Marktanalyse und Prognose zur Verabreichung von Arzneimitteln über das Auge nach Größe, Anteil, Wachstum, Trends 2028

Marktprognose für okuläre Arzneimittelverabreichung bis 2028 – Auswirkungen von COVID-19 und globale Analyse nach Technologie (implantierbare okuläre Arzneimittelverabreichungssysteme, partikuläre Arzneimittelverabreichungssysteme, Nanopartikel-Arzneimittelverabreichungssystem und andere), Formulierungstyp (Liposomen und Nanopartikel, Lösung, Emulsion, Suspension und Salbe), Krankheitstyp (Glaukom, diabetische Retinopathie, Syndrom des trockenen Auges, Makuladegeneration, Katarakt, diabetisches Makulaödem und andere) und Endbenutzer (Krankenhäuser, Augenkliniken und ambulante chirurgische Zentren) und Geografie

- Status : Veröffentlicht

- Berichtscode : TIPRE00004206

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 171

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 13, 2024

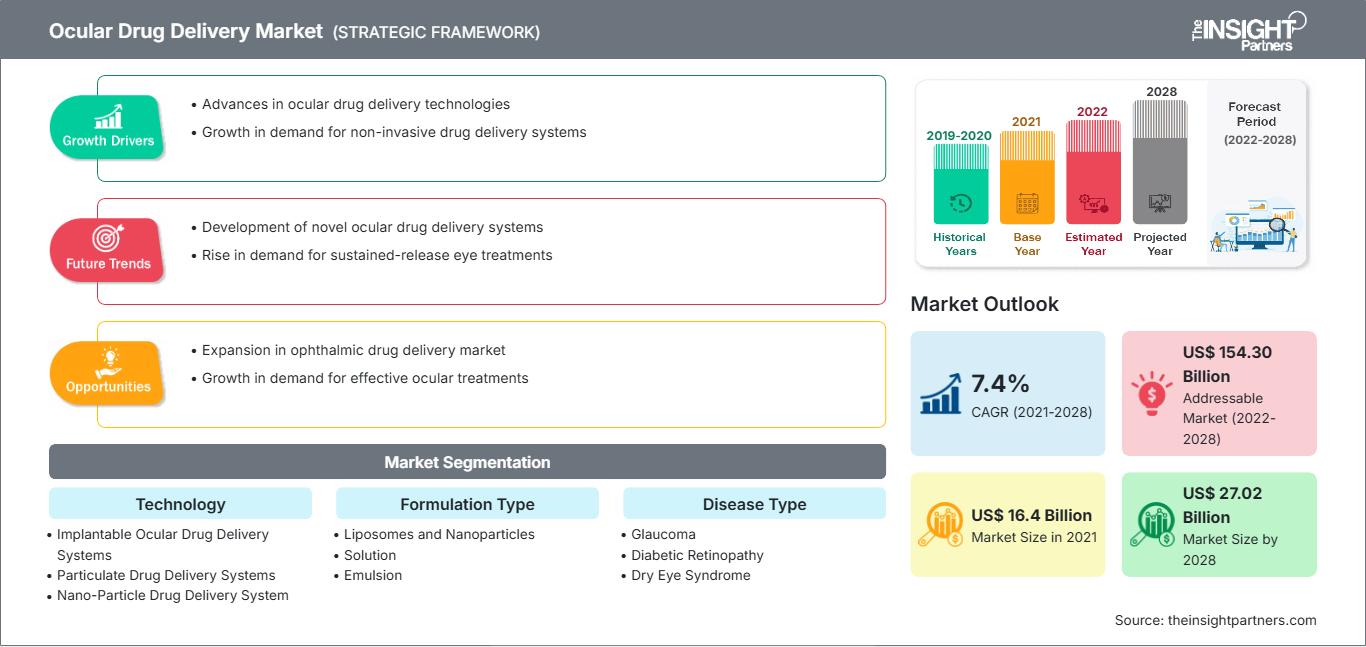

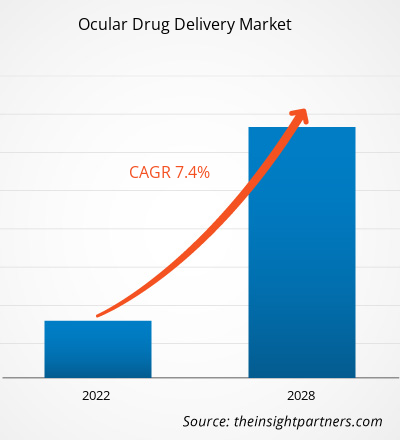

Der Markt für okuläre Arzneimittelverabreichung wurde im Jahr 2021 auf 16.404,32 Millionen US-Dollar geschätzt und soll bis 2028 27.016,20 Millionen US-Dollar erreichen; von 2021 bis 2028 wird ein CAGR-Wachstum von 7,4 % erwartet.

Ein okuläres Arzneimittelverabreichungssystem (ODDS) ist eine Darreichungsform, ein Vehikel oder ein System zur Verabreichung oder Freisetzung von Arzneimitteln in das Auge gegen Krankheiten oder Störungen, die das Sehvermögen betreffen oder beeinträchtigen. Das Angebot reicht von einfachen sterilen Augentropfen für die Augenoberfläche bis hin zu komplexen Implantaten für intraokulares Gewebe. Okuläre Arzneimittelformulierungen sind vorwiegend flüssige Formen wie Lösungen, Suspensionen und Emulsionen zur Behandlung von Erkrankungen des vorderen Augenabschnitts. Diese Formulierungen können in Form von fortschrittlichen Arzneimittelverabreichungssystemen wie In-situ-Gel, Mikroemulsion, Nanopartikel, Liposomen, Iontophorese, Nanosuspension und okulären Einsätzen erhältlich sein.

Der Markt für okuläre Arzneimittelverabreichung wurde nach Technologie, Formulierungstyp, Krankheitstyp, Endverbraucher und Geografie segmentiert. Geografisch unterteilt sich der Markt hauptsächlich in Nordamerika, Europa, den asiatisch-pazifischen Raum, den Nahen Osten und Afrika sowie Süd- und Mittelamerika. Der Bericht bietet Einblicke und eine detaillierte Analyse des Marktes für okuläre Arzneimittelverabreichung und legt dabei Wert auf Parameter wie Markttrends, technologische Fortschritte und Marktdynamik sowie eine Analyse der Wettbewerbslandschaft der weltweit führenden Marktteilnehmer.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für okuläre Arzneimittelverabreichung: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

Markteinblicke: Zunehmende Prävalenz von Augenerkrankungen fördert Wachstum des Marktes für okuläre Arzneimittelverabreichung

Die weltweit häufigsten Ursachen für Blindheit oder Sehschwäche sind Katarakt, Glaukom, altersbedingte Makuladegeneration, diabetische Retinopathie und unbehandelte Refraktionsfehler. Die Mehrheit der Weltbevölkerung leidet oder hatte im Laufe ihres Lebens eine Augenerkrankung. Laut dem im Februar 2021 veröffentlichten Bericht „Blindheit und Sehbehinderung“ der Weltgesundheitsorganisation (WHO) leiden weltweit rund 2,2 Milliarden Menschen an einer Sehbehinderung im Nah- oder Fernbereich. Schätzungen zufolge sind Katarakt (94 Millionen) und unkorrigierte Refraktionsfehler (88,4 Millionen) die häufigsten Ursachen für Sehverlust oder Sehschwäche. Weitere häufige Ursachen für Sehverlust sind Glaukom (7,7 Millionen), Hornhauttrübungen (4,2 Millionen), diabetische Retinopathie (3,9 Millionen) und Trachom (2 Millionen).

Laut dem National Eye Institute (NEI) wird sich die Zahl der Menschen mit Katarakt in den USA voraussichtlich von 24,4 Millionen im Jahr 2010 auf etwa 50 Millionen im Jahr 2050 verdoppeln. Dem Factsheet „Glaucoma: Facts & Figures 2019“ zufolge leben in den USA über 3 Millionen Menschen mit Glaukom. Darüber hinaus waren laut der Canadian Survey on Disabilities 2017 1,5 Millionen Kanadier erblindet und rund 5,59 Millionen hatten eine Augenkrankheit, die zu weiterem Sehverlust führen könnte.

Darüber hinaus waren laut dem Royal National Institute of Blind People im Jahr 2017 in Großbritannien rund 350.000 Menschen als blind und sehbehindert registriert, etwa 173.735 waren als stark sehbehindert und 176.125 als sehbehindert registriert.

Technologiebasierte Erkenntnisse

Basierend auf der Technologie ist der Markt für okuläre Arzneimittelverabreichung in implantierbare okuläre Arzneimittelverabreichungssysteme, partikuläre Arzneimittelverabreichungssysteme, Nanopartikel-Arzneimittelverabreichungssysteme und andere unterteilt. Das Segment der implantierbaren okulären Arzneimittelverabreichungssysteme dürfte 2021 den größten Marktanteil einnehmen und im Prognosezeitraum voraussichtlich die höchste durchschnittliche jährliche Wachstumsrate (CAGR) verzeichnen.

Erkenntnisse nach Formulierungstyp

Basierend auf dem Formulierungstyp ist der Markt für okuläre Arzneimittelverabreichung in Liposomen und Nanopartikel, Lösung, Emulsion, Suspension und Salbe unterteilt. Das Lösungssegment dürfte 2021 den größten Marktanteil einnehmen und wird voraussichtlich zwischen 2021 und 2028 die höchste durchschnittliche jährliche Wachstumsrate (CAGR) verzeichnen. Das Wachstum des Lösungssegments ist auf die zunehmende Verbreitung von okulären Arzneimittelverabreichungssystemen in Lösungsform wie Augentropfen und Injektionen zurückzuführen.

Erkenntnisse basierend auf Krankheitstypen

Basierend auf dem Krankheitstyp ist der Markt für okuläre Arzneimittelverabreichung in Glaukom, diabetische Retinopathie, trockenes Auge, Makuladegeneration, Katarakt, diabetisches Makulaödem und andere unterteilt. Das Kataraktsegment dürfte 2021 den größten Marktanteil ausmachen. Der Markt für dieses Segment wird voraussichtlich von 2021 bis 2028 mit der höchsten CAGR wachsen.

Erkenntnisse basierend auf Endbenutzern

Basierend auf dem Endbenutzer ist der Markt für okuläre Arzneimittelverabreichung in Krankenhäuser, Augenkliniken und ambulante chirurgische Zentren unterteilt. Das Segment Krankenhäuser dürfte 2021 den größten Marktanteil halten, während das Segment Augenkliniken im Prognosezeitraum voraussichtlich die höchste durchschnittliche jährliche Wachstumsrate (CAGR) verzeichnen wird.

Die COVID-19-Pandemie hat sich weltweit zur größten Herausforderung entwickelt. Da diese Pandemie die Gesundheitssysteme weltweit belastet hat, war es unerlässlich, die begrenzten Ressourcen zu priorisieren, um Krankenhauseinweisungen zu minimieren. Trotz der gestiegenen Nachfrage nach Augentherapeutika wie Augentropfen, -salben und -suspensionen kam es jedoch zu einem Mangel an diesen Produkten, als neue Verbraucher auf den Markt kamen. Aufgrund von Lieferengpässen sehen sich die Hersteller außerdem mit steigenden Preisen und einem möglichen Mangel an Rohstoffen konfrontiert. Mit der Aufhebung der Beschränkungen und der Wiederaufnahme der Geschäftstätigkeit normalisieren sich die Angebots- und Nachfragevariablen jedoch wieder. Dies bietet zahlreiche Wachstumsaussichten für Therapeutika zur Verabreichung von Arzneimitteln am Auge.

Akquisitionen, Kooperationen, Partnerschaften, Produkteinführungen und Expansionen sind gängige Strategien von Unternehmen, um ihre Präsenz weltweit auszubauen und die wachsende Nachfrage zu decken. Die Akteure auf dem Markt für okuläre Arzneimittelverabreichung verfolgen vor allem die Strategie der Produktinnovation, um der sich weltweit ändernden Kundennachfrage gerecht zu werden, was ihnen auch dabei hilft, ihren Markennamen weltweit zu behaupten.

Okulare Arzneimittelverabreichung

Regionale Einblicke in den Markt für okuläre ArzneimittelverabreichungDie Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Markt für okuläre Arzneimittelverabreichung im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Verteilung der okulären Arzneimittelverabreichung in Nordamerika, Europa, dem asiatisch-pazifischen Raum, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika erörtert.

Umfang des Marktberichts zur okulären Arzneimittelverabreichung

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2021 | US$ 16.4 Billion |

| Marktgröße nach 2028 | US$ 27.02 Billion |

| Globale CAGR (2021 - 2028) | 7.4% |

| Historische Daten | 2019-2020 |

| Prognosezeitraum | 2022-2028 |

| Abgedeckte Segmente |

By Technologie

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Marktteilnehmer im Bereich der okulären Arzneimittelverabreichung: Verständnis ihrer Auswirkungen auf die Geschäftsdynamik

Der Markt für okuläre Arzneimittelverabreichung wächst rasant. Dies wird durch die steigende Endverbrauchernachfrage aufgrund veränderter Verbraucherpräferenzen, technologischer Fortschritte und eines stärkeren Bewusstseins für die Produktvorteile vorangetrieben. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Markt für okuläre Arzneimittelverabreichung Übersicht der wichtigsten Akteure

- AbbVie Inc.

- Bausch Health Companies Inc.

- Taiwan Liposome Company, Ltd.

- Ocular Therapeutix, Inc.

- GRAYBUG VISION, INC.

- Alimera Sciences, Inc.

- Envisia Therapeutics

- Novartis AG

- EYEGATE PHARMACEUTICALS, INC

- Clearside Biomedical, Inc.

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends