Wachstum, Größe, Anteil, Trends, Analyse der wichtigsten Akteure und Prognose des Flughafenantennenmarktes bis 2027

Marktprognose für Flughafenantennen bis 2027 – Auswirkungen von COVID-19 und globale Analyse nach Flughafentyp (Militärflughafen, Verkehrsflughafen), Antennentyp (Dipol, Monopol), Frequenzband (Hochfrequenz, Sehr hohe Frequenz, Ultrahochfrequenz) und Anwendung (SATCOM, Überwachung, Navigation und andere)

- Status : Veröffentlicht

- Berichtscode : TIPRE00014280

- Kategorie : Elektronik und Halbleiter

- Anzahl der Seiten : 181

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 20, 2024

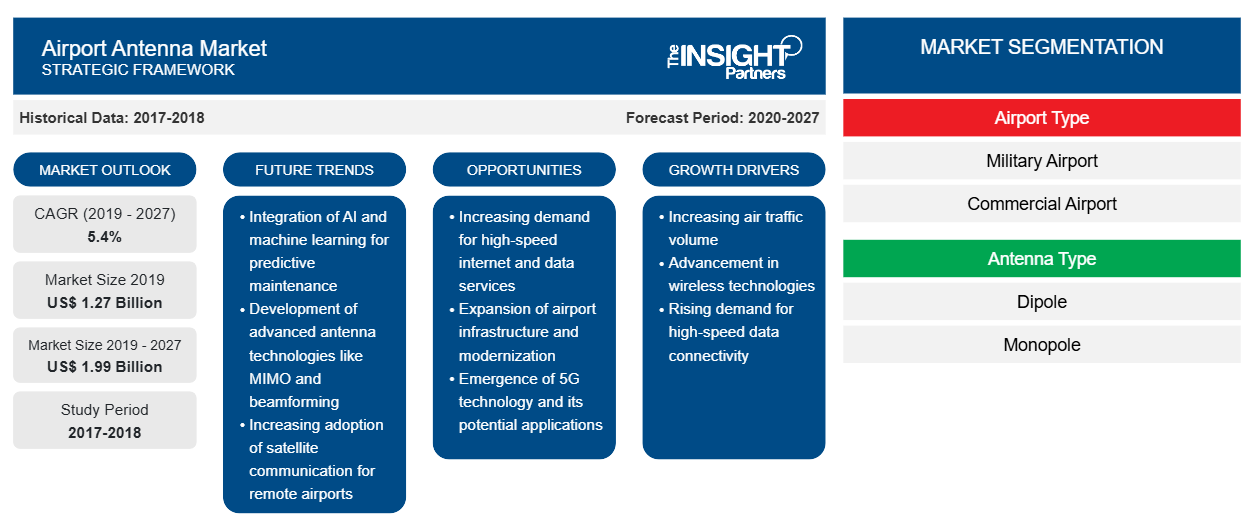

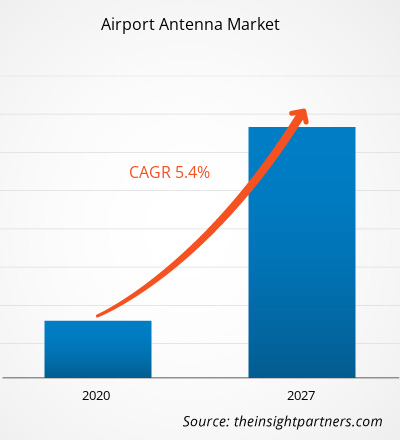

Der Markt für Flughafenantennen wurde im Jahr 2019 auf 1,27 Milliarden US-Dollar geschätzt und soll voraussichtlich1,99 Milliarden bis 2027; für den Prognosezeitraum wird ein durchschnittliches jährliches Wachstum von 5,4 % erwartet.

Eine Antenne ist ein Gerät, das elektrische Signale empfängt und überträgt. Antennen spielen auf Flughäfen eine wichtige Rolle, um Mobiltelefonie, Satellitenkommunikation und drahtlose lokale Netzwerke zu ermöglichen. Ein Flugzeug verwendet Hochfrequenzantennen, um seine Ziele anzusteuern und mit der Flugsicherung zu kommunizieren. Flughafenantennen werden hauptsächlich auf Militärflughäfen und Verkehrsflughäfen verwendet. Auf Militärflughäfen ermöglichen die Antennen eine verbesserte Kommunikation durch die Einführung von Hochfrequenz-, Höchstfrequenz- und Ultrahochfrequenzbändern. Diese fortschrittlichen Antennenlösungen bieten Anwendungen in Fahrzeugen, am Boden, in der Luft und an Bord von Schiffen, die bei der Darstellung zahlreicher militärischer Operationen helfen.

Die Fortschritte bei Flughafenantennensystemen nehmen aufgrund des zunehmenden Baus und der Renovierung neuer und bestehender Flughäfen auf der ganzen Welt zu. Da die Zahl der Passagiere, die mit dem Flugzeug reisen, zunimmt, werden in Flughäfen in großem Umfang WLAN-Hotspot-Antennen für WLAN eingesetzt, um den Passagieren einen Hochgeschwindigkeits-Internetzugang zu bieten. Das in Großbritannien ansässige Unternehmen Mobile Mark, Inc. bot im Oktober 2019 5G-Flottenmanagementantennen für das Global Navigation Satellite System (GNSS) und WLAN-Einrichtungen an, die für Kommunikation, öffentliche Sicherheit und Fahrzeugflottenmanagement verwendet werden sollen.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos individuelle Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für Flughafenantennen: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Auswirkungen der COVID-19-Pandemie auf den Markt für Flughafenantennen

Die globale Luftfahrtindustrie ist eine der wichtigsten Branchen, die infolge der COVID-19-Pandemie mit schwerwiegenden Störungen wie Flugausfällen, vorübergehenden Lockdowns und Passagierrückgängen konfrontiert ist. Laut der Internationalen Zivilluftfahrt-Organisation (ICAO) gab es im Jahr 2020 einen Rückgang der Passagierzahlen um ~57–60 % im Vergleich zu 2019 und von Januar bis August 2020 einen Verlust an Passagiereinnahmen von ~256 Milliarden US-Dollar. In der Folge ist die Nachfrage nach Verbesserungen der Flughafeninfrastruktur, einschließlich der Nachfrage nach Flughafenantennen, weltweit stark zurückgegangen. Darüber hinaus beeinträchtigt die Schließung verschiedener Werke und Fabriken, die Komponenten, Sensoren, Controller und Material für Antennen entwickeln, in führenden Regionen wie Nordamerika, Europa, dem Nahen Osten und Afrika sowie Südamerika die globalen Lieferketten und wirkt sich negativ auf die Entwicklung von Flughäfen, den Bau neuer Flughäfen und die Rohstoffversorgung aus.

Einblicke in den Markt für Flughafenantennen

Starker Ausbau und Modernisierung der Flughafeninfrastruktur

Angesichts der weltweit steigenden Zahl von Fluggästen konzentrieren sich die Regierungen verschiedener Länder auf die Verbesserung der Flughafeninfrastruktur. Laut 20-Jahres-Schätzungen der International Air Transport Association (IATA) wird die Zahl der weltweiten Fluggäste bis 2037 voraussichtlich auf rund 8,2 Milliarden ansteigen, was einer durchschnittlichen jährlichen Wachstumsrate von 3,5 % entspricht. Berechnungen der IATA zufolge wird die Luftfahrtindustrie in den nächsten 20 Jahren voraussichtlich ein robustes Wachstum erleben und den verschiedenen am Ökosystem beteiligten Akteuren diverse Vorteile bieten. Für Nordamerika wird ein Wachstum von rund 1,4 Milliarden Passagieren um eine durchschnittliche jährliche Wachstumsrate von 2,4 % prognostiziert, und für Europa wird ein Wachstum von rund 2,0 % auf rund 1,9 Milliarden Passagiere im Prognosezeitraum erwartet. Der größte Teil des Wachstums wird jedoch voraussichtlich aus dem Osten der Welt kommen. Die IATA schätzt außerdem, dass die Region Asien-Pazifik aufgrund des zunehmenden Flugverkehrswachstums in Ländern wie Indien, Singapur, China und Japan den größten Beitrag zum Umsatz der globalen Luftfahrtindustrie leisten wird. In der Region Asien-Pazifik wird mit einem Anstieg der Passagierzahlen auf rund 2,35 Milliarden bis 2037 gerechnet, im Jahr 2037 dürften es rund 3,90 Milliarden Passagiere sein.

Markteinblicke basierend auf Flughafentypen

Basierend auf dem Flughafentyp ist der Markt für Flughafenantennen in Militärflughäfen und Verkehrsflughäfen unterteilt. Die Flughafenantennen in Flughäfen werden für verschiedene Anwendungen verwendet, darunter Überwachung, Navigation und Boden-Luft-Kommunikation. Die Militärflughafenantennen sind speziell nach militärischen Standards entwickelte Antennen und unterscheiden sich von den Antennen für Verkehrsflughäfen. Die wachsende Zahl militärischer und Verkehrsflughäfen weltweit ist einer der Hauptfaktoren, die das Wachstum des Flughafenantennenmarktes unterstützen. Darüber hinaus konzentrieren sich die Unternehmen auf dem Flughafenantennenmarkt darauf, hochmoderne Lösungen anzubieten, um den spezifischen Anforderungen kommerzieller und militärischer Flughäfen gerecht zu werden.

Antennentyp-basierteMarkteinblicke

Basierend auf dem Antennentyp ist der Markt für Flughafenantennen in Monopolantennen und Dipolantennen unterteilt. Die Dipolantennen werden in Flughäfen für Kommunikation, Überwachung und andere Anwendungen eingesetzt. Die Monopolantennen eignen sich für RFID und drahtlose Netzwerke. Die auf dem Markt tätigen Unternehmen konzentrieren sich auf die Einführung effizienter Antennen, um die Leistung der Flughafeninfrastruktur zu verbessern.

FrequenzbandbasierteMarkteinblicke

Basierend auf dem Frequenzband ist der Markt für Flughafenantennen in Hochfrequenz (HF), Sehr hohe Frequenz (VHF) und Ultrahohe Frequenz (UHF) unterteilt. Die HF-Antennen werden für Kommunikationszwecke an Flughäfen verwendet. VHF- und UHF-Antennen werden für Punkt-zu-Punkt-, Boden-zu-Luft- und Luft-zu-Boden-Anwendungen verwendet. Die auf dem Markt tätigen Unternehmen bieten HF-, UHF- und VHF-Antennen in verschiedenen Konfigurationen, Funktionen und Eigenschaften an, um den Anforderungen verschiedener Installationen gerecht zu werden. Einige der Unternehmen bieten auch kundenspezifische Produkte an, um die spezifischen Anforderungen ihrer Kunden zu erfüllen.

AnwendungsbasierteMarkteinblicke

Basierend auf der Anwendung ist der Markt für Flughafenantennen in SATCOM, Überwachung, Navigation und andere unterteilt. Die Flughafenantennen sind in verschiedene Flughafeninfrastrukturen integriert, die für unterschiedliche Anwendungen im Flughafen verwendet werden. Flughafenantennen helfen dabei, Kollisionen zu vermeiden, Flugzeuge zu überwachen und den Flugverkehr zu steuern, um die Effizienz des Flughafens zu verbessern. Darüber hinaus wird erwartet, dass der wachsende Flugverkehr, eine zunehmende Anzahl von Flughäfen und eine starke Betonung der Flugzeugsicherheit und der Verbesserung des Flugverkehrsflusses die wachsende Nachfrage nach Flughafenantennen für verschiedene Anwendungen unterstützen werden. Die auf dem Markt tätigen Unternehmen arbeiten auch konsequent daran, effiziente Antennen für verschiedene Flughafenanwendungen anzubieten, um eine starke Marktposition zu erreichen.

Regionale Einblicke in den Markt für Flughafenantennen

Die regionalen Trends und Faktoren, die den Markt für Flughafenantennen im Prognosezeitraum beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die Geografie von Flughafenantennen in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionalspezifische Daten zum Flughafenantennenmarkt

Umfang des Marktberichts für Flughafenantennen

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2019 | 1,27 Milliarden US-Dollar |

| Marktgröße bis 2027 | 1,99 Milliarden US-Dollar |

| Globale CAGR (2019 - 2027) | 5,4 % |

| Historische Daten | 2017-2018 |

| Prognosezeitraum | 2020–2027 |

| Abgedeckte Segmente |

Nach Flughafentyp

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktteilnehmerdichte für Flughafenantennen: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Flughafenantennen wächst rasant, angetrieben durch die steigende Nachfrage der Endnutzer aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung der Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten auf dem Markt für Flughafenantennen tätigen Unternehmen sind:

- Northrop Grumman Corporation

- Cobham Limited

- Wade Antenna, Inc

- Amphenol Procom

- Antenna Product Corporation

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Flughafenantennenmarkt

Die Akteure auf dem Flughafenantennenmarkt konzentrieren sich auf Strategien wie Marktinitiativen, Akquisitionen und Produkteinführungen, um ihre Positionen auf dem Markt zu behaupten. Nachfolgend sind einige Entwicklungen der wichtigsten Akteure aufgeführt:

Im Jahr 2020 übernahm HENSOLDT Südafrika das Verteidigungs- und Sicherheitsunternehmen Tellumat sowie das Flugverkehrsmanagement. Mit dieser Strategie wird HENSOLDT sein Portfolio sowie seine Präsenz in Afrika weiter ausbauen.

2019 nahm NAV CANADA das erste SCANTER 5502 Solid State Surface Movement Radar im größten Flughafen des Landes in Toronto in Betrieb. Das Unternehmen liefert die neue, beheizte Anti-Icing-Antenne, die verhindern kann, dass sich beim Drehen Eis auf der Antenne bildet.

Markt für Flughafenantennen – nach Flughafentyp

- Kommerzieller Flughafen

- Militärflughafen

Flughafenantennenmarkt – nach Antennentyp

- Dipol

- Monopol

Markt für Flughafenantennen – nach Frequenzband

- Hochfrequenz

- Sehr hohe Frequenz

- Ultrahochfrequenz

Flughafenantennenmarkt – nach Anwendung

- SATCOM

- Navigation

- Überwachung

- Sonstiges

Markt für Flughafenantennen – nach Geografie

-

Nordamerika

- UNS

- Kanada

- Mexiko

-

Europa

- Vereinigtes Königreich

- Deutschland

- Frankreich

- Italien

- Spanien

- Schweiz

- Skandinavien

- Restliches Europa

-

Asien-Pazifik (APAC)

- China

- Japan

- Indien

- Australien

- Südkorea

- Singapur

- Malaysia

- Thailand

- Restlicher Asien-Pazifik-Raum

-

Naher Osten und Afrika (MEA)

- Saudi-Arabien

- Vereinigte Arabische Emirate

- Südafrika

- Rest von MEA

-

Südamerika (SAM)

- Brasilien

- Argentinien

- Chile

- Rest von SAM

Markt für Flughafenantennen – Firmenprofile

- Northrop Grumman Corporation

- Cobham Limited

- Wade Antenna, Inc

- Amphenol Procom

- Antenna Product Corporation

- Comrod Communication AS

- HENSOLDT Inc

- Rohde & Schwarz GmbH & Co.

- Terma

- Watts Antenna Company

Naveen ist ein erfahrener Marktforschungs- und Beratungsexperte mit über 9 Jahren Erfahrung in kundenspezifischen, syndizierten und Beratungsprojekten. In seiner aktuellen Funktion als Associate Vice President hat er erfolgreich Stakeholder entlang der gesamten Projektwertschöpfungskette gemanagt und ist Autor von über 100 Forschungsberichten und über 30 Beratungsaufträgen. Seine Arbeit erstreckt sich auf Industrie- und Regierungsprojekte und trägt maßgeblich zum Kundenerfolg und zur datengesteuerten Entscheidungsfindung bei.

Naveen hat einen Ingenieursabschluss in Elektronik und Kommunikation von der VTU, Karnataka, und einen MBA in Marketing und Operations von der Manipal University. Er ist seit 9 Jahren aktives IEEE-Mitglied und nimmt an Konferenzen und technischen Symposien teil und engagiert sich ehrenamtlich auf Sektions- und regionaler Ebene. Vor seiner aktuellen Position arbeitete er als Associate Strategic Consultant bei IndustryARC und als Industrial Server Consultant bei Hewlett Packard (HP Global).

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends