Marktwachstum, Größe, Anteil, Trends, Analyse der wichtigsten Akteure und Prognose für Kohlefaser in leichten Druckbehältern bis 2027

Historische Daten : 2016-2017 | Basisjahr : 2018 | Prognosezeitraum : 2019-2027Markt für Kohlefasern in leichten Druckbehältern bis 2027 – Globale Analyse und Prognosen nach Vorläufertyp (PAN, Pitch), nach Schleppgröße (12 k bis 24 k, 24 k und mehr) und Geografie

- Status : Veröffentlicht

- Berichtscode : TIPRE00006456

- Kategorie : Chemikalien und Materialien

- Anzahl der Seiten : 144

- Verfügbare Berichtsformate :

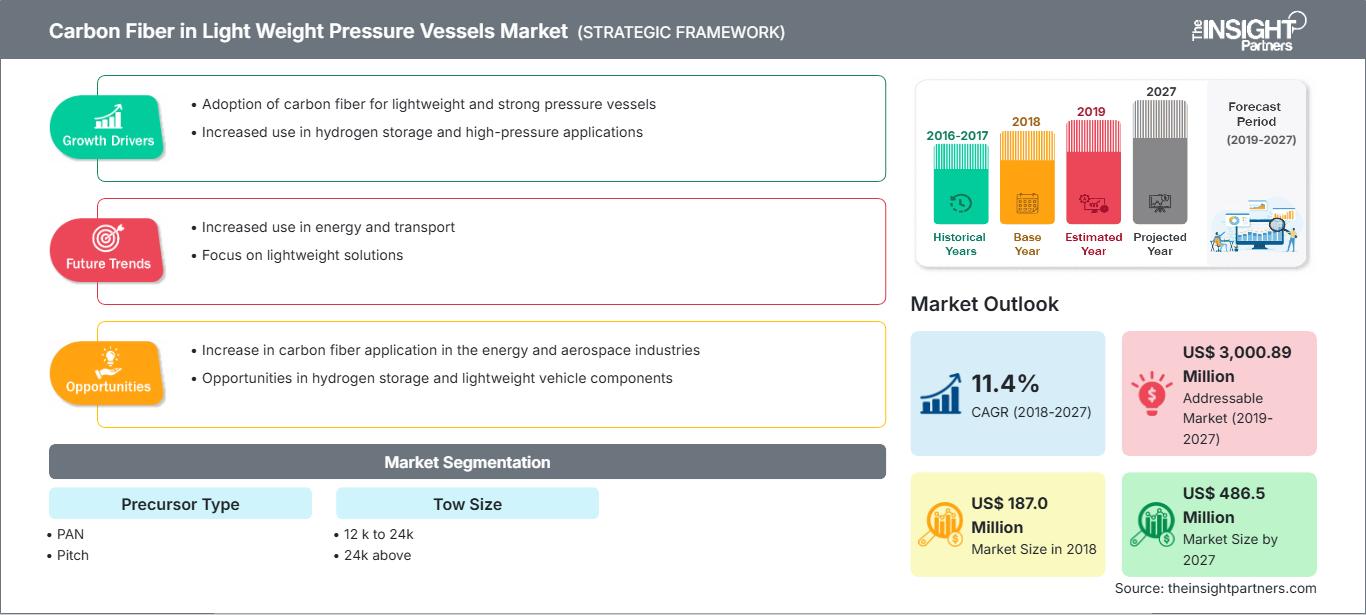

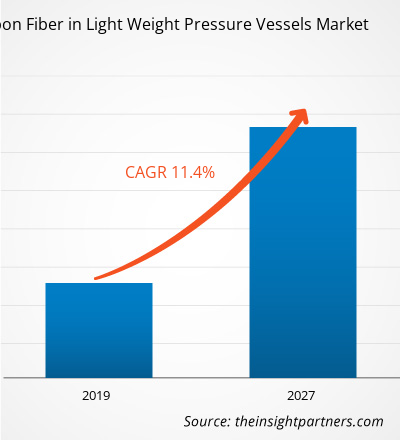

Der globale Markt für Kohlefaser in leichten Druckbehältern belief sich im Jahr 2018 auf 187,0 Mio. US-Dollar und wird im Prognosezeitraum 2019–2027 voraussichtlich mit einer durchschnittlichen jährlichen Wachstumsrate (CAGR) von 11,4 % wachsen und bis 2027 486,5 Mio. US-Dollar erreichen.

Die Region Asien-Pazifik ist die am schnellsten wachsende Region für Druckbehälter auf Kohlefaserbasis. Dies ist auf die wachsende Bevölkerung und die zunehmenden Umweltbedenken der Regierungen in Ländern wie Indien, China und Japan zurückzuführen, gepaart mit der zunehmenden Konzentration auf energieeffiziente und umweltfreundliche CNG-Fahrzeuge. Darüber hinaus wird erwartet, dass die wachsende Nachfrage aus der Automobilindustrie das Wachstum des Marktes für Kohlefaser in leichten Druckbehältern in der Region vorantreiben wird.

Markteinblicke: Die steigende Nachfrage aus der Automobil- und Industriebranche bietet Wachstumschancen für den Markt für Kohlefaser in leichten Druckbehältern.

Kohlefaser bietet einen hohen Modul und eine hohe spezifische Festigkeit, hohe Dauerfestigkeit, hohe Steifigkeit, hohe Druckfestigkeit, einen niedrigen Wärmeausdehnungskoeffizienten, Korrosionsbeständigkeit und weitere vorteilhafte Eigenschaften, die sie für Druckbehälter in der Automobilindustrie und anderen industriellen Anwendungen nützlich machen. Auch die steigende Nachfrage nach Leichtbaumaterialien sowie staatliche Initiativen zur Reduzierung der Schadstoffemissionen und zur Steigerung der Kraftstoffeffizienz werden voraussichtlich den Markt für Kohlefaser in leichten Druckbehältern in der Automobilindustrie vorantreiben.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für Kohlefasern im Leichtbau-Druckbehälter: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

Es wird erwartet, dass der globale Markt für Kohlenstofffasern in leichten Druckbehältern eine steigende Nachfrage nach Kohlenstofffasern in geschlossenen Behältern zur Speicherung von Wasserstoffgas unter hohem Druck verzeichnen wird. Kohlenstofffasern gelten als beste Option für die Herstellung zuverlässiger und sicherer Druckbehälter, da sie dem hohen Druck von Wasserstoff standhalten können. Daher beteiligen sich globale Automobilhersteller zunehmend an der Entwicklung von Brennstoffzellenfahrzeugen, und auch die jeweiligen nationalen Regierungen unterstützen den Aufbau der Infrastruktur für die Produktion von Brennstoffzellenfahrzeugen.

Einblicke in Vorläufermaterialien

Auf Basis von Vorläufermaterialien wurde der globale Markt für Kohlenstofffasern in leichten Druckbehältern in Polyacrylnitril (PAN) und Pech segmentiert. Das Segment Polyacrylnitril (PAN) ist der weltweite Markt für Kohlenstofffasern in leichten Druckbehältern. Polyacrylnitril (PAN) ist eine Kohlenstofffaser, die zu etwa 68 % aus Kohlenstoff besteht und eine der am häufigsten verwendeten Ausgangsmaterialien für Kohlenstofffasern ist. PAN wird im Polymerisationsprozess mithilfe von üblicherweise verwendeten Inhibitoren wie Azoverbindungen und Peroxiden aus Acrylnitril (AN) polymerisiert. Die steigende Nachfrage nach Kohlenstofffasern in leichten Druckbehältern hat zu einem Anstieg der Herstellung und Produktion von PAN geführt, da es eines der am häufigsten verwendeten Ausgangsmaterialien ist.

Einblicke in die Stranggröße

Der globale Markt für Kohlenstofffasern in leichten Druckbehältern wurde nach Stranggröße in 12.000 bis 24.000 und über 24.000 unterteilt. Das Segment 12.000 bis 24.000 machte den größten Anteil am globalen Markt für Kohlenstofffasern in leichten Druckbehältern aus. Die hohe Festigkeit und Steifheit von 12k- bis 24k-Carbonfasern erweist sich als vorteilhaft für militärische und wissenschaftliche Anwendungen und trägt maßgeblich zum weltweiten Wachstum und zur Verbreitung von 12k- bis 24k-Carbonfasern bei. Zu den wichtigsten Herstellern von 12k- bis 24k-Carbonfasern zählen unter anderem Toray Composite Materials America, Inc., Teijin Limited und die SGL Group.

Carbonfasern in leichten Druckbehältern

Regionale Einblicke in den Markt für Kohlefasern in leichten DruckbehälternDie Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Markt für Kohlefaser in leichten Druckbehältern im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Lage für Kohlefaser in leichten Druckbehältern in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

Umfang des Marktberichts zu Kohlefasern in leichten Druckbehältern

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2018 | US$ 187.0 Million |

| Marktgröße nach 2027 | US$ 486.5 Million |

| Globale CAGR (2018 - 2027) | 11.4% |

| Historische Daten | 2016-2017 |

| Prognosezeitraum | 2019-2027 |

| Abgedeckte Segmente |

By Vorläufertyp

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte von Kohlenstofffasern in leichten Druckbehältern: Einfluss der Marktteilnehmer auf die Geschäftsdynamik verstehen

Der Markt für Carbonfasern in leichten Druckbehältern wächst rasant. Dies ist auf die steigende Endverbrauchernachfrage zurückzuführen, die auf Faktoren wie veränderte Verbraucherpräferenzen, technologische Fortschritte und ein stärkeres Bewusstsein für die Produktvorteile zurückzuführen ist. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Markt für Kohlefasern im Leichtbau-Druckbehälter Übersicht der wichtigsten Akteure

Fusionen und Übernahmen, die Entwicklung neuer Produkte in Investitionsszenarien und andere wurden als die am häufigsten angewandten Strategien auf dem globalen Markt für Kohlefasern in leichten Druckbehältern beobachtet. Einige der jüngsten Entwicklungen auf dem globalen Markt für Kohlefasern in leichten Druckbehältern sind nachstehend aufgeführt:

- 2019: Teijin Limited stimmte der Übernahme der Renegade Materials Corporation (Renegade) zu, wodurch Teijin sein Geschäft mit Kohlefasern und Zwischenmaterialien stärken und seine Position als führender Anbieter von Lösungen für die Luft- und Raumfahrt behaupten will.

- 2018: Toray Industries Inc. schloss eine Vereinbarung mit Koninklijke Ten Cate BV über den Erwerb aller Anteile seiner Tochtergesellschaft TenCate Advanced Composites Holding BV. Diese Übernahme sollte erhebliche Synergien durch die Kombination der Produktpalette der Koninklijke Ten Cate BV mit dem Angebot an Kohlefasern und Polymertechnologien hervorbringen.

- 2017: Hexcel brachte MAXIM auf den Markt, ein neues, mit 7,4 Millionen Pfund staatlich gefördertes Unternehmen für Forschung und Entwicklung von Kohlefasergeweben, und erweiterte seine Produktionsstätte in Leicester.

GLOBALER MARKT FÜR KOHLEFASER IN LEICHTGEWICHTIGEN DRUCKBEHÄLTERN SEGMENTIERUNG

Nach Vorläufern

- Polyacrylnitril (PAN)

- Pitch

Nach Tow-Größe

- 12k bis 24k

- Über 24k

Nach Geographie

-

Nordamerika

- USA

- Kanada

- Mexiko

-

Europa

- Deutschland

- Frankreich

- Italien

- Vereinigtes Königreich

- Russland

- Rest von Europa

-

Asien Pazifik

- Australien

- China

- Indien

- Japan

- Südkorea

- Rest des asiatisch-pazifischen Raums

-

Rest der Welt

- Brasilien

- Argentinien

- Rest Südamerika (SAM)

Unternehmensprofile

- HYOSUNG CORPORATION

- Solvay

- Formosa Plastics Corporation

- Toray Industries, Inc

- Teijin Limited

- SGL Carbon

- Mitsubishi Chemical Corporation

- Kureha Corporation

- Hexcel Corporation

- Dowaksa

- Historische Analyse (2 Jahre), Basisjahr, Prognose (7 Jahre) mit CAGR

- PEST- und SWOT-Analyse

- Marktgröße Wert/Volumen – Global, Regional, Land

- Branchen- und Wettbewerbslandschaft

- Excel-Datensatz

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends

Exklusive Berichtsrabatte freischalten

Jetzt anfragen

Kostenlose Probe anfordern für - Markt für Kohlefasern im Leichtbau-Druckbehälter

Kostenlose Probe anfordern für - Markt für Kohlefasern im Leichtbau-Druckbehälter