعية الدموية، وجراحة الأعصاب، وجراحة العظام، والتنظير البطني، وجراحة المسالك البولية، والجراحة العامة، وغيرها. ومن المتوقع أن يسجل قطاع طب الأعصاب أسرع معدل نمو سنوي مركب خلال الفترة 2022-2030. إن الاستخدام المتزايد للروبوتات الجراحية في الجراحات العامة والفوائد التي تقدمها مقارنة بالطرق الجراحية التقليدية تفيد السوق بشكل عام. علاوة على ذلك، من المتوقع أن تعمل التحسينات في التكنولوجيا والنتائج الناجحة لجراحة الأعصاب الروبوتية على دفع توسع سوق أنظمة الجراحة بمساعدة الروبوت في السنوات القادمة. وفقًا لشركة SS Innovations Interventional Inc.، تم إجراء ما يقرب من 1.6 مليون عملية جراحية روبوتية على مستوى العالم في عام 2020.

من حيث المستخدم النهائي، يتم تقسيم سوق أنظمة الجراحة بمساعدة الروبوت إلى المستشفيات ومراكز الجراحة الخارجية والمستخدمين النهائيين الآخرين. هيمن قطاع المستشفيات على السوق في عام 2022 ومن المتوقع أن يسجل معدل نمو سنوي مركب مرتفع خلال الفترة 2022-2030. يُعزى نمو سوق قطاع المستشفيات إلى ارتفاع تكاليف الرعاية الصحية في العديد من الاقتصادات. توفر المستشفيات جودة رعاية فائقة من خلال استخدام أحدث المعدات الجراحية بمساعدة الروبوت. علاوة على ذلك، يفضل الأطباء والجراحون الأنظمة التي تعمل بمساعدة الروبوت. ارتفع استخدام العمليات بمساعدة الروبوت في الإجراءات الجراحية الإجمالية عدة مرات من 1.8٪ في عام 2013 إلى 15.1٪ في عام 2019، وفقًا لورقة بحثية نُشرت في شبكة JAMA.

التحليل الإقليمي:

بناءً على الجغرافيا، ينقسم سوق أنظمة الجراحة بمساعدة الروبوتات إلى أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى. أمريكا الشمالية هي المساهم الأكثر أهمية في نمو هذا السوق. يُعزى تقدم السوق في هذه المنطقة إلى الاستخدام المتزايد للأدوات الجراحية الآلية وتبني أنظمة الرعاية الصحية من الجيل التالي في الولايات المتحدة. علاوة على ذلك، من المتوقع أن يفيد نقص الجراحين والمتخصصين الطبيين في الولايات المتحدة مقارنة بعدد المرضى سوق أنظمة الجراحة بمساعدة الروبوتات. إن الانتشار المتزايد للأمراض المزمنة مثل مرض السكري والسرطان وأمراض القلب والأوعية الدموية يدفع الطلب على أنظمة الجراحة بمساعدة الروبوتات في الولايات المتحدة.

إن الشعبية المتزايدة للإجراءات الجراحية الأقل توغلاً مقارنة بالعمليات الجراحية التقليدية تصب في صالح سوق أنظمة الجراحة بمساعدة الروبوتات. في ديسمبر 2022، وسعت شركة هوغو التجارب السريرية لأنظمة الجراحة بمساعدة الروبوتات (RAS) في الولايات المتحدة من خلال تسجيل أول مريض لها، وفقًا لشركة ميدترونيك. علاوة على ذلك، في عام 2022، أجرى طبيب في مستشفى جامعة ديوك في دورهام بولاية نورث كارولينا عملية استئصال البروستاتا بمساعدة الروبوتات.

من المتوقع أن ينمو سوق أنظمة الجراحة بمساعدة الروبوتات في منطقة آسيا والمحيط الهادئ بأسرع معدل نمو سنوي مركب خلال الفترة 2022-2030 بسبب النمو السكاني للمرضى والاستخدام المتزايد للأدوات الجراحية الآلية المتطورة. بالإضافة إلى ذلك، من المتوقع أن يستفيد نمو السوق في هذه المنطقة في المستقبل من توسيع مرافق الرعاية الصحية المعاصرة وزيادة الوعي العام بمزايا التقنيات الطبية المتطورة. تحاول حكومات الدول في منطقة آسيا والمحيط الهادئ إنشاء بنية تحتية متطورة للرعاية الصحية، مما يجذب الشركات الدولية للاستثمار في إنشاء مرافق تطوير الأدوات الآلية في هذه المنطقة. تمتلك الصين أكبر حصة في سوق أنظمة الجراحة بمساعدة الروبوتات في منطقة آسيا والمحيط الهادئ، ومن المتوقع أن تسجل الهند أعلى معدل نمو سنوي مركب خلال الفترة 2022-2030. اختصرت الشركات العاملة في مجال الروبوتات الجراحية في الصين وقت طرحها في السوق من خلال الاستفادة من مسار الموافقة الخاص الذي يسرع الموافقة التنظيمية على المنتجات الطبية المبتكرة. علاوة على ذلك، ينشأ عدد متزايد من شركات التكنولوجيا الطبية المتخصصة في الروبوتات الجراحية في البلاد. في السنوات الأخيرة، دخلت شركة JianJia Robots وHurwa السوق الصينية لتطوير حلول الروبوتات الجراحية جنبًا إلى جنب مع شركة TINAVI، وهي شركة محلية متخصصة في الروبوتات الجراحية العظمية. تسدد بكين تكاليف جراحات العمود الفقري والورك والركبة بمساعدة الروبوتات لشركة TINAVI.

رؤى إقليمية حول سوق أنظمة الجراحة بمساعدة الروبوتات

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق أنظمة الجراحة بمساعدة الروبوتات طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق أنظمة الجراحة بمساعدة الروبوتات والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق أنظمة الجراحة بمساعدة الروبوت

نطاق تقرير سوق أنظمة الجراحة بمساعدة الروبوت

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2022 | 7,831.93 مليون دولار أمريكي |

| حجم السوق بحلول عام 2030 | 23,816.80 مليون دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2022 - 2030) | 14.9% |

| البيانات التاريخية | 2020-2022 |

| فترة التنبؤ | 2022-2030 |

| القطاعات المغطاة | حسب نوع المنتج

|

| المناطق والدول المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

كثافة اللاعبين في سوق أنظمة الجراحة بمساعدة الروبوتات: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق أنظمة الجراحة بمساعدة الروبوتات نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلكين المتطورة والتقدم التكنولوجي والوعي الأكبر بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق أنظمة الجراحة بمساعدة الروبوتات هي:

- شركة الجراحة البديهية

- شركة سترايكر

- شركة جونسون آند جونسون

- شركة اس ار اي الدولية

- شركة أكوراي المحدودة

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق أنظمة الجراحة بمساعدة الروبوتات

تطورات الصناعة والفرص المستقبلية:

فيما يلي قائمة بالمبادرات المختلفة التي اتخذها اللاعبون الرئيسيون العاملون في سوق أنظمة الجراحة بمساعدة الروبوتات العالمية:

- في أكتوبر 2023، قدمت شركة Johnson & Johnson MedTech، وهي شركة متخصصة في جراحة العظام تابعة لشركة DePuy Synthes، حل VELYS Robotic Assisted Solution. وقد تم استخدام الحل في عمليات استبدال الركبة بالكامل في ألمانيا وبلجيكا وسويسرا. ومن خلال هذا الإطلاق، تعمل شركة DePuy Synthes على توسيع التقنيات المتصلة بالشبكة داخل منصة الجراحة الرقمية الخاصة بها لتلبية الطلبات غير الملباة على الروبوتات العظمية.

- في نوفمبر 2022، دخلت شركة هندية تعمل في مجال التكنولوجيا الطبية في شراكة مع شركة Avra Medical Robotics، وهي شركة أمريكية مدرجة في بورصة ناسداك. وقد طرحت شركة SS Innovations أول روبوت جراحي "صُنع بالكامل في الهند"، وهو SSI Mantra. وهو نظام روبوتي جراحي متطور للغاية يتمتع بقدرات وتطبيقات أكثر من الأنظمة الأخرى الموجودة في السوق.

- في نوفمبر 2022، وافقت إدارة الغذاء والدواء الأمريكية في الولايات المتحدة على تحديث برنامج Accelus لنظام Remi Robotic Navigation System، والذي يسمح للجراحين الذين يقومون بتثبيت العمود الفقري القطني بوضع مسامير السويقة بمساعدة الروبوت. Accelus هي شركة تكنولوجيا طبية خاصة تركز على اعتماد الجراحة الأقل توغلاً (MIS) كمعيار للرعاية في العمود الفقري.

المنافسة والشركات الرئيسية:

تعد شركات Intuitive Surgical Inc. وStryker Corporation وJohnson & Johnson Inc. وSRI International Inc. وAccuray Incorporated وRenishaw PLC وMedtronic PLC وBrainlab وSmith & Nephew PLC وGlobus Medical وZimmer Biomet من بين أبرز الشركات في سوق أنظمة الجراحة بمساعدة الروبوتات. تركز هذه الشركات على توسيع عروضها لتلبية الطلب المتزايد من المستهلكين في جميع أنحاء العالم. يسمح لها وجودها العالمي بخدمة مجموعة كبيرة من العملاء، مما يسمح لها لاحقًا بتوسيع حصتها في السوق.

- التحليل التاريخي (سنتان)، السنة الأساسية، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالميًا وإقليميًا وقطريًا

- الصناعة والمنافسة

- مجموعة بيانات Excel

- Green Hydrogen Market

- Analog-to-Digital Converter Market

- Vision Care Market

- Organoids Market

- Military Rubber Tracks Market

- Machine Condition Monitoring Market

- Artificial Intelligence in Healthcare Diagnosis Market

- Ceramic Injection Molding Market

- Human Microbiome Market

- Biopharmaceutical Contract Manufacturing Market

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

الأسئلة الشائعة

The robotic assisted surgery systems market has major market players, including Intuitive Surgical Inc., Stryker Corporation, Johnson & Johnson Inc., SRI International Inc., Accuray Incorporated, Renishaw PLC, Medtronic PLC, Brainlab, Smith & Nephew PLC, Globus Medical, and Zimmer Biomet.

Based on product type, the surgical robot segment held a substantial revenue share of the robotic assisted surgery systems market in 2022. The need for surgical robots to perform precise and accurate procedures is predicted to increase due to the surging global incidence of cardiovascular and cancer disorders. The US is expected to report 1.9 million new cancer cases in 2023, according to the American Cancer Society's Cancer Statistics 2023. As per the Australian Institute of Health and Welfare's (AIHW) 2021 report, the estimated new cases of cancer in Australia in 2021 were 150,800. The March 2022 report from the Australian Bureau of Statistics states that 4.0% of Australians, or 1.0 million people, were estimated to have heart disease in 2021.

Growing preference for robotically assisted treatments, rising inclination toward minimally invasive surgeries, and the increasing number of product launches are the key factors driving the robotic assisted surgery systems market progress. However, the stringent regulatory processes and high cost of devices hinder the robotic assisted surgery systems market growth.

The robotic assisted surgery systems market was valued at US$ 7,831.93 million in 2022.

The robotic assisted surgery systems market is expected to be valued at US$ 23,816.80 million in 2030.

The robotic assisted surgery systems market encompasses an array of technologically advanced surgical platforms that integrate robotics, imaging, and navigation systems to assist surgeons in performing minimally invasive procedures with increased precision and control. These systems are designed to enhance surgical capabilities, improve patient outcomes, and minimize the invasiveness of traditional surgical techniques.

Based on application, the robot-assisted surgical systems market is classified into gynecological surgery, cardiovascular, neurosurgery, orthopedic surgery, laparoscopy, urology, general surgery, and others. The neurology sector is expected to record the fastest CAGR during 2022–2030. The increasing usage of surgical robots in general surgeries and the benefits they offer over conventional surgical methods benefit the overall market. Furthermore, improvements in technology and the successful results of robotic neurosurgery are anticipated to propel the expansion of the robot-assisted surgical systems market in the coming years. According to SS Innovations Interventional Inc., approximately 1.6 million robotic surgeries were performed globally in 2020.

The List of Companies - Robotic Assisted Surgery Systems Market

- Intuitive Surgical Inc.

- Stryker Corporation

- Johnson & Johnson Inc.

- SRI International Inc.

- Accuray Incorporated

- Renishaw PLC

- Medtronic PLC

- Brainlab

- Smith & Nephew PLC

- Globus Medical

- Zimmer Biomet

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

احصل على عينة مجانية لهذا التقرير

احصل على عينة مجانية لهذا التقرير