Rapporto sul mercato della fibra di carbonio in recipienti a pressione leggeri 2027 per segmenti, geografia, dinamiche, sviluppi recenti e approfondimenti strategici

Dati storici : 2016-2017 | Anno base : 2018 | Periodo di previsione : 2019-2027Mercato della fibra di carbonio nei recipienti a pressione leggeri fino al 2027 - Analisi e previsioni globali per tipo di precursore (PAN, passo), per dimensione del rimorchio (da 12 k a 24 k, 24 k oltre) e area geografica

- Stato : Edito

- Codice del report : TIPRE00006456

- Categoria : Prodotti chimici e materiali

- Numero di pagine : 144

- Formati di report disponibili :

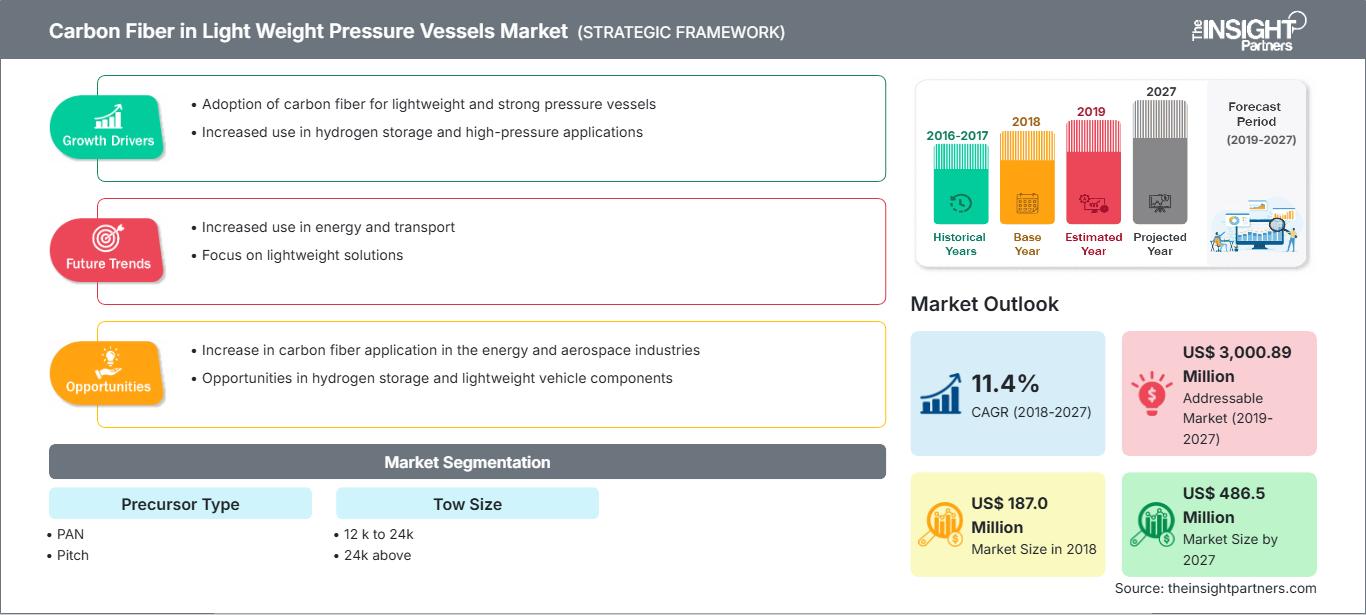

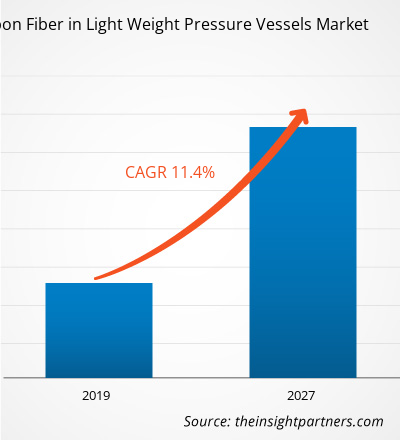

Il mercato globale della fibra di carbonio nei recipienti a pressione leggeri ha rappresentato 187,0 milioni di dollari USA nel 2018 e si prevede che crescerà a un CAGR dell'11,4% nel periodo di previsione 2019-2027, fino a raggiungere i 486,5 milioni di dollari USA entro il 2027.

La regione APAC è la regione in più rapida crescita per i recipienti a pressione in fibra di carbonio, a causa dell'aumento della popolazione e delle crescenti preoccupazioni ambientali dei governi di paesi come India, Cina e Giappone, insieme alla crescente attenzione verso veicoli CNG efficienti dal punto di vista energetico e rispettosi dell'ambiente. Inoltre, si prevede che la crescente domanda da parte dell'industria automobilistica stimolerà la crescita del mercato della fibra di carbonio nei recipienti a pressione leggeri nella regione.

Approfondimenti di mercato: la crescente domanda da parte delle applicazioni automobilistiche e industriali offre un'opportunità di crescita per il mercato della fibra di carbonio nei recipienti a pressione leggeri

La fibra di carbonio offre un elevato modulo elastico e una resistenza specifica, un'elevata resistenza alla fatica, un'elevata rigidità, una capacità di resistenza ad alta pressione, un coefficiente di dilatazione termica inferiore, resistenza alla corrosione e altre proprietà vantaggiose, che la rendono utile nei recipienti a pressione per applicazioni automobilistiche e industriali. Inoltre, si prevede che la crescente domanda di materiali leggeri, insieme alle iniziative governative per ridurre le emissioni di gas nocivi e aumentare l'efficienza del carburante, stimolerà il mercato della fibra di carbonio nei recipienti a pressione leggeri nelle applicazioni automobilistiche.

Personalizza questo rapporto in base alle tue esigenze

Potrai personalizzare gratuitamente qualsiasi rapporto, comprese parti di questo rapporto, o analisi a livello di paese, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Fibra di carbonio nel mercato dei recipienti a pressione leggeri: Approfondimenti strategici

-

Ottieni le principali tendenze chiave del mercato di questo rapporto.Questo campione GRATUITO includerà l'analisi dei dati, che vanno dalle tendenze di mercato alle stime e alle previsioni.

Si prevede che il mercato globale della fibra di carbonio nei recipienti a pressione leggeri registrerà una crescente domanda di fibre di carbonio in recipienti a tenuta stagna per lo stoccaggio di idrogeno gassoso ad alta pressione. La fibra di carbonio è considerata l'opzione migliore per la produzione di recipienti a pressione affidabili e sicuri, in quanto ha la capacità di mantenere l'elevata pressione dell'idrogeno. Grazie a ciò, le case automobilistiche globali sono sempre più coinvolte nello sviluppo di veicoli a celle a combustibile, e i rispettivi governi nazionali stanno anche fornendo supporto alla costruzione di infrastrutture per la produzione di veicoli a celle a combustibile.

Approfondimenti sui precursori

Sulla base dei precursori, il mercato globale della fibra di carbonio nei recipienti a pressione leggeri è stato segmentato in poliacrilonitrile (PAN) e pece. Il segmento del poliacrilonitrile (PAN) ha guidato il mercato globale della fibra di carbonio nei recipienti a pressione leggeri. Il poliacrilonitrile (PAN) è una fibra di carbonio che contiene circa il 68% di carbonio ed è uno dei precursori più utilizzati per le fibre di carbonio. Il PAN viene polimerizzato dall'acrilonitrile (AN) mediante inibitori comunemente utilizzati come composti azoici e perossidi attraverso il processo di polimerizzazione. La crescente domanda di fibra di carbonio nei recipienti a pressione leggeri ha portato a un'impennata nella produzione e nella produzione di PAN, essendo uno dei precursori più utilizzati.

Approfondimenti sulle dimensioni del traino

Il mercato globale della fibra di carbonio nei recipienti a pressione leggeri in base alle dimensioni del traino è stato segmentato in 12.000-24.000 e oltre 24.000. Il segmento da 12.000 a 24.000 rappresenta la quota maggiore del mercato globale della fibra di carbonio nei recipienti a pressione leggeri. La natura pesante e rigida delle fibre di carbonio da 12k a 24k si rivela vantaggiosa nelle applicazioni militari e scientifiche, un fattore determinante che contribuisce alla crescita e all'espansione della fibra di carbonio da 12k a 24k in tutto il mondo. Tra i principali produttori di fibra di carbonio da 12k a 24k figurano Toray Composite Materials America, Inc., Teijin Limited e il gruppo SGL, tra molti altri.

Fibra di carbonio nei recipienti a pressione leggeri: analisi regionali del mercato

Le tendenze regionali e i fattori che influenzano il mercato della fibra di carbonio nei recipienti a pressione leggeri durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di The Insight Partners. Questa sezione illustra anche i segmenti e la geografia del mercato della fibra di carbonio nei recipienti a pressione leggeri in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa, America meridionale e centrale.

Ambito del rapporto di mercato sulla fibra di carbonio nei recipienti a pressione leggeri

| Attributo del rapporto | Dettagli |

|---|---|

| Dimensioni del mercato in 2018 | US$ 187.0 Million |

| Dimensioni del mercato per 2027 | US$ 486.5 Million |

| CAGR globale (2018 - 2027) | 11.4% |

| Dati storici | 2016-2017 |

| Periodo di previsione | 2019-2027 |

| Segmenti coperti |

By Tipo di precursore

|

| Regioni e paesi coperti |

Nord America

|

| Leader di mercato e profili aziendali chiave |

|

Fibra di carbonio nei recipienti a pressione leggeri: densità degli attori del mercato: comprendere il suo impatto sulle dinamiche aziendali

Il mercato della fibra di carbonio nei recipienti a pressione leggeri è in rapida crescita, trainato dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

- Ottieni il Fibra di carbonio nel mercato dei recipienti a pressione leggeri Panoramica dei principali attori chiave

Fusioni e acquisizioni, scenari di investimento, sviluppo di nuovi prodotti e altre sono state osservate come le strategie più adottate nel mercato globale della fibra di carbonio nei recipienti a pressione leggeri. Di seguito sono elencati alcuni degli sviluppi recenti nel mercato globale della fibra di carbonio nei recipienti a pressione leggeri:

- 2019: Teijin Limited ha accettato di acquisire Renegade Materials Corporation (Renegade), attraverso la quale Teijin mira a rafforzare le sue attività in fibra di carbonio e materiali intermedi per mantenere la sua posizione di fornitore leader di soluzioni per applicazioni aerospaziali.

- 2018: Toray Industries Inc. ha stipulato un accordo con Koninklijke Ten Cate BV per l'acquisto di tutte le azioni della sua controllata TenCate Advanced Composites Holding BV. Si prevedeva che questa acquisizione avrebbe prodotto sinergie sostanziali combinando la gamma di prodotti di quest'ultima con la gamma di fibre di carbonio insieme alle tecnologie polimeriche.

- 2017: Hexcel ha lanciato MAXIM, un nuovo governo supportato da 7,4 milioni di sterline in ricerca e sviluppo di tessuti in fibra di carbonio e ha ampliato il suo stabilimento di produzione a Leicester.

FIBRA DI CARBONIO GLOBALE NEI RECIPIENTI A PRESSIONE LEGGERI SEGMENTAZIONE DEL MERCATO

Per precursori

- Poliacrilonitrile (PAN)

- Passo

Per dimensione di traino

- Da 12k a 24k

- Sopra 24k

Per area geografica

-

Nord America

- Stati Uniti

- Canada

- Messico

-

Europa

- Germania

- Francia

- Italia

- Regno Unito

- Russia

- Resto dell’Europa

-

Asia Pacifico

- Australia

- Cina

- India

- Giappone

- Corea del Sud

- Resto dell'Asia-Pacifico

-

Resto del mondo

- Brasile

- Argentina

- Resto del Sud America (SAM)

Profili aziendali

- HYOSUNG CORPORATION

- Solvay

- Formosa Plastics Corporation

- Toray Industries, Inc

- Teijin Limited

- SGL Carbon

- Mitsubishi Chemical Corporation

- Kureha Corporation

- Hexcel Corporation

- Dowaksa

- Analisi storica (2 anni), anno base, previsione (7 anni) con CAGR

- Analisi PEST e SWOT

- Valore/volume delle dimensioni del mercato - Globale, Regionale, Nazionale

- Industria e panorama competitivo

- Set di dati Excel

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative

Sblocca sconti esclusivi sui report

Richiedi ora

Ottieni un campione gratuito per - Fibra di carbonio nel mercato dei recipienti a pressione leggeri

Ottieni un campione gratuito per - Fibra di carbonio nel mercato dei recipienti a pressione leggeri