Automotive Infotainment SoC-Marktbericht 2027 nach Segmenten, Geografie, Dynamik, jüngsten Entwicklungen und strategischen Erkenntnissen

Historische Daten : 2016-2017 | Basisjahr : 2018 | Prognosezeitraum : 2019-2027Markt für Automotive-Infotainment-SoCs bis 2027 – Globale Analyse und Prognosen nach Installationstyp (In-Dash und Rücksitz); Anwendung (Head Unit, eCockpit, Soundsystem und andere); Fahrzeugtyp (Pkw und Nutzfahrzeug)

- Status : Veröffentlicht

- Berichtscode : TIPRE00005572

- Kategorie : Elektronik und Halbleiter

- Anzahl der Seiten : 154

- Verfügbare Berichtsformate :

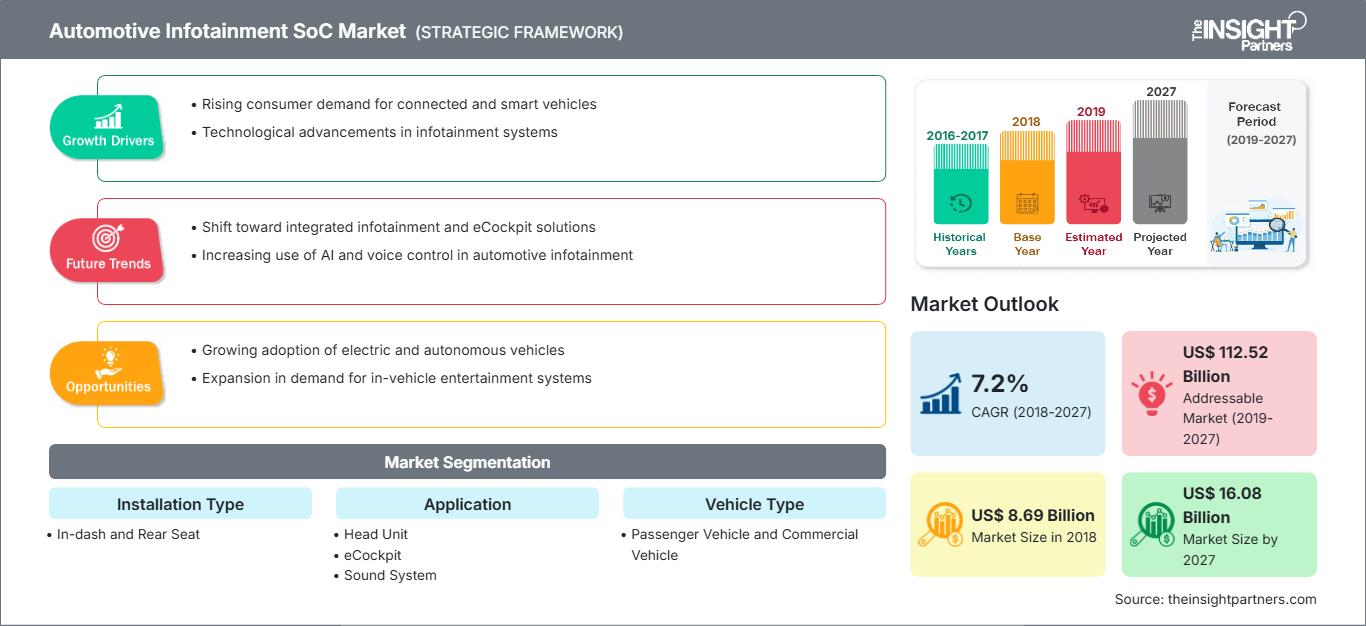

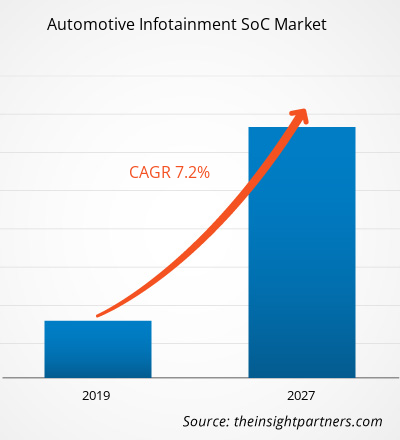

Der Markt für Automotive-Infotainment-SoCs wurde 2018 auf 8.694,6 Mio. US-Dollar geschätzt und soll bis 2027 voraussichtlich 16.077,6 Mio. US-Dollar erreichen; von 2019 bis 2027 wird ein CAGR von 7,2 % erwartet.

Das Automotive-Infotainment-SoC ist ein integrierter Chip für Informations-, Telefon- und Unterhaltungsdienste in Personenkraftwagen und Nutzfahrzeugen. Es handelt sich um ein komplettes elektronisches Substratsystem mit analogen, digitalen, gemischten Signal- und Hochfrequenzfunktionen. Automotive-Infotainment-SoCs benötigen weniger Platz und Fläche als Multi-Chip-Designs. SoCs werden häufig in eingebetteten Systemen und im Internet der Dinge für die Automobil-Computertechnik eingesetzt. Die Branche agiert in einem wettbewerbsintensiven Markt, in dem führende Unternehmen in diesem Markt ihren Zielmarkt kontinuierlich erweitern, indem sie ihr aktuelles Produktportfolio erweitern, ihren Kundenstamm diversifizieren und neue Anwendungen und Märkte entwickeln. Neuentwicklungen sowie Fusionen und Übernahmen sind die beiden bemerkenswerten Markttrends der letzten Jahre. Unternehmen in der Wertschöpfungskette erwerben und gehen Partnerschaften mit anderen Marktteilnehmern ein, um ihre Marktposition zu behaupten und ihren Kunden effiziente Lösungen anzubieten. Wichtige Marktteilnehmer im Bereich Automotive-Infotainment-SoCs haben ihren Sitz in den USA und anderen europäischen Ländern wie Deutschland. Die Automobilindustrie in Industrie- und Schwellenländern erlebt einen digitalen Wandel. Viele Industrieunternehmen der Automobilbranche investieren beträchtliche Ressourcen in die Forschung und Entwicklung im Bereich der Fahrzeugautomatisierung, um den veränderten Anforderungen gerecht zu werden und das Fahrerlebnis der Kunden zu verbessern. Autos der nächsten Generation werden unter anderem mit audiovisueller Sensorik, Spracherkennung, Bildkompatibilität, fortschrittlicher Fahrerassistenz, GPS- und Radarfunktionen, Sicherheit der nächsten Stufe und IC-integrierter LED-Frontbeleuchtung ausgestattet sein. Automotive-Infotainment-SoCs spielen eine Schlüsselrolle in der Fahrzeugautomatisierung, da sie in Autos verwendet werden, um verschiedene fortschrittliche Funktionen in Fahrzeuge zu integrieren. Daher setzen verschiedene Automobilhersteller Automotive-Infotainment-SoCs ein, um ihren Kunden ein optimales Fahrerlebnis zu bieten und so die Nachfrage nach Automotive-Infotainment-SoCs zu fördern. Im Prognosezeitraum wird die Automobilindustrie voraussichtlich die weltweite Nachfrage nach Automotive-Infotainment-SoCs ankurbeln und damit den Automotive-Infotainment-SoC-Markt ankurbeln.

Die Region Asien-Pazifik wird voraussichtlich im Prognosezeitraum ihre dominierende Position im globalen Automotive-Infotainment-SoC-Markt behaupten. Derzeit verzeichnet der Automotive-Infotainment-SoC-Markt in der Region ein rasantes Wachstum, das auf zahlreiche Faktoren zurückzuführen ist. Die wichtigsten Faktoren für das Wachstum dieser Branche sind das höhere verfügbare Einkommen der Verbraucher und die damit verbundene Zunahme der Pkw-Zahl; eine höhere Verkehrsdichte, die zu mehr Staus und einer längeren durchschnittlichen Verweildauer der Reisenden führt, sowie parallele Fortschritte in der Unterhaltungselektronik. Die Verbraucherausgaben für Automobilelektronik und verwandtes Zubehör haben sich drastisch verändert, was derzeit enorme Geschäftschancen bietet. Touchscreen-Systeme sind in vielen Unterhaltungselektronikgeräten wie Smartphones weit verbreitet, und ihr Potenzial wurde auf diese Branche übertragen. Diese Faktoren treiben die Nachfrage nach Automotive-Infotainment-SoCs in der Region Asien-Pazifik an. Darüber hinaus hatte Europa einen Anteil von 32,59 % am globalen Automotive-Infotainment-SoC-Markt. Ein Schlüsselfaktor für das Wachstum des europäischen Marktes für Infotainment-SoCs im Automobilbereich ist die hohe Verbreitung von Infotainmentsystemen in Premium- sowie Mittelklassefahrzeugen. Auch andere Faktoren, wie wachsende Sicherheitsbedenken und die damit einhergehenden gesetzlichen Regulierungen, dürften das Wachstum des Marktes für Infotainment-SoCs im Automobilbereich vorantreiben. Darüber hinaus dürfte das schnelle Wachstum bei der Herstellung von Elektrofahrzeugen die Nachfrage nach Infotainmentsystemen im Automobilbereich ankurbeln, da diese die Nutzer von Elektrofahrzeugen auf nahegelegene Ladestationen aufmerksam machen können. Die steigende Nachfrage nach Infotainmentsystemen im Automobilbereich treibt somit auch die Nachfrage nach Infotainment-SoCs im Automobilbereich an.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Automotive Infotainment SoC Markt: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

Die Entwicklungsregionen der Welt wie Asien-Pazifik, Naher Osten, Afrika und Südamerika zeichnen sich durch positive globale Wirtschaftsaussichten, eine wachsende Mittelschichtbevölkerung und steigende verfügbare Einkommen aus. Alle diese Faktoren treiben den Pkw-Absatz in diesen Regionen an. Trotz einiger Rückgänge bei den Verkäufen der Automobilindustrie in jüngster Zeit werden die allgemeinen Wachstumsaussichten für den Prognosezeitraum 2019 bis 2027 als positiv eingeschätzt. Der Autobesitz variiert erheblich zwischen Entwicklungsmärkten, jedoch ist die Zahl der Pkw pro Haushalt im letzten Jahrzehnt konstant gestiegen. Steigende verfügbare Einkommen und eine wachsende Mittelschichtbevölkerung sind die Hauptfaktoren, die den Pkw-Absatz in den Schwellenländern der Welt antreiben. Entwicklungsländer haben in der Zeit nach der Rezession ein stetiges Wachstum erlebt und somit auch das verfügbare Einkommen der Verbraucher.

Markteinblicke basierend auf Installationstypen

Der Markt für Automotive-Infotainment-SOCs (PV) wurde nach Installationstypen in Armaturenbrett- und Rücksitzinstallationen unterteilt. Das Armaturenbrettsegment hatte 2018 den größten Anteil am Automotive-Infotainment-SOC-Markt. Darüber hinaus wird das Rücksitzsegment im Prognosezeitraum voraussichtlich schneller wachsen. Automotive-Infotainment-SOCs werden zunehmend in Armaturenbrettern verwendet, um das Fahrerlebnis zu verbessern. Mit dem Wachstum der Branche werden sie jedoch auch zunehmend für Rücksitzinstallationen nachgefragt.

Markteinblicke basierend auf Anwendungen

Der globale Automotive-Infotainment-SOC-Markt wurde nach Anwendungen in Headunits, eCockpits, Soundsysteme und andere unterteilt. Das Head-Unit-Segment dominierte 2018 den globalen Markt für Automotive-Infotainment-SOCs. Mit dem wachsenden technologischen Fortschritt und der Integration verbesserter Designs werden Automotive-Infotainmentsysteme in mehreren Anwendungsbereichen eingesetzt.

Produktentwicklung ist die von Unternehmen häufig verfolgte Strategie zur Erweiterung ihres Produktportfolios. Texas Instruments Incorporated, Intel Corporation, Qualcomm Incorporated, NVIDIA Corporation und Infineon Technologies AG sind unter anderem die Hauptakteure, die Strategien zur Vergrößerung des Kundenstamms und zur Eroberung bedeutender Anteile am globalen Automotive-Infotainment-SOC-Markt umsetzen, was ihnen wiederum die Aufrechterhaltung ihres Markennamens ermöglicht. Einige der jüngsten wichtigen Entwicklungen sind:

- 2019 kam Polestar auf den Markt, eine neue, eigenständige Performance-Marke für Elektroautos, an der Volvo Cars einen 50-prozentigen Anteil hält und die ein auf einem Intel Atom®-Prozessor laufendes In-Vehicle-Infotainmentsystem (IVI) integriert. Prozessor der A3900-Serie.

- Im Jahr 2019 hat Infineon Technologies Cypress Semiconductor für 10 Milliarden US-Dollar übernommen. Dies ist die jüngste Übernahme in einer Reihe von Zukäufen von Anbietern von Konnektivitätschips in den letzten Monaten. Der Großteil des Automobilgeschäfts von Cypress basiert auf Infotainment-Mikrocontrollern und Konnektivitätslösungen, was die Stärke des Unternehmens weiter stärken wird.

Automotive Infotainment SoC

Regionale Einblicke in den Automotive-Infotainment-SoC-MarktDie Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Markt für Automotive-Infotainment-SoCs im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Lage in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

Umfang des Marktberichts zum Infotainment-SoC im Automobilbereich

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2018 | US$ 8.69 Billion |

| Marktgröße nach 2027 | US$ 16.08 Billion |

| Globale CAGR (2018 - 2027) | 7.2% |

| Historische Daten | 2016-2017 |

| Prognosezeitraum | 2019-2027 |

| Abgedeckte Segmente |

By Installationstyp

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Marktteilnehmer für Infotainment-SoCs im Automobilbereich: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Automotive-Infotainment-SoCs wächst rasant. Dies wird durch die steigende Endverbrauchernachfrage aufgrund veränderter Verbraucherpräferenzen, technologischer Fortschritte und eines stärkeren Bewusstseins für die Produktvorteile vorangetrieben. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Automotive Infotainment SoC Markt Übersicht der wichtigsten Akteure

- Im Armaturenbrett

- Rücksitz

Nach Anwendung

- Head Unit

- eCockpit

- Soundsystem

- Sonstige

Nach Fahrzeugtyp

- Pkw

- Nutzfahrzeug

Firmenprofile

- Infineon Technologies AG

- Intel Corporation

- NEC Corporation

- NVIDIA Corporation

- NXP Semiconductors NV

- Qualcomm Incorporated

- Renesas Electronics Corporation

- STMicroelectronics NV

- Texas Instruments Incorporated

- Semiconductor Components Industries, LLC (ON Halbleiter)

Naveen ist ein erfahrener Marktforschungs- und Beratungsexperte mit über 9 Jahren Erfahrung in kundenspezifischen, syndizierten und Beratungsprojekten. In seiner aktuellen Funktion als Associate Vice President hat er erfolgreich Stakeholder entlang der gesamten Projektwertschöpfungskette gemanagt und ist Autor von über 100 Forschungsberichten und über 30 Beratungsaufträgen. Seine Arbeit erstreckt sich auf Industrie- und Regierungsprojekte und trägt maßgeblich zum Kundenerfolg und zur datengesteuerten Entscheidungsfindung bei.

Naveen hat einen Ingenieursabschluss in Elektronik und Kommunikation von der VTU, Karnataka, und einen MBA in Marketing und Operations von der Manipal University. Er ist seit 9 Jahren aktives IEEE-Mitglied und nimmt an Konferenzen und technischen Symposien teil und engagiert sich ehrenamtlich auf Sektions- und regionaler Ebene. Vor seiner aktuellen Position arbeitete er als Associate Strategic Consultant bei IndustryARC und als Industrial Server Consultant bei Hewlett Packard (HP Global).

- Historische Analyse (2 Jahre), Basisjahr, Prognose (7 Jahre) mit CAGR

- PEST- und SWOT-Analyse

- Marktgröße Wert/Volumen – Global, Regional, Land

- Branchen- und Wettbewerbslandschaft

- Excel-Datensatz

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends

Exklusive Berichtsrabatte freischalten

Jetzt anfragen

Kostenlose Probe anfordern für - Automotive Infotainment SoC Markt

Kostenlose Probe anfordern für - Automotive Infotainment SoC Markt