Nachfrage, Marktanteil und Wachstum des Marktes für medizinische Roboter bis 2034

Marktgröße und Prognosen für Medizinroboter (2021–2034), globaler und regionaler Marktanteil, Trends und Wachstumschancenanalyse. Berichtsabdeckung: Nach Produkt (Chirurgieroboter, Krankenhaus- und Apothekenroboter, Rehabilitationsroboter, nicht-invasive Radiochirurgieroboter und Sonstige), Anwendung (Laparoskopie, Neurologie, Orthopädie, Gynäkologie, Urologie, Kardiologie und Sonstige), Endnutzer (Krankenhäuser, ambulante Operationszentren und Sonstige) und Geografie (Nordamerika, Europa, Asien-Pazifik sowie Süd- und Mittelamerika).

- Status : Veröffentlichte Daten

- Berichtscode : TIPHE100000816

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 23, 2026

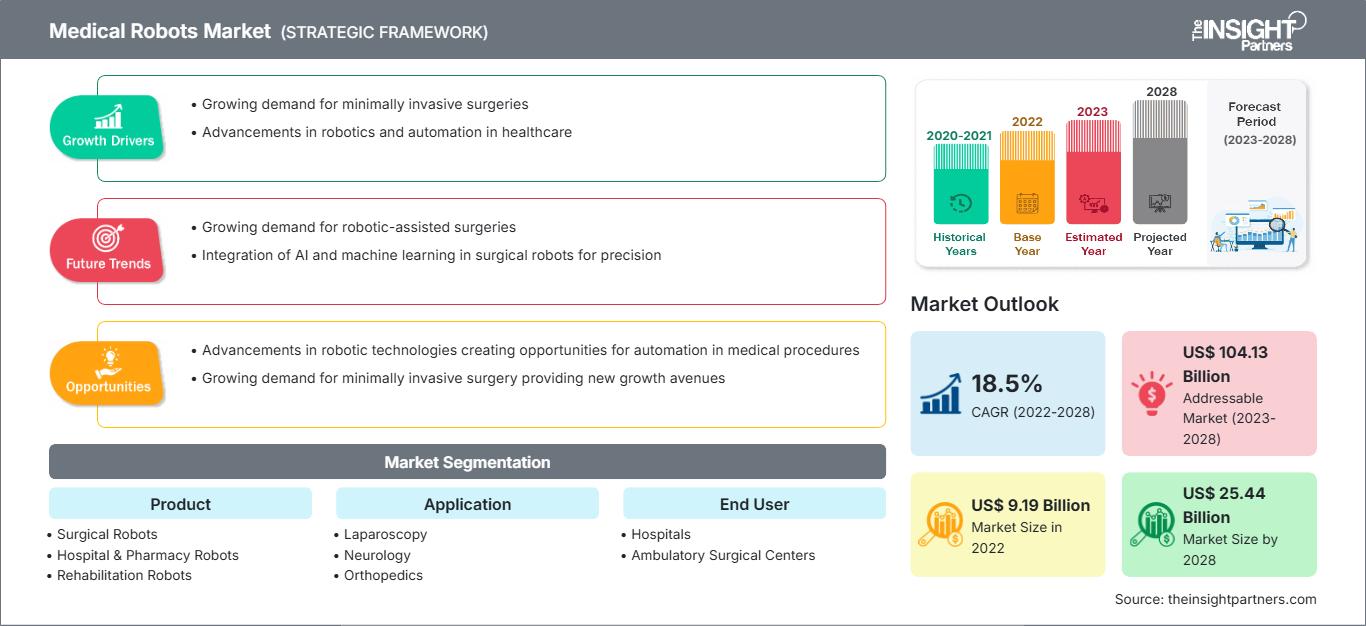

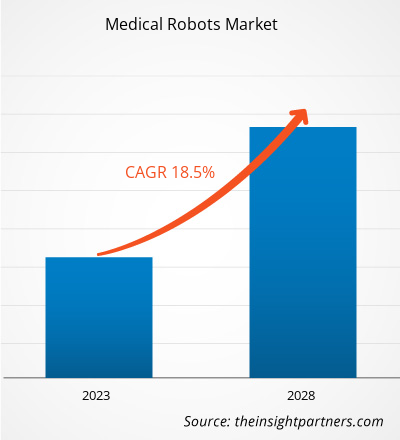

Der globale Markt für medizinische Roboter wird bis 2034 voraussichtlich ein Volumen von 61,27 Milliarden US-Dollar erreichen, gegenüber 15,98 Milliarden US-Dollar im Jahr 2025. Es wird erwartet, dass der Markt im Prognosezeitraum 2026–2034 eine durchschnittliche jährliche Wachstumsrate (CAGR) von 16,11 % verzeichnen wird.

Zu den wichtigsten Marktdynamiken zählen der weltweit zunehmende Trend zu minimalinvasiven Eingriffen, die rasanten Fortschritte in der KI-gestützten Präzisionsmedizin und der steigende Bedarf an Automatisierung, um dem globalen Fachkräftemangel im Gesundheitswesen zu begegnen. Darüber hinaus dürfte der Markt von der wachsenden Zahl älterer Menschen mit chronischen Erkrankungen, dem Ausbau robotergestützter Plattformen in Schwellenländern und dem zunehmenden Fokus auf die Verkürzung von Krankenhausaufenthalten und Genesungszeiten durch hochpräzise robotergestützte Eingriffe profitieren.

Marktanalyse für medizinische Roboter

Die Marktanalyse für Medizinroboter zeigt einen deutlichen Wandel hin zu hochpräzisen, fachübergreifenden Plattformen, die ihre traditionelle Dominanz in Urologie und Gynäkologie überwinden. Der Markt diversifiziert sich in spezialisierte Bereiche wie orthopädischen Gelenkersatz, Neurochirurgie und den schnell wachsenden Bereich der Rehabilitationsrobotik. Strategische Chancen ergeben sich durch die Integration von Künstlicher Intelligenz und Maschinellem Lernen zur intraoperativen Entscheidungsunterstützung, wobei Echtzeit-Datenanalysen einen klaren Wettbewerbsvorteil für bessere Operationsergebnisse bieten. Das Marktwachstum hängt von der Demokratisierung der Technologie durch kostengünstigere, modulare Robotersysteme ab, die für kleinere Krankenhäuser und ambulante Einrichtungen konzipiert sind. Die Wettbewerbsdifferenzierung basiert nun auf leistungsgestützter Chirurgie, bei der Plattformen haptisches Feedback, 3D-Visualisierung und integrierte digitale Arbeitsabläufe bieten, um Sicherheit und Transparenz zu gewährleisten.

Marktübersicht für medizinische Roboter

Medizinische Roboter haben sich von experimentellen Nischenprodukten zu unverzichtbaren Bestandteilen moderner klinischer Infrastrukturen entwickelt. Der Markt umfasst ein breites Spektrum an Systemen, darunter OP-Assistenten, autonome Logistikroboter für Krankenhäuser, Automatisierungsplattformen für Apotheken und fortschrittliche Exoskelette für die Rehabilitation. Sowohl etablierte Medizintechnikkonzerne als auch agile Startups konkurrieren in diesem Markt und nutzen Technologien wie 5G-basierte Telechirurgie und Softrobotik. Die steigende Nachfrage nach ambulanten Eingriffen und wertorientierter Versorgung in Nordamerika und Europa hat die Beliebtheit kompakter Robotersysteme als mobile Lösung für Fachkliniken erhöht. Nordamerika ist aufgrund seiner fortschrittlichen Gesundheitsinfrastruktur und günstigen Erstattungspolitik führend im Umsatz, während der asiatisch-pazifische Raum rasante Fortschritte bei der Entwicklung eigener Technologien und deren großflächiger Anwendung in Krankenhäusern erzielt. Der US-Markt bleibt globaler Marktführer, angetrieben von einem hochentwickelten Gesundheitsökosystem und einer breiten klinischen Anwendung. Das Wachstum resultiert aus der hohen Nachfrage nach minimalinvasiven Eingriffen und fortschrittlicher Rehabilitation. Günstige Erstattungspolitik und erhebliche Investitionen in die chirurgische Automatisierung festigen die Position der USA als wichtiges Zentrum für technologische Innovation.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für medizinische Roboter: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Markttreiber und Chancen für medizinische Roboter

Markttreiber:

- Nachfrage nach minimalinvasiven Verfahren: Patienten und Ärzte bevorzugen zunehmend Verfahren mit kleineren Einschnitten, da diese zu weniger Schmerzen und schnelleren Genesungszeiten führen.

- Fortschritte in der KI- und Sensortechnologie: Die Integration hochentwickelter Sensoren und künstlicher Intelligenz ermöglicht eine höhere Präzision, Echtzeit-Feedback und eine verbesserte chirurgische Sicherheit.

- Personalmangel im Gesundheitswesen: Die Automatisierung in Apotheken und der Krankenhauslogistik trägt dazu bei, die Auswirkungen des Personalmangels abzumildern, indem sie sich wiederholende Aufgaben wie die Medikamentenausgabe und den Materialtransport übernimmt.

Marktchancen:

- Expansion in ambulante Operationszentren: Die Entwicklung kostengünstiger, platzsparender Robotersysteme speziell für ambulante Zentren bietet einen bedeutenden Wachstumspfad.

- Wachstum bei Telestroke und Fernchirurgie: Die Verbesserung der Telekommunikationsinfrastruktur bietet Spezialisten die Möglichkeit, Patienten in abgelegenen oder ländlichen Gebieten robotische Unterstützung zu leisten.

- Integration mit Digital-Twin-Technologie: Der Einsatz digitaler Zwillinge für die präoperative Planung und Simulation kann die Erfolgsraten von Eingriffen und die Effizienz der Chirurgenausbildung verbessern.

Marktbericht für medizinische Roboter: Segmentierungsanalyse

Der Marktanteil von Medizinrobotern wird in verschiedenen Segmenten analysiert, um ein besseres Verständnis seiner Struktur, seines Wachstumspotenzials und der aufkommenden Trends zu ermöglichen. Nachfolgend ist der in den meisten Branchenberichten verwendete Standard-Segmentierungsansatz dargestellt:

Nach Produkt:

- Chirurgische Roboter: Das größte Segment, mit Systemen, die für komplexe chirurgische Eingriffe mit verbesserter Geschicklichkeit und Visualisierung entwickelt wurden.

- Krankenhaus- und Apothekenroboter: Dazu gehören autonome mobile Roboter für die Auslieferung, Telepräsenzeinheiten und automatisierte Medikamentenausgabesysteme.

- Rehabilitationsroboter: Schwerpunkt sind Assistenzgeräte, Exoskelette und Therapieroboter, die die Mobilität und die körperliche Genesung von Patienten unterstützen.

- Nicht-invasive Radiochirurgie-Roboter: Hochpräzisionssysteme, die vorwiegend in der Onkologie eingesetzt werden, um gezielte Strahlung ohne chirurgische Einschnitte zu verabreichen.

- Sonstige: Dazu gehören spezialisierte Plattformen wie Mikroroboter und robotische Notfallreaktionseinheiten.

Auf Antrag:

- Laparoskopie: Ein dominantes Anwendungsgebiet, bei dem Roboter durch kleine Einschnitte bei abdominalen und thorakalen Eingriffen assistieren.

- Orthopädie: Bietet robotergestützte Technologie für Gelenkersatz, Wirbelsäulenoperationen und Knochenkonturierung.

- Neurologie: Systeme für hochpräzise Hirnchirurgie, Biopsien und Elektrodenplatzierung.

- Gynäkologie: Roboterplattformen werden für Hysterektomien und andere komplexe Eingriffe im Beckenbereich eingesetzt.

- Urologie: Eine der etabliertesten Anwendungen, vorwiegend bei Prostataoperationen und Nierenoperationen.

- Kardiologie: Zunehmender Einsatz von Robotern bei katheterbasierten Eingriffen und Herzklappenreparaturen.

- Sonstige: Dazu gehören Anwendungen in der Augenheilkunde, Zahnmedizin und Gefäßchirurgie.

Vom Endbenutzer:

- Krankenhäuser: Die Hauptanwender aufgrund des hohen Patientenaufkommens und der finanziellen Möglichkeiten, in groß angelegte Roboterinfrastruktur zu investieren.

- Ambulante Operationszentren: Ein schnell wachsendes Segment, da immer mehr Operationen vom stationären in den ambulanten Bereich verlagert werden.

- Sonstige: Umfasst Fachkliniken, Rehabilitationszentren und akademische Forschungseinrichtungen.

Nach Geographie:

- Nordamerika

- Europa

- Asien-Pazifik

- Süd- und Mittelamerika

- Naher Osten und Afrika

Berichtsumfang zum Markt für medizinische Roboter

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 15,98 Milliarden US-Dollar |

| Marktgröße bis 2034 | 61,27 Milliarden US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2026 - 2034) | 16,11 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2026–2034 |

| Abgedeckte Segmente |

Nebenprodukt

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte der Medizinroboter: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für medizinische Roboter wächst rasant, angetrieben durch die steigende Nachfrage der Endnutzer. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen, um den Kundenbedürfnissen gerecht zu werden, und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

Marktanteilsanalyse für medizinische Roboter nach Regionen

Der asiatisch-pazifische Raum wird voraussichtlich in den kommenden Jahren das schnellste Wachstum verzeichnen. Auch die aufstrebenden Märkte in Süd- und Mittelamerika, dem Nahen Osten und Afrika bieten zahlreiche ungenutzte Expansionsmöglichkeiten für führende Medizintechnikanbieter und Entwickler von Gesundheitsinfrastruktur.

Der Markt für Medizinroboter durchläuft einen tiefgreifenden digitalen Wandel und entwickelt sich von spezialisierten chirurgischen Instrumenten hin zu integrierten Plattformen für die autonome Gesundheitsversorgung. Das Wachstum wird durch die weltweite Expansion minimalinvasiver Chirurgie (MIS), den Aufstieg ambulanter Operationszentren und die Integration KI-gestützter Diagnostik angetrieben. Nachfolgend finden Sie eine Zusammenfassung der Marktanteile und Trends nach Regionen:

1. Nordamerika

- Marktanteil: Besitzt weltweit den größten Marktanteil, was auf hohe Gesundheitsausgaben und ein starkes Netzwerk spezialisierter Operationszentren zurückzuführen ist.

-

Wichtigste Einflussfaktoren:

- Weitverbreitete Anwendung robotergestützter Systeme in der Urologie und im orthopädischen Gelenkersatz.

- Frühe Integration von 5G- und KI-Technologien in chirurgische Plattformen.

- Günstige Erstattungspolitiken für robotergestützte Eingriffe in den USA und Kanada.

- Trends: Ein deutlicher Trend hin zu ambulanten Operationszentren (ASCs) und die Etablierung roboterassistierter Wirbelsäulen- und Herz-Kreislauf-Eingriffe.

2. Europa

- Marktanteil: Stellt einen bedeutenden Teil des globalen Marktes dar, gestützt auf fortschrittliche klinische Forschung und einen starken Fokus auf Rehabilitationsrobotik.

-

Wichtigste Einflussfaktoren:

- Hohe Inlandsnachfrage nach fortschrittlichen neurologischen und geriatrischen Versorgungssystemen.

- Starke staatliche Unterstützung für öffentlich-private Partnerschaften im Bereich der Automatisierung im Gesundheitswesen.

- Ausgereifte regulatorische Rahmenbedingungen gewährleisten hohe Standards für die Sicherheit von Medizinprodukten.

- Trends: Strategischer Fokus auf modulare Roboterarme, die von mehreren Krankenhausabteilungen gemeinsam genutzt werden können, um den Return on Investment und die Kosteneffizienz zu maximieren.

3. Asien-Pazifik

- Marktanteil: Die am schnellsten wachsende Region, wobei China, Japan und Indien die wichtigsten Märkte für die Modernisierung von Krankenhäusern im großen Stil darstellen.

-

Wichtigste Einflussfaktoren:

- Massive Investitionen in intelligente Gesundheitsinfrastruktur zur Unterstützung der wachsenden städtischen Bevölkerung.

- Regierungsinitiativen mit Schwerpunkt auf der Herstellung hochwertiger inländischer Medizinprodukte.

- Steigende verfügbare Einkommen führen zu einer Präferenz für präzise, minimalinvasive Behandlungen.

- Trends: Hohe Abhängigkeit von einheimischen technologischen Innovationen und B2B-Verträgen für die Automatisierung von Krankenhäusern und Apotheken zur Bewältigung hoher Patientenzahlen.

4. Süd- und Mittelamerika

- Marktanteil: Aufstrebender Markt mit einem wachsenden privaten Gesundheitssektor in Ländern wie Brasilien und Chile.

-

Wichtigste Einflussfaktoren:

- Das Bewusstsein für die klinischen Vorteile roboterassistierter Chirurgie zur schnelleren Genesung wird gestärkt.

- Modernisierung privater chirurgischer Kliniken zu Hightech-Zentren zur Anwerbung von Medizintouristen.

- Zunehmendes Interesse an laparoskopischen und robotergestützten gynäkologischen Anwendungen.

- Trends: Wachstum von spezialisierten chirurgischen Zentren und Einführung von generalüberholten Robotersystemen zur Verbesserung der Zugänglichkeit für Bevölkerungsgruppen mit mittlerem Einkommen.

5. Naher Osten und Afrika

- Marktanteil: Entwicklungsmarkt mit tiefgreifenden strategischen Investitionen in digitale Gesundheitszentren in der gesamten Golfregion.

-

Wichtigste Einflussfaktoren:

- Strategischer Schwerpunkt auf der Reduzierung der Abhängigkeit von ausländischer medizinischer Expertise durch lokale, hochmoderne Operationszentren.

- Hohe Nachfrage nach Telepräsenz- und autonomen Lieferrobotern in modernen Krankenhauskomplexen.

- Investitionen in die Infrastruktur zur Finanzierung modernster medizinischer Einrichtungen.

- Trends: Einsatz von telechirurgischen Plattformen zur spezialisierten Versorgung in unterversorgten Gebieten, verbunden mit einem Fokus auf robotische Apothekensysteme zur Steigerung der betrieblichen Effizienz.

Hohe Marktdichte und starker Wettbewerb

Der Wettbewerb verschärft sich aufgrund der Präsenz etablierter Marktführer wie Intuitive Surgical, Stryker und Medtronic. Regionale Innovatoren und Nischenanbieter wie CMR Surgical und Asensus Surgical sowie Orthopädiespezialisten wie Zimmer Biomet und Smith & Nephew tragen ebenfalls zu einem vielfältigen und schnell wachsenden Marktumfeld bei.

Dieses wettbewerbsintensive Umfeld zwingt die Anbieter dazu, sich durch Folgendes zu differenzieren:

- Wertorientierte Preismodelle: Unternehmen bieten Leasing- und Pay-per-Procedure-Modelle an, um die Robotertechnologie auch kleineren Krankenhäusern zugänglicher zu machen.

- Fortschrittliche Bildintegration: Echtzeit-3D-Mapping und Fluoreszenzbildgebung werden zu Standardfunktionen, um die chirurgische Genauigkeit zu verbessern.

- Verbesserte Ausbildung von Chirurgen: Bereitstellung umfassender Virtual-Reality-Simulationsplattformen zur Verkürzung der Lernkurve für das klinische Personal.

Chancen und strategische Schritte

- Partnerschaften mit ambulanten Operationszentren (ASCs): Nutzen Sie die steigende Nachfrage nach ambulanten Eingriffen, indem Sie kompakte, kostengünstige Robotersysteme entwickeln, die speziell für kleinere Operationssäle geeignet sind.

- Integration von KI und maschinellem Lernen: Durch die Integration von prädiktiven Analysen und intraoperativer Echtzeitführung ist das Angebot für High-End-Krankenhäuser attraktiv, die ihre Erfolgsraten bei Operationen verbessern und menschliche Fehler reduzieren möchten.

Die wichtigsten Unternehmen, die auf dem Markt für medizinische Roboter tätig sind, sind:

- Abbott

- F. Hoffmann-La Roche Ltd.

- Immunexpress Inc.

- BD

- Danaher

- Luminex Corporation

- Thermo Fisher Scientific Inc.

- bioMerieux SA.

- T2 Biosystems, Inc.

- Axis-Shield Diagnostics Ltd.

Hinweis: Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge geordnet.

Neuigkeiten und aktuelle Entwicklungen auf dem Markt für medizinische Roboter

- Im Mai 2026 gab Johnson & Johnson die Ergebnisse der ersten klinischen Studie des experimentellen robotergestützten chirurgischen Systems OTTAVA™ bekannt. Es handelte sich um eine prospektive, multizentrische klinische Studie zur Bewertung der Sicherheit und Leistungsfähigkeit des Systems bei Roux-en-Y-Magenbypass-Operationen.

- Im Mai 2026 gab die Olympus Corporation (Olympus), ein weltweit tätiges Medizintechnikunternehmen, das sich der Weiterentwicklung der Endoskopie verschrieben hat, die Unterzeichnung eines exklusiven globalen Vertriebsabkommens mit EndoRobotics Co., Ltd. bekannt. Gemäß dieser Vereinbarung werden die von EndoRobotics hergestellten robotergestützten Technologien exklusiv von Olympus als Teil des EndoTherapy-Portfolios weltweit vertrieben. Diese Zusammenarbeit wird die breitere Anwendung fortschrittlicher endoskopischer Verfahren wie der endoskopischen Submukosadissektion (ESD) fördern und Klinikern helfen, organerhaltende, minimalinvasive Behandlungen präzise und sicher durchzuführen.

Marktbericht zu Medizinrobotern: Abdeckung und Ergebnisse

Der Bericht „Marktgröße und Prognose für medizinische Roboter (2021–2034)“ bietet eine detaillierte Analyse des Marktes und deckt folgende Bereiche ab:

- Marktgröße und Prognose für medizinische Roboter auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Geltungsbereich abgedeckt werden

- Markttrends für medizinische Roboter sowie Marktdynamiken wie Treiber, Hemmnisse und wichtige Chancen

- Detaillierte PEST- und SWOT-Analyse

- Marktanalyse für medizinische Roboter: Wichtige Markttrends, globale und regionale Rahmenbedingungen, Hauptakteure, regulatorische Rahmenbedingungen und aktuelle Marktentwicklungen

- Branchenlandschafts- und Wettbewerbsanalyse mit Fokus auf Marktkonzentration, Heatmap-Analyse, prominente Akteure und aktuelle Entwicklungen auf dem Markt für medizinische Roboter.

- Detaillierte Unternehmensprofile

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends