Marktstrategien für elektronische Gesundheitsakten, Top-Player, Wachstumschancen, Analyse und Prognose bis 2031

Marktgröße und Prognose für elektronische Patientenakten (2021 – 2031), Bericht über globale und regionale Anteils-, Trend- und Wachstumschancenanalyse: Nach Installationstyp (Cloud-basiert und vor Ort), Typ (Akut-EHR, Ambulante EHR und Postakute EHR), Anwendung (Klinische Aufzeichnungen, Verwaltungsaufgaben und Abrechnung, Arztunterstützung und Patientenportal), Vertriebskanal (Krankenhäuser und Kliniken, Ambulante Pflegezentren und Arztpraxen oder Fachpflegezentren) und Geografie (Nordamerika, Europa, Asien-Pazifik, Naher Osten und Afrika, Süd- und Mittelamerika)

- Status : Veröffentlicht

- Berichtscode : TIPHE100000822

- Kategorie : Technologie, Medien und Telekommunikation

- Anzahl der Seiten : 248

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 10, 2026

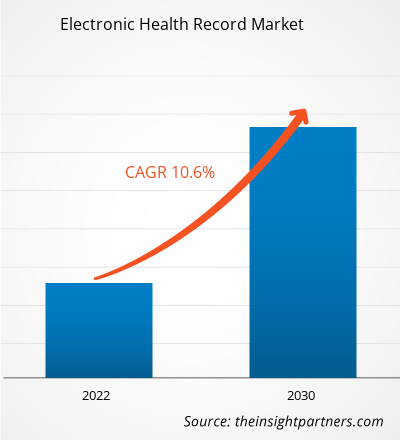

[Forschungsbericht] Der Markt für elektronische Patientenakten soll von 33.144,25 Millionen US-Dollar im Jahr 2022 auf 74.233,46 Millionen US-Dollar im Jahr 2030 wachsen; für den Zeitraum 2022–2030 wird eine durchschnittliche jährliche Wachstumsrate (CAGR) von 10,6 % erwartet.

Markteinblicke und Analystenmeinung:

Eine elektronische Patientenakte eines Anbieters enthält wichtige administrative und klinische Daten von Patienten, darunter demografische Daten, Verlaufsberichte, Gesundheitsprobleme, Medikamente, Vitalfunktionen, Anamnese, Impfungen, Labordaten und Röntgenberichte. Die elektronische Patientenakte automatisiert den Zugriff auf Informationen und hat das Potenzial, den Arbeitsablauf des Arztes zu optimieren. Die elektronische Patientenakte kann über verschiedene Schnittstellen auch andere pflegebezogene Aktivitäten unterstützen, darunter evidenzbasierte Entscheidungsunterstützung, Qualitätsmanagement und Ergebnisberichterstattung. Der Markt für elektronische Patientenakten wird maßgeblich durch die zunehmende Zahl von Medikationsfehlern und steigende Anreize seitens der Bundesregierung angetrieben.

Wachstumstreiber:

Zunehmende Nutzung elektronischer Patientenakten

Elektronische Patientenakten erfreuen sich mit der zunehmenden Digitalisierung des Gesundheitswesens zunehmender Beliebtheit. Laut The New England Journal of Medicine stellte die Bundesregierung, sobald der Health Information Technology for Economic and Clinical Health (HITECH) Act 2009 in Kraft trat, 300 Millionen US-Dollar bereit, um Gesundheitseinrichtungen bei der Einführung eines landesweiten Systems zum Austausch von Gesundheitsinformationen zu unterstützen. Die Centers for Medicare and Medicaid Services (CMS) boten zudem Anreizzahlungen in Höhe von über 35 Milliarden US-Dollar für die Einführung elektronischer Patientenakten. Laut dem Office of the National Coordinator for Health Information Technology (ONC) führten im Jahr 2021 etwa vier von fünf niedergelassenen Ärzten (78 %) und fast alle nicht-bundesstaatlichen Akutkrankenhäuser (96 %) zertifizierte elektronische Patientenakten ein. Dies markierte einen beachtlichen Fortschritt in den letzten zehn Jahren, in denen seit 2011 28 % der Krankenhäuser und 34 % der Ärzte elektronische Patientenakten eingeführt hatten. Laut Daten von Definitive Healthcare aus dem Jahr 2020 setzten mehr als 89 % aller Krankenhäuser elektronische Patientenaktensysteme für stationäre oder ambulante Patienten ein.

Darüber hinaus plante die US-Bundesregierung im Mai 2020 den Federal Health IT Strategic Plan 2020–2025, um die Verwendung elektronischer Patientenakten durch Gesundheitsdienstleister vorzuschreiben.

Regierungsinitiativen zur Förderung der IT-Nutzung im Gesundheitswesen treiben den Markt an. Beispielsweise ist My Health Record Australiens nationale Plattform für digitale Patientenakten. Jeder australische Bürger hat ein „My Health Record“. Darüber hinaus wird erwartet, dass die Einführung technologisch fortschrittlicher Gesundheitsdienste das Wachstum des Marktes für elektronische Patientenakten vorantreiben wird. Anhand der oben genannten Fakten und Statistiken ist ersichtlich, dass sich die Akzeptanz elektronischer Patientenakten im Prognosezeitraum voraussichtlich weiter verbessern wird.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für elektronische Patientenakten: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

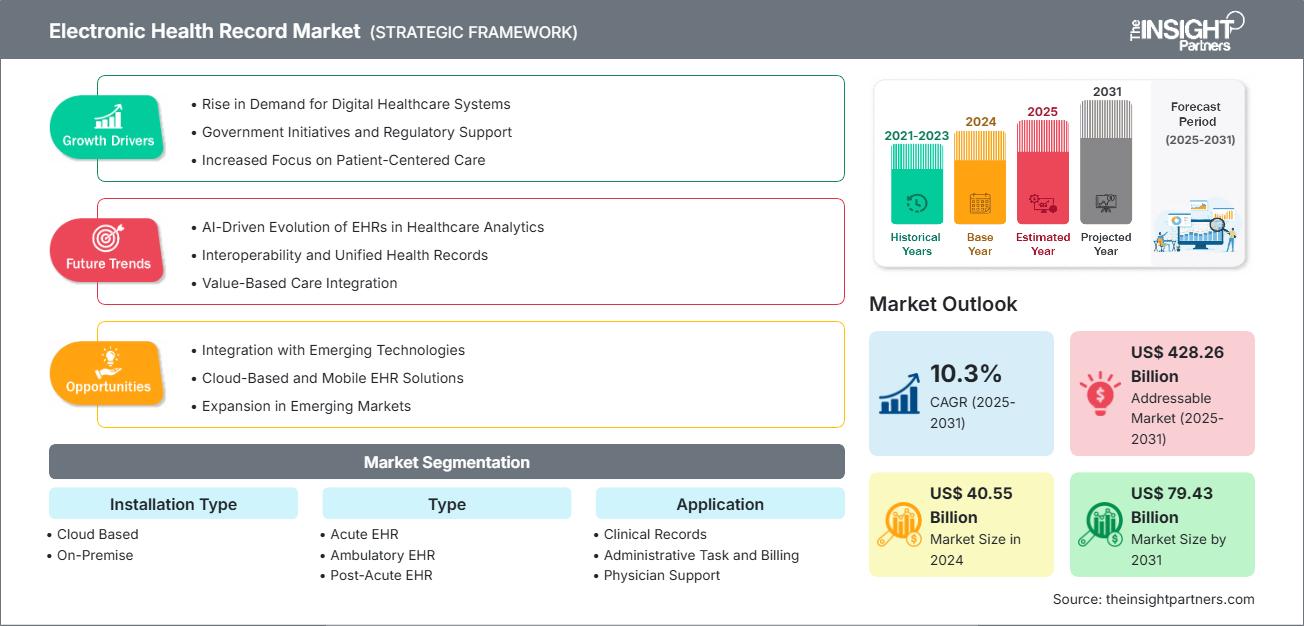

Der Markt für elektronische Patientenakten ist nach Installationsart, Typ, Anwendung und Endbenutzer segmentiert. Basierend auf der Installationsart wird der Markt in Cloud-basiert und vor Ort aufgeteilt. Hinsichtlich des Typs wird der Markt für elektronische Patientenakten in elektronische Patientenakten für akute Fälle, ambulante elektronische Patientenakten und elektronische Patientenakten für die postakute Behandlung unterteilt. Nach Anwendung wird der Markt in klinische Aufzeichnungen, Verwaltungsaufgaben und Abrechnung, Arztunterstützung und Patientenportal segmentiert. Nach Endbenutzer wird der Markt in Krankenhäuser und Kliniken, Arztpraxen/Fachzentren und ambulante chirurgische Zentren segmentiert.

Segmentanalyse:

Nach der Installationsart wird der Markt für elektronische Patientenakten in Cloud-basiert und vor Ort aufgeteilt. Das Cloud-basierte Segment hatte 2022 einen größeren Marktanteil und wird voraussichtlich zwischen 2022 und 2030 eine höhere durchschnittliche jährliche Wachstumsrate (CAGR) verzeichnen. Eine Cloud-basierte elektronische Patientenakte ermöglicht die Speicherung von Patientenakten in der Cloud statt auf den internen Servern der Gesundheitseinrichtung. Die gesammelten Daten werden in umsetzbaren und gemeinsam nutzbaren Formaten organisiert und gepflegt, um eine effektive Kommunikation zwischen Gesundheitsdienstleistern, Drittzahlern und Patienten zu ermöglichen. Cloud-basierte elektronische Patientenakten sind bei Ärzten und Gesundheitsdienstleistern mit kleinerem Praxisumfang beliebt. Diese Systeme können ohne eigene Server installiert werden und bieten eine breite Palette an Anpassungen und Verbesserungen je nach Bedarf.

Der Markt für elektronische Patientenakten ist nach Typ segmentiert in akute elektronische Patientenakten, ambulante elektronische Patientenakten und postakute elektronische Patientenakten. Das Segment der akuten elektronischen Patientenakten hatte 2022 den größten Marktanteil, und das Segment der postakuten elektronischen Patientenakten wird voraussichtlich zwischen 2022 und 2030 die höchste CAGR verzeichnen. Zu den postakuten Pflegeeinrichtungen gehören Rehabilitationszentren, ambulante Pflegedienste und Langzeitpflegekrankenhäuser. Rehabilitationszentren bieten Patienten mit neurologischen, kardiovaskulären, muskuloskelettalen, orthopädischen und anderen Erkrankungen Schulungen, medizinisch überwachte Übungen und Unterstützung an.

Der Markt für elektronische Patientenakten ist in die Anwendungsbereiche klinische Aufzeichnungen, Verwaltungsaufgaben und Abrechnung, Arztunterstützung und Patientenportal unterteilt. Das Segment klinische Aufzeichnungen hatte 2022 den größten Marktanteil und wird voraussichtlich zwischen 2022 und 2030 die höchste durchschnittliche jährliche Wachstumsrate (CAGR) verzeichnen. Ein klinisches Dokument enthält Informationen zur Pflege und den dem Patienten bereitgestellten Leistungen. Es erhöht die Bedeutung elektronischer Patientenakten, indem es die elektronische Erfassung klinischer Berichte, Patientenbeurteilungen und Verlaufsberichte ermöglicht. Ein klinisches Dokument kann Notizen von Ärzten, Pflegekräften und anderen Klinikern, relevante Daten und Zeiten im Zusammenhang mit dem Dokument, die Ausführenden der beschriebenen Pflege, Flussdiagramme (Vitalzeichen, Input und Output und Problemlisten), perioperative Notizen, Entlassungsberichte, Transkriptionsdokumentenverwaltung und Abstracts von Krankenakten enthalten.

Basierend auf dem Endnutzer ist der Markt für elektronische Patientenakten in Krankenhäuser und Kliniken, Arztpraxen/Fachzentren und ambulante chirurgische Zentren segmentiert. Das Segment Krankenhäuser und Kliniken hatte 2022 den größten Anteil am Markt für elektronische Patientenakten und wird zwischen 2022 und 2030 voraussichtlich die höchste durchschnittliche jährliche Wachstumsrate (CAGR) auf dem Markt verzeichnen. Krankenhäuser und Kliniken sind die primären Anlaufstellen für Patienten, um ihre Diagnose zu erhalten und Behandlungsmöglichkeiten und -alternativen zu wählen. Die verfügbare Infrastruktur in Krankenhäusern und Kliniken kann eine qualitativ hochwertige Versorgung für alle Krankheitszustände bieten, da sie Zugang zu fortschrittlichen medizinischen Geräten haben. Das Segment Krankenhäuser und Kliniken wird voraussichtlich einen beträchtlichen Anteil halten, da die meisten Patienten in Schwellen- und Industrieländern bei gesundheitlichen Problemen lieber Krankenhäuser aufsuchen.

Regionale Analyse:

Geografisch ist der globale Markt für elektronische Patientenakten in die Regionen Asien-Pazifik, Europa, Naher Osten und Afrika, Nordamerika sowie Süd- und Mittelamerika unterteilt. Im Jahr 2022 hatte Nordamerika den größten Anteil am globalen Markt für elektronische Patientenakten. Der Asien-Pazifik-Raum wird zwischen 2022 und 2030 voraussichtlich die höchste durchschnittliche jährliche Wachstumsrate verzeichnen.

Der nordamerikanische Markt für elektronische Patientenakten ist in die USA, Kanada und Mexiko aufgeteilt. Die USA sind der größte Markt für elektronische Patientenakten in Nordamerika. Der Markt wird maßgeblich durch die Transformation des digitalen Gesundheitswesens, die steigende Zahl chronischer Krankheiten und die Unterstützung der Bundesregierung bei der Einführung elektronischer Patientenakten zur Verbesserung der Versorgungsqualität vorangetrieben. Weitere Faktoren wie die Einführung fortschrittlicher Softwaretechnologien im Gesundheitswesen, eine steigende Zahl von Krankenhäusern und die Umsetzung strategischer Regierungsrichtlinien fördern das Wachstum des Marktes für elektronische Patientenakten. Der Bedarf an automatisierten Systemen aufgrund der steigenden Patientenzahlen und der Ressourcenknappheit im Gesundheitswesen dürfte die Einführung elektronischer Patientenakten in den USA zusätzlich vorantreiben. Auch die Reduzierung von Fehlern in der Krankenhausverwaltung, die zu zahlreichen Todesfällen führt, dürfte das Marktwachstum im Prognosezeitraum maßgeblich ankurbeln. Einer im Journal of Patient Safety veröffentlichten Studie zufolge sterben in den USA jährlich schätzungsweise 400.000 Patienten aufgrund von Verwaltungsfehlern.

Elektronische Patientenakten

Regionale Einblicke in den Markt für elektronische GesundheitsaktenDie Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Markt für elektronische Patientenakten im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Lage elektronischer Patientenakten in Nordamerika, Europa, dem asiatisch-pazifischen Raum, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika erörtert.

Umfang des Marktberichts über elektronische Patientenakten

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2024 | US$ 40.55 Billion |

| Marktgröße nach 2031 | US$ 79.43 Billion |

| Globale CAGR (2025 - 2031) | 10.3% |

| Historische Daten | 2021-2023 |

| Prognosezeitraum | 2025-2031 |

| Abgedeckte Segmente |

By Installationstyp

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Marktteilnehmer für elektronische Patientenakten: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für elektronische Patientenakten wächst rasant. Die steigende Nachfrage der Endnutzer ist auf Faktoren wie veränderte Verbraucherpräferenzen, technologische Fortschritte und ein stärkeres Bewusstsein für die Produktvorteile zurückzuführen. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Markt für elektronische Patientenakten Übersicht der wichtigsten Akteure

Nachfolgend sind verschiedene Initiativen wichtiger Akteure auf dem Markt für elektronische Patientenakten aufgeführt:

- Im November 2023 hat eClinicalWorks LLC KI-Assistenztools auf den Markt gebracht, die medizinische Dokumente problemlos in die Patientendokumente übersetzen. Muttersprache innerhalb der elektronischen Patientenakte.

- Im September 2023 kündigte Oracle bedeutende Erweiterungen seiner Gesundheitslösungen an, darunter neue Cloud-basierte Funktionen für elektronische Patientenakten, generative KI-Dienste, öffentliche Anwendungsprogrammierschnittstellen (APIs) und Backoffice-Erweiterungen für die Gesundheitsbranche.

Wettbewerbslandschaft und Schlüsselunternehmen:

Oracle Corp, AltexSoft Inc, Veradigm Inc, Greenway Health LLC, eClinicalWorks LLC, Infor-Med Inc, Microwize Technology Inc, Athenahealth Inc, ChipSoft BV, CureMD.com Inc, AdvancedMD Inc und PracticeSuite Inc gehören zu den führenden Unternehmen auf dem Markt für elektronische Patientenakten. Diese Unternehmen konzentrieren sich auf neue Technologien, die Weiterentwicklung bestehender Produkte und geografische Expansionen, um der weltweit wachsenden Verbrauchernachfrage gerecht zu werden.

Ankita ist eine dynamische Marktforschungs- und Beratungsexpertin mit über 8 Jahren Erfahrung in den Bereichen Technologie, Medien, IKT sowie Elektronik und Halbleiter. Sie hat über 100 Beratungs- und Forschungsaufträge für globale Kunden wie Microsoft, Oracle, NEC Corporation, SAP, KPMG und Expeditors International erfolgreich geleitet und durchgeführt. Zu ihren Kernkompetenzen gehören Marktbewertung, Datenanalyse, Prognose, Strategieformulierung, Wettbewerbsbeobachtung und das Verfassen von Berichten. Ankita ist versiert in der Abwicklung kompletter Projektzyklen – von der Angebotserstellung vor dem Verkauf und Kundengesprächen bis hin zur Bereitstellung umsetzbarer Erkenntnisse nach dem Verkauf. Sie ist versiert in der Leitung funktionsübergreifender Teams, der Strukturierung komplexer Forschungsmodule und der Ausrichtung von Lösungen an kundenspezifischen Geschäftszielen. Ihre ausgezeichneten Kommunikationsfähigkeiten, Führungsqualitäten und Präsentationsfähigkeiten haben es ihr ermöglicht, in einem schnelllebigen und sich entwickelnden Marktumfeld stets wertorientierte Ergebnisse zu liefern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends