Analisi e previsioni del mercato della somministrazione di farmaci oculari per dimensione, quota, crescita, tendenze 2028

Previsioni di mercato per la somministrazione di farmaci oculari fino al 2028 - Impatto del COVID-19 e analisi globale per tecnologia (sistemi di somministrazione di farmaci oculari impiantabili, sistemi di somministrazione di farmaci in particelle, sistemi di somministrazione di farmaci con nanoparticelle e altri), tipo di formulazione (liposomi e nanoparticelle, soluzione, emulsione, sospensione e unguento), tipo di malattia (glaucoma, retinopatia diabetica, sindrome dell'occhio secco, degenerazione maculare, cataratta, edema maculare diabetico e altri) e utente finale (ospedali, cliniche oftalmiche e centri chirurgici ambulatoriali) e area geografica

- Stato : Edito

- Codice del report : TIPRE00004206

- Categoria : Scienze della vita

- Numero di pagine : 171

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : June 13, 2024

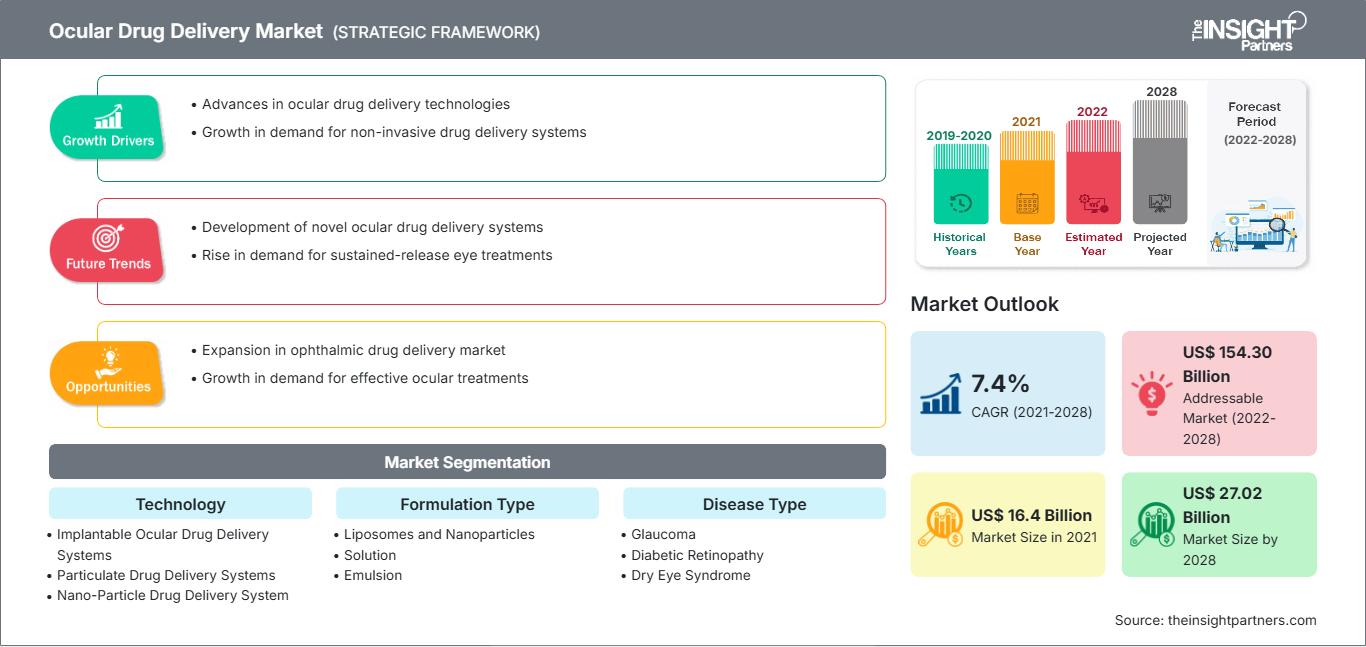

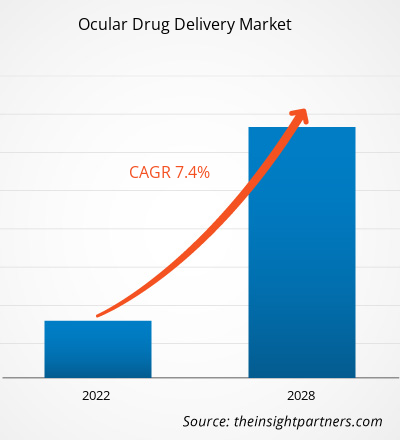

Il mercato dei sistemi di somministrazione di farmaci oculari è stato valutato a 16.404,32 milioni di dollari nel 2021 e si prevede che raggiungerà i 27.016,20 milioni di dollari entro il 2028; si prevede una crescita a un CAGR del 7,4% dal 2021 al 2028.

Un sistema di somministrazione di farmaci oculari (ODDS) è una forma di dosaggio, un veicolo o un sistema destinato a instillare, somministrare o rilasciare un farmaco/medicinale nell'occhio contro qualsiasi disturbo o patologia che coinvolga o influisca sulla vista. La gamma spazia da semplici colliri sterili per la superficie oculare a complessi impianti per il tessuto intraoculare. Le formulazioni di farmaci oculari sono principalmente in forma liquida, come soluzioni, sospensioni ed emulsioni per il trattamento delle patologie del segmento anteriore dell'occhio. Queste formulazioni possono essere disponibili sotto forma di sistemi avanzati di somministrazione di farmaci come gel in situ, microemulsione, nanoparticelle, liposomi, ionoforesi, nanosospensioni e inserti oculari.

Il mercato della somministrazione di farmaci oculari è stato segmentato in base a tecnologia, tipo di formulazione, tipo di patologia, utente finale e area geografica. Per area geografica, il mercato è principalmente suddiviso in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa e America meridionale e centrale. Il rapporto offre approfondimenti e analisi approfondite del mercato della somministrazione di farmaci oculari, evidenziando parametri quali tendenze di mercato, progressi tecnologici e dinamiche di mercato, insieme a un'analisi del panorama competitivo dei principali attori del mercato a livello globale.

Personalizza questo rapporto in base alle tue esigenze

Potrai personalizzare gratuitamente qualsiasi rapporto, comprese parti di questo rapporto, o analisi a livello di paese, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato della somministrazione di farmaci oculari: Approfondimenti strategici

-

Ottieni le principali tendenze chiave del mercato di questo rapporto.Questo campione GRATUITO includerà l'analisi dei dati, che vanno dalle tendenze di mercato alle stime e alle previsioni.

Approfondimenti di mercato: la crescente prevalenza di disturbi oculari favorirà la crescita del mercato dei farmaci oculari

Le principali cause di cecità o ipovisione in tutto il mondo sono la cataratta, il glaucoma, la degenerazione maculare legata all'età, la retinopatia diabetica e i difetti di rifrazione non corretti. La maggior parte della popolazione mondiale soffre o ha sofferto di qualche disturbo oculare nel corso della propria vita. Secondo il rapporto dell'Organizzazione Mondiale della Sanità (OMS) "Cecità e deficit visivo", pubblicato a febbraio 2021, circa 2,2 miliardi di persone in tutto il mondo soffrono di deficit visivo da vicino o da lontano. Si stima inoltre che la principale causa di perdita della vista o ipovisione sia la cataratta (94 milioni) e i difetti di rifrazione non corretti (88,4 milioni). Inoltre, le altre cause comuni di perdita della vista sono il glaucoma (7,7 milioni), le opacità corneali (4,2 milioni), la retinopatia diabetica (3,9 milioni) e il tracoma (2 milioni).

Secondo il National Eye Institute (NEI), negli Stati Uniti si prevede che il numero di persone affette da cataratta raddoppierà, passando da 24,4 milioni nel 2010 a circa 50 milioni nel 2050. Analogamente, secondo il Factsheet Glaucoma: Facts & Figures 2019, oltre 3 milioni di persone negli Stati Uniti convivevano con il glaucoma. Inoltre, secondo il Canadian Survey on Disabilities del 2017, 1,5 milioni di canadesi hanno subito una perdita della vista e circa 5,59 milioni hanno sofferto di una malattia oculare che potrebbe portare a un'ulteriore perdita della vista.

Inoltre, secondo il Royal National Institute of Blind People nel 2017, nel Regno Unito erano registrate circa 350.000 persone come cieche e ipovedenti; circa 173.735 erano registrate come ipovedenti gravi e 176.125 erano registrate come ipovedenti.

Approfondimenti basati sulla tecnologia

In base alla tecnologia, il mercato della somministrazione di farmaci oculari è segmentato in sistemi di somministrazione di farmaci oculari impiantabili, sistemi di somministrazione di farmaci tramite particelle, sistemi di somministrazione di farmaci tramite nanoparticelle e altri. Il segmento dei sistemi impiantabili per la somministrazione di farmaci oculari rappresenterebbe la quota di mercato maggiore nel 2021 e si prevede che lo stesso segmento registrerà il CAGR più elevato durante il periodo di previsione.

Approfondimenti basati sul tipo di formulazione

In base al tipo di formulazione, il mercato della somministrazione di farmaci oculari è segmentato in liposomi e nanoparticelle, soluzioni, emulsioni, sospensioni e unguenti. Il segmento delle soluzioni deterrebbe la quota di mercato maggiore nel 2021 e si stima che registrerà il CAGR più elevato nel periodo 2021-2028. La crescita del segmento delle soluzioni è attribuita alla crescente adozione di sistemi di somministrazione di farmaci oculari in forma di soluzione, come colliri e iniettabili.

Approfondimenti basati sul tipo di patologia

In base al tipo di patologia, il mercato della somministrazione di farmaci oculari è segmentato in glaucoma, retinopatia diabetica, sindrome dell'occhio secco, degenerazione maculare, cataratta, edema maculare diabetico e altre. Il segmento della cataratta rappresenterà la quota di mercato maggiore nel 2021. Si stima che il mercato per questo segmento crescerà al CAGR più elevato dal 2021 al 2028.

Approfondimenti basati sull'utente finale

In base all'utente finale, il mercato della somministrazione di farmaci oculari è segmentato in ospedali, cliniche oftalmiche e centri chirurgici ambulatoriali. Il segmento ospedaliero deterrà la quota di mercato maggiore nel 2021, mentre si stima che il segmento delle cliniche oftalmiche registrerà il CAGR più elevato del mercato durante il periodo di previsione.

La pandemia di COVID-19 è diventata la sfida più significativa a livello mondiale. Poiché questa pandemia ha messo a dura prova i sistemi sanitari di tutto il mondo, dare priorità alle risorse limitate è stato essenziale per ridurre al minimo i ricoveri ospedalieri. Tuttavia, nonostante l'aumento della domanda di terapie oculari come colliri, unguenti e sospensioni, si è verificata una carenza di questi prodotti con l'ingresso di nuovi consumatori nel mercato. I produttori stanno inoltre riscontrando un aumento dei prezzi e potenziali carenze di materie prime a causa delle restrizioni all'approvvigionamento. Tuttavia, con la revoca delle restrizioni e la ripresa delle attività, le variabili domanda-offerta stanno tornando alla normalità. Ciò offrirà diverse prospettive di crescita per le terapie per la somministrazione di farmaci oculari.

Acquisizioni, collaborazioni, partnership, lanci di prodotti ed espansioni sono strategie comunemente adottate dalle aziende per espandere la propria presenza a livello mondiale e soddisfare la crescente domanda. Gli operatori del mercato della somministrazione di farmaci oculari hanno adottato principalmente la strategia dell'innovazione di prodotto per soddisfare la mutevole domanda dei clienti in tutto il mondo, il che li aiuta anche a mantenere il loro marchio a livello globale.

Approfondimenti regionali sul mercato della somministrazione di farmaci oculari

Le tendenze regionali e i fattori che influenzano il mercato della somministrazione di farmaci oculari durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di The Insight Partners. Questa sezione illustra anche i segmenti e la geografia del mercato della somministrazione di farmaci oculari in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa, America meridionale e centrale.

Ambito del rapporto sul mercato della somministrazione di farmaci oculari

| Attributo del rapporto | Dettagli |

|---|---|

| Dimensioni del mercato in 2021 | US$ 16.4 Billion |

| Dimensioni del mercato per 2028 | US$ 27.02 Billion |

| CAGR globale (2021 - 2028) | 7.4% |

| Dati storici | 2019-2020 |

| Periodo di previsione | 2022-2028 |

| Segmenti coperti |

By Tecnologia

|

| Regioni e paesi coperti |

Nord America

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato della somministrazione di farmaci oculari: comprendere il suo impatto sulle dinamiche aziendali

Il mercato della somministrazione di farmaci oculari è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

- Ottieni il Mercato della somministrazione di farmaci oculari Panoramica dei principali attori chiave

- AbbVie Inc.

- Bausch Health Companies Inc.

- Taiwan Liposome Company, Ltd.

- Ocular Therapeutix, Inc.

- GRAYBUG VISION, INC.

- Alimera Sciences, Inc.

- Envisia Therapeutics

- Novartis AG

- EYEGATE PHARMACEUTICALS, INC

- Clearside Biomedical, Inc.

Mrinal è un'analista di ricerca esperta con oltre 8 anni di esperienza nella consulenza e nell'intelligence di mercato nel settore delle scienze biologiche. Grazie a una mentalità strategica e a un costante impegno verso l'eccellenza, ha maturato una profonda competenza nelle previsioni farmaceutiche, nella valutazione delle opportunità di mercato e nello sviluppo di benchmark di settore. Il suo lavoro è incentrato sulla fornitura di insight fruibili che consentono ai clienti di prendere decisioni strategiche consapevoli.

Il punto di forza di Mrinal risiede nella capacità di tradurre complessi set di dati quantitativi in business intelligence significative. Il suo acume analitico è fondamentale per definire strategie di go-to-market (GTM) e individuare opportunità di crescita nei settori farmaceutico e dei dispositivi medici. In qualità di consulente di fiducia, si concentra costantemente sulla semplificazione dei processi di flusso di lavoro e sulla definizione di best practice, promuovendo così l'innovazione e l'efficienza operativa per i suoi clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative