Análisis y pronósticos del mercado de administración de medicamentos oculares por tamaño, participación, crecimiento y tendencias para 2028

Análisis y pronósticos del mercado de administración de medicamentos oculares por tamaño, participación, crecimiento y tendencias para 2028

- Estado : Publicada

- Código de informe : TIPRE00004206

- Categoría : Ciencias de la vida

- Número de páginas : 171

- Formatos de informe disponibles :

- Fecha de última actualización : June 13, 2024

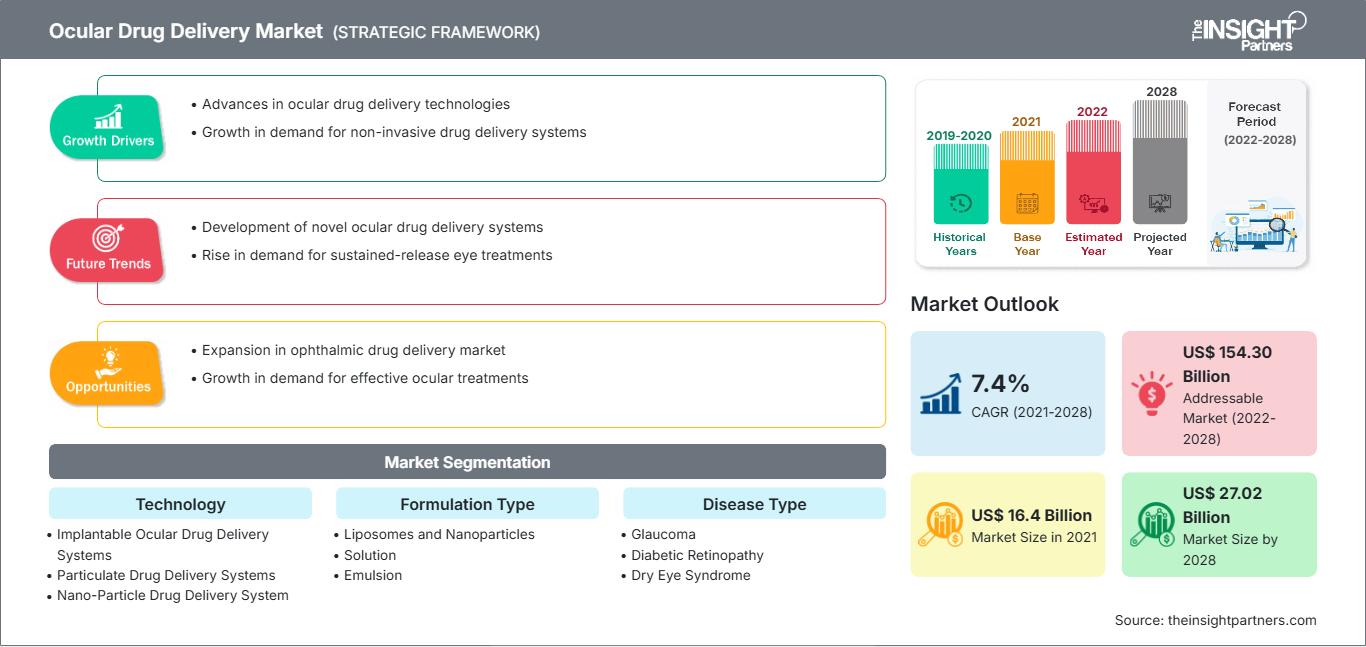

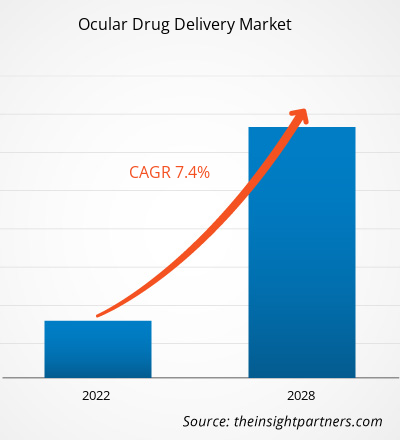

El mercado de administración de fármacos oculares se valoró en 16.404,32 millones de dólares estadounidenses en 2021 y se prevé que alcance los 27.016,20 millones de dólares estadounidenses en 2028; se espera que crezca a una tasa de crecimiento anual compuesta (TCAC) del 7,4 % entre 2021 y 2028.

Un sistema de administración de fármacos oculares (ODDS, por sus siglas en inglés) es una forma farmacéutica, vehículo o sistema diseñado para instilar, administrar o liberar un fármaco o medicamento en el ojo para tratar cualquier afección o trastorno que afecte la visión. Su alcance abarca desde simples gotas oftálmicas estériles para la superficie ocular hasta implantes complejos para el tejido intraocular. Las formulaciones de fármacos oculares se presentan principalmente en forma líquida, como soluciones, suspensiones y emulsiones, para el tratamiento de enfermedades del segmento anterior del ojo. Estas formulaciones pueden estar disponibles en forma de sistemas avanzados de administración de fármacos, como geles in situ, microemulsiones, nanopartículas, liposomas, iontoforesis, nanosuspensiones e insertos oculares.

El mercado de administración de fármacos oftálmicos se ha segmentado según la tecnología, el tipo de formulación, el tipo de enfermedad, el usuario final y la geografía. Geográficamente, el mercado se divide principalmente en Norteamérica, Europa, Asia Pacífico, Oriente Medio y África, y Sudamérica y Centroamérica. El informe ofrece información y un análisis exhaustivo del mercado de administración de fármacos oftálmicos, haciendo hincapié en parámetros como las tendencias del mercado, los avances tecnológicos y la dinámica del mercado, además de un análisis del panorama competitivo de los principales actores del mercado a nivel mundial.

Obtendrá personalización en cualquier informe, sin cargo, incluidas partes de este informe o análisis a nivel de país, paquete de datos de Excel, así como también grandes ofertas y descuentos para empresas emergentes y universidades.

Mercado de administración de fármacos oculares: Perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, que abarcarán desde tendencias de mercado hasta estimaciones y pronósticos.

Perspectivas del mercado

El aumento de la prevalencia de trastornos oculares impulsará el crecimiento del mercado de administración de fármacos oftálmicos.

Las principales causas de ceguera o baja visión en todo el mundo son las cataratas, el glaucoma, la degeneración macular asociada a la edad, la retinopatía diabética y los errores de refracción no corregidos. La mayoría de la población mundial padece o ha padecido algún trastorno ocular a lo largo de su vida. Según el informe de la Organización Mundial de la Salud (OMS) «Ceguera y discapacidad visual», publicado en febrero de 2021, alrededor de 2200 millones de personas en todo el mundo tienen discapacidad visual, ya sea de cerca o de lejos. Se estima que las principales causas de pérdida de visión o baja visión son las cataratas (94 millones) y los errores de refracción no corregidos (88,4 millones). Otras causas comunes de pérdida de visión son el glaucoma (7,7 millones), las opacidades corneales (4,2 millones), la retinopatía diabética (3,9 millones) y el tracoma (2 millones).

Según el Instituto Nacional del Ojo (NEI), en Estados Unidos se prevé que el número de personas con cataratas se duplique, pasando de 24,4 millones en 2010 a unos 50 millones en 2050. Asimismo, según la hoja informativa «Glaucoma: Datos y cifras 2019», más de 3 millones de personas en Estados Unidos vivían con glaucoma. Además, según la Encuesta Canadiense sobre Discapacidades de 2017, 1,5 millones de canadienses presentaban pérdida de visión y alrededor de 5,59 millones padecían alguna enfermedad ocular que podría derivar en pérdida de visión.

Además, según el Royal National Institute of Blind People en 2017, en el Reino Unido había alrededor de 350.000 personas registradas como ciegas y parcialmente visuales; alrededor de 173.735 estaban registradas como personas con discapacidad visual grave; y 176.125 estaban registradas como personas con discapacidad visual.

Perspectivas basadas en la tecnología

Según la tecnología empleada, el mercado de administración de fármacos oculares se segmenta en sistemas implantables, sistemas de administración de fármacos particulados, sistemas de administración de fármacos basados en nanopartículas y otros. Se prevé que el segmento de sistemas implantables represente la mayor cuota de mercado en 2021 y registre la mayor tasa de crecimiento anual compuesto (TCAC) durante el período de pronóstico.

Información basada en el tipo de formulación

Según el tipo de formulación, el mercado de administración de fármacos oftálmicos se segmenta en liposomas y nanopartículas, soluciones, emulsiones, suspensiones y ungüentos. Se prevé que el segmento de soluciones ostente la mayor cuota de mercado en 2021 y registre la mayor tasa de crecimiento anual compuesto (TCAC) entre 2021 y 2028. El crecimiento de este segmento se atribuye a la creciente adopción de sistemas de administración de fármacos oftálmicos en forma de soluciones, como colirios e inyectables.

Perspectivas basadas en el tipo de enfermedad

Según el tipo de enfermedad, el mercado de administración de fármacos oculares se segmenta en glaucoma, retinopatía diabética, síndrome del ojo seco, degeneración macular, cataratas, edema macular diabético y otras. Se prevé que el segmento de cataratas represente la mayor cuota de mercado en 2021. Se estima que este segmento experimentará el mayor crecimiento anual compuesto (CAGR) entre 2021 y 2028.

Información basada en el usuario final

Según el usuario final, el mercado de administración de fármacos oftalmológicos se segmenta en hospitales, clínicas oftalmológicas y centros quirúrgicos ambulatorios. Se prevé que el segmento de hospitales ostente la mayor cuota de mercado en 2021, mientras que se estima que el segmento de clínicas oftalmológicas registre la mayor tasa de crecimiento anual compuesto (TCAC) durante el período de pronóstico.

La pandemia de COVID-19 se ha convertido en el desafío más importante a nivel mundial. Dado que esta pandemia ha ejercido una gran presión sobre los sistemas de salud de todo el mundo, priorizar los recursos limitados fue esencial para minimizar los ingresos hospitalarios. Sin embargo, a pesar del aumento de la demanda de tratamientos oftálmicos como gotas, ungüentos y suspensiones, se produjo una escasez de estos productos debido a la entrada de nuevos consumidores al mercado. Los fabricantes también están experimentando un aumento de precios y una posible escasez de materias primas debido a las restricciones de suministro. No obstante, a medida que se han levantado las restricciones y las empresas reanudan sus actividades, la oferta y la demanda se están normalizando. Esto ofrecerá diversas perspectivas de crecimiento para los tratamientos oftálmicos de administración de fármacos.

Las adquisiciones, colaboraciones, alianzas, lanzamientos de productos y expansiones son estrategias comunes que adoptan las empresas para ampliar su presencia mundial y satisfacer la creciente demanda. Los actores del mercado de administración de fármacos oftálmicos han adoptado principalmente la estrategia de innovación de productos para atender la cambiante demanda de los clientes en todo el mundo, lo que también les ayuda a mantener su prestigio de marca a nivel global.

Perspectivas regionales del mercado de administración de fármacos oculares

Los analistas de The Insight Partners han explicado en detalle las tendencias regionales y los factores que influyen en el mercado de administración de fármacos oftálmicos durante el período de previsión. Esta sección también analiza los segmentos y la geografía del mercado de administración de fármacos oftálmicos en Norteamérica, Europa, Asia Pacífico, Oriente Medio y África, y Sudamérica y Centroamérica.

Alcance del informe de mercado sobre administración de fármacos oculares

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2021 | 16.400 millones de dólares |

| Tamaño del mercado para 2028 | US$ 27.020 millones |

| Tasa de crecimiento anual compuesto global (2021 - 2028) | 7,4% |

| Datos históricos | 2019-2020 |

| Período de pronóstico | 2022-2028 |

| Segmentos cubiertos |

Por tecnología

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de los actores del mercado de administración de fármacos oculares: comprensión de su impacto en la dinámica empresarial

El mercado de administración de fármacos oculares está creciendo rápidamente, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor conciencia de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

- Obtenga una visión general de los principales actores del mercado de administración de fármacos oculares.

Perfiles de empresas

- AbbVie Inc.

- Bausch Health Companies Inc.

- Compañía de Liposomas de Taiwán, Ltd.

- Terapeuta Ocular, Inc.

- GRAYBUG VISION, INC.

- Alimera Sciences, Inc.

- Terapéutica Envisia

- Novartis AG

- EYEGATE PHARMACEUTICALS, INC

- Clearside Biomedical, Inc.

Mrinal es una experimentada analista de investigación con más de 8 años de experiencia en inteligencia de mercado y consultoría en ciencias de la vida. Con una mentalidad estratégica y un firme compromiso con la excelencia, ha desarrollado una amplia experiencia en pronósticos farmacéuticos, evaluación de oportunidades de mercado y desarrollo de indicadores de referencia para la industria. Su trabajo se centra en brindar información práctica que permita a los clientes tomar decisiones estratégicas informadas.

La principal fortaleza de Mrinal reside en convertir conjuntos de datos cuantitativos complejos en inteligencia de negocios significativa. Su perspicacia analítica es fundamental para definir estrategias de salida al mercado (GTM) y descubrir oportunidades de crecimiento en los sectores farmacéutico y de dispositivos médicos. Como consultora de confianza, se centra constantemente en optimizar los procesos de flujo de trabajo y establecer las mejores prácticas, impulsando así la innovación y la eficiencia operativa para sus clientes.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias