Marktstrategien für die industrielle Radiographie, Top-Player, Wachstumschancen, Analyse und Prognose bis 2031

Historische Daten : 2021-2022 | Basisjahr : 2023 | Prognosezeitraum : 2024-2031Marktgröße und Prognose für die industrielle Radiographie (2021 – 2031), Bericht über globale und regionale Anteile, Trends und Wachstumschancenanalysen: Nach Technik (filmbasierte Radiographie und digitale Radiographie); Endverbraucherindustrie (Fertigung, Luft- und Raumfahrt, Automobil- und Transportwesen, Energieerzeugung, Petrochemie und Gas usw.) und Geografie

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00003160

- Kategorie : Elektronik und Halbleiter

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

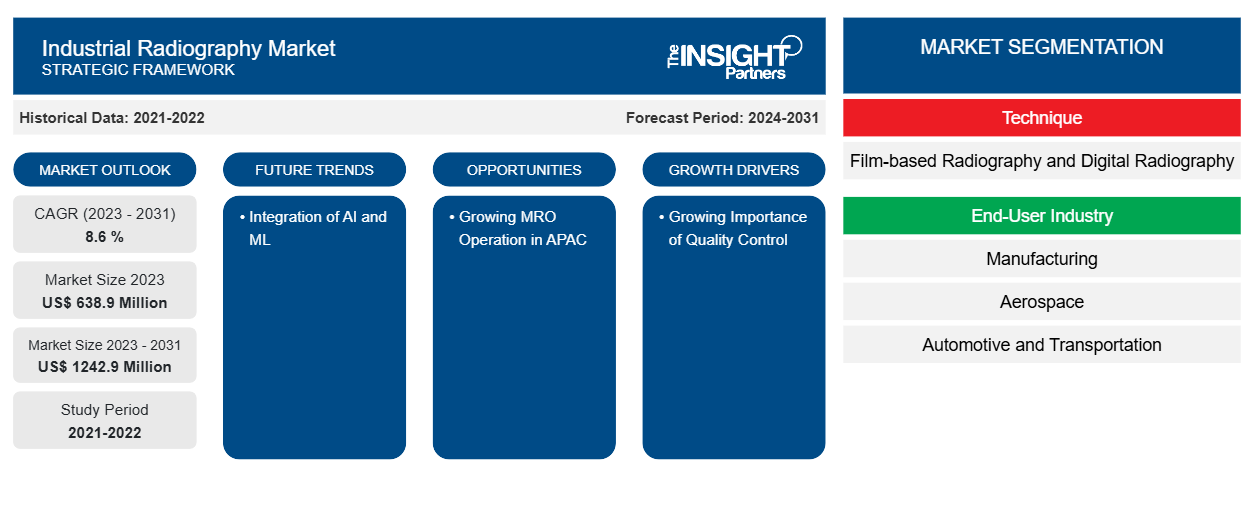

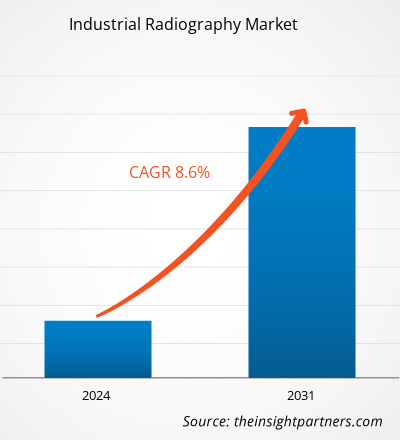

Der Markt für industrielle Radiographie soll von 638,9 Millionen US-Dollar im Jahr 2023 auf 1.242,9 Millionen US-Dollar im Jahr 2031 anwachsen. Der Markt wird zwischen 2023 und 2031 voraussichtlich eine durchschnittliche jährliche Wachstumsrate (CAGR) von 8,6 % verzeichnen. Die Integration von KI und ML dürfte ein wichtiger Trend auf dem Markt bleiben.

Marktanalyse für industrielle Radiographie

Bei der industriellen Radiographie analysieren Prüfer die innere Struktur von Materialien und Komponenten mithilfe ionisierender Strahlung wie Röntgen- oder Gammastrahlen. Dadurch können versteckte Defekte aufgedeckt, Dicken gemessen und die Integrität verschiedener Konstruktionen überprüft werden, ohne dabei Schäden zu verursachen. Darüber hinaus treiben zunehmende Wartungs-, Reparatur- und Betriebskosten das Wachstum des Marktes voran.

Marktübersicht für industrielle Radiographie

Die industrielle Radiographie ist eine zerstörungsfreie Prüfmethode, bei der ionisierende Strahlung zur Prüfung von Materialien und Komponenten verwendet wird, um Fehler und Materialverschlechterungen zu erkennen und zu messen, die zum Zusammenbruch technischer Strukturen führen könnten. Hersteller nutzen die industrielle Radiographie, um Brüche oder Fehler in Materialien zu erkennen. Bei der industriellen Radiographie werden hauptsächlich Röntgen- und Gammastrahlen eingesetzt , um Fehler aufzudecken, die mit bloßem Auge nicht erkennbar sind. Die industrielle Radiographie ist eine zerstörungsfreie Art der physikalischen Prüfung. Diese Art der Radiographie verwendet ionisierende Strahlung, die unter geregelten Bedingungen von einer radioaktiven Quelle abgegeben wird, um die innere Struktur eines Objekts zu erkennen oder zu bestimmen, ohne seine äußere Morphologie zu beschädigen. Daher kann sie verwendet werden, um ein klares Verständnis der Bestandteile oder Komponenten des untersuchten Gegenstands oder Produkts zu erlangen.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos individuelle Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für industrielle Radiographie: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Treiber und Chancen auf dem Markt für industrielle Radiographie

Wachsende Bedeutung der Qualitätskontrolle zur Förderung des Marktes

Qualitätskontrollinspektoren für industrielle Radiographie bewerten die Gesamtqualität von Röntgenbildern und Prüfmethoden. Sie garantieren, dass die Prüfungen den Industriestandards entsprechen und die Geräte ordnungsgemäß funktionieren. Die industrielle Radiographie wird hauptsächlich verwendet, um innere Mängel in Materialien und Strukturen wie Risse, Hohlräume, Einschlüsse und Diskontinuitäten zu erkennen. Sie gewährleistet die strukturelle Integrität und Sicherheit zahlreicher Systemkomponenten. Die industrielle Radiographie wird verwendet, um Materialien wie Metalle, Polymere , Verbundwerkstoffe und Keramik zu bewerten. Schweißnähte, Rohrleitungen, Gussteile, Schmiedestücke, Luftfahrtkomponenten und andere Gegenstände werden häufig geprüft.

Wachsendes MRO-Geschäft im Asien-Pazifik-Raum

Indiens MRO-Nachfrage wird voraussichtlich schneller wachsen als der Weltdurchschnitt und damit Chancen für in- und ausländische Investoren, OEMs und Top-MROs schaffen. In- und ausländische Investoren könnten sich beteiligen. Darüber hinaus sind die Heimat des größten MRO-Standorts Asiens und die hohe Konzentration der Luft- und Raumfahrtindustrie sowie die Präsenz großer Branchengrößen wie Rolls Royce und Airbus die Gründe für den wachsenden MRO-Betrieb in Asien. MRO ist ein wichtiger Bestandteil vieler Branchen. Die folgenden Branchen machen starken Gebrauch von MRO-Praktiken: Produktionsunternehmen sind in hohem Maße auf Wartungs- und Reparaturtätigkeiten für Produktionsanlagen, Maschinen und Werkzeuge angewiesen. Dies umfasst die Automobil-, Flugzeug-, Elektronik-, Konsumgüter- und andere Branchen. Die Transportbranche, zu der Fluggesellschaften, Züge, Schifffahrt und Logistik gehören, verlässt sich auf MRO-Techniken, um ihre Auto-, Flugzeug-, Lokomotiv- und Schiffscontainerflotten zu warten.

Segmentierungsanalyse des Marktberichts zur industriellen Radiographie

Wichtige Segmente, die zur Ableitung der Marktanalyse für industrielle Radiographie beigetragen haben, sind Technik und Endverbraucherindustrie.

- Basierend auf der Technik ist der Markt für industrielle Radiographie in filmbasierte Radiographie und digitale Radiographie segmentiert.

- Basierend auf der Endverbraucherbranche ist der Markt für industrielle Radiographie in die Branchen Fertigung, Luft- und Raumfahrt, Automobil und Transport, Stromerzeugung, Petrochemie und Gas und Sonstige segmentiert.

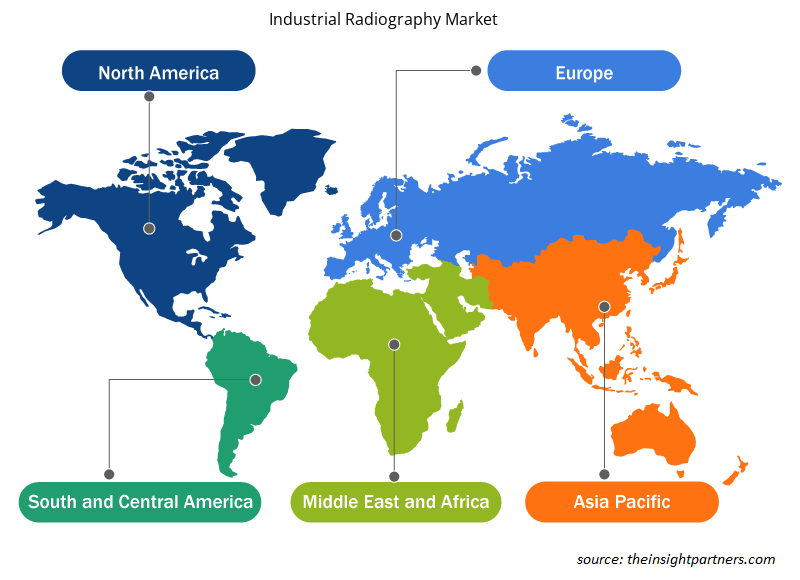

Industrielle Radiographie Marktanteilsanalyse nach Geografie

Der geografische Umfang des Marktberichts zur industriellen Radiographie ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten und Afrika sowie Süd- und Mittelamerika. Der Markt für industrielle Radiographie in Nordamerika ist in die USA, Kanada und Mexiko unterteilt. Nordamerika hat die Luft- und Raumfahrt- und Verteidigungsindustrie, die Meteorologie und die Automobilfahrzeugproduktion entwickelt. Die Region verfügt über verschiedene renommierte Automobilhersteller wie Ford, Hona, Toyota, Tesla und andere. Das Hauptziel der industriellen Radiographie besteht darin, innere Defekte in Materialien und Strukturen wie Risse, Hohlräume, Einschlüsse und Diskontinuitäten zu erkennen. Hersteller verwenden sie, um Produkte auf Risse oder Fehler zu prüfen.

Regionale Einblicke in den Markt für industrielle Radiographie

Die regionalen Trends und Faktoren, die den Markt für industrielle Radiographie im Prognosezeitraum beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die Geografie der industriellen Radiographie in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zum Markt für industrielle Radiographie

Umfang des Marktberichts zur industriellen Radiographie

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2023 | 638,9 Millionen US-Dollar |

| Marktgröße bis 2031 | 1242,9 Millionen US-Dollar |

| Globale CAGR (2023 - 2031) | 8,6 % |

| Historische Daten | 2021-2022 |

| Prognosezeitraum | 2024–2031 |

| Abgedeckte Segmente |

Nach Technik

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktteilnehmerdichte: Der Einfluss auf die Geschäftsdynamik

Der Markt für industrielle Radiographie wächst rasant, angetrieben durch die steigende Nachfrage der Endnutzer aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung von Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten auf dem Markt für industrielle Radiographie tätigen Unternehmen sind:

- 3DX-RAY

- Anritsu

- Comet-Gruppe

- Fujifilm Corporation

- ALLGEMEINE ELEKTRIK

- METTLER TOLEDO

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Markt für industrielle Radiographie

Neuigkeiten und aktuelle Entwicklungen auf dem Markt für industrielle Radiographie

Der Markt für industrielle Radiographie wird durch die Erhebung qualitativer und quantitativer Daten nach Primär- und Sekundärforschung bewertet, die wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken umfasst. Nachfolgend sind einige der Entwicklungen auf dem Markt für industrielle Radiographie aufgeführt:

- Die Royal Air Force hat 3DX-Ray einen Vertrag über die Lieferung von drei tragbaren ThreatScan-LSC-Röntgenscansystemen (RAF) erteilt. Die ThreatScan-LSCs werden bestehende Systeme ersetzen, und dies ist der erste Vertrag von 3DX-Ray mit der RAF.

(Quelle: 3DX-RAY, Januar 2021)

- Teledyne Industrial X-Ray Solutions, ein Anbieter von Hochleistungsröntgenbildgebung, hat eine neue Produktlinie schneller, leistungsstarker dynamischer Industriedetektoren auf Basis unserer innovativen strahlungsresistenten IGZO-Sensortechnologie vorgestellt. Die Detektoren Rad-Xcam 1717, 1723 und 3030 sind auf die hohen Anforderungen industrieller Inspektionen sowie biomedizinischer und wissenschaftlicher Anwendungen ausgelegt und bieten überzeugende Integrationskostenvorteile. (Quelle: Teledyne., Juli 2023)

Marktbericht zur industriellen Radiographie – Umfang und Ergebnisse

Der Bericht „Marktgröße und Prognose für die industrielle Radiographie (2021–2031)“ bietet eine detaillierte Analyse des Marktes, die die folgenden Bereiche abdeckt:

- Marktgröße und Prognose für die industrielle Radiographie auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt sind

- Markttrends für die industrielle Radiographie sowie Marktdynamiken wie Treiber, Einschränkungen und wichtige Chancen

- Detaillierte PEST/Porters Five Forces- und SWOT-Analyse

- Marktanalyse für industrielle Radiographie mit wichtigen Markttrends, globalen und regionalen Rahmenbedingungen, wichtigen Akteuren, Vorschriften und aktuellen Marktentwicklungen

- Branchenlandschaft und Wettbewerbsanalyse, einschließlich Marktkonzentration, Heatmap-Analyse, prominenten Akteuren und aktuellen Entwicklungen auf dem Markt für industrielle Radiographie

- Detaillierte Firmenprofile

Naveen ist ein erfahrener Marktforschungs- und Beratungsexperte mit über 9 Jahren Erfahrung in kundenspezifischen, syndizierten und Beratungsprojekten. In seiner aktuellen Funktion als Associate Vice President hat er erfolgreich Stakeholder entlang der gesamten Projektwertschöpfungskette gemanagt und ist Autor von über 100 Forschungsberichten und über 30 Beratungsaufträgen. Seine Arbeit erstreckt sich auf Industrie- und Regierungsprojekte und trägt maßgeblich zum Kundenerfolg und zur datengesteuerten Entscheidungsfindung bei.

Naveen hat einen Ingenieursabschluss in Elektronik und Kommunikation von der VTU, Karnataka, und einen MBA in Marketing und Operations von der Manipal University. Er ist seit 9 Jahren aktives IEEE-Mitglied und nimmt an Konferenzen und technischen Symposien teil und engagiert sich ehrenamtlich auf Sektions- und regionaler Ebene. Vor seiner aktuellen Position arbeitete er als Associate Strategic Consultant bei IndustryARC und als Industrial Server Consultant bei Hewlett Packard (HP Global).

- Historische Analyse (2 Jahre), Basisjahr, Prognose (7 Jahre) mit CAGR

- PEST- und SWOT-Analyse

- Marktgröße Wert/Volumen – Global, Regional, Land

- Branchen- und Wettbewerbslandschaft

- Excel-Datensatz

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends

Exklusive Berichtsrabatte freischalten

Jetzt anfragen

Kostenlose Probe anfordern für - Markt für industrielle Radiographie

Kostenlose Probe anfordern für - Markt für industrielle Radiographie