Tendencias, demanda y crecimiento del mercado de la salud animal hasta 2034

Tamaño y pronósticos del mercado de salud animal (2021-2034), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por producto (con receta y sin receta), tipo de animal (animal de producción y animal de compañía) y geografía (América del Norte, Europa, Asia Pacífico y América del Sur y Central).

- Estado : Datos publicados

- Código de informe : TIPRE00003540

- Categoría : Ciencias de la vida

- Número de páginas : 194

- Formatos de informe disponibles :

- Fecha de última actualización : August 04, 2026

Tamaño del mercado en 2025

76.020 millones de dólares estadounidenses

Valor del año base

Pronóstico para 2034

160.900 millones de dólares estadounidenses

Proyecciones para 2034

Tasa de crecimiento anual compuesta (CAGR) 2026-2034

8,69 %

Índice de crecimiento

Mercado potencial

US$ 1.062,00 mil millones

(2026-2034)

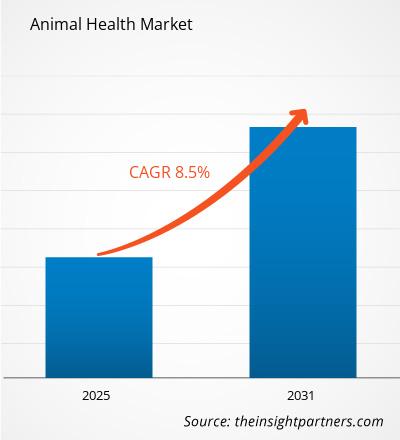

El mercado de la salud animal abarca productos y soluciones que apoyan la prevención, el diagnóstico, el tratamiento y el bienestar general de animales de granja y de compañía. Este mercado, valorado en 76.020 millones de dólares estadounidenses en 2025, se prevé que alcance los 160.900 millones de dólares estadounidenses en 2034, con una tasa de crecimiento anual compuesta (TCAC) del 8,69 % entre 2026 y 2034. La creciente adopción de servicios veterinarios, la expansión de los sistemas de producción animal y la creciente demanda de soluciones de atención preventiva están impulsando el desarrollo del mercado a nivel mundial.

América del Norte representa un ecosistema maduro con una expansión continua, respaldada por una infraestructura veterinaria avanzada, la tenencia de animales de compañía y el creciente gasto en bienestar animal. Se estima que la región crecerá a una tasa de crecimiento anual compuesta (TCAC) de entre el 7,50 % y el 8,20 % entre 2026 y 2034, impulsada por plataformas veterinarias digitales, una mejor adopción de diagnósticos y el aumento de las inversiones en servicios de salud preventiva. El tamaño del mercado de salud animal en esta región está influenciado por compañías farmacéuticas consolidadas, prácticas avanzadas de manejo ganadero y el énfasis regulatorio en el control de enfermedades animales.

Evaluación y perspectivas del mercado de la salud animal

- América del Norte: La región mantiene una posición significativa con una participación estimada del 34-38% para 2025 y se espera que crezca a una tasa de crecimiento anual compuesta (TCAC) del 7,50-8,20% entre 2026 y 2034. Las sólidas redes veterinarias, el gasto en animales de compañía y los programas de salud animal respaldan una demanda sostenida.

- EE. UU. representa aproximadamente entre el 75 % y el 80 % de la cuota de mercado de Norteamérica en 2025 y se prevé que crezca a una tasa de crecimiento anual compuesta (TCAC) del 7,60 % al 8,30 % entre 2026 y 2034. Los productos farmacéuticos veterinarios avanzados, los diagnósticos y la adopción de servicios veterinarios siguen siendo factores clave.

- Europa representa una cuota estimada del 27-31% en 2025 y se prevé que registre una tasa de crecimiento anual compuesta (TCAC) del 7,20-7,90% entre 2026 y 2034. Alemania, el Reino Unido, Francia, Italia y España contribuyen a través de la producción ganadera, los marcos regulatorios y la innovación veterinaria.

- La región Asia-Pacífico representa aproximadamente entre el 22 % y el 26 % de la cuota de mercado en 2025 y se prevé que registre una tasa de crecimiento anual compuesta (CAGR) del 9,10 % al 9,80 % entre 2026 y 2034. China, India, Japón, Corea del Sur y Australia impulsan este crecimiento mediante la expansión de la producción animal y la modernización de la atención sanitaria.

- El segmento más grande, el de animales de producción, representa una cuota de mercado estimada del 55-60% en 2025 y se prevé que crezca a una tasa de crecimiento anual compuesta (CAGR) del 8,20-8,80% entre 2026 y 2034 debido a las necesidades de gestión de enfermedades del ganado.

- El segmento de animales de compañía, de alto crecimiento, representará entre el 40 % y el 45 % de la cuota de mercado en 2025 y se espera que alcance una tasa de crecimiento anual compuesta (CAGR) del 9,10 % al 9,70 % entre 2026 y 2034 debido al aumento del gasto en atención médica para mascotas.

- Empresas clave analizadas en detalle: Merck & Co., Inc., Boehringer Ingelheim International GmbH, Ceva Sante Animale, Cargill Incorporated, Zoetis Inc., Bayer AG, Vetoquinol SA, Nutreco NV, Virbac, Elanco.

Fuente: Análisis de The Insight Partners basado en investigaciones propias, publicaciones gubernamentales, informes anuales de empresas, presentaciones para inversores, bases de datos del sector y entrevistas con expertos.

El crecimiento del mercado se ha visto impulsado por los avances en medicamentos veterinarios, productos biotecnológicos y herramientas de monitorización de precisión. Los fabricantes incorporan cada vez más diagnósticos, tecnología y análisis de datos en los sistemas de atención sanitaria animal. Los procesos de producción se han orientado hacia un enfoque preventivo, dado que los ganaderos se preocupan por la productividad, la seguridad alimentaria y la resistencia a las enfermedades. Las empresas farmacéuticas se están diversificando hacia vacunas, terapias, productos nutricionales y medicamentos con receta para satisfacer las nuevas demandas veterinarias.

El desarrollo del mercado en el futuro estará impulsado por inversiones en países en desarrollo, una mejor regulación y un mayor uso de prácticas veterinarias preventivas. Los gobiernos y las organizaciones han comenzado a invertir en la vigilancia de enfermedades animales e iniciativas de bioseguridad para proteger las cadenas de suministro de alimentos. Un mayor énfasis en la producción ganadera sostenible y el acceso a la atención sanitaria para animales de compañía generará nuevas oportunidades.

Alcance del informe de mercado de salud animal

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2025 | 76.020 millones de dólares estadounidenses |

| Tamaño del mercado para 2034 | 160.900 millones de dólares estadounidenses |

| Tasa de crecimiento anual compuesta global (2026 - 2034) | 8,69% |

| Datos históricos | 2021-2024 |

| Período de pronóstico | 2026-2034 |

Análisis del mercado de la salud animal

La demanda de soluciones para el mercado de la salud animal está aumentando debido al incremento de la producción ganadera, la creciente tenencia de mascotas y la necesidad de reducir las pérdidas económicas causadas por enfermedades animales. El crecimiento de este mercado se sustenta en cadenas de valor integradas que involucran a fabricantes farmacéuticos, clínicas veterinarias, distribuidores, granjas y proveedores de cuidado de mascotas. Los enfoques de salud preventiva, incluyendo vacunas e intervenciones nutricionales, están cobrando mayor importancia a medida que los productores buscan mejorar la productividad y reducir los riesgos de enfermedades.

La dinámica de la oferta está evolucionando gracias a la ampliación de la capacidad de fabricación, las redes de distribución regionales y las inversiones en investigación y desarrollo. Las empresas se centran en formulaciones innovadoras, métodos de administración mejorados y terapias combinadas. Las normativas relativas a los animales destinados a la producción de alimentos influyen en el desarrollo de productos, mientras que la demanda de atención médica para animales de compañía sigue impulsando la diversificación de servicios y productos.

El informe del mercado de salud animal destaca la creciente competitividad a medida que las empresas de todo el mundo invierten en innovaciones, expansiones y colaboraciones. Merck & Co., Inc. mantiene su enfoque en productos farmacéuticos veterinarios y soluciones biológicas, mientras que Boehringer Ingelheim International GmbH diversifica su cartera de soluciones de salud animal mediante métodos basados en la investigación. Zoetis Inc. cuenta con una sólida presencia en diversos tipos de animales con una amplia gama de soluciones para el cuidado de la salud.

Las iniciativas estratégicas incluyen innovaciones en tecnología veterinaria digital, diagnósticos avanzados y productos terapéuticos. Ceva Santé Animale, Bayer AG, Elanco, Virbac, Vetoquinol SA, Cargill Incorporated y Nutreco NV son algunas de las empresas que adoptan soluciones específicas para la nutrición animal, la prevención de enfermedades y la gestión sanitaria. Los competidores utilizan el desarrollo de productos y la expansión regional como su principal estrategia competitiva.

● PERSONALIZACIÓN DE INFORMES

Adapte este informe para que se ajuste a sus necesidades comerciales específicas.

Este informe se puede personalizar para que se ajuste con precisión a sus objetivos comerciales, alcance y mercados objetivo. Las opciones de personalización incluyen segmentación a medida, análisis geográfico, análisis de la competencia e información estratégica para facilitar la toma de decisiones informadas.

Personaliza este informe →LO QUE PUEDES AJUSTAR

- ● Segmentaciones

- ● Geografía

- ● Análisis de la competencia

- ● Preferencias de idioma

Mercado de la salud animal: Perspectivas estratégicas

Perspectivas regionales

Mercado de salud animal de Norteamérica

América del Norte mantiene una posición de liderazgo con una participación estimada del 34-38% en 2025 y se espera que crezca a una tasa de crecimiento anual compuesta (TCAC) del 7,50-8,20% entre 2026 y 2034. La región cuenta con infraestructura veterinaria consolidada, un alto gasto en atención médica para animales de compañía y sistemas modernos de producción ganadera. Estados Unidos representa la mayor demanda regional gracias a su uso de productos farmacéuticos y servicios veterinarios especializados.

Otros países que contribuyen al desarrollo regional son Canadá y México, gracias a la mejora de sus programas de gestión sanitaria y prevención de enfermedades en el ganado. Un marco regulatorio riguroso, la alta demanda de productos biológicos y la adopción de soluciones de monitorización digital veterinaria están generando nuevas oportunidades de mercado. La presencia de empresas multinacionales, junto con las actividades de investigación y diagnóstico, garantiza un gran potencial de crecimiento en el sector de la salud animal, tanto para animales de compañía como de producción.

Mercado de salud animal de EE. UU.

Estados Unidos representa aproximadamente entre el 75 % y el 80 % de la cuota de mercado de salud animal en Norteamérica para 2025 y se prevé que registre una tasa de crecimiento anual compuesta (TCAC) del 7,60 % al 8,30 % entre 2026 y 2034. El país cuenta con una amplia gama de servicios veterinarios, una gran cantidad de mascotas y técnicas sofisticadas de manejo ganadero. Cada vez más empresas farmacéuticas y otros proveedores de servicios están avanzando con nuevos productos en las áreas de medidas preventivas, diagnóstico y métodos de tratamiento.

Entre los principales actores del mercado se encuentran Zoetis Inc., Merck & Co., Inc. y Elanco, que cuentan con una amplia presencia gracias a su gama de productos para animales de compañía y ganado. Las tendencias de uso apuntan hacia sistemas de gestión sanitaria precisos, la digitalización de los servicios veterinarios y técnicas de tratamiento personalizadas.

Mercado europeo de salud animal

Europa representará entre el 27 % y el 31 % del mercado en 2025 y se prevé que crezca a una tasa de crecimiento anual compuesta (TCAC) del 7,20 % al 7,90 % entre 2026 y 2034. La región se beneficia de sistemas veterinarios consolidados, marcos regulatorios sólidos y una amplia capacidad de producción ganadera. Alemania constituye uno de los mercados líderes gracias a su avanzado sector agrícola, su infraestructura veterinaria y su enfoque en la producción animal sostenible.

El Reino Unido sigue impulsando el desarrollo del mercado mediante el aumento del gasto en atención sanitaria para animales de compañía y la adopción de servicios veterinarios avanzados. Francia, Italia y España contribuyen a través de la ganadería, los programas de prevención de enfermedades y la creciente adopción de productos farmacéuticos veterinarios. El crecimiento regional se ve influenciado por el énfasis normativo en el uso responsable de medicamentos, las normas de seguridad alimentaria y las innovaciones en la prestación de servicios de salud animal.

Mercado de salud animal en Asia-Pacífico

Se estima que la región Asia-Pacífico representará entre el 22 % y el 26 % del mercado en 2025, y se prevé que crezca a una tasa de crecimiento anual compuesta (TCAC) del 9,10 % al 9,80 % entre 2026 y 2034. China lidera la demanda regional gracias a sus elevados volúmenes de producción ganadera y a la creciente adopción de servicios veterinarios. India, Japón, Corea del Sur y Australia también contribuyen mediante la modernización de la ganadería y el desarrollo del cuidado de los animales de compañía.

La agricultura a escala industrial, el creciente consumo de proteínas y las iniciativas gubernamentales para el control de enfermedades animales están fortaleciendo las oportunidades regionales. Se espera que las inversiones en infraestructura veterinaria y un mejor acceso a productos sanitarios aceleren su adopción en las economías emergentes.

Mercado de salud animal de Oriente Medio y África

Se estima que la región de Oriente Medio y África crecerá a una tasa de crecimiento anual compuesta (TCAC) del 6,80 % al 7,50 % entre 2026 y 2034. Arabia Saudita y los Emiratos Árabes Unidos están mejorando sus sistemas de salud animal mediante inversiones en seguridad alimentaria y modernización agrícola. Sudáfrica sigue siendo un actor clave gracias a sus consolidadas actividades de producción animal y servicios veterinarios.

El crecimiento en el resto de la región de Oriente Medio y África se ve impulsado por el desarrollo de infraestructuras, el aumento de las iniciativas de productividad ganadera y los programas de control de enfermedades. Los ingresos del sector energético y la capacidad de inversión pública en varios países contribuyen indirectamente a la diversificación agrícola y a la mejora de la sanidad animal.

Análisis de segmentación

Producto

El segmento de productos se clasifica en soluciones con receta y sin receta. Se prevé que este segmento registre una tasa de crecimiento anual compuesta (TCAC) del 8,50 % al 9,10 % entre 2026 y 2034. La creciente demanda de prevención de enfermedades, terapias veterinarias y productos para la salud nutricional impulsa la expansión del mercado. El alcance del mercado dentro de las categorías de productos continúa ampliándose a medida que los fabricantes introducen formulaciones avanzadas, productos biológicos y soluciones preventivas. Las principales tendencias del mercado de salud animal incluyen la creciente adopción de animales de compañía, un mayor enfoque en la atención médica preventiva, el uso cada vez mayor de vacunas y productos biológicos, los avances en el manejo de enfermedades del ganado y la integración de tecnologías de salud digital para mejorar el monitoreo, el diagnóstico y los resultados del tratamiento en animales.

- Los medicamentos con receta siguen siendo importantes para el tratamiento de enfermedades y la atención veterinaria especializada, respaldados por diagnósticos profesionales, aprobaciones regulatorias y una creciente adopción entre los productores de ganado y los dueños de animales de compañía.

- Los productos sin receta experimentan una demanda constante gracias a sus aplicaciones de bienestar preventivo, suplementos nutricionales y soluciones sanitarias de fácil acceso utilizadas por agricultores y dueños de mascotas.

Tipo de animal

El segmento Tipo de Animal incluye las categorías de Animales de Producción y Animales de Compañía. Se prevé que este segmento crezca a una tasa de crecimiento anual compuesta (TCAC) del 8,70 % al 9,30 % entre 2026 y 2034. La expansión de la producción ganadera, el aumento de la tenencia de mascotas y la creciente concienciación sobre la atención sanitaria preventiva influyen en los patrones de adopción. Este segmento sigue siendo fundamental para el desarrollo del mercado, ya que los profesionales sanitarios atienden las diversas necesidades de los animales.

- Production Animal Solutions apoya la gestión de la salud del ganado mediante la prevención de enfermedades, la mejora de la productividad y el cumplimiento de los requisitos de seguridad alimentaria en bovinos, aves de corral, porcinos y otros sistemas agrícolas.

- Los servicios y productos para animales de compañía están cobrando mayor importancia debido al aumento de la tenencia de mascotas, el incremento de las visitas al veterinario y el creciente interés de los consumidores por el bienestar animal a largo plazo.

Resumen de la oportunidad

|

Tipo de animal |

Contribución de ingresos |

Etiqueta de tendencia |

Etapa de adopción |

|

Animal de producción |

Alto |

Bienestar del ganado |

Maduro |

|

Animal de compañía |

Alto |

Cuidado de la salud de las mascotas |

Escalada |

Factores de crecimiento del mercado de la salud animal y análisis de su impacto

Aumento de la demanda de atención veterinaria preventiva

El uso de la atención sanitaria preventiva se está consolidando como uno de los principales factores determinantes del gasto en el sector de la salud animal, ya que los ganaderos y los dueños de mascotas prefieren ahora prevenir las enfermedades en lugar de curarlas. Las herramientas preventivas, como las vacunas, las medidas nutricionales y de diagnóstico, pueden minimizar los costes de producción y mejorar el bienestar animal. Existe una creciente necesidad de soluciones estandarizadas para la salud animal en la cadena de valor alimentaria internacional, lo que fomenta la oferta de productos sanitarios más fiables. Tanto la industria veterinaria como los organismos reguladores promueven, además, mejores sistemas de vigilancia epidemiológica, lo que generará una mayor demanda de productos innovadores.

Expansión de los sistemas de producción ganadera

Ante el aumento de la demanda mundial de productos alimenticios de origen animal, los sistemas de producción animal se están modernizando. Se están implementando intervenciones sanitarias que contribuyen a aumentar la eficiencia en la ganadería y a mejorar la salud animal. Para que las grandes explotaciones puedan operar, es necesario combinar diversos métodos, como medicamentos, pruebas diagnósticas, control nutricional y atención veterinaria. Las economías emergentes invierten en el desarrollo de infraestructura agrícola para garantizar la seguridad alimentaria y la calidad del ganado. De esta forma, las organizaciones sanitarias tienen más oportunidades de ofrecer soluciones escalables en diferentes contextos.

Crecimiento del gasto en atención médica para animales de compañía

El creciente número de mascotas y la mayor concienciación sobre su salud están impulsando un mayor gasto en soluciones sanitarias para animales. Los dueños buscan tratamientos, servicios de diagnóstico, nutrición y atención veterinaria que contribuyan a prolongar la vida de sus mascotas y garantizarles una mejor calidad de vida. La creciente urbanización y el aumento de los ingresos disponibles hacen que el acceso a servicios sanitarios de alta gama sea más accesible. Las clínicas veterinarias están diversificando su oferta de servicios para atender diversas enfermedades y necesidades de prevención.

Tendencias futuras del mercado de la salud animal

Plataformas veterinarias digitales y atención animal basada en datos

Se prevé que el uso de tecnologías digitales transformará la toma de decisiones veterinarias mediante la monitorización remota, los dispositivos conectados y los sistemas de gestión sanitaria basados en datos. Las futuras aplicaciones dependerán cada vez más del diagnóstico, la inteligencia artificial y el análisis de datos para la detección precoz de problemas de salud y una mayor eficacia de los tratamientos aplicados. Los ganaderos podrían empezar a emplear tecnologías de sensores para monitorizar el comportamiento, la nutrición y el estado de salud de los animales. Los profesionales sanitarios de animales de compañía también implementarán tecnologías de consulta digital e historiales clínicos electrónicos. Estos avances tecnológicos propiciarán enfoques más personalizados en la atención sanitaria y una mayor eficiencia operativa.

Expansión de soluciones sostenibles para el cuidado de la salud animal.

Se prevé que los factores de responsabilidad ambiental influyan en los desarrollos futuros, ya que los productores buscan formas sostenibles de gestionar sus animales. Es probable que adopten estrategias que mejoren el rendimiento animal y, al mismo tiempo, contribuyan a reducir el uso de recursos y a fomentar prácticas de medicación responsables. Se espera que los productos nutricionales alternativos, las técnicas de prevención de enfermedades y los mejores sistemas de gestión de enfermedades sean importantes en la gestión ganadera. Se prevé que las iniciativas destinadas a lograr una agricultura sostenible y mejorar la seguridad alimentaria impulsen la innovación. La combinación de los objetivos de sostenibilidad y la ciencia veterinaria creará nuevas oportunidades para los profesionales de la salud.

Oportunidades de mercado en el sector de la salud animal

Inversión en infraestructura veterinaria para mercados emergentes

Las economías en desarrollo presentan importantes oportunidades a medida que los gobiernos y las organizaciones privadas mejoran la infraestructura veterinaria, los sistemas de vigilancia de enfermedades y el acceso a la atención sanitaria para el ganado. La expansión de las actividades agrícolas en Asia Pacífico, América Latina y algunas partes de África requiere soluciones sanitarias fiables para mejorar la productividad y fortalecer la seguridad alimentaria. Las empresas pueden implementar estrategias localizadas mediante alianzas regionales, la expansión de la producción y la mejora de la distribución. Las previsiones del mercado de la salud animal indican que las regiones emergentes ofrecerán oportunidades a largo plazo a medida que aumente la adopción de la atención sanitaria en los sectores de animales de producción y de compañía. Las inversiones en programas de capacitación, capacidades de diagnóstico y redes veterinarias pueden impulsar aún más la penetración en el mercado y crear vías de crecimiento sostenible para los participantes del sector.

Innovación en terapias y diagnósticos avanzados

Los avances en biotecnología, diagnóstico y terapias dirigidas están creando oportunidades para que las empresas se diferencien mediante soluciones especializadas. Las inversiones en investigación y desarrollo pueden impulsar la creación de vacunas mejoradas, tratamientos de precisión y tecnologías para la identificación más rápida de enfermedades. Los profesionales de la salud veterinaria buscan cada vez más productos que mejoren la precisión, reduzcan los retrasos en el tratamiento y optimicen los resultados para los animales. Las colaboraciones estratégicas entre compañías farmacéuticas, proveedores de tecnología y organizaciones de investigación pueden acelerar la innovación. Las empresas centradas en plataformas integradas de atención médica que combinan diagnóstico, terapia y capacidades de monitorización están bien posicionadas para satisfacer las necesidades cambiantes de los clientes en aplicaciones para ganado y animales de compañía.

Novedades recientes

- Enero de 2026: Zoetis Inc. anunció la continua expansión de sus iniciativas de innovación en salud animal mediante inversiones en diagnóstico, soluciones biológicas y capacidades de salud digital diseñadas para apoyar a veterinarios y propietarios de animales en todo el mundo. La compañía hizo hincapié en la mejora de la detección de enfermedades y la gestión del tratamiento a través de tecnologías integradas en aplicaciones de salud para animales de compañía y ganado.

- Septiembre de 2025: Elanco Animal Health Incorporated presentó iniciativas estratégicas centradas en fortalecer su cartera de productos para la salud animal y ampliar el acceso a soluciones veterinarias. La compañía continuó invirtiendo en innovación, alianzas y desarrollo de productos para satisfacer las necesidades cambiantes de atención médica tanto de animales de compañía como de animales de producción de alimentos.

- Marzo de 2025: Boehringer Ingelheim International GmbH destacó los avances en sus programas de investigación en salud animal, centrándose en vacunas, atención médica preventiva y soluciones para el manejo de enfermedades. La compañía continuó desarrollando productos veterinarios destinados a mejorar la salud animal, al tiempo que apoya la producción ganadera sostenible y el cuidado de los animales de compañía en todo el mundo.

Preguntas frecuentes

Mrinal es una experimentada analista de investigación con más de 8 años de experiencia en inteligencia de mercado y consultoría en ciencias de la vida. Con una mentalidad estratégica y un firme compromiso con la excelencia, ha desarrollado una amplia experiencia en pronósticos farmacéuticos, evaluación de oportunidades de mercado y desarrollo de indicadores de referencia para la industria. Su trabajo se centra en brindar información práctica que permita a los clientes tomar decisiones estratégicas informadas.

La principal fortaleza de Mrinal reside en convertir conjuntos de datos cuantitativos complejos en inteligencia de negocios significativa. Su perspicacia analítica es fundamental para definir estrategias de salida al mercado (GTM) y descubrir oportunidades de crecimiento en los sectores farmacéutico y de dispositivos médicos. Como consultora de confianza, se centra constantemente en optimizar los procesos de flujo de trabajo y establecer las mejores prácticas, impulsando así la innovación y la eficiencia operativa para sus clientes.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias