Marktstrategien für Umverteilungsschichtmaterialien, Top-Player, Wachstumschancen, Analyse und Prognose bis 2030

Marktgröße und Prognosen für Umverteilungsschichtmaterialien (2020 – 2030), globaler und regionaler Anteil, Trends und Berichtsabdeckung zur Analyse von Wachstumschancen: Nach Typ [Polyimid (PI), Polybenzoxazol (PBO), Benzocyclobuten (BCB) und andere] und Anwendung {Fan-Out Wafer Level Packaging (FOWLP) und 2,5D/3D IC Packaging [High Bandwidth Memory (HBM), Multi-Chip Integration, Package on Package (FOPOP) und andere]}

- Status : Veröffentlicht

- Berichtscode : TIPRE00002904

- Kategorie : Chemikalien und Materialien

- Anzahl der Seiten : 161

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 13, 2024

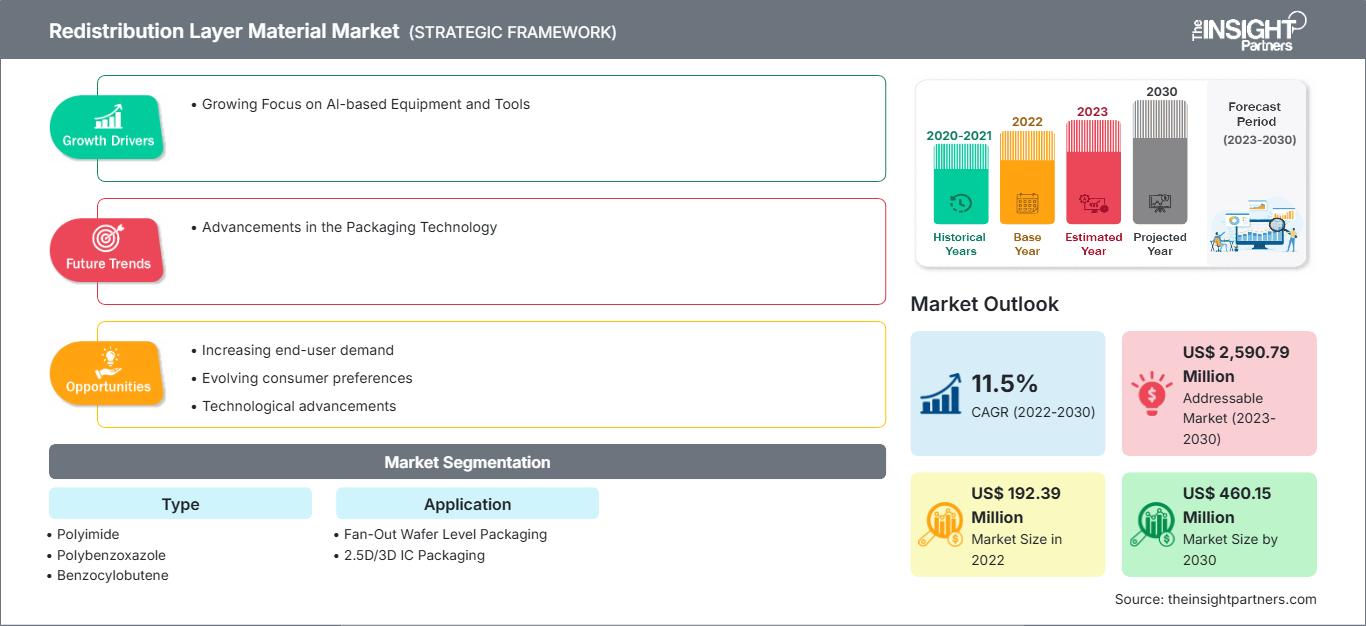

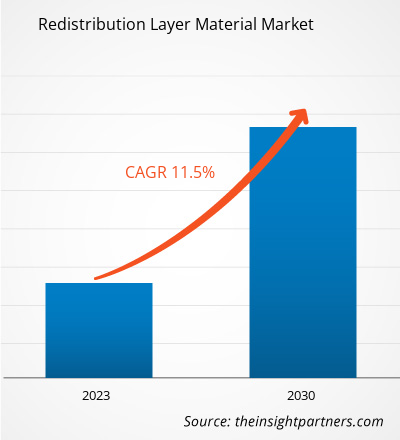

[Forschungsbericht] Der Markt für Umverteilungsschichtmaterialien soll von 192,39 Millionen US-Dollar im Jahr 2022 auf 460,15 Millionen US-Dollar im Jahr 2030 wachsen; von 2022 bis 2030 wird eine durchschnittliche jährliche Wachstumsrate (CAGR) von 11,5 % erwartet.

Markteinblicke und Analystenmeinung:

Der fortschrittliche Verpackungsprozess beginnt auf Chipebene, wobei das Ziel stets darin besteht, die Chipgröße zu verringern, ohne die Eingabe-/Ausgabedichte (I/O) zu beeinträchtigen. Mehrere andere aufstrebende Verpackungstechnologien spielen eine Schlüsselrolle bei der heterogenen Integration von Geräten. Wafer-Level Fan-Out Packaging (WLFO) ist eine der wichtigsten Verpackungstechnologien, die sich als umfassender Verpackungsprozess etabliert hat. Der WLFO-Prozess hatte früher nur Einzelchip-Designs, d. h. eine einzelne Umverteilungsschicht (RDL) auf einer Seite eines rekonstituierten Wafers. RDL ist ein entscheidender Schritt beim fortschrittlichen Wafer-Packaging. RDL dient der Umleitung des I/O-Layouts und ermöglicht eine höhere I/O-Anzahl. Eine hohe I/O-Dichte führt in der Regel zu einer besseren elektrischen Leistung, da mehr Ausgänge zu schnelleren elektrischen Signalen zwischen den Chips führen und das Risiko von Kurzschlüssen minimieren. Außerdem ermöglicht eine höhere I/O-Dichte dem Paket gleichzeitig eine bessere Leistung. Darüber hinaus hat Asiens strategische Lage als globales Fertigungszentrum, gepaart mit wettbewerbsfähigen Produktionskosten, multinationale Konzerne angezogen, die ihre Lieferketten optimieren möchten. Dadurch ist ein robustes Ökosystem für den Markt für Redistribution-Layer-Materialien entstanden, in dem sich verschiedene Lieferanten und Hersteller in der Region niedergelassen haben. Dieser Faktor treibt das Wachstum des globalen Marktes für Redistribution-Layer-Materialien maßgeblich voran.

Wachstumstreiber und Herausforderungen:

Redistribution-Layer-Materialien (RDL) sind von grundlegender Bedeutung für die Miniaturisierung von Halbleiterpaketen, die für die zunehmende Komplexität von KI-Geräten unerlässlich ist. Das Streben nach fortschrittlicheren KI-Fähigkeiten erfordert die Entwicklung kompakter und dicht integrierter Hardwarekomponenten. Mit immer ausgefeilteren KI-Systemen steigt die Nachfrage nach kleineren und effizienteren Komponenten. Die steigende Nachfrage nach KI-basierten Geräten und Werkzeugen treibt somit den Markt für Redistribution-Layer-Materialien an. Darüber hinaus erlebt der globale Markt für Redistribution-Layer-Materialien ein starkes Wachstum, das vor allem durch die steigende Nachfrage aus zwei Schlüsselindustrien getrieben wird: der Automobilindustrie und der Telekommunikation. Der stetig steigende Produktionsbedarf der Automobilindustrie treibt das Wachstum des Marktes voran. Laut dem ISEAS-Yusof Ishak Institute ist Südostasien ein wichtiger Standort für die Automobilproduktion. Südostasien ist der siebtgrößte Automobilproduktionsstandort weltweit und produzierte 2021 3,5 Millionen Fahrzeuge. Schwankende Rohstoffpreise stellen jedoch eine erhebliche Herausforderung für das Wachstum des globalen Marktes für Redistribution-Layer-Materialien dar. Diese Preisänderungen können erhebliche Auswirkungen auf die Branche haben und sich auf Produktionskosten, Preisstrategien und die allgemeine Marktstabilität auswirken. Eines der Hauptprobleme ist die Abhängigkeit von importierten Rohstoffen. Viele wesentliche Komponenten für Umverteilungsschichtmaterialien, wie beispielsweise spezielle Polymere, Metalle und Chemikalien, werden häufig von internationalen Lieferanten bezogen.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für Umverteilungsschichtmaterialien: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

Berichtssegmentierung und -umfang:

Der globale Markt für Umverteilungsschichtmaterialien ist nach Typ und Anwendung unterteilt. Nach Typ ist der Markt für Umverteilungsschichtmaterialien in Polyimid (PI), Polybenzoxazol (PBO), Benzocyclobuten (BCB) und andere segmentiert. Nach Anwendung ist der Markt für Umverteilungsschichtmaterialien in Fan-Out-Wafer-Level-Packaging (FOWLP) und 2,5D/3D-IC-Packaging unterteilt. Geografisch ist der Markt in Nordamerika (USA, Kanada und Mexiko), Europa (Deutschland, Frankreich, Italien, Großbritannien, Russland und übriges Europa), Asien-Pazifik (Australien, China, Japan, Indien, Südkorea und übriger Asien-Pazifik-Raum), Naher Osten und Afrika (VAE, Saudi-Arabien, Südafrika und übriger Naher Osten und Afrika) sowie Süd- und Südamerika unterteilt. Mittelamerika (Brasilien, Argentinien und übriges Süd- und Mittelamerika).

Segmentanalyse:

Basierend auf dem Typ ist der Markt für Umverdrahtungsschichtmaterialien in Polyimid (PI), Polybenzoxazol (PBO), Benzocyclobuten (BCB) und andere unterteilt. Das Segment Polyimid (PI) hatte 2022 den größten Marktanteil. Polyimide sind polymerbasierte Thermoplaste mit hoher Schmelzviskosität und erfordern höhere Drücke zur Herstellung von Formteilen. Polyimide bieten eine gute chemische Beständigkeit, hohe mechanische Festigkeit, höhere thermische Stabilität und außergewöhnliche elektrische Eigenschaften. Für die IC-Verpackungsmethoden werden Polyimide als Hochtemperaturklebstoffe, mechanische Spannungspuffer und als Folie zur Unterstützung der Mikroschaltkreise verwendet. Der einzige Nachteil der verwendeten Polyimide waren die höheren Aushärtungstemperaturen, während die Verpackung niedrigere Aushärtungstemperaturen erfordert. Mehrere Materiallieferanten haben sich daher darauf konzentriert, Polyimide mit niedrigeren Aushärtungstemperaturen anzubieten. PI wird hauptsächlich in allen Flip-Chip-Wafer-Bumping- und WLP-Anwendungen verwendet. Je nach Anwendung ist der Markt für Redistribution-Layer-Materialien in Fan-Out-Wafer-Level-Packaging (FOWLP) und 2,5D/3D-IC-Packaging [High Bandwidth Memory (HBM), Multi-Chip-Integration, Package-on-Package (FOPOP) und andere] unterteilt. Der Marktanteil von Redistribution-Layer-Materialien im Segment 2,5D/3D-IC-Packaging war im Jahr 2022 bemerkenswert. Die gestiegenen Kosten für Lithografieschritte und Waferverarbeitung im Allgemeinen an den Siliziumknoten der nächsten Generation zwingen die Branche, Alternativen zur Verbesserung der Leistung und Funktionalität elektronischer Geräte zu finden. Darüber hinaus treibt die Notwendigkeit, unterschiedliche Technologien wie Logik, Speicher, HF und Sensoren in kleinen Formfaktoren zu integrieren, die Branche in Richtung 3D-Integration als Lösung.

Regionale Analyse:

Der Markt für Redistribution-Layer-Materialien ist in fünf Schlüsselregionen segmentiert: Nordamerika, Europa, Asien-Pazifik, Süd- und Mittelamerika sowie der Nahe Osten und Afrika. Der asiatisch-pazifische Raum dominierte den globalen Markt für Umverteilungsschichtmaterialien, der im Jahr 2022 etwa 150 Millionen US-Dollar ausmachte. Nordamerika leistet ebenfalls einen wichtigen Beitrag und hält einen bedeutenden globalen Marktanteil an Umverteilungsschichtmaterialien. Der nordamerikanische Markt für Umverteilungsschichtmaterialien wird bis 2030 voraussichtlich über 60 Millionen US-Dollar erreichen. Europa wird voraussichtlich von 2022 bis 2030 eine beträchtliche CAGR von über 10 % verzeichnen. Der Markt für Umverteilungsschichtmaterialien im asiatisch-pazifischen Raum ist nach Ländern segmentiert in Australien, China, Indien, Japan, Südkorea und den Rest des asiatisch-pazifischen Raums. Der Markt wird durch die wachsende Nachfrage nach Umverteilungsschichtmaterialien seitens der Automobil- und Telekommunikationsindustrie angetrieben. Taiwan dominiert den regionalen Markt, gefolgt von Ländern wie China, Südkorea, Japan und Vietnam. Die Region gilt aufgrund der Präsenz vielfältiger Fertigungsindustrien als globales Produktionszentrum. Mit Chinas Entwicklung zu einem Zentrum für hochqualifizierte Produktion ziehen Entwicklungsländer wie Indien, Südkorea, Taiwan und Vietnam zahlreiche Unternehmen an, die ihre Produktionsstätten für gering- bis mittelqualifizierte Mitarbeiter in Nachbarländer verlagern wollen, was zu geringeren Arbeitskosten führt.

Branchenentwicklungen und zukünftige Chancen:

Nachfolgend sind verschiedene Initiativen wichtiger Akteure auf dem Markt für Umverteilungsschichtmaterialien aufgeführt:

- Im August 2022 veranstaltete ASE Technology eine Zeremonie zum Bau einer neuen Anlage für Halbleitermontage und -prüfung in Penang, Malaysia. Die neue Anlage bei ASE Malaysia (ASEM) wird aus zwei Gebäuden (Werke 4 und 5) mit einer bebauten Fläche von 982.000 Quadratfuß bestehen und sich in der freien Industriezone Bayan Lepas befinden.

- Im Juli 2021 eröffnete DuPont Mobility & Materials gab seinen Plan bekannt, 5 Millionen US-Dollar in Kapital und Betriebsmittel an seinen Produktionsstandorten in Deutschland und der Schweiz zu investieren, um die Kapazität für seine Hochleistungsklebstoffe für die Automobilindustrie zu erhöhen.

Auswirkungen der COVID-19-Pandemie:

Die COVID-19-Pandemie hatte negative Auswirkungen auf fast alle Branchen in verschiedenen Ländern. Lockdowns, Geschäftsschließungen und Reisebeschränkungen in Nordamerika, Europa, im asiatisch-pazifischen Raum (APAC), in Süd- und Mittelamerika (SAM) sowie im Nahen Osten und Afrika (MEA) bremsten das Wachstum mehrerer Branchen, darunter der Chemie- und Werkstoffindustrie. Die Schließung von Produktionseinheiten störte die globalen Lieferketten, Fertigungsaktivitäten, Lieferpläne sowie den Verkauf lebenswichtiger und nicht lebenswichtiger Produkte. Verschiedene Unternehmen meldeten Verzögerungen bei Produktlieferungen und einen Einbruch ihrer Produktverkäufe im Jahr 2020. Aufgrund der pandemiebedingten Wirtschaftsrezession wurden die Verbraucher bei Kaufentscheidungen vorsichtiger und wählerischer. Die Verbraucher reduzierten nicht lebensnotwendige Einkäufe aufgrund niedrigerer Einkommen und unsicherer Verdienstaussichten erheblich, insbesondere in Entwicklungsregionen. Viele Hersteller von Umverteilungsschichtmaterialien meldeten aufgrund der geringeren Verbrauchernachfrage in der Anfangsphase der Pandemie sinkende Gewinne. Ende 2021 waren jedoch viele Länder vollständig geimpft, und die Regierungen kündigten Lockerungen bestimmter Vorschriften an, darunter Ausgangssperren und Reiseverbote. Das verfügbare Einkommen der Bevölkerung stieg, wodurch der Fokus verstärkt auf den Kauf neuer Möbel und Renovierungen gerichtet war, was wiederum die Nachfrage nach Umverteilungsschichtmaterialien ankurbelte. All diese Faktoren fördern das Wachstum des Marktes für Umverteilungsschichtmaterialien in verschiedenen Regionen.

Umverteilungsschichtmaterial

Regionale Einblicke in den Markt für UmverteilungsschichtmaterialienDie Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Markt für Umverteilungsschichtmaterialien im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Lage in Nordamerika, Europa, dem asiatisch-pazifischen Raum, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika erörtert.

Umfang des Marktberichts zu Umverteilungsschichtmaterialien

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2022 | US$ 192.39 Million |

| Marktgröße nach 2030 | US$ 460.15 Million |

| Globale CAGR (2022 - 2030) | 11.5% |

| Historische Daten | 2020-2021 |

| Prognosezeitraum | 2023-2030 |

| Abgedeckte Segmente |

By Typ

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Marktteilnehmer für Umverteilungsschichtmaterialien: Verständnis ihrer Auswirkungen auf die Geschäftsdynamik

Der Markt für Redistribution Layer-Materialien wächst rasant. Dies wird durch die steigende Endverbrauchernachfrage aufgrund veränderter Verbraucherpräferenzen, technologischer Fortschritte und eines stärkeren Bewusstseins für die Produktvorteile vorangetrieben. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Markt für Umverteilungsschichtmaterialien Übersicht der wichtigsten Akteure

Wettbewerbslandschaft und Schlüsselunternehmen:

SK Hynix Inc, Samsung Electronics Co Ltd, Infineon Technologies AG, Dupont De Nemours Inc, Fujifilm Holdings Corp, Amkor Technology Inc, ASE Technology Holding Co Ltd., NXP Semiconductors NV, JCET Group Co Ltd und Shin-Etsu Chemical Co Ltd gehören zu den führenden Akteuren auf dem globalen Markt für Umverdrahtungsschichtmaterialien. Diese Unternehmen bieten hochwertiges Umverdrahtungsschichtmaterial an und beliefern zahlreiche Verbraucher weltweit.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends