Automotive Body-in-White Market Outlook and Strategic Insights by 2025

Published Report - Automotive Body-in-White Market to 2025 - Global Analysis and Forecast by Material Type (Aluminium, Steel, Magnesium and CFRP), Component Position (Structural, Inner and Exposed), Component Types (Fenders, Closures, Shock Towers, A-Post/ B-Post, and Others), and Body Structure (Frame Mounted Structure and Monocoque Structure)

- Status : Published

- Report Code : TIPAR100000560

- Category : Automotive and Transportation

- No. of Pages : 156

- Available Report Formats :

- Last update date : June 11, 2024

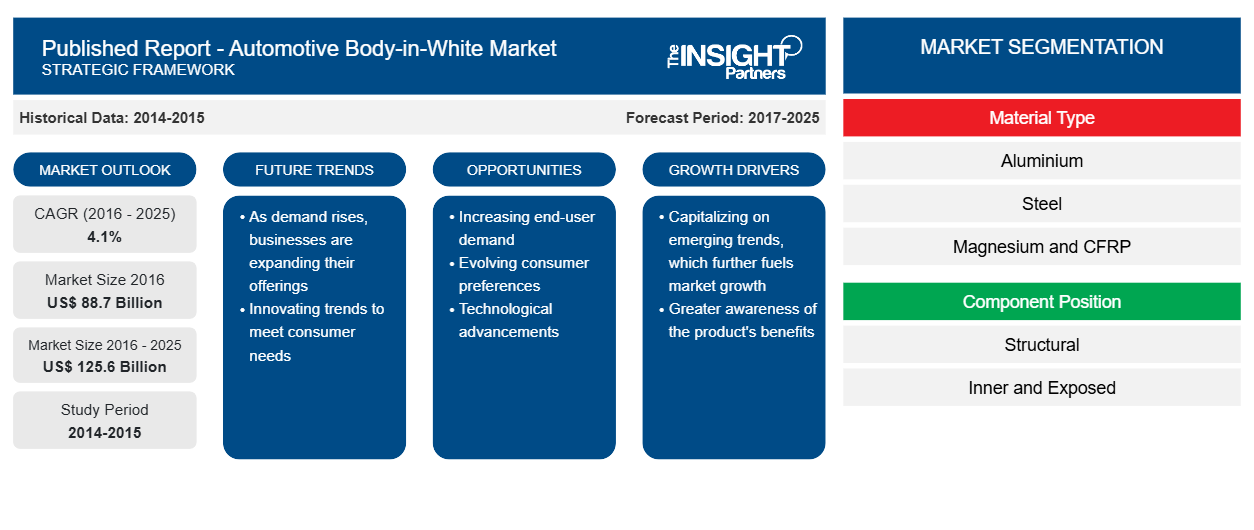

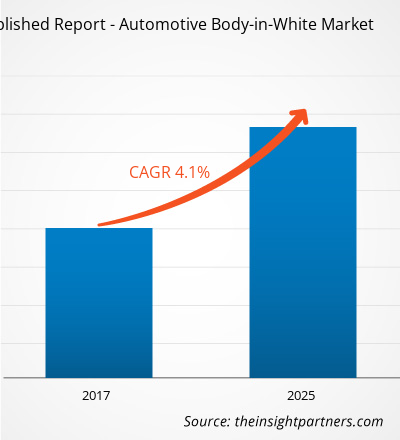

2016 Market Size

US$ 88.7 Bn

Base year value

2025 Forecast

US$ 125.6 Bn

Projected by 2025

CAGR 2017-2025

4.1 %

Growth rate

Addressable Market

US$ 981.19 Bn

(2017-2025)

[Research Report] The Automotive Body-In-White Component market was valued at US$ 88.7 Bn in 2016 and is projected to reach US$ 125.6 Bn by 2025; it is expected to grow at a CAGR of 4.1% from 2017 to 2025.

The automotive BIW component market has experienced significant growth rate owing to increasing vehicle production in the region. The BIW components accounts for 20 – 33 % of curb weight of the vehicle and therefore represents high revenue potential for component suppliers across the automotive value chain. Despite disruptions in the automotive sector such as evolution of electric / hybrid vehicle, development of driverless and connected vehicles, BIW components is invariable segment of automotive sector and therefore associated as the major business segment in overall automotive industry. With wide variety of material availed for vehicle production, selection of material depends on economic effectiveness, lightweight, safety characteristics, volume production and life cycle considerations. Only a handful of players dominate the global BIW component market owing to high investments, enhanced R&D capabilities, and strong supplier relationships among others. The automotive BIW component market is in line with production of automotive vehicle. Further, BIW component including chassis is estimated to register value of US$ 1,300 per vehicle globally. This number is further expected to increase in the future owing to adoption of high costs material and superior manufacturing techniques for vehicle production. Adoption of high cost material is primarily driven by stringent emission and fuel efficiency regulations globally.

Asia Pacific includes countries such as India, China, Japan, and South Korea. This region accounted for over 58% of the global automotive BIW component market owing to the presence of prominent vehicle manufacturing countries such as China, japan and South Korea. Production of passenger cars in China grew at around 15% over the previous year. Major global OEMs are in a bid to open manufacturing facilities in India and China owing to the availability of cheap labor, raw materials, and favorable government regulations. Price of raw material to produce different materials such as steel, aluminum, magnesium is much minor than other regions of the world. This has welcomed OEMs around the world to set up their manufacturing unit in the Asia Pacific region. Presence of global suppliers across these countries contributes only 1 – 15 % of the total supply with regional / specialized players sharing lion’s share. Moreover, these countries together contribute 53.1 % of the global passenger car production in 2016 and is expected to remain dominant over the forecast period. Low penetration of global suppliers in the countries combined with high vehicle production creates significant opportunity for international players to win larger pie of the market.,

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Published Report - Automotive Body-in-White Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Market Insights

Robust growth in passenger car production globally is fueling the revenue growth

The global passenger car production has grown at a CAGR of 3.8% in the last five years to reach 72.1 Mn units in 2016 according to the International Organization of Motor Vehicle Manufacturers. Supported by the large, growing vehicle consumers, this growth rate is expected to be double by 2025. The BIW components account for 22-33% of the total vehicle mass and contributes to an estimated value of US$ 1,300 per vehicle. Taken together, the significant value contribution of BIW components per vehicle and robust growth in vehicle production will greatly drive the revenue growth in the global automotive BIW component market.

Material Type-Based Market Insights

The global automotive BIW component market by material type is broadly segmented into four categories steel, aluminum, magnesium and CFRP. Each of the material used in the manufacture of BIW component has its own set of advantages and disadvantages. While the steel is the favored material prevalent since quite few years, aluminum has taken up pace off late and is expected to outpace all other material because various benefits it offers over other material.

Component -Based Market Insights

The global automotive BIW market by component type is broadly segmented into three categories structural, inner, and exposed. Structural components generally form the main structure or chassis of the vehicle. These components must be rigid and strong to support the overall structure of the vehicle’s body. These components form an integral part of the chassis and generally includes crumple zones or force absorption zones for safety. It is expected that around 65% of the BIW structural components are outsourced in the Europe, North and South America region and around 25% are outsourced in the APAC and MEA region in the year 2016.

Body Structure – Based Market Insights

The global automotive BIW component market by body structure is broadly segmented into two categories monocoque and frame mounted. Monocoque body structure is likely hold the prime market share in 2016 and is expected to grow at a lightening CAGR over the forecast period as compared to frame mounted body structure. Owing to added safety and light-weightiness of monocoque structure over ladder frame structure is primarily pushing the vehicle manufacturers to adopt it over traditional ladder frame structure. Safety standards such as Euro NCAP ratings have made it mandatory to add crumple zones at the front and the back of vehicles has also encouraged OEMs to adhere the monocoque body structure.

Product development is the commonly adopted strategy by companies to expand their product portfolio. Magna International, Gestamp Services, Benteler International AG, ThyssenKrupp Systems Engineering, Santec Group, Schuler Group, Orchid International, Hyundai Rotem, Aida Global, Texas Instruments Incorporated, among others are the key players implementing strategies to enlarge the customer base and gain significant share in the global Automotive Body-In-White Component market, which in turn permits them to maintain their brand name. A few of the recent key developments are:

- In 2017, Gestamp recently opened its new R&D centre in Japan, which will be equipped with simulation resources, and advanced simulation of hot stamping process..

- In 2017, Benteler inaugurated its new sales and service location in Coventry, England. This expansion is aimed to build strong presence in key markets and close collaboration on excellent products and services.

Automotive Body-in-White

Published Report - Automotive Body-in-White Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2016 | US$ 88.7 Billion |

| Market Size by 2025 | US$ 125.6 Billion |

| Global CAGR (2016 - 2025) | 4.1% |

| Historical Data | 2014-2015 |

| Forecast period | 2017-2025 |

| Segments Covered |

By Material Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Published Report - Automotive Body-in-White Market Players Density: Understanding Its Impact on Business Dynamics

The Published Report - Automotive Body-in-White Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Automotive Body-In-White Component Market Segmentation:

By Material Type

- Steel

- MS

- HSS

- AHSS

- UHSS

- Aluminium

- Magnesium

- CFRP

By Components Position

- Structural

- Inner

- Exposed

By Component Type

- Fenders

- Closures

- Shock Towers

- A-Post / B-Post

- Others

Company Profiles

- Magna International

- Gestamp Services

- Benteler International AG

- ThyssenKrupp Systems Engineering

- Santec Group

- Schuler Group

- Orchid International

- Hyundai Rotem

- Aida Global

- Texas Instruments Incorporated

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends