Markt für Milchalternativen – Erkenntnisse durch globale und regionale Analyse – Prognose bis 2031

Marktgröße und Prognose für Milchalternativen (2021–2031), Bericht über globale und regionale Anteile, Trends und Wachstumschancenanalysen: Nach Quelle (Soja, Mandel, Kokosnuss, Hafer und andere), Produkttyp (Milch, Eiscreme, Joghurt, Käse und andere), Vertriebskanal (Supermärkte und Hypermärkte, Convenience Stores, Online-Einzelhandel und andere) und Geografie

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00004533

- Kategorie : Speisen und Getränke

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : May 16, 2024

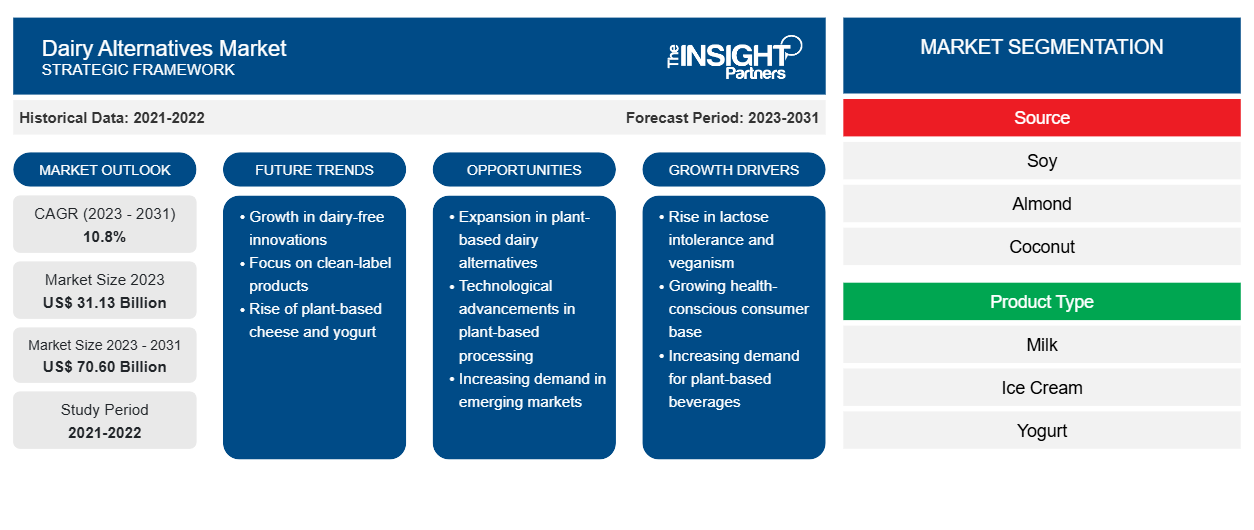

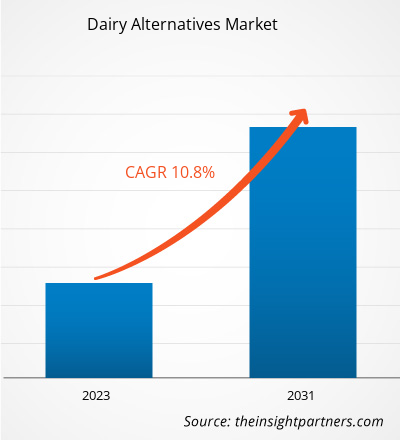

Der Markt für Milchalternativen soll von 31,13 Milliarden US-Dollar im Jahr 2023 auf 70,60 Milliarden US-Dollar im Jahr 2031 anwachsen. Für den Zeitraum 2023–2031 wird ein durchschnittliches jährliches Wachstum von 10,8 % erwartet. Die steigende Nachfrage nach funktionellen Milchalternativen dürfte ein wichtiger Trend auf dem Markt bleiben.CAGR of 10.8% during 2023–2031. Surging demand for functional dairy alternatives is likely to remain a key trend in the market.

Marktanalyse für Milchalternativen

Die vegane Bevölkerung ist in den letzten Jahren deutlich gewachsen. Laut Veganuary (einer gemeinnützigen Organisation, die Menschen weltweit dazu ermutigt, den gesamten Januar über vegan zu leben) haben sich im Jahr 2022 mehr als 620.000 Menschen für die Veganuary-Kampagne registriert, und die Registrierungen sind in den letzten 3 Jahren um 200 % gestiegen. Aufgrund gestiegener Gesundheits- und Nachhaltigkeitsbedenken stellen immer mehr Menschen auf eine vegane Ernährung um. Die Viehwirtschaft ist einer der Hauptverursacher der gesamten menschengemachten Treibhausgasemissionen. Laut der Ernährungs- und Landwirtschaftsorganisation (FAO) stößt die weltweite Viehwirtschaft 7,1 Gigatonnen Kohlendioxid pro Jahr aus, was 14,5 % aller vom Menschen verursachten Treibhausgasemissionen entspricht. Der Milchsektor ist für 30 % der gesamten Viehwirtschaftsemissionen verantwortlich.Veganuary (a non-profit organization that encourages individuals worldwide to go vegan for the entire month of January), more than 620,000 people registered for the Veganuary campaign in 2022, and the registrations increased by 200% in the last 3 years. People are increasingly switching to a vegan diet due to increased health and sustainability concerns. The livestock industry is one of the significant contributors to the total anthropogenic greenhouse gas emissions. According to the Food and Agriculture Organization (FAO), the worldwide livestock industry emits 7.1 gigatons of carbon dioxide per year, accounting for 14.5% of all human-caused greenhouse gas emissions. The dairy sector is responsible for 30% of the total livestock emissions.

Zahlreiche Studien haben gezeigt, dass die Umstellung auf eine vegane Ernährung die Kohlendioxidemissionen deutlich senken kann. Laut Dr. Fredrik Hedenus, Professor an der Chalmers University of Technology in Schweden und Co-Autor einer in der Zeitschrift „Climate Change“ veröffentlichten Forschungsarbeit über Fleisch- und Milchkonsum, kann die Reduzierung des Konsums von Fleisch und Milchprodukten entscheidend dazu beitragen, die landwirtschaftliche Klimaverschmutzung auf ein akzeptables Niveau zu senken.

Darüber hinaus glauben viele Organisationen wie die Vereinten Nationen, PETA und das Good Food Institute, dass Veganismus dazu beitragen kann, den Planeten vor der Klimakrise zu retten. Das Bewusstsein für die schädlichen Auswirkungen der Viehwirtschaft auf die Umwelt nimmt bei den Verbrauchern zu. Der Verzehr pflanzlicher Milchprodukte trägt dazu bei, den CO2-Fußabdruck zu minimieren, Wasser und andere natürliche Ressourcen zu sparen und die allgemeinen Umweltauswirkungen zu verringern. Daher steigen die Verbraucher schnell auf pflanzliche Milch- und Fleischprodukte um. Dieser Faktor treibt den Markt für Milchalternativen erheblich an.

Marktübersicht für Milchalternativen

Milchalternativen wie Milch, Joghurt, Eiscreme, Käse und Butter werden aus Sojamilch, Erbsenmilch und Kokosmilch hergestellt. Sojamilch ist günstiger als andere Pflanzenmilch und bietet eine ähnliche Menge an Protein wie Vollmilch. Aufgrund zunehmender gesundheitlicher Bedenken und eines wachsenden Bewusstseins für den Tierschutz neigen Verbraucher stark zu pflanzlichen oder veganen Produkten. Pflanzliche Produkte werden allgemein als gesündere Alternativen wahrgenommen. Darüber hinaus wirkt sich die Milchwirtschaft negativ auf die Umwelt insgesamt aus und führt zum Klimawandel. Dieser Faktor beeinflusst auch das Wachstum des Marktes für Milchalternativen.soymilk, pea milk, , and coconut milk. Soymilk is more affordable than other plant milk, and it provides a similar amount of protein as whole milk. Consumers are highly inclined toward plant-based or vegan-friendly products due to increasing health concerns and growing awareness of animal welfare. Plant-based products are generally perceived to be healthier alternatives. Moreover, dairy farming is negatively impacting the overall environment leading to climate change. This factor is also influencing the growth of the dairy alternatives market.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlose Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für Milchalternativen: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Markttreiber und Chancen für Milchalternativen

Steigende Fälle von Laktoseintoleranz begünstigen den Markt

Laut dem National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK) leiden durchschnittlich 68 % der Weltbevölkerung an Laktoseintoleranz . Laut dem National Institute of Health (NIH) ist Laktoseintoleranz bei der erwachsenen Bevölkerung Ostasiens recht verbreitet und betrifft 75–95 % der Menschen in diesen Gemeinschaften. Darüber hinaus ist angeborener Laktosemangel im asiatisch-pazifischen Raum und in Afrika weit verbreitet. Daher sind Länder wie China, Japan, Südkorea und Taiwan potenzielle Märkte für Milchalternativen.

Pflanzliche Milchprodukte haben eine ähnliche Textur, Cremigkeit und Konsistenz wie herkömmliche Milchprodukte. Sie sind mit Nährstoffen wie Protein und Kalzium angereichert, um den täglichen Nährstoffbedarf der Verbraucher zu decken. Daher treibt die zunehmende Verbreitung von Laktoseintoleranz und Milchallergien bei Verbrauchern den Markt für Milchalternativen an.

Zunehmende Anzahl neuer Produkteinführungen bietet enorme Wachstumschancen

Hersteller von Milchalternativen investieren erheblich in Produktinnovationen, um eine große Gruppe von Verbrauchern anzusprechen. Eine Produktinnovationsstrategie verschafft den Akteuren auf dem Markt einen Wettbewerbsvorteil und steigert ihre Rentabilität. Die Hersteller von Milchalternativen bieten zertifizierte Bio-, gentechnikfreie, glutenfreie, Clean-Label- und allergenfreie Produkte an, um den neuen Kundenanforderungen gerecht zu werden. Darüber hinaus bevorzugen Verbraucher, da sie gesundheitsbewusst geworden sind , kalorien- und fettarme Produkte. Daher bieten Hersteller von pflanzlichen Milchprodukten ungesüßte und zuckerarme Produkte an. So brachte Hasla Foods im Februar 2021 einen zuckerfreien Hafermilchjoghurt in einer 24-oz-Familiengröße auf den Markt. Das Produkt enthält nur 90 Kalorien pro Portion und keinen zugesetzten Zucker. Im Juni 2021 erweiterte dasselbe Unternehmen seine Einzelhandelspräsenz, indem es seine Produkte in 160 National Grocers by Vitamin Cottage-Filialen in den USA anbietet.

Darüber hinaus experimentieren Hersteller mit verschiedenen pflanzlichen Milchquellen wie Gerste, Erbsen, Hanf, Chiasamen, Bananen und Cashews. Take Two Foods, einer der wichtigsten Hersteller pflanzlicher Milch, bietet beispielsweise nährstoffangereicherte Gerstenmilch an, die ein vollständiges Nährstoffportfolio wie Protein, Ballaststoffe, Kalzium und ungesättigte Fette enthält. Solche Strategien dürften dem Markt für Milchalternativen im Prognosezeitraum lukrative Möglichkeiten bieten.

Marktbericht zu Milchalternativen – Segmentierungsanalyse

Wichtige Segmente, die zur Ableitung der Marktanalyse für Milchalternativen beigetragen haben, sind Quelle, Produkttyp und Vertriebskanal.

- Der Markt für Milchalternativen ist nach Herkunft in Soja, Mandeln, Kokosnüsse, Hafer und andere unterteilt. Das Sojasegment hatte 2023 den größten Marktanteil. Soja wird voraussichtlich bei älteren und weiblichen Verbrauchern in den USA an Beliebtheit gewinnen, da es Isoflavone enthält, die das Risiko von Herzerkrankungen und Brustkrebs senken sollen. Soja enthält auch Phytoöstrogen, ein Hormon, das bei Frauen ähnlich wie Östrogen wirkt. Der Verzehr von Milchalternativen auf Sojabasis ist bei Frauen als alternative Therapie zur Erhöhung des Östrogenspiegels beliebt. Soja ist reich an Nährstoffen und hat im Vergleich zu anderen Milchalternativen einen hohen Proteingehalt; daher treibt die Beliebtheit von Soja aufgrund seiner Vorteile den Markt für dieses Segment im Prognosezeitraum an.

In Bezug auf die Vertriebskanäle ist der Markt in Supermärkte und Hypermärkte, Convenience Stores, Online-Einzelhandel und andere unterteilt. Das Segment Supermärkte und Hypermärkte dominierte den Markt im Jahr 2023. Supermärkte und Hypermärkte sind große Einzelhandelsgeschäfte, die ein breites Sortiment an Lebensmitteln, Nahrungsmitteln, Getränken und anderen Haushaltswaren anbieten. In diesen Geschäften sind Produkte verschiedener Marken zu angemessenen Preisen erhältlich, sodass die Käufer schnell das richtige Produkt finden können. Darüber hinaus bieten diese Geschäfte attraktive Rabatte, mehrere Zahlungsoptionen und ein angenehmes Kundenerlebnis. Supermärkte und Hypermärkte konzentrieren sich darauf, den Produktabsatz zu maximieren, um ihre Gewinnspannen zu erhöhen. Hersteller pflanzlicher Milchprodukte ziehen es in der Regel vor, ihre Produkte über Supermärkte und Hypermärkte zu verkaufen, da diese Geschäfte eine hohe Kundenfrequenz aufweisen. Die zunehmende Urbanisierung, die steigende Arbeiterbevölkerung und wettbewerbsfähige Preise steigern die Beliebtheit von Supermärkten und Hypermärkten in entwickelten und sich entwickelnden Regionen.

Marktanteilsanalyse für Milchalternativen nach geografischer Lage

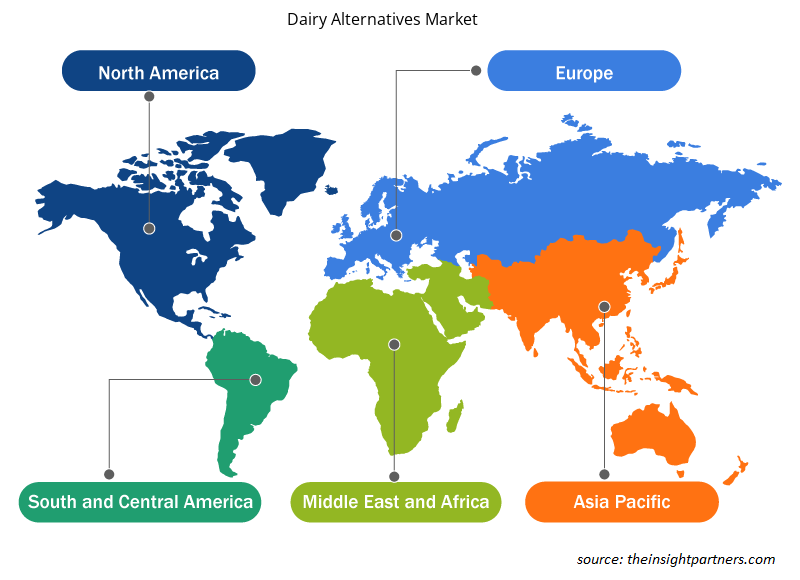

Der geografische Umfang des Marktberichts für Milchalternativen ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten und Afrika sowie Südamerika/Süd- und Mittelamerika.

Der Markt für Milchalternativen im asiatisch-pazifischen Raum hatte 2023 den größten Marktanteil. In den letzten Jahren ist der Konsum von Milchalternativen aufgrund der wachsenden Zahl laktoseintoleranter Menschen und gesundheitlicher Bedenken hinsichtlich Antibiotika und Wachstumshormonen, die häufig in Kuhmilch enthalten sind, stetig gestiegen. Die von Rakuten im Jahr 2021 durchgeführte Untersuchung ergab, dass 87 % der Verbraucher in China pflanzliche Milch, 50 % andere Milchersatzprodukte, 42 % pflanzliches Fleisch und 32 % vegane Eiersatzprodukte probiert hatten. Darüber hinaus ergab die gleiche Untersuchung, dass 3 % der Befragten nur pflanzliche Lebensmittel konsumieren. Der Markt für Milchalternativen wächst also aufgrund der steigenden Nachfrage nach pflanzlichen Milchprodukten aufgrund der zunehmenden Verbreitung von Laktoseintoleranz im gesamten asiatisch-pazifischen Raum.

Regionale Einblicke in den Markt für Milchalternativen

Die regionalen Trends und Faktoren, die den Markt für Milchalternativen im Prognosezeitraum beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch Marktsegmente und Geografie für Milchalternativen in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zum Markt für Milchalternativen

Umfang des Marktberichts zu Milchalternativen

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2023 | 31,13 Milliarden US-Dollar |

| Marktgröße bis 2031 | 70,60 Milliarden US-Dollar |

| Globale CAGR (2023 - 2031) | 10,8 % |

| Historische Daten | 2021-2022 |

| Prognosezeitraum | 2023–2031 |

| Abgedeckte Segmente |

Nach Quelle

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte von Milchalternativen: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Milchalternativen wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung der Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten Unternehmen auf dem Markt für Milchalternativen sind:

- SunOpta

- Blaue Diamantenzüchter

- Nestlé SA

- Danone SA

- Oatly Inc

- Califia Farms, LLC

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Markt für Milchalternativen

Marktnachrichten und aktuelle Entwicklungen zu Milchalternativen

Der Markt für Milchalternativen wird durch die Erhebung qualitativer und quantitativer Daten nach Primär- und Sekundärforschung bewertet, die wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken umfasst. Im Folgenden finden Sie eine Liste der Entwicklungen auf dem Markt für Sprach- und Sprechstörungen:

- Die pflanzliche Milchmarke Milkadamia zieht in den Kühlbereich ein und beweist mit der Einführung ihrer Bio-Macadamiamilch und -mischungen, die auf Füllstoffe und Gummis verzichtet, die in vielen milchfreien Getränken üblich sind, „weniger ist mehr“, und reagiert auf die wachsende Nachfrage nach hausgemachteren Alternativen. (Quelle: Dairy Alternatives – Milkadamia, Pressemitteilung/Unternehmenswebsite/Newsletter, 2024)

- Califia Farms hat Califia Farms Complete auf den Markt gebracht, eine cremige Pflanzenmilch mit neun essentiellen Nährstoffen, acht Gramm Protein, allen neun essentiellen Aminosäuren und der Hälfte des Zuckers von Kuhmilch, erklärte das Unternehmen. (Quelle: Dairy Alternatives Califia Farms LLC, Pressemitteilung/Unternehmenswebsite/Newsletter, 2024)

Marktbericht zu Milchalternativen: Umfang und Ergebnisse

Der Bericht „Marktgröße und Prognose für Milchalternativen (2023–2031)“ bietet eine detaillierte Analyse des Marktes, die die folgenden Bereiche abdeckt:

- Marktgröße und Prognose auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Projekts abgedeckt sind

- Marktdynamik wie Treiber, Beschränkungen und wichtige Chancen

- Wichtige Zukunftstrends

- Detaillierte PEST/Porters Five Forces- und SWOT-Analyse

- Globale und regionale Marktanalyse mit wichtigen Markttrends, wichtigen Akteuren, Vorschriften und aktuellen Marktentwicklungen

- Branchenlandschaft und Wettbewerbsanalyse, einschließlich Marktkonzentration, Heatmap-Analyse, prominenten Akteuren und aktuellen Entwicklungen

- Detaillierte Firmenprofile

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends