Markt für CMOs im Gesundheitswesen, Marktgröße für CMOs im Gesundheitswesen, Marktanteil für CMOs im Gesundheitswesen, Marktprognose für CMOs im Gesundheitswesen, Wachstum des Marktes für CMOs im Gesundheitswesen, Marktanalyse für CMOs im Gesundheitswesen Marktanalyse und Prognose nach Größe, Anteil, Wachstum, Trends CAGR von 13,7 %

Marktgröße und Prognose für CMOs im Gesundheitswesen (2021 – 2031), Berichtsabdeckung für globale und regionale Anteile, Trends und Wachstumschancenanalyse: Nach Dienstleistung (Pharmazeutische Auftragsfertigungsdienste und Auftragsfertigungsdienste für Medizinprodukte) und Geografie (Nordamerika, Europa, Asien-Pazifik, Naher Osten und Afrika sowie Süd- und Mittelamerika)

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00003263

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : February 15, 2025

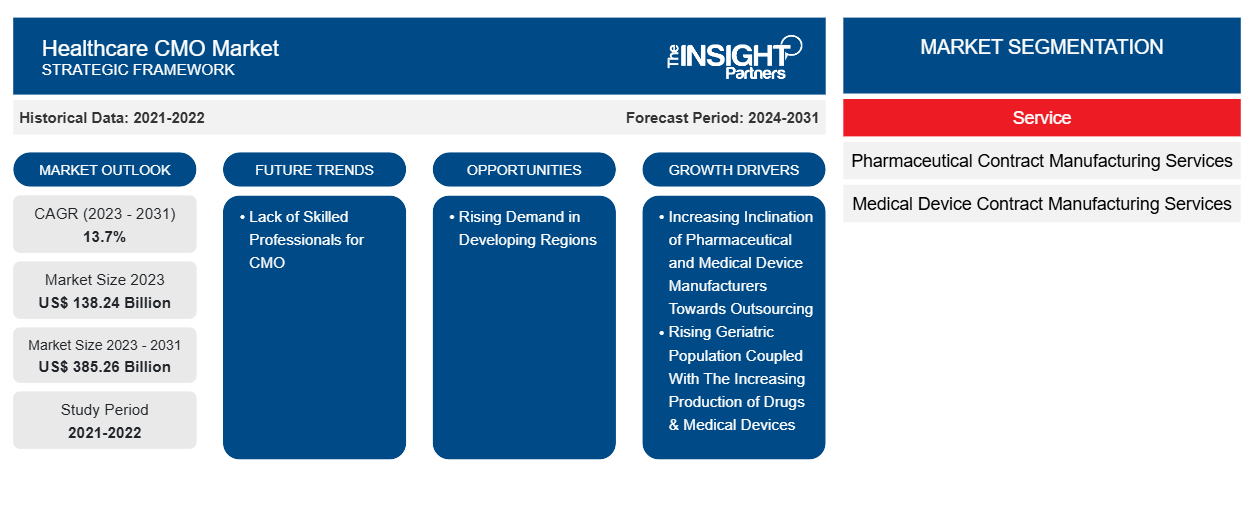

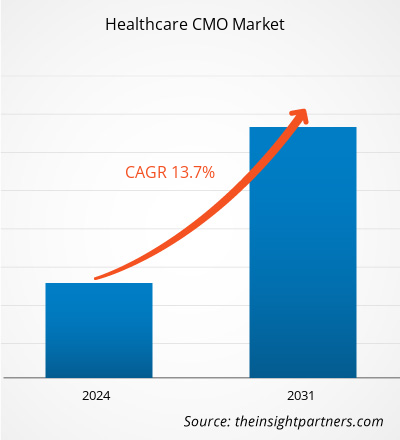

Der Markt für CMOs im Gesundheitswesen wird voraussichtlich von 138,24 Milliarden US-Dollar im Jahr 2023 auf 385,26 Milliarden US-Dollar im Jahr 2031 anwachsen. Der Markt wird zwischen 2023 und 2031 voraussichtlich eine durchschnittliche jährliche Wachstumsrate von 13,7 % verzeichnen. Die zunehmende Marktkonsolidierung und die Zunahme von Fusionen und Übernahmen werden voraussichtlich weiterhin die wichtigsten Trends auf dem Markt bleiben.

CMO-Marktanalyse im Gesundheitswesen

Aufgrund der Fortschritte in der Biotechnologie und innovativer Therapien besteht eine wachsende Nachfrage nach Dienstleistungen von Auftragsherstellern (CMOs) für Biopharmazeutika und Biologika. Die Zunahme komplexer und spezialisierter Moleküle, darunter hochwirksame Arzneimittel und personalisierte Medikamente, hat die Nachfrage nach CMOs mit Fachkenntnissen in der Verwaltung komplexer Herstellungsprozesse erhöht. Der CMO-Markt im Gesundheitswesen wird zunehmend globaler, und Unternehmen suchen nach Partnerschaften mit CMOs in verschiedenen Regionen, um von Kosteneffizienzen, regulatorischen Vorteilen und Zugang zu unterschiedlichen Märkten zu profitieren.

Überblick über den CMO-Markt im Gesundheitswesen

CMOs bieten Dienstleistungen im Zusammenhang mit der Entwicklung, Herstellung und Verpackung von Arzneimitteln , Biotechnologieprodukten, Medizinprodukten und anderen Gesundheitsprodukten an. In der Gesundheitsbranche tendiert der Trend zum Outsourcing an CMOs. Unternehmen nutzen das Fachwissen und die Fähigkeiten von CMOs, um Herstellungsprozesse zu optimieren und sich auf Kernkompetenzen zu konzentrieren. CMOs, die flexible und skalierbare Fertigungslösungen anbieten, sind gefragt. Die Anpassung an unterschiedliche Produktionsgrößen und -pläne ist für Pharma- und Biotechunternehmen von entscheidender Bedeutung.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos individuelle Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

CMO-Markt im Gesundheitswesen: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Treiber und Chancen auf dem CMO-Markt im Gesundheitswesen

Steigende geriatrische Bevölkerung gepaart mit der zunehmenden Produktion von Medikamenten und medizinischen Geräten begünstigen den Markt

Die Zahl der geriatrischen Bevölkerung ist weltweit deutlich gestiegen. Laut den von den Vereinten Nationen veröffentlichten Daten wächst die geriatrische Bevölkerung schätzungsweise jedes Jahr um 3 %. Europa und der asiatisch-pazifische Raum haben die höchste Altersgruppe der über 60-Jährigen. Darüber hinaus wird die alternde Weltbevölkerung voraussichtlich von 1,4 Milliarden im Jahr 2030 auf 2,1 Milliarden im Jahr 2050 anwachsen. Die Alterung wird mit verschiedenen chronischen Krankheiten wie Herz-Kreislauf-Erkrankungen, Diabetes, Krebs und vielen anderen in Verbindung gebracht. Dadurch steigt die Nachfrage nach therapeutischen Produkten und medizinischen Geräten in diesen Altersgruppen. Daher wird erwartet, dass die oben genannten Faktoren den Markt für CMOs im Gesundheitswesen aufgrund der steigenden Nachfrage weltweit ankurbeln werden.

Wachstumschancen durch zunehmende Entwicklung von Biosimilars

Die Biosimilars werden immer attraktiver, da sich die Verbraucher offensichtlich Kosteneinsparungen erhoffen und sich für Hersteller alternativer Arzneimittel die Möglichkeit bietet, sowohl in etablierte als auch in aufstrebende Märkte einzutreten. Technologische Fortschritte und Verbesserungen beim Verständnis von Krankheiten wie Krebs, rheumatoider Arthritis und anderen führen zu einer erhöhten Nachfrage nach der Entwicklung von Biosimilars und Biologika. Um die unerfüllten Bedingungen zu erfüllen, investieren viele Unternehmen massiv in die Herstellung von Biologika, was im Gegenzug höhere Umsätze generieren würde. Die Schwellenländer wie China, Indien, Australien und Südkorea verfügen über die größten Biotechnologiezentren und erleben aufgrund der aufstrebenden Akteure ein Marktwachstum. Daher ziehen es die Unternehmen vor, die Herstellungsdienstleistungen an die CMOs auszulagern, um interne Kosten und Zeit für Testdienstleistungen während des Entwicklungsprozesses der Biologika und Biosimilars zu sparen. Diese Verschiebung hin zur Bevorzugung von CMOs gegenüber der internen Herstellung dürfte die Wachstumschancen der CMOs weltweit in den kommenden Jahren erhöhen.

Segmentierungsanalyse des CMO-Marktberichts im Gesundheitswesen

Wichtige Segmente, die zur Ableitung der CMO-Marktanalyse im Gesundheitswesen beigetragen haben, basieren auf Dienstleistungen.

- Basierend auf dem Service ist der CMO-Markt im Gesundheitswesen in pharmazeutische Auftragsfertigungsdienste und Auftragsfertigungsdienste für medizinische Geräte unterteilt. Die pharmazeutischen Auftragsfertigungsdienste werden weiter in aktive pharmazeutische Inhaltsstoffe (API), Herstellung der endgültigen Darreichungsform und Verpackung unterteilt. In ähnlicher Weise sind die Auftragsfertigungsdienste für medizinische Geräte in Outsourcing-Design, Geräteherstellung und Endmontage unterteilt. Das Segment der pharmazeutischen Auftragsfertigungsdienste hatte 2023 den größten Marktanteil und wird im Prognosezeitraum voraussichtlich die höchste durchschnittliche jährliche Wachstumsrate verzeichnen.

Marktanteilsanalyse für CMOs im Gesundheitswesen nach geografischer Lage

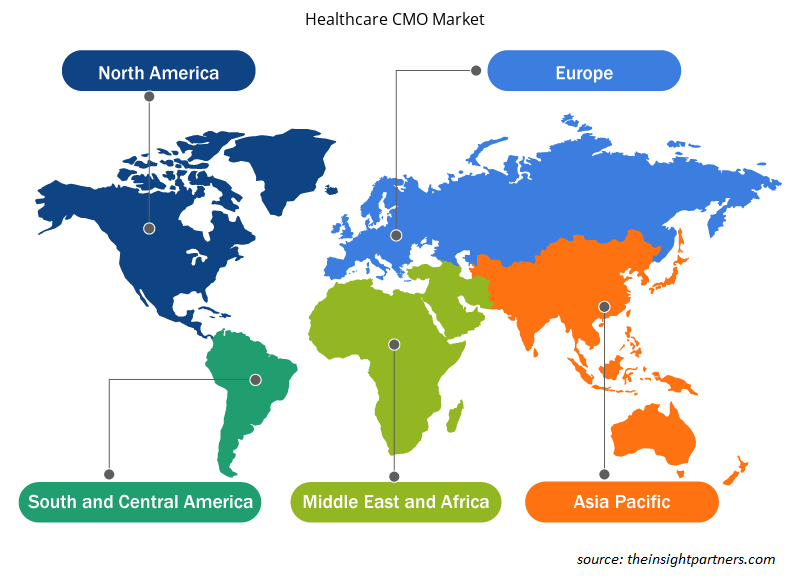

Der geografische Umfang des Berichts zum CMO-Markt im Gesundheitswesen ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten und Afrika sowie Süd- und Mittelamerika.

Nordamerika dominiert den CMO-Markt im Gesundheitswesen. Das Wachstum des CMO-Marktes im Gesundheitswesen in Nordamerika ist auf die Zunahme der Pharma-, Biopharma- und Medizingerätebranche, günstige Bedingungen und eine gut regulierte Gesundheitsbranche zurückzuführen. Die USA hatten 2023 den größten Marktanteil. Die USA sind der größte Markt für die Pharma- und Biopharmaindustrie, das Land macht etwa ein Drittel des Weltmarkts aus. Die USA gelten als weltweit führend bei Forschungs- und Entwicklungsaktivitäten im Bereich Biopharmazie. Darüber hinaus fördert die Unterstützung durch die Regierung die Auftragsfertigung von Pharmazeutika und Biopharmazeutika. Dies trägt dazu bei, Unternehmen zur Entwicklung von Medikamenten, Gegenmaßnahmen und entsprechenden Diagnostika zu bewegen, die für die öffentliche Gesundheit und Sicherheit erforderlich sind. Darüber hinaus hat eine Zunahme der Herstellung komplexer Geräte Freiheit von den alltäglichen Sorgen verschafft und ermöglicht es, sich stärker auf die Kerntechnologie des Unternehmens zu konzentrieren und sich stärker darauf zu konzentrieren, was das Marktwachstum in der Region fördert.

Regionale Einblicke in den CMO-Markt im Gesundheitswesen

Die regionalen Trends und Faktoren, die den CMO-Markt im Gesundheitswesen während des Prognosezeitraums beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die Geografie des CMO-Marktes im Gesundheitswesen in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zum CMO-Markt im Gesundheitswesen

Umfang des CMO-Marktberichts im Gesundheitswesen

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2023 | 138,24 Milliarden US-Dollar |

| Marktgröße bis 2031 | 385,26 Milliarden US-Dollar |

| Globale CAGR (2023 - 2031) | 13,7 % |

| Historische Daten | 2021-2022 |

| Prognosezeitraum | 2024–2031 |

| Abgedeckte Segmente |

Nach Service

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktteilnehmerdichte: Der Einfluss auf die Geschäftsdynamik

Der Markt für CMOs im Gesundheitswesen wächst rasant. Dies wird durch die steigende Nachfrage der Endnutzer aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts vorangetrieben. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung der Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten auf dem CMO-Markt im Gesundheitswesen tätigen Unternehmen sind:

- Königliches DSM

- Catalent, Inc

- Boehringer Ingelheim International GmbH

- Recipharm AB (publ)

- Fareva

- Lonza

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Healthcare CMO-Markt

Neuigkeiten und aktuelle Entwicklungen zum CMO-Markt im Gesundheitswesen

Der CMO-Markt im Gesundheitswesen wird durch die Erhebung qualitativer und quantitativer Daten nach Primär- und Sekundärforschung bewertet, die wichtige Unternehmenspublikationen, Verbandsdaten und Datenbanken umfasst. Nachfolgend sind einige der Entwicklungen auf dem CMO-Markt im Gesundheitswesen aufgeführt:

- Kühne Holding AG hat eine endgültige Vereinbarung zur Übernahme der Pharma-Vertragsentwicklungs- und -herstellungsorganisation Aenova Group von der führenden internationalen Investmentfirma BC Partners geschlossen. Im Rahmen der Transaktion werden die von BC Partners beratenen Fonds neben der Kühne Holding AG reinvestieren und Aenova weiterhin als Minderheitsaktionär unterstützen. Finanzielle Bedingungen wurden nicht bekannt gegeben. Die Aenova Group ist eine der weltweit führenden CDMOs (Contract Development and Manufacturing Organizations) in der Pharma- und Gesundheitsbranche. (BC Partners, News, April 2024)

- Pharmascience, das größte kanadische Pharmaunternehmen, kündigte eine umfangreiche Erweiterung der Produktionsanlage für sterile Injektionspräparate im Wert von 120 Millionen US-Dollar an seinem Standort in Candiac an. Nach diesem wichtigen Meilenstein ist das Unternehmen nun stolz darauf, die Erweiterung seiner Auftragsentwicklungs- und Fertigungsorganisationsdienste (CDMO) mit der Schaffung einer neuen Geschäftseinheit für Injektionspräparate bekannt zu geben. (Pharmascience Inc., News, Februar 2024)

- Danaher Corporation gab eine endgültige Vereinbarung zur Übernahme des in Privatbesitz befindlichen Unternehmens Aldevron bekannt. Der Barkaufpreis beträgt rund 9,6 Milliarden US-Dollar. Danaher geht davon aus, die Übernahme mit Barmitteln und/oder durch die Ausgabe von Commercial Papers zu finanzieren. (Danaher Corporation, Pressemitteilung, Juni 2021)

Abdeckung und Ergebnisse des CMO-Marktberichts im Gesundheitswesen

Der Bericht „Marktgröße und Prognose für CMOs im Gesundheitswesen (2021–2031)“ bietet eine detaillierte Analyse des Marktes, die die folgenden Bereiche abdeckt:

- Größe und Prognose des CMO-Marktes im Gesundheitswesen auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt sind

- Trends im Healthcare-CMO-Markt sowie Marktdynamiken wie Treiber, Einschränkungen und wichtige Chancen

- Detaillierte PEST- und SWOT-Analyse

- Analyse des CMO-Marktes im Gesundheitswesen, die wichtige Markttrends, globale und regionale Rahmenbedingungen, wichtige Akteure, Vorschriften und aktuelle Marktentwicklungen umfasst

- Branchenlandschaft und Wettbewerbsanalyse, einschließlich Marktkonzentration, Heatmap-Analyse, prominenten Akteuren und aktuellen Entwicklungen für den CMO-Markt im Gesundheitswesen

- Detaillierte Firmenprofile

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends