Wachstum, Größe, Anteil, Trends, Analyse der wichtigsten Akteure und Prognose des Connected Health-Marktes bis 2031

Marktgröße und Prognose für Connected Health (2021–2031), Bericht über globale und regionale Anteile, Trends und Wachstumschancenanalyse: Nach Produkttyp (M-Health-Dienste und M-Health-Geräte); Anwendung (Überwachungsanwendungen, Aufklärung und Bewusstsein, Wellness und Prävention, Gesundheitsmanagement und andere); Endbenutzer (Krankenhäuser und Kliniken, Heimüberwachung und andere) und Geografie

- Status : Veröffentlicht

- Berichtscode : TIPRE00002975

- Kategorie : Technologie, Medien und Telekommunikation

- Anzahl der Seiten : 255

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : October 08, 2025

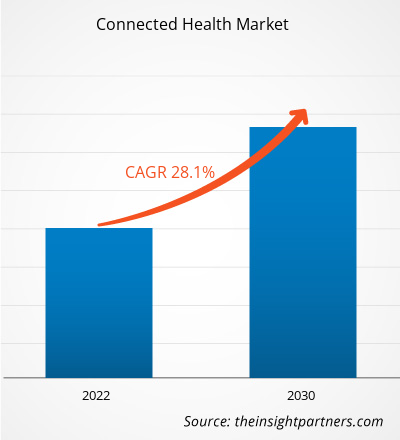

[Forschungsbericht] Der Markt für vernetzte Gesundheit wurde im Jahr 2022 auf 62,61 Milliarden US-Dollar geschätzt und soll bis 2030 453,56 Milliarden US-Dollar erreichen. Der Markt wird von 2022 bis 2030 voraussichtlich eine durchschnittliche jährliche Wachstumsrate (CAGR) von 28,1 % verzeichnen.

Markteinblicke und Analystenmeinung:

Zahlreiche Gesundheitsorganisationen finden aufgrund der Nachfrage nach Mehrwert und eines zunehmend wettbewerbsorientierten Umfelds neue und effizientere Wege, die Qualität ihrer Behandlungen zu verbessern. Die Ermöglichung einer jederzeit und überall verfügbaren Konnektivität zwischen Patient und Arzt ist eine Möglichkeit, Dienstleistungen zugänglicher und möglicherweise kostengünstiger zu machen. Ferndiagnose, -behandlung, -überwachung und -kommunikation sind mit Connected Health (cHealth), einem integrierten, technologiegestützten Gesundheitsversorgungssystem, möglich. Faktoren wie die zunehmende Verbreitung von Digital Health und das mAgeing-Programm der WHO treiben das Wachstum des Connected-Health-Marktes voran.

Markttreiber:

Digital Health trägt dazu bei, die Gesundheitsversorgung handhabbarer und einfacher zu machen, indem es gesundheitsbezogene Daten oder Gesundheitsinformationen sammelt und Patienten Dienstleistungen anbietet. Connected-Health-Technologie ist ein Werkzeug, das Behandlungen, das Management chronischer Krankheiten und die Krankheitsüberwachung unterstützt. Die Zahl chronischer Krankheiten, darunter Herzkrankheiten, Diabetes und Krebs, steigt aufgrund veränderter Lebensstile. Für Patienten mit nicht übertragbaren Krankheiten, die ständig überwacht werden müssen, spielt Digital Health eine Schlüsselrolle bei der Erfüllung dieser Anforderungen. In vielen Fällen hat sich das Management chronischer Krankheiten durch Fernüberwachung mittels M-Health-Technologien und Datenauswertung über digitale Tools und Wearables verändert. Neben der Verlagerung des Schwerpunkts von der akuten und reaktiven Versorgung zur proaktiven und präventiven Versorgung hat Connected Health die Art und Weise verändert, wie Patienten mit Gesundheitsdienstleistern und gesundheitsbasierten Systemen interagieren. Die zunehmende Entwicklung und Implementierung von Technologien, die digitale Gesundheitsversorgung erschwinglich und komfortabel machen, hat zu ihrer Verbreitung beigetragen.

Die zunehmende Informationstechnologie führt zu einer steigenden Verbreitung im Gesundheitssektor und trägt dazu bei, dass die vernetzte Gesundheitsversorgung weltweit rasant wächst. Im Bereich mHealth spielen Geräte wie Mobiltelefone, Laptops und Tablets eine wichtige Rolle bei der Verbesserung der Gesundheitsversorgung. Aufgrund der zunehmenden Mobiltechnologie setzen Regierungen und andere Organisationen auf mobile Geräte, um ihre Produktivität zu steigern und gleichzeitig ihre Leistungsfähigkeit zu bündeln, um aktuelle Gesundheitsdaten zeitnah zu nutzen. Die rasante Entwicklung fortschrittlicher Technologien ermöglicht einen verstärkten Datenaustausch zwischen elektronischen Systemen. Die zunehmende Sicherheit von Gesundheitsdaten hilft Nutzern, genaue Daten zu erhalten, und ermöglicht Entscheidungsträgern, kritische Entscheidungen besser zu treffen. Dank des einfachen Zugangs und der großen Anwendungsvielfalt können viele Menschen digitale Gesundheitsdienste nutzen, was das Wachstum des vernetzten Gesundheitsmarktes voraussichtlich ankurbeln wird.

Die Einführung des Internet of Medical Things (IoMT) dürfte in den kommenden Jahren neue Trends im vernetzten Gesundheitsmarkt mit sich bringen. Viele Gesundheitsorganisationen bergen jedoch Risiken, die zu Verletzungen des Schutzes persönlicher Gesundheitsdaten führen können, und bieten keine Richtlinien zum Schutz elektronischer persönlicher Gesundheitsinformationen. Die steigenden Bedrohungen durch die Nutzung dieser Dienste erhöhen daher proportional die Gesundheitsdatensicherheit, die den vernetzten Gesundheitsmarkt einschränkt.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Vernetzter Gesundheitsmarkt: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

Segmentierung und Umfang des Berichts:

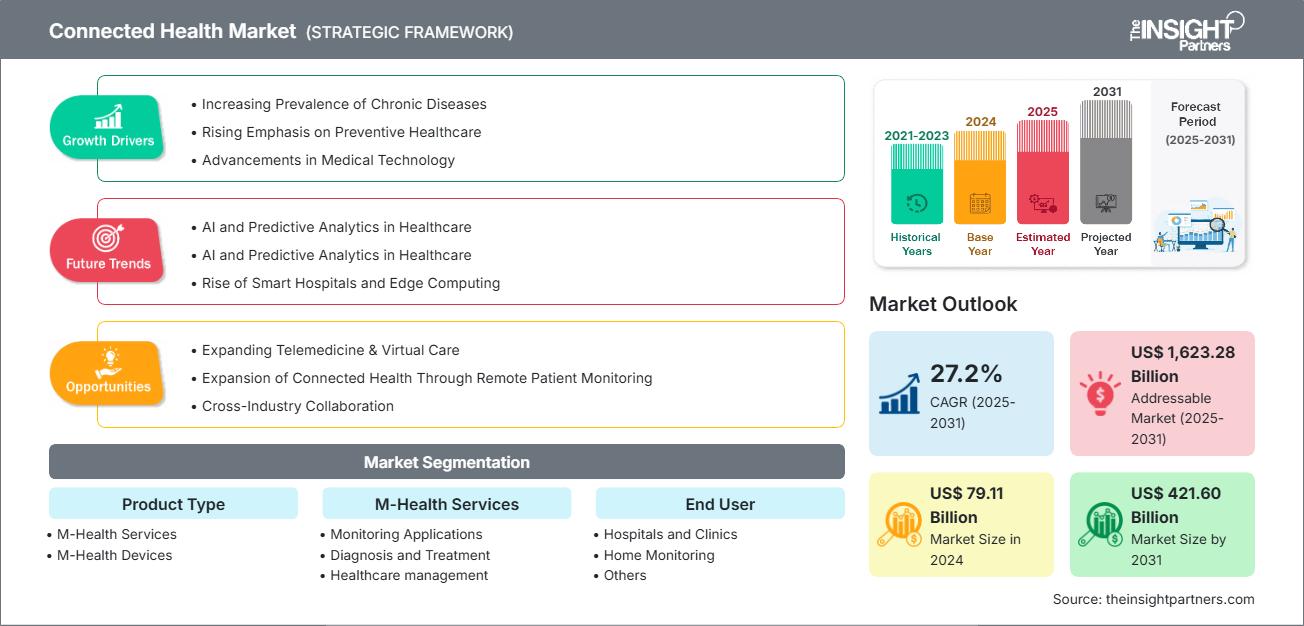

Die „Marktanalyse für vernetzte Gesundheit“ wurde unter Berücksichtigung der folgenden Segmente durchgeführt: Typ, Anwendung und Endbenutzer. Nach Typ ist der Markt in M-Health-Dienste und M-Health-Geräte unterteilt. Nach Anwendung ist der Markt in Überwachungsanwendungen, Diagnose und Behandlung, Gesundheitsmanagement, Wellness und Prävention und Sonstiges segmentiert. Basierend auf dem Endbenutzer ist der Markt in Krankenhäuser und Kliniken, Heimüberwachung und Sonstiges kategorisiert.

Segmentanalyse:

Der Markt für vernetzte Gesundheit ist nach Typ in M-Health-Dienste und M-Health-Geräte unterteilt. Das Segment M-Health-Dienste hatte 2022 einen größeren Marktanteil; das Segment M-Health-Geräte wird jedoch zwischen 2022 und 2030 voraussichtlich eine höhere durchschnittliche jährliche Wachstumsrate (CAGR) im Markt für vernetzte Gesundheit verzeichnen. Anstatt Patienten in medizinischen Einrichtungen intern zu überwachen, legt Connected Health mehr Wert auf die Ferndatenübertragung und die Bereitstellung geeigneter Gesundheitsdienste zu Hause. Neben der Möglichkeit, Gesundheitsversorgung aus der Ferne zu leisten, ist der größte Durchbruch im Bereich Connected Health die enorme Datenmenge, die dadurch zur Verfügung gestellt wird. Mithilfe von Connected-Health-Diensten können Ärzte fundiertere Entscheidungen treffen und eine proaktive Behandlung anbieten, die die Bedürfnisse der Patienten in den Vordergrund stellt.

Nach Anwendung ist der Markt für Connected Health in Überwachungsanwendungen, Diagnose und Behandlung, Gesundheitsmanagement, Wellness und Prävention und weitere segmentiert. Das Segment Überwachungsanwendungen hatte 2022 den größten Marktanteil; das Segment Diagnose und Behandlung dürfte jedoch zwischen 2022 und 2030 die höchste durchschnittliche jährliche Wachstumsrate im Markt für Connected Health verzeichnen. Fernüberwachungssysteme, die mit dem Internet der Dinge (IoT), digitalen Sensoren und Big-Data-Tools integriert sind, verbessern den Zugang zu Patienten, was neue Möglichkeiten eröffnet, die sich auf die Verbesserung der Gesundheitsversorgung konzentrieren. Die Integration dieser Systeme hat während der COVID-19-Krise deutlich zugenommen. Gesundheitsfernüberwachungssysteme (HRMS) bieten verschiedene Vorteile, darunter eine geringere Patientenbelastung in Gesundheitszentren und Krankenhäusern.

Der Markt für vernetzte Gesundheit ist nach Endnutzern in Krankenhäuser und Kliniken, Heimüberwachung und andere segmentiert. Im Jahr 2022 dominierte das Segment Krankenhäuser und Kliniken den Marktanteil im Bereich vernetzte Gesundheit. Es wird jedoch erwartet, dass das Segment Heimüberwachung zwischen 2022 und 2030 die höchste durchschnittliche jährliche Wachstumsrate (CAGR) verzeichnen wird. Laut OAE Publishing Inc. haben im Jahr 2021 etwa die Hälfte aller amerikanischen Krankenhäuser irgendeine Form von Connected Health zur Fernüberwachung von Patienten implementiert, und etwa 80 % der europäischen Länder haben Telemedizindienste in ihre Gesundheitsdienste aufgenommen.

Regionale Analyse:

Der Umfang des Berichts zum Connected-Health-Markt ist hauptsächlich in Nordamerika (USA, Kanada und Mexiko), Europa (Spanien, Großbritannien, Deutschland, Frankreich, Italien und das übrige Europa), Asien-Pazifik (Südkorea, China, Indien, Japan, Australien und der übrige Asien-Pazifik-Raum), Naher Osten und Afrika (Südafrika, Saudi-Arabien, die Vereinigten Arabischen Emirate und der übrige Nahe Osten und Afrika) sowie Süd- und Mittelamerika (Brasilien, Argentinien und der übrige Süd- und Mittelamerika) unterteilt.

In Bezug auf den Umsatz dominierte Nordamerika im Jahr 2022 den Marktanteil im Bereich Connected Health. Der Markt im Asien-Pazifik-Raum wird zwischen 2022 und 2030 voraussichtlich die höchste durchschnittliche jährliche Wachstumsrate verzeichnen. Der Markt im asiatisch-pazifischen Raum wächst aufgrund steigender Investitionen internationaler Akteure in Indien und China, der Ausweitung von CRO-Diensten, der Verbesserung der Gesundheitsinfrastruktur und der Verbesserung der staatlichen Unterstützung. Darüber hinaus führte Apollo 2023 das Comprehensive Connected Care Programme in Indien ein. Dieses Programm nutzt die hochmoderne Connected Care-Technologie von Apollo. Die Comprehensive Connected Care-Dienste von Apollo werden landesweit eingeführt und bieten klinischen Teams und Pflegepersonal Zugang zu einem umfassenden und aktuellen Patientenüberblick in jeder Phase der Patientenversorgung, einschließlich der häuslichen Pflege, der postoperativen Versorgung, der stationären Versorgung sowie des Notfall- und Krankentransports.

Connected Health

Regionale Einblicke in den Connected Health-MarktDie Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Markt für vernetzte Gesundheitsversorgung im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Lage in Nordamerika, Europa, dem asiatisch-pazifischen Raum, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika erörtert.

Umfang des Marktberichts zum Thema Connected Health

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2024 | US$ 79.11 Billion |

| Marktgröße nach 2031 | US$ 421.60 Billion |

| Globale CAGR (2025 - 2031) | 27.2% |

| Historische Daten | 2021-2023 |

| Prognosezeitraum | 2025-2031 |

| Abgedeckte Segmente |

By Produkttyp

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Akteure im Connected Health-Markt: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für vernetzte Gesundheitslösungen wächst rasant. Die steigende Nachfrage der Endnutzer ist auf Faktoren wie veränderte Verbraucherpräferenzen, technologische Fortschritte und ein stärkeres Bewusstsein für die Produktvorteile zurückzuführen. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Vernetzter Gesundheitsmarkt Übersicht der wichtigsten Akteure

Wettbewerbslandschaft und Schlüsselunternehmen:

Der Bericht zum Connected-Health-Markt konzentriert sich auf führende Akteure wie Athena Health, AgaMatrix, AirStrip, AliveCor Inc, Allscripts Healthcare LLC, Apple Inc, NXGN Management LLC, Cerner Corporation, Cognizant und Honeywell International Inc. Die Marktprognose für Connected Health kann Stakeholdern bei der Planung ihrer Wachstumsstrategien helfen. Diese Unternehmen konzentrieren sich auf neue Technologien, die Verbesserung bestehender Produkte und Markterweiterungen, um der weltweit wachsenden Verbrauchernachfrage gerecht zu werden.

- Im Dezember 2023 schlossen GE HealthCare und AirStrip eine gemeinsame Vermarktungsvereinbarung. GE HealthCare wurde der exklusive Vertriebspartner von AirStrip-Lösungen für Kardiologie und Patientenüberwachung in den USA und bietet Gesundheitssystemen Datenvisualisierungstechnologie an.

- Im Januar 2023 ging BioIntelliSense eine Partnerschaft mit care.ai ein, um die hochfrequenten Vitaldaten-Trenddaten und die algorithmenbasierte Alarmierung von BioIntelliSense in die Ambient-Monitoring-Workflows von care.ai zu integrieren. Die Partnerschaft verbindet die komplementären Fähigkeiten dieser transformativen Technologien, um die Patientenzufriedenheit zu verbessern, klinische Abläufe zu optimieren und die wichtigsten Herausforderungen des überlasteten Gesundheitspersonals direkt anzugehen.

Ankita ist eine dynamische Marktforschungs- und Beratungsexpertin mit über 8 Jahren Erfahrung in den Bereichen Technologie, Medien, IKT sowie Elektronik und Halbleiter. Sie hat über 100 Beratungs- und Forschungsaufträge für globale Kunden wie Microsoft, Oracle, NEC Corporation, SAP, KPMG und Expeditors International erfolgreich geleitet und durchgeführt. Zu ihren Kernkompetenzen gehören Marktbewertung, Datenanalyse, Prognose, Strategieformulierung, Wettbewerbsbeobachtung und das Verfassen von Berichten. Ankita ist versiert in der Abwicklung kompletter Projektzyklen – von der Angebotserstellung vor dem Verkauf und Kundengesprächen bis hin zur Bereitstellung umsetzbarer Erkenntnisse nach dem Verkauf. Sie ist versiert in der Leitung funktionsübergreifender Teams, der Strukturierung komplexer Forschungsmodule und der Ausrichtung von Lösungen an kundenspezifischen Geschäftszielen. Ihre ausgezeichneten Kommunikationsfähigkeiten, Führungsqualitäten und Präsentationsfähigkeiten haben es ihr ermöglicht, in einem schnelllebigen und sich entwickelnden Marktumfeld stets wertorientierte Ergebnisse zu liefern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends