Marktstrategien für Luftstromsensoren, Top-Player, Wachstumschancen, Analyse und Prognose bis 2030

Marktgröße und Prognose für Luftstromsensoren (2020 – 2030), Bericht über globale und regionale Anteile, Trends und Wachstumschancenanalyse: Nach Typ (Volumen-Luftstromsensoren und Massen-Luftstromsensoren), Ausgangssignal (analog und digital) und Anwendung (Automobilindustrie, Luft- und Raumfahrt, Fertigung, Energie- und Versorgungsunternehmen und andere) sowie Geografie

- Status : Veröffentlicht

- Berichtscode : TIPRE00002807

- Kategorie : Elektronik und Halbleiter

- Anzahl der Seiten : 158

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : August 26, 2024

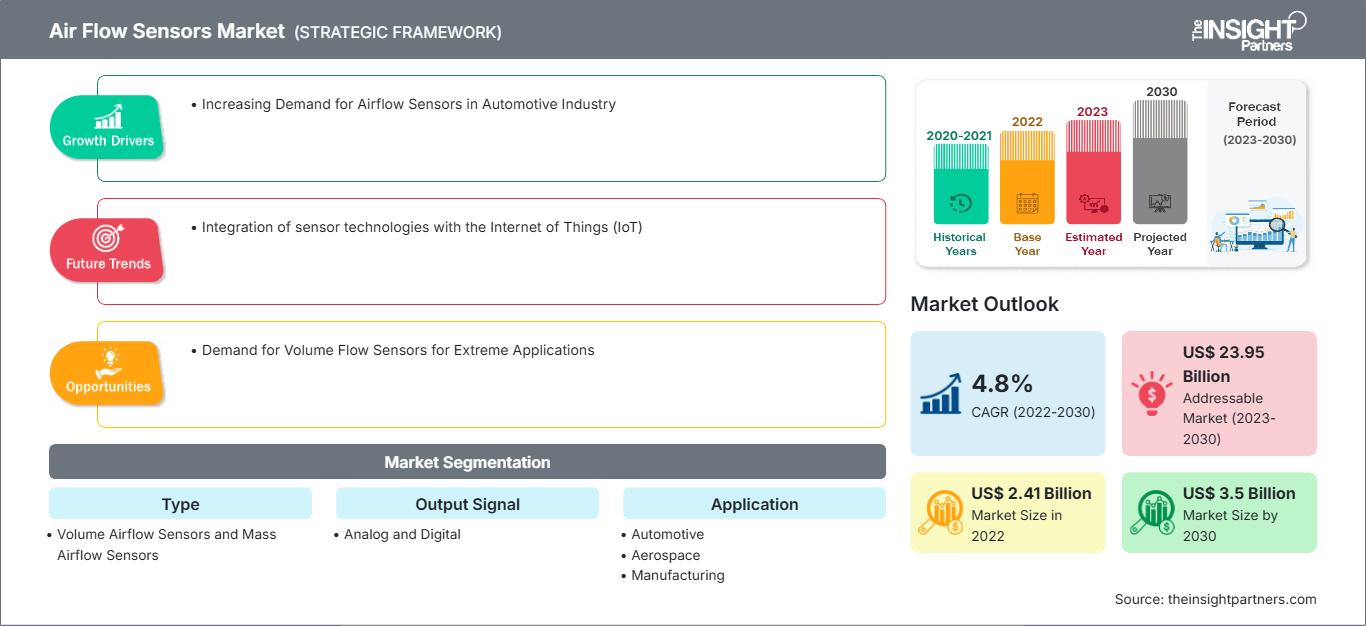

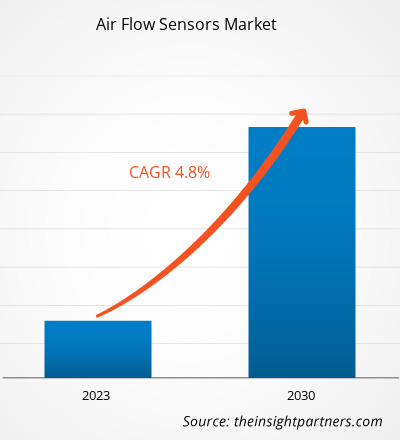

Der Markt für Luftstromsensoren soll von 2,41 Milliarden US-Dollar im Jahr 2022 auf 3,50 Milliarden US-Dollar im Jahr 2030 anwachsen. Für den Zeitraum 2022–2030 wird ein durchschnittliches jährliches Wachstum (CAGR) von 4,8 % erwartet. Die Integration von Sensortechnologien in das Internet der Dinge (IoT) wird voraussichtlich ein wichtiger Markttrend bleiben.

Marktanalyse für Luftstromsensoren

HLK-Systeme verwenden Luftstromsensoren, um einen effizienten Betrieb zu gewährleisten und den Energieverbrauch zu senken. HLK-Systeme verfügen über Luftstromsensoren, die es ihnen ermöglichen, die tatsächliche Temperatur eines Bereichs mit einer Zieltemperatur zu vergleichen und entsprechende Maßnahmen zu ergreifen. HLK-Steuerungen werden häufig in verschiedenen Geschäftsbereichen eingesetzt, darunter im Gastgewerbe, in Unternehmen, im Einzelhandel und im Wohnbereich.

Marktübersicht für Luftstromsensoren

Luftstromsensoren werden verwendet, um das Volumen oder die Masse des Luftstroms in einem Kanal zu bestimmen. Es gibt zwei Kategorien von Luftstromsensoren: Massen-Luftstromsensoren und Volumen-Luftstromsensoren. Luftstromsensoren sind einfach zu installieren und messen den Gesamtdruck, den statischen Druck des Luftstroms und die Luftgeschwindigkeit. Luftstromsensoren finden Anwendung in zahlreichen Industriesystemen. In Kraftfahrzeugen sind Luftstromsensoren entscheidend für die Aufrechterhaltung optimaler Kraftstoffeffizienz und Emissionswerte und unterstützen das Motorsteuergerät bei der Anpassung der Kraftstoffeinspritzung, um eine effiziente Verbrennung zu gewährleisten.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für Luftstromsensoren: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

Markttreiber und -chancen für Luftstromsensoren

Steigende Nachfrage nach Luftstromsensoren in der Automobilindustrie begünstigt den Markt

Die Automobilindustrie ist ein wichtiger Endverbraucher von Luftstromsensoren. Die steigende Nachfrage nach Kraftfahrzeugen treibt gleichzeitig den Bedarf an Luftstromsensoren voran, da diese Sensoren in Motoren und Abgassystemen zur Überwachung und Steuerung des Luftstroms eingesetzt werden. Die Automobilindustrie wächst weltweit rasant. Auch die Verbreitung von Elektrofahrzeugen nimmt weltweit deutlich zu. Laut der Europäischen Kommission bietet die Automobilindustrie 13,8 Millionen Europäern direkte und indirekte Arbeitsplätze, was 15,1 % der gesamten europäischen Beschäftigung entspricht. Laut den von der Europäischen Föderation für Verkehr und Umwelt zitierten Statistiken hat sich die britische Regierung zu einem Netto-Null-Emissionsziel bis 2050 verpflichtet und ein Verkaufsverbot für alle umweltschädlichen Fahrzeuge bis 2035 vorgeschlagen. Daher treiben Initiativen für Netto-Null-Emissionen und die Nachfrage der Verbraucher nach umweltfreundlichen Fahrzeugen den Markt für Luftstromsensoren an.

Nachfrage nach Volumenstromsensoren für extreme Anwendungen

Zahlreiche Branchen wie die Automobilindustrie, die Luft- und Raumfahrt, die Fertigung, die Energie- und Versorgungsindustrie und andere stellen hohe Anforderungen an Volumenstromsensoren, die extremen Bedingungen standhalten. Dies ermutigt die Marktteilnehmer, Volumenstromsensoren für extreme Anwendungen zu entwickeln. So stellte ENVEA im September 2023 AirFlow P vor, eine Hochtemperaturversion des Volumenstromsensors für extreme Anwendungen. AirFlow P ist ein Sensor zur Volumenstrommessung in staubbeladenen Sensoren, der für Hochtemperaturanwendungen bis 800 °C geeignet ist.

Segmentierungsanalyse des Marktberichts zu Luftstromsensoren

Schlüsselsegmente, die zur Ableitung der Marktanalyse für Luftstromsensoren beigetragen haben, sind Typ und Anwendung.

- Basierend auf dem Typ ist der Markt für Luftstromsensoren in Volumenstromsensoren und Massenstromsensoren unterteilt. Das Segment Volumenstrom hatte 2022 einen größeren Marktanteil.

- Basierend auf der Anwendung ist der Markt in Automobil, Luft- und Raumfahrt, Fertigung, Energie & Versorgung und Sonstige unterteilt. Das Automobilsegment hatte 2022 einen größeren Marktanteil.

Marktanteilsanalyse für Luftstromsensoren nach Geografie

Der geografische Umfang des Marktberichts für Luftstromsensoren ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten & Afrika sowie Süd- und Mittelamerika.

Länder wie Japan, Indien, China, Australien, Singapur, Taiwan und Indonesien verfügen über eine Vielzahl von Fertigungsindustrien, darunter Elektronik, Lebensmittel und Getränke, Chemie, Textilien, Automobile und Gesundheitswesen. Regierungsinitiativen wie „Made in China 2025“ und „Made in India“ fördern diese Branchen in verschiedenen Ländern des asiatisch-pazifischen Raums, was die Nachfrage nach Luftstromsensoren ankurbelt. China verfügt zudem über eine schnell wachsende Luft- und Raumfahrtindustrie. Ein Team aus technologisch versierten Kandidaten und jungen Wissenschaftlern in Peking hat in der Vergangenheit maßgeblich an Missionen wie den Chang'e-Mondsonden und der Tianwen-Marserkundung mitgewirkt. Solche Entwicklungen in der Luft- und Raumfahrtindustrie treiben das Wachstum des Marktes für Luftstromsensoren in China voran. Das wachsende Bewusstsein für die Bedeutung der Überwachung der Luftqualität steigert zudem die Nachfrage nach HLK-Systemen im asiatisch-pazifischen Raum und profitiert damit vom Markt für Luftstromsensoren in der Region.

Luftstromsensoren

Regionale Einblicke in den Markt für LuftstromsensorenDie Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Markt für Luftstromsensoren im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Lage von Luftstromsensoren in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

Umfang des Marktberichts zu Luftstromsensoren

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2022 | US$ 2.41 Billion |

| Marktgröße nach 2030 | US$ 3.5 Billion |

| Globale CAGR (2022 - 2030) | 4.8% |

| Historische Daten | 2020-2021 |

| Prognosezeitraum | 2023-2030 |

| Abgedeckte Segmente |

By Typ

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte von Luftstromsensoren: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Luftstromsensoren wächst rasant. Die steigende Nachfrage der Endverbraucher ist auf Faktoren wie veränderte Verbraucherpräferenzen, technologische Fortschritte und ein stärkeres Bewusstsein für die Produktvorteile zurückzuführen. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Markt für Luftstromsensoren Übersicht der wichtigsten Akteure

Marktneuigkeiten und aktuelle Entwicklungen zu Luftstromsensoren

Der Markt für Luftstromsensoren wird durch die Erhebung qualitativer und quantitativer Daten aus Primär- und Sekundärforschung bewertet, die wichtige Unternehmenspublikationen, Verbandsdaten und Datenbanken umfasst. Einige der Entwicklungen auf dem Markt für Luftstromsensoren sind nachfolgend aufgeführt:

- ENVEA, ein führender Anbieter von Lösungen zur Umweltüberwachung, präsentiert die Erweiterung seiner AirFlow P-Sensorserie um eine Hochtemperaturversion, die Temperaturen von bis zu 800 °C standhält. Diese Ergänzung erweitert die Fähigkeiten des AirFlow P-Sensors und macht ihn zu einer idealen Lösung für noch anspruchsvollere industrielle Anwendungen. (Quelle: ENVEA, Unternehmenswebsite, September 2023)

- Posifa Technologies stellte die neueste Version seiner Luftstromsensoren vor, die in der Beatmungstherapie sowie anderen Gesundheits- und Instrumentierungszwecken eingesetzt werden. Die Sensoren der Serien PMF83000 und PMF86000 sind für den Einsatz in rauen Umgebungen mit hoher Luftfeuchtigkeit und geringen Konzentrationen korrosiver Gase vorgesehen. (Quelle: Posifa Technologies, Unternehmenswebsite, April 2021)

Marktbericht zu Luftstromsensoren: Umfang und Ergebnisse

Der Bericht „Marktgröße und Prognose für Luftstromsensoren (2020–2030)“ bietet eine detaillierte Analyse des Marktes und deckt die folgenden Bereiche ab:

- Marktgröße und Prognose für Luftstromsensoren auf globaler, regionaler und Länderebene für alle abgedeckten wichtigen Marktsegmente

- Markttrends und Marktdynamiken für Luftstromsensoren wie Treiber, Einschränkungen und wichtige Chancen

- Detaillierte PEST/Porters Fünf-Kräfte- und SWOT-Analyse

- Marktanalyse für Luftstromsensoren mit wichtigen Markttrends, globalen und regionalen Rahmenbedingungen, wichtigen Akteuren, Vorschriften und aktuellen Marktentwicklungen

- Branchenlandschaft und Wettbewerbsanalyse mit Marktkonzentration, Heatmap-Analyse, prominenten Akteuren und aktuellen Entwicklungen für den Markt für Luftstromsensoren

- Detaillierte Unternehmensprofile

Naveen ist ein erfahrener Marktforschungs- und Beratungsexperte mit über 9 Jahren Erfahrung in kundenspezifischen, syndizierten und Beratungsprojekten. In seiner aktuellen Funktion als Associate Vice President hat er erfolgreich Stakeholder entlang der gesamten Projektwertschöpfungskette gemanagt und ist Autor von über 100 Forschungsberichten und über 30 Beratungsaufträgen. Seine Arbeit erstreckt sich auf Industrie- und Regierungsprojekte und trägt maßgeblich zum Kundenerfolg und zur datengesteuerten Entscheidungsfindung bei.

Naveen hat einen Ingenieursabschluss in Elektronik und Kommunikation von der VTU, Karnataka, und einen MBA in Marketing und Operations von der Manipal University. Er ist seit 9 Jahren aktives IEEE-Mitglied und nimmt an Konferenzen und technischen Symposien teil und engagiert sich ehrenamtlich auf Sektions- und regionaler Ebene. Vor seiner aktuellen Position arbeitete er als Associate Strategic Consultant bei IndustryARC und als Industrial Server Consultant bei Hewlett Packard (HP Global).

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends