Marktgröße, Wachstum und Trends für industrielle Holzleime bis 2034

Marktgröße und Prognose für industrielle Holzleime (2021 - 2034), globaler und regionaler Marktanteil, Trend- und Wachstumschancenanalyse. Berichtsabdeckung: Nach Harztyp (natürlich und synthetisch) und Technologie (lösemittelbasiert, wasserbasiert, lösemittelfrei und andere).

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00022059

- Kategorie : Chemikalien und Materialien

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : February 20, 2026

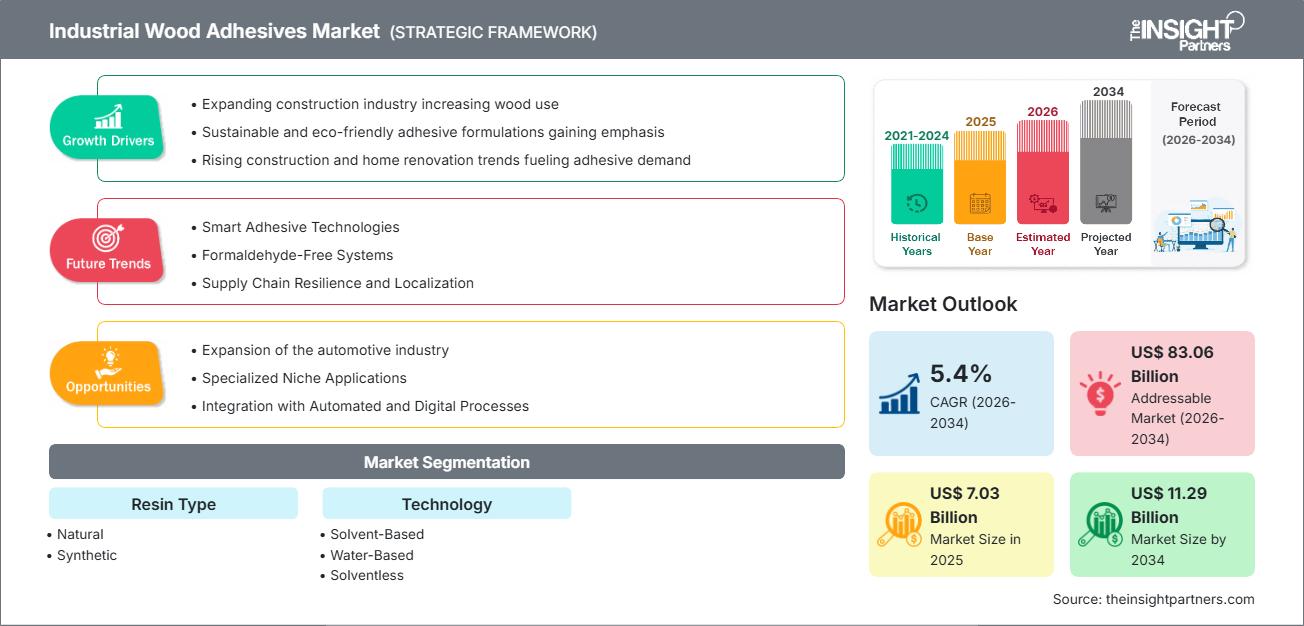

Der globale Markt für industrielle Holzleime wird bis 2034 voraussichtlich ein Volumen von 11,29 Milliarden US-Dollar erreichen, gegenüber 7,03 Milliarden US-Dollar im Jahr 2025. Für den Prognosezeitraum 2026–2034 wird ein jährliches Wachstum von 5,4 % erwartet. Zu den wichtigsten Markttreibern zählen die rasante Expansion des globalen Bausektors, die steigende Nachfrage nach Holzwerkstoffen wie Brettsperrholz (CLT) und Furnierschichtholz (LVL) sowie der zunehmende Fokus auf nachhaltige, VOC-arme (flüchtige organische Verbindungen) Klebstofflösungen. Darüber hinaus dürfte der Markt vom Wachstum des organisierten Möbelhandels, Fortschritten bei automatisierten Hochgeschwindigkeits-Holzbearbeitungsmaschinen und dem zunehmenden Ersatz traditioneller mechanischer Verbindungselemente durch Hochleistungsklebstoffe im Modulbau profitieren.

Marktanalyse für industrielle Holzklebstoffe

Die Marktanalyse für industrielle Holzleime zeigt einen entscheidenden Wandel hin zu „grüner Chemie“, da die Regulierungsbehörden die Grenzwerte für Formaldehydemissionen verschärfen. Um Marktanteile zu sichern, müssen Hersteller die Entwicklung biobasierter Harze und sojabasierter Klebstoffe priorisieren, die die strengen LEED- und CARB-II-Zertifizierungen erfüllen. Strategische Chancen eröffnen sich im Segment der Brettsperrholz-Klebstoffe (CLT), wo die Nachfrage nach struktureller Integrität und Feuchtigkeitsbeständigkeit Anbietern von Polyurethan- und Emulsionspolymer-Isocyanat-Systemen (EPI) einen signifikanten Wettbewerbsvorteil verschafft. Die Analyse zeigt zudem, dass der operative Erfolg von der Optimierung der Offenzeit und der Presszykluseffizienz der Klebstoffe abhängt, um den hohen Durchsatzanforderungen moderner Möbelfabriken gerecht zu werden. Hersteller sollten sich durch maßgeschneiderten technischen Support und integrierte Applikationssysteme differenzieren und sich von einfachen Rohstofflieferanten zu Anbietern umfassender Klebelösungen entwickeln.

Marktübersicht für industrielle Holzklebstoffe

Industrielle Holzleime entwickeln sich von einfachen Klebeverbindungen hin zu spezialisierten, hochleistungsfähigen Strukturverbindungen. Während in der Vergangenheit Harnstoff-Formaldehyd-Klebstoffe für die kostensensible Plattenproduktion dominierten, diversifizieren sich industrielle Holzleime hin zu fortschrittlichen wasserbasierten und lösemittelfreien Technologien, um den steigenden Sicherheitsstandards gerecht zu werden. Industrielle Holzleime finden in einer Vielzahl von Anwendungen Verwendung, darunter Fußböden, Möbel und Konstruktionsholz. Unterstützt werden sie sowohl von großen Chemiekonzernen als auch von spezialisierten Nischenherstellern. Die zunehmende Urbanisierung und der DIY-Trend (Do-it-yourself) in den Industrieländern treiben die Nachfrage nach langlebigen und einfach anzuwendenden Holzbearbeitungsklebstoffen an. Während Europa und Nordamerika weiterhin Zentren für technologische Innovation und die Einhaltung hoher Standards sind, hat sich der asiatisch-pazifische Raum als globales Produktionszentrum für Holzwerkstoffplatten und Möbelexporte für den Massenmarkt etabliert. Der US-Markt beispielsweise ist durch einen ausgereiften Bausektor und eine starke Nachfrage nach nachhaltigen Baustoffen gekennzeichnet. Inländische Hersteller setzen zunehmend auf biobasierte Klebstoffe, um den strengen Umweltauflagen zu entsprechen. Der Anstieg von Hausrenovierungsprojekten und die Expansion der Fertighausindustrie stimulieren zusätzlich den Verbrauch von Hochleistungs-Holzklebstoffen.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für industrielle Holzleime: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Markttreiber und Chancen für industrielle Holzklebstoffe

Markttreiber:

- Zunehmende Verwendung von Konstruktionsholz im nachhaltigen Bauwesen: Die globale Bauindustrie ersetzt zunehmend traditionellen Stahl und Beton durch Konstruktionsholzprodukte wie Brettsperrholz (CLT) und Brettschichtholz (BSH), um den CO₂-Fußabdruck zu reduzieren. Dieser Wandel ist ein Haupttreiber, da diese tragenden Holzbauteile für ihre Stabilität vollständig auf hochfeste chemische Verbindungen angewiesen sind, was eine massive und kontinuierliche Nachfrage nach industriellen Konstruktionsklebstoffen erzeugt.

- Strengere Vorschriften für Formaldehydemissionen: Internationale Regulierungsbehörden setzen deutlich strengere Grenzwerte für Emissionen flüchtiger organischer Verbindungen (VOC), insbesondere Formaldehyd, durch, um die Raumluftqualität zu verbessern. Dieser regulatorische Druck führt zu einem marktweiten Wandel von herkömmlichen Harnstoff-Formaldehyd-Harzen hin zu fortschrittlicheren, umweltfreundlicheren Klebstofflösungen wie wasserbasierten und sojabasierten Klebstoffen und zwingt die Hersteller zur Modernisierung ihrer Produktportfolios.

- Rasante Expansion des organisierten Möbelhandels und Automatisierung: Die zunehmende Produktion von großflächigen, zerlegbaren Möbeln erfordert Hochgeschwindigkeits-Produktionslinien, um die weltweite Verbrauchernachfrage zu decken. Dies treibt den Markt für schnellhärtende Schmelz- und wasserbasierte Klebstoffe an, die mit automatisierten Maschinen mithalten können und so eine sofortige Verpackung und einen Versand ohne die langen Trocknungszeiten herkömmlicher Klebstoffe ermöglichen.

Marktchancen

- Entwicklung und Vermarktung biobasierter Harze: Die Entwicklung von Klebstoffen aus natürlichen Rohstoffen wie Lignin, Sojaprotein und Stärke bietet eine bedeutende strategische Chance, um die Nachfrage nach klimaneutralen Baumaterialien zu decken. Unternehmen, die diese erneuerbaren Bindemittel erfolgreich in großem Maßstab produzieren, können das wachsende Segment umweltbewusster Bauherren und Verbraucher erschließen, die bereit sind, für zertifiziert nachhaltige Produkte einen höheren Preis zu zahlen.

- Fortschritte bei modularen und vorgefertigten Wohntechnologien: Da die Bauindustrie zunehmend auf die modulare Vorfertigung setzt, um Zeit und Arbeitskosten zu sparen, ergeben sich spezielle Anforderungen an Klebstoffe mit schneller Aushärtung und hoher Vibrationsfestigkeit. Diese Klebstoffe sind entscheidend, um die strukturelle Integrität vorgefertigter Holzmodule während Transport und Montage vor Ort zu gewährleisten.

- Expansion in wachstumsstarke Schwellenländer: Die Märkte im asiatisch-pazifischen Raum und im Nahen Osten erleben einen massiven Infrastrukturausbau und eine fortschreitende Industrialisierung. Die Errichtung lokaler Produktionsstätten oder strategischer Partnerschaften in diesen Regionen ermöglicht es Klebstoffherstellern, von Produktionszentren mit hohem Durchsatz zu profitieren, in denen die Nachfrage nach Holzwerkstoffen aufgrund neuer Stadtentwicklungsprojekte stark ansteigt.

Marktbericht für industrielle Holzklebstoffe: Segmentierungsanalyse

Der Marktanteil von industriellen Holzleimen wird in verschiedenen Segmenten analysiert, um ein besseres Verständnis seiner Struktur, seines Wachstumspotenzials und der aufkommenden Trends zu ermöglichen. Nachfolgend ist der in den meisten Branchenberichten verwendete Standard-Segmentierungsansatz dargestellt:

Nach Harztyp:

- Natural: Ein aufstrebendes Segment mit Fokus auf Nachhaltigkeit, das erneuerbare Energiequellen nutzt, um schadstoffarme Klebelösungen für umweltbewusste Märkte anzubieten.

- Synthetisch: Der wichtigste Volumenbeitragende, der eine breite Palette chemisch formulierter Harze umfasst, die für ihre hohe Haftfestigkeit, Haltbarkeit und Kosteneffizienz im industriellen Maßstab bekannt sind.

Durch Technologie:

- Wasserbasiert: Das führende Technologiesegment, das aufgrund seines niedrigen VOC-Gehalts, der einfachen Reinigung und der Einhaltung moderner Sicherheits- und Umweltstandards bevorzugt wird.

- Lösungsmittelbasiert: Wird trotz zunehmender behördlicher Kontrollen für spezielle, anspruchsvolle Anwendungen eingesetzt, die eine schnelle Trocknung und hohe Beständigkeit gegenüber extremen Umweltbedingungen erfordern.

- Lösungsmittelfrei: Ein Wachstumssegment mit hohem Potenzial, das Schmelzklebstoffe und 100% Feststoffe umfasst und Effizienzsteigerungen in automatisierten Fertigungsprozessen sowie eine geringere Umweltbelastung bietet.

- Sonstige: Dazu gehören Spezialtechnologien wie strahlungsgehärtete und Hybridsysteme, die für spezielle, leistungsstarke Holzbearbeitungsanwendungen entwickelt wurden.

Nach Geographie:

- Nordamerika

- Europa

- Asien-Pazifik

- Süd- und Mittelamerika

- Naher Osten und Afrika

Markt für industrielle Holzklebstoffe – Regionale Einblicke

Die regionalen Trends, die den Markt für industrielle Holzleime beeinflussen, wurden in wichtigen geografischen Regionen analysiert.

Marktbericht über industrielle Holzklebstoffe – Umfang

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 7,03 Milliarden US-Dollar |

| Marktgröße bis 2034 | 11,29 Milliarden US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2026 - 2034) | 5,4 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2026–2034 |

| Abgedeckte Segmente |

Nach Harztyp

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte der Akteure im Markt für industrielle Holzleime: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für industrielle Holzleime wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen, um den Kundenbedürfnissen gerecht zu werden, und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

Marktanteilsanalyse für industrielle Holzklebstoffe nach Regionen

Der asiatisch-pazifische Raum wird voraussichtlich in den kommenden Jahren das schnellste Wachstum verzeichnen. Auch die aufstrebenden Märkte in Süd- und Mittelamerika, dem Nahen Osten und Afrika bieten Herstellern von Premium-Klebstoffen und industriellen Holzbearbeitungsmaschinen zahlreiche ungenutzte Expansionsmöglichkeiten.

Der Markt für industrielle Holzleime befindet sich im Wandel und entwickelt sich von traditionellen Harzformulierungen hin zu leistungsstarken, nachhaltigen Klebesystemen. Das Wachstum wird durch den weltweiten Boom im Holzbau, die steigende Nachfrage nach emissionsarmen Möbeln und die Expansion automatisierter Holzverarbeitungsbetriebe angetrieben. Nachfolgend finden Sie eine Zusammenfassung der Marktanteile und Trends nach Regionen:

Nordamerika

- Marktanteil: Hält einen bedeutenden Anteil am Weltmarkt, was auf ein Wiederaufleben des Wohnungsbaus und der fortschrittlichen Fertigung zurückzuführen ist.

-

Wichtigste Einflussfaktoren:

- Starke Nachfrage nach formaldehydfreien und sojabasierten Klebstoffen zur Einhaltung strenger Innenraumluftqualitätsstandards.

- Zunehmende Verwendung von Massivholz und Brettsperrholz (CLT) bei gewerblichen Bauprojekten.

- Eine ausgeprägte Heimwerker- und Renovierungskultur treibt den Einzelhandelsabsatz von Hochleistungsholzleimen an.

- Trends: Strategische Verlagerung hin zu biobasierten Polyurethansystemen und die zunehmende Verbreitung von „grünen“ Gebäudezertifizierungen wie LEED im Holzverarbeitungssektor.

Europa

- Marktanteil: Stellt einen dominanten Anteil am Weltmarkt dar, der durch hochwertige Möbelzentren in Deutschland, Italien und Skandinavien geprägt ist.

-

Wichtigste Einflussfaktoren:

- Die strengen E0- und REACH-Vorschriften schreiben die Verwendung von wenig toxischen und nachhaltigen Bindemitteln vor.

- Hochentwickelte Holzwerkstoffindustrie, spezialisiert auf strukturelles Brettschichtholz und hochwertige Möbel.

- Starke staatliche Unterstützung für Initiativen zur Kreislaufwirtschaft und Rohstoffe aus Bioraffinerien.

- Trends: Konsolidierung der Marktteilnehmer und Fokus auf „intelligente“ Klebstoffe, die die einfache Demontage und das Recycling von Holzbauteilen ermöglichen.

Asien-Pazifik

- Marktanteil: Die größte und am schnellsten wachsende Region, die als globale Drehscheibe für den Export von Sperrholz, Plattenwerkstoffen und Möbeln fungiert.

-

Wichtigste Einflussfaktoren:

- Massive Infrastrukturentwicklung und städtische Wohnungsbauprojekte in China, Indien und Südostasien.

- Die rasche Industrialisierung und das Vorhandensein kostengünstiger Produktionsstätten für globale Möbelmarken spielen dabei eine wichtige Rolle.

- Staatlich geförderte Verlagerung hin zu höherwertiger Holzverarbeitung, um internationale Exportsicherheitsstandards zu erfüllen.

- Trends: Hohe Investitionen in automatisierte Produktionslinien und ein zunehmender Übergang von kostengünstigen Harnstoffharzen zu hochwertigen wasserbasierten und Schmelzklebstofftechnologien.

Süd- und Mittelamerika

- Marktanteil: Ein aufstrebender Markt mit einem wachsenden Sektor für industrielle Holzverarbeitung in Ländern wie Brasilien, Argentinien und Chile.

-

Wichtigste Einflussfaktoren:

- Ausbau der regionalen Forst- und Zellstoffindustrie hin zu Holzprodukten mit höherer Wertschöpfung.

- Das steigende verfügbare Einkommen der Mittelschicht führt zu einer Vorliebe für moderne, ästhetisch ansprechende Inneneinrichtungen.

- Modernisierung kleiner und mittlerer holzverarbeitender Betriebe zu Produktionsanlagen in kommerzieller Qualität.

- Trends: Wachstum von Boutique-Möbelmarken und die schrittweise Einführung von Zertifizierungen für nachhaltige Forstwirtschaft, die sich auf die Klebstoffauswahl auswirken.

Naher Osten und Afrika

- Marktanteil: Ein sich entwickelnder Markt mit erheblichem Potenzial, der den Übergang von der traditionellen Tischlerei zur formalisierten industriellen Produktion vollzieht.

-

Wichtigste Einflussfaktoren:

- Hohe Nachfrage nach langlebigen und hitzebeständigen Klebstoffen, die für die extremen klimatischen Bedingungen der Region geeignet sind.

- Groß angelegte „Smart City“- und Luxushotellerieprojekte in den GCC-Staaten (z. B. Saudi-Arabien und die VAE).

- Strategische Bemühungen zur Verringerung der Importabhängigkeit durch die Errichtung lokaler Produktionsstätten für Chemikalien und Harze.

- Trends: Einsatz moderner Kühl- und Applikationstechnologien zur Steuerung der Klebstoffleistung in ariden Umgebungen, verbunden mit einem Fokus auf hochfeste Verbindungen für anspruchsvolle strukturelle Anwendungen.

Hohe Marktdichte und starker Wettbewerb

Der Wettbewerb verschärft sich aufgrund der Präsenz etablierter Marktführer wie HBFuller Company, Henkel AG & Company KGAA, Ashland, Arkema Group, Sika AG, Pidilite Industries Ltd, Jubilant Industries Ltd, Dow, Inc. und 3M, die ebenfalls zu einer vielfältigen und schnell wachsenden Marktlandschaft beitragen.

Dieses wettbewerbsintensive Umfeld zwingt die Anbieter dazu, sich durch Folgendes zu differenzieren:

- Premiumisierung und nachhaltiges Branding: Positionierung von Klebstoffen als unverzichtbar für leistungsstarkes, umweltfreundliches Bauen durch Betonung niedriger VOC-Emissionen, biobasierter Harzherkunft und Einhaltung strenger Umweltzertifizierungen.

- Spezialisierte Produktportfolios: Industrielle Holzleime umfassen heute neben Basisharzen auch feuchtigkeitsaktivierte Systeme für Bootsbauholz, mikro-emissionsfähige Schmelzklebstoffe für die Kantenanleimung im Innenbereich sowie hochfeste, feuerbeständige Lösungen für Brettsperrholz (CLT).

- Technologische Integration und Forschung & Entwicklung: Unternehmen steuern die gesamte Innovationskette – von der Entwicklung eigener Kunstharze bis hin zur Entwicklung intelligenter Applikationswerkzeuge. Dies gewährleistet Präzision im industriellen Umfeld, reduziert Materialverschwendung und erfüllt ethische Produktionsstandards mit Clean Label.

- Fortschrittliche Verarbeitung für Kreislaufwirtschaft: Neue Formulierungstechnologien, wie die Beimischung von Biofüllstoffen und die Verwendung feuchtigkeitsbeständiger Polymere, tragen zur Herstellung langlebiger Holzprodukte bei, die nachhaltige Bauweisen unterstützen und eine einfachere Demontage zum Recycling ermöglichen.

Chancen und strategische Schritte

- Partnerschaften mit großen Möbelproduktionszentren und Automatisierungsanbietern eingehen: Nutzen Sie die steigende Nachfrage nach schnellhärtenden, maschinenfertigen Klebstoffen, indem Sie strategische Allianzen mit großen Möbelexporteuren und Robotermontagewerken in den Märkten Asien-Pazifik und Nordamerika bilden.

- Integration biobasierter Chemie und Niedrigemissionsstandards: Einführung von Zertifizierungen für erneuerbare Kohlenstoffanteile und Lebenszyklusanalysen, um umweltbewusste Bauherren und staatlich geförderte Infrastrukturprojekte anzusprechen, die nach Gutschriften für nachhaltiges Bauen suchen.

Die wichtigsten Unternehmen auf dem Markt für industrielle Holzleime sind:

- HBFuller Company

- Henkel AG & Company KGAA

- Ashland

- Arkema-Gruppe

- Sika AG

- Pidilite Industries Ltd

- Jubilant Industries Ltd

- Dow, Inc.

- 3M

Hinweis: Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge geordnet.

Marktneuigkeiten und aktuelle Entwicklungen im Bereich industrieller Holzklebstoffe

- Im Januar 2025 präsentierte Kiilto eine neue Produktlinie industrieller Holzleime, die ein umfassendes Angebot an technischen Lösungen speziell für die Holzwerkstoffindustrie bietet. Die Kiilto Pro SW-Produktlinie wurde für Hochleistungsanwendungen entwickelt, die außergewöhnliche Festigkeit und Qualität erfordern, um jahrzehntelanger intensiver Nutzung standzuhalten.

- Im Dezember 2024 schloss Arkema die Übernahme des Geschäftsbereichs für flexible Verpackungslaminierklebstoffe von Dow ab, einem weltweit führenden Hersteller mit einem Jahresumsatz von rund 250 Millionen US-Dollar. Diese strategische Transaktion erweiterte Arkemas Portfolio an industriellen Holzklebstoffen und Speziallösungen erheblich und positionierte den Konzern als dominanten Akteur in den wachstumsstarken Märkten für flexible Verpackungen und industrielle Laminierung.

Marktbericht über industrielle Holzklebstoffe: Abdeckung und Ergebnisse

Der Bericht „Marktgröße und Prognose für industrielle Holzleime (2021–2034)“ bietet eine detaillierte Analyse des Marktes und deckt folgende Bereiche ab:

- Marktgröße und Prognose für industrielle Holzleime auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt werden

- Markttrends für industrielle Holzleime sowie Marktdynamiken wie Treiber, Hemmnisse und wichtige Chancen

- Detaillierte PEST- und SWOT-Analyse

- Marktanalyse für industrielle Holzleime: Wichtige Markttrends, globale und regionale Rahmenbedingungen, Hauptakteure, regulatorische Bestimmungen und aktuelle Marktentwicklungen

- Branchenlandschafts- und Wettbewerbsanalyse mit Fokus auf Marktkonzentration, Heatmap-Analyse, prominente Akteure und aktuelle Entwicklungen auf dem Markt für industrielle Holzleime.

- Detaillierte Unternehmensprofile

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends