Tendenze, domanda e crescita del mercato della salute animale entro il 2034

Dimensioni e previsioni del mercato della salute animale (2021-2034), quota di mercato globale e regionale, tendenze e analisi delle opportunità di crescita. Copertura del rapporto: per prodotto (con e senza prescrizione medica), per tipo di animale (animale da produzione e animale da compagnia) e per area geografica (Nord America, Europa, Asia Pacifico e Sud e Centro America).

- Stato : Dati rilasciati

- Codice del report : TIPRE00003540

- Categoria : Scienze della vita

- Numero di pagine : 194

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : August 04, 2026

Dimensioni del mercato nel 2025

76,02 miliardi di dollari USA

Valore dell'anno base

Previsioni per il 2034

160,90 miliardi di dollari USA

Previsione entro il 2034

CAGR 2026-2034

8,69 %

Tasso di crescita

Mercato di riferimento

1.062,00 miliardi di dollari USA

(2026-2034)

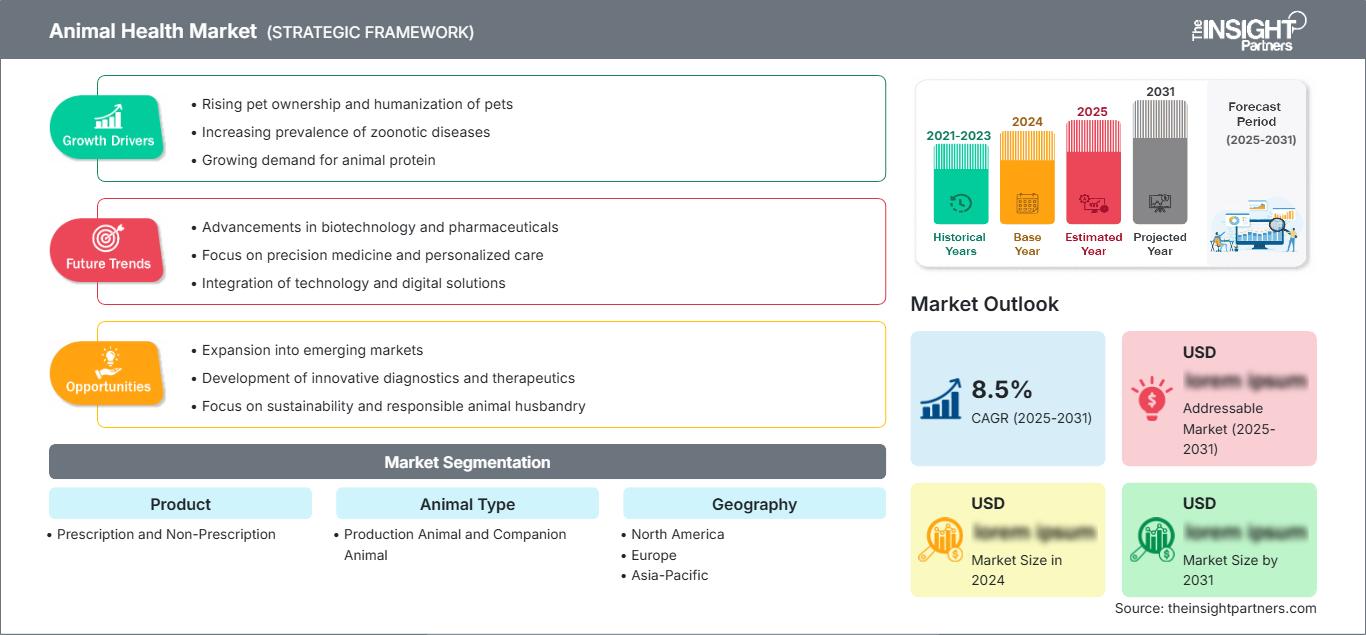

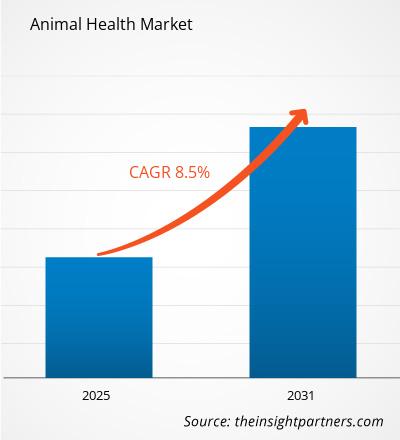

Il mercato della salute animale comprende prodotti e soluzioni a supporto della prevenzione, diagnosi, trattamento e benessere generale di animali da allevamento e da compagnia. Il mercato, valutato a 76,02 miliardi di dollari nel 2025, dovrebbe raggiungere i 160,90 miliardi di dollari entro il 2034, con un tasso di crescita annuo composto (CAGR) dell'8,69% dal 2026 al 2034. La crescente adozione di servizi di assistenza veterinaria, l'espansione dei sistemi di produzione animale e la crescente domanda di soluzioni di medicina preventiva stanno plasmando lo sviluppo del mercato a livello globale.

Il Nord America rappresenta un ecosistema maturo in continua espansione, supportato da infrastrutture veterinarie avanzate, dalla diffusione degli animali da compagnia e da una spesa crescente per il benessere animale. Si stima che la regione crescerà a un tasso annuo composto (CAGR) compreso tra il 7,50% e l'8,20% tra il 2026 e il 2034, trainata dalle piattaforme veterinarie digitali, dalla migliore adozione di strumenti diagnostici e dai crescenti investimenti nei servizi di assistenza sanitaria preventiva. Le dimensioni del mercato della salute animale in questa regione sono influenzate da aziende farmaceutiche consolidate, pratiche avanzate di gestione del bestiame e dall'enfasi normativa sul controllo delle malattie animali.

Analisi e approfondimenti sul mercato della salute animale

- Nord America La regione mantiene una posizione significativa con una quota stimata per il 2025 tra il 34% e il 38% e si prevede che crescerà a un tasso di crescita annuo composto (CAGR) del 7,50-8,20% tra il 2026 e il 2034. Solide reti veterinarie, la spesa per gli animali da compagnia e i programmi di salute del bestiame supportano una domanda sostenuta.

- Gli Stati Uniti rappresentano circa il 75-80% della quota nordamericana nel 2025 e si prevede che cresceranno a un tasso annuo composto (CAGR) del 7,60-8,30% tra il 2026 e il 2034. I farmaci veterinari avanzati, la diagnostica e l'adozione di servizi veterinari rimangono fattori chiave.

- L'Europa rappresenta una quota stimata tra il 27% e il 31% nel 2025 e si prevede che registrerà un tasso di crescita annuo composto (CAGR) del 7,20-7,90% tra il 2026 e il 2034. Germania, Regno Unito, Francia, Italia e Spagna contribuiscono attraverso la produzione zootecnica, i quadri normativi e l'innovazione veterinaria.

- La regione Asia-Pacifico detiene una quota di mercato pari a circa il 22-26% nel 2025 e si prevede che registrerà un tasso di crescita annuo composto (CAGR) del 9,10-9,80% tra il 2026 e il 2034. Cina, India, Giappone, Corea del Sud e Australia sostengono la crescita attraverso l'espansione della produzione animale e la modernizzazione del settore sanitario.

- Il segmento più ampio, quello degli animali da produzione, rappresenta una quota di mercato stimata tra il 55% e il 60% nel 2025 e si prevede che crescerà a un CAGR (tasso di crescita annuale composto) dell'8,20-8,80% tra il 2026 e il 2034, a causa delle esigenze di gestione delle malattie del bestiame.

- Il segmento degli animali da compagnia, caratterizzato da una forte crescita, rappresenta circa il 40-45% della quota di mercato nel 2025 e si prevede che raggiungerà un CAGR (tasso di crescita annuale composto) del 9,10-9,70% tra il 2026 e il 2034, grazie all'aumento della spesa per la salute degli animali domestici.

- Aziende chiave analizzate nel dettaglio: Merck & Co., Inc., Boehringer Ingelheim International GmbH, Ceva Sante Animale, Cargill Incorporated, Zoetis Inc., Bayer AG, Vetoquinol SA, Nutreco NV, Virbac, Elanco.

Fonte: Analisi di The Insight Partners basata su ricerche proprietarie, pubblicazioni governative, bilanci annuali aziendali, presentazioni agli investitori, database di settore e interviste a esperti.

La crescita del mercato è stata trainata dagli sviluppi nel campo dei farmaci veterinari, dei prodotti biotecnologici e degli strumenti di monitoraggio di precisione. Diagnostica, tecnologia e analisi dei dati vengono sempre più integrate dai produttori nei sistemi di assistenza sanitaria animale. I processi produttivi si sono orientati verso un approccio preventivo, poiché gli allevatori sono preoccupati per la produttività, la sicurezza alimentare e la resistenza alle malattie. Le aziende farmaceutiche si stanno diversificando nei settori dei vaccini, delle terapie, dei prodotti nutrizionali e dei farmaci da prescrizione per soddisfare le nuove esigenze veterinarie.

Lo sviluppo futuro del mercato sarà trainato dagli investimenti nei paesi in via di sviluppo, da una migliore regolamentazione e da un maggiore utilizzo di pratiche veterinarie preventive. I governi e le organizzazioni hanno iniziato a investire nella sorveglianza delle malattie animali e in iniziative di biosicurezza per proteggere le filiere alimentari. Una maggiore attenzione alla produzione zootecnica sostenibile e all'accesso alle cure sanitarie per gli animali da compagnia genererà nuove opportunità.

Ambito del rapporto sul mercato della salute animale

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2025 | 76,02 miliardi di dollari USA |

| Dimensioni del mercato entro il 2034 | 160,90 miliardi di dollari USA |

| Tasso di crescita annuo composto (CAGR) globale (2026-2034) | 8,69% |

| Dati storici | 2021-2024 |

| periodo di previsione | 2026-2034 |

Analisi del mercato della salute animale

La domanda di soluzioni per il mercato della salute animale è in aumento a causa della crescente produzione zootecnica, del numero sempre maggiore di animali domestici e della necessità di ridurre le perdite economiche causate dalle malattie animali. La crescita del mercato della salute animale è supportata da catene del valore integrate che coinvolgono produttori farmaceutici, cliniche veterinarie, distributori, allevamenti e fornitori di servizi per animali domestici. Gli approcci di assistenza sanitaria preventiva, tra cui vaccini e interventi nutrizionali, stanno acquisendo sempre maggiore importanza, poiché i produttori cercano di migliorare la produttività e ridurre i rischi di malattia.

Le dinamiche dell'offerta si stanno evolvendo grazie all'ampliamento della capacità produttiva, alle reti di distribuzione regionali e agli investimenti in ricerca e sviluppo. Le aziende si stanno concentrando su formulazioni innovative, metodi di somministrazione migliorati e terapie combinate. Gli standard normativi relativi agli animali destinati alla produzione alimentare influenzano lo sviluppo dei prodotti, mentre la domanda di assistenza sanitaria per animali da compagnia continua a incentivare la diversificazione di servizi e prodotti.

Il rapporto sul mercato della salute animale evidenzia la crescente competitività, con aziende di tutto il mondo che investono in innovazione, espansione e collaborazioni. Merck & Co., Inc. mantiene la sua attenzione sui farmaci veterinari e sulle soluzioni biologiche, mentre Boehringer Ingelheim International GmbH diversifica il suo portafoglio di soluzioni per la salute animale impiegando metodi basati sulla ricerca. Zoetis Inc. vanta una solida presenza in diverse tipologie di animali con una vasta gamma di soluzioni sanitarie.

Le iniziative strategiche includono innovazioni nella tecnologia veterinaria digitale, diagnostica avanzata e prodotti terapeutici. Ceva Sante Animale, Bayer AG, Elanco, Virbac, Vetoquinol SA, Cargill Incorporated e Nutreco NV sono alcune delle aziende che adottano soluzioni mirate per la nutrizione animale, la prevenzione delle malattie e la gestione sanitaria. I concorrenti utilizzano lo sviluppo di prodotti e l'espansione regionale come principali strategie competitive.

● PERSONALIZZAZIONE DEL REPORT

Personalizza questo report in base alle tue specifiche esigenze aziendali.

Questo report può essere personalizzato per allinearsi perfettamente ai vostri obiettivi aziendali, al vostro ambito di applicazione e ai vostri mercati di riferimento. Le opzioni di personalizzazione includono segmentazione su misura, analisi geografica, analisi della concorrenza e approfondimenti strategici a supporto di un processo decisionale informato.

Personalizza questo report →COSA PUOI REGOLARE

- ● Segmentazione

- ● Geografia

- ● Analisi della concorrenza

- ● Preferenze linguistiche

Mercato della salute animale: spunti strategici

Approfondimenti regionali

Mercato della salute animale del Nord America

Il Nord America mantiene una posizione di leadership con una quota stimata tra il 34% e il 38% nel 2025 e si prevede che crescerà a un tasso di crescita annuo composto (CAGR) del 7,50-8,20% tra il 2026 e il 2034. L'area beneficia della presenza di infrastrutture veterinarie consolidate, di un'elevata spesa per la salute degli animali da compagnia e di moderni sistemi di produzione zootecnica. Gli Stati Uniti rappresentano la maggiore fonte di domanda a livello regionale, grazie al consumo di prodotti farmaceutici e ai servizi veterinari specializzati.

Tra gli altri contributori allo sviluppo regionale figurano il Canada e il Messico, grazie al miglioramento della gestione della salute del bestiame e dei programmi di prevenzione delle malattie. Un quadro normativo rigoroso, l'elevata domanda di prodotti biologici e l'adozione di soluzioni di monitoraggio veterinario digitale stanno ampliando le opportunità di mercato. La presenza di aziende multinazionali, unitamente alle attività di ricerca e diagnostica, garantisce un potenziale di crescita futura nel settore della salute degli animali da compagnia e da produzione.

Mercato statunitense della salute animale

Gli Stati Uniti rappresentano circa il 75-80% della quota di mercato nordamericana nel settore della salute animale nel 2025 e si prevede che registreranno un tasso di crescita annuo composto (CAGR) del 7,60-8,30% tra il 2026 e il 2034. Il Paese gode di un'ampia disponibilità di servizi veterinari, di una diffusa presenza di animali domestici e di sofisticate tecniche di gestione del bestiame. Sempre più aziende farmaceutiche e altri fornitori di servizi stanno compiendo progressi con nuovi prodotti nei settori della prevenzione, della diagnosi e del trattamento.

Tra i principali attori del settore figurano Zoetis Inc., Merck & Co., Inc. ed Elanco, che vantano una presenza capillare grazie alla loro gamma di prodotti per animali da compagnia e da allevamento. Le tendenze di utilizzo si stanno orientando verso sistemi di gestione sanitaria di precisione, la digitalizzazione dei servizi veterinari e tecniche di trattamento personalizzate.

Mercato europeo della salute animale

Si stima che l'Europa rappresenterà una quota di mercato compresa tra il 27% e il 31% nel 2025 e si prevede che crescerà a un tasso annuo composto (CAGR) del 7,20-7,90% tra il 2026 e il 2034. La regione beneficia di sistemi veterinari consolidati, solidi quadri normativi e ampie capacità di produzione zootecnica. La Germania rappresenta uno dei mercati leader grazie al suo settore agricolo avanzato, alle infrastrutture veterinarie e all'attenzione alla produzione animale sostenibile.

Il Regno Unito continua a sostenere lo sviluppo del mercato aumentando la spesa per la salute degli animali da compagnia e adottando servizi veterinari avanzati. Francia, Italia e Spagna contribuiscono attraverso attività di allevamento, programmi di prevenzione delle malattie e l'espansione dell'uso di farmaci veterinari. La crescita regionale è influenzata dall'enfasi normativa sull'uso responsabile dei farmaci, sugli standard di sicurezza alimentare e sulle innovazioni nell'erogazione dei servizi sanitari per gli animali.

Mercato della salute animale nella regione Asia-Pacifico

Si stima che la regione Asia-Pacifico detenga una quota di mercato compresa tra il 22% e il 26% nel 2025 e si prevede che crescerà a un tasso annuo composto (CAGR) del 9,10-9,80% tra il 2026 e il 2034. La Cina è leader nella domanda regionale grazie agli elevati volumi di produzione zootecnica e alla crescente diffusione dei servizi di assistenza veterinaria. Anche India, Giappone, Corea del Sud e Australia contribuiscono attraverso la modernizzazione degli allevamenti e lo sviluppo della cura degli animali da compagnia.

L'allevamento su scala industriale, il crescente consumo di proteine e le iniziative governative a sostegno del controllo delle malattie animali stanno rafforzando le opportunità a livello regionale. Si prevede che gli investimenti nelle infrastrutture veterinarie e un migliore accesso ai prodotti sanitari accelereranno l'adozione di tali tecnologie nelle economie emergenti.

Mercato della salute animale in Medio Oriente e Africa

Si stima che la regione del Medio Oriente e dell'Africa crescerà a un tasso annuo composto (CAGR) del 6,80-7,50% tra il 2026 e il 2034. L'Arabia Saudita e gli Emirati Arabi Uniti stanno migliorando i sistemi sanitari per il bestiame attraverso investimenti nella sicurezza alimentare e nella modernizzazione dell'agricoltura. Il Sudafrica rimane un attore chiave grazie alle consolidate attività di produzione animale e ai servizi veterinari.

La crescita nel resto della regione MEA è sostenuta dallo sviluppo delle infrastrutture, da iniziative volte ad aumentare la produttività del bestiame e da programmi di gestione delle malattie. I ricavi del settore energetico e la capacità di investimento pubblico in diversi paesi supportano indirettamente la diversificazione agricola e il miglioramento della salute animale.

Analisi di segmentazione

Prodotto

Il segmento dei prodotti è suddiviso in soluzioni con e senza prescrizione medica. Si prevede che questo segmento registrerà un CAGR (tasso di crescita annuale composto) compreso tra l'8,50% e il 9,10% tra il 2026 e il 2034. La crescente domanda di prodotti per la prevenzione delle malattie, terapie veterinarie e prodotti nutrizionali per la salute animale supporta l'espansione del mercato. L'ambito di mercato all'interno delle categorie di prodotti continua ad ampliarsi man mano che i produttori introducono formulazioni avanzate, prodotti biologici e soluzioni preventive. I principali trend del mercato della salute animale includono la crescente adozione di animali da compagnia, la maggiore attenzione alla medicina preventiva, il crescente utilizzo di vaccini e farmaci biologici, i progressi nella gestione delle malattie del bestiame e l'integrazione di tecnologie digitali per la salute al fine di migliorare il monitoraggio, la diagnosi e i risultati del trattamento degli animali.

- I farmaci soggetti a prescrizione medica rimangono importanti per il trattamento delle malattie e per le cure veterinarie specialistiche, supportati da diagnosi professionali, approvazioni normative e una crescente diffusione tra gli allevatori e i proprietari di animali da compagnia.

- I prodotti da banco registrano una domanda costante grazie ad applicazioni per il benessere preventivo, integratori alimentari e soluzioni sanitarie facilmente accessibili utilizzate da agricoltori e proprietari di animali domestici.

Tipo di animale

Il segmento "Tipologia di animale" comprende le categorie "Animali da produzione" e "Animali da compagnia". Si prevede che questo segmento crescerà a un tasso annuo composto (CAGR) dell'8,70-9,30% tra il 2026 e il 2034. L'espansione della produzione zootecnica, l'aumento del numero di animali domestici e la crescente consapevolezza in materia di assistenza sanitaria preventiva influenzano i modelli di adozione. Il segmento rimane centrale per lo sviluppo del mercato, in quanto i fornitori di servizi sanitari si occupano delle diverse esigenze degli animali.

- Production Animal Solutions supporta la gestione della salute del bestiame attraverso la prevenzione delle malattie, il miglioramento della produttività e il rispetto dei requisiti di sicurezza alimentare per bovini, pollame, suini e altri sistemi agricoli.

- I servizi e i prodotti per animali da compagnia stanno acquisendo sempre maggiore importanza a causa dell'aumento del numero di animali domestici posseduti, dell'incremento delle visite veterinarie e della crescente attenzione dei consumatori al benessere a lungo termine degli animali.

Panoramica dell'opportunità

|

Tipo di animale |

Contributo di entrate |

Etichetta di tendenza |

Fase di adozione |

|

Animale da produzione |

Alto |

Benessere del bestiame |

Maturo |

|

Animale da compagnia |

Alto |

Assistenza sanitaria per animali domestici |

Scalatura |

Fattori di crescita e analisi del loro impatto sul mercato della salute animale

Aumento della domanda di assistenza sanitaria veterinaria preventiva

L'utilizzo della medicina preventiva si sta affermando come uno dei principali fattori determinanti della spesa nel settore della salute animale, con allevatori e proprietari di animali da compagnia che ora preferiscono prevenire le malattie piuttosto che curarle. Strumenti preventivi come vaccini, misure nutrizionali e diagnostiche possono ridurre al minimo i costi di produzione e migliorare il benessere animale. Vi è una crescente necessità di soluzioni standardizzate per la salute animale nella catena del valore alimentare internazionale, il che incoraggia la fornitura di prodotti sanitari più affidabili. L'industria veterinaria, così come gli enti regolatori, stanno inoltre promuovendo migliori sistemi di sorveglianza delle malattie, il che creerà una maggiore domanda di prodotti innovativi.

Espansione dei sistemi di produzione zootecnica

Con l'aumento della domanda di prodotti alimentari di origine animale in tutto il mondo, i sistemi di produzione animale si stanno modernizzando. Vengono impiegati interventi sanitari che contribuiscono ad aumentare l'efficienza degli allevamenti e a migliorare la salute degli animali. Per il buon funzionamento dei grandi allevamenti, è necessario un approccio integrato che includa farmaci, test diagnostici, controllo nutrizionale e assistenza veterinaria. Le economie emergenti investono nello sviluppo di infrastrutture agricole per garantire la sicurezza alimentare e la qualità del bestiame. In questo modo, le organizzazioni sanitarie hanno maggiori opportunità di offrire soluzioni scalabili in contesti diversi.

Crescita della spesa sanitaria per gli animali da compagnia

Il crescente numero di animali domestici e la maggiore consapevolezza in materia di salute degli animali stanno portando a una maggiore spesa per soluzioni sanitarie dedicate a questi animali. I proprietari di animali domestici sono alla ricerca di trattamenti, servizi diagnostici, nutrizione e assistenza veterinaria che contribuiscano a prolungare la vita dei loro animali e a garantirne una migliore qualità. La crescente urbanizzazione e l'aumento del reddito disponibile rendono più accessibile l'accesso a soluzioni sanitarie di alta qualità. Le cliniche veterinarie stanno diversificando la gamma di servizi offerti per far fronte a diverse patologie e alle esigenze di prevenzione.

Tendenze future del mercato della salute animale

Piattaforme veterinarie digitali e assistenza veterinaria basata sui dati

Si prevede che l'utilizzo delle tecnologie digitali trasformerà il processo decisionale in ambito veterinario, grazie al monitoraggio remoto, ai dispositivi connessi e ai sistemi di gestione sanitaria basati sui dati. Le applicazioni future si baseranno sempre più su diagnostica, intelligenza artificiale e analisi dei dati per l'individuazione precoce dei problemi di salute e per una maggiore efficacia dei trattamenti. Gli allevatori potrebbero iniziare a utilizzare tecnologie di sensoristica per monitorare il comportamento, l'alimentazione e lo stato di salute degli animali. Anche i veterinari che si occupano di animali da compagnia implementeranno tecnologie di consultazione digitale e cartelle cliniche elettroniche. Tali progressi tecnologici porteranno ad approcci più personalizzati nell'assistenza sanitaria e a una maggiore efficienza operativa.

Espansione delle soluzioni sostenibili per la salute animale

Si prevede che i fattori di responsabilità ambientale influenzeranno gli sviluppi futuri, poiché i produttori cercano metodi sostenibili per la gestione dei loro animali. È probabile che i produttori adottino strategie che migliorino le prestazioni degli animali e, al contempo, contribuiscano a ridurre il consumo di risorse e a promuovere pratiche di somministrazione dei farmaci responsabili. Si prevede che prodotti nutrizionali alternativi, tecniche di prevenzione delle malattie e sistemi di gestione delle patologie più efficaci saranno fondamentali nella gestione del bestiame. Le iniziative volte a rendere l'agricoltura sostenibile e a migliorare la sicurezza alimentare dovrebbero guidare l'innovazione. La combinazione di obiettivi di sostenibilità e scienza veterinaria creerà nuove opportunità per gli operatori sanitari.

Opportunità di mercato nel settore della salute animale

Investimenti nelle infrastrutture veterinarie dei mercati emergenti

Le economie in via di sviluppo offrono significative opportunità, poiché governi e organizzazioni private migliorano le infrastrutture veterinarie, i sistemi di monitoraggio delle malattie e l'accessibilità all'assistenza sanitaria per il bestiame. L'espansione delle attività agricole nell'area Asia-Pacifico, in America Latina e in alcune zone dell'Africa richiede soluzioni sanitarie affidabili per migliorare la produttività e rafforzare la sicurezza alimentare. Le aziende possono perseguire strategie localizzate attraverso partnership regionali, espansione della produzione e miglioramento della distribuzione. Le previsioni del mercato della salute animale indicano che le regioni emergenti offriranno opportunità a lungo termine, man mano che l'adozione di soluzioni sanitarie aumenterà sia nel settore della produzione che in quello degli animali da compagnia. Gli investimenti in programmi di formazione, capacità diagnostiche e reti veterinarie possono ulteriormente favorire la penetrazione del mercato e creare percorsi di crescita sostenibili per gli operatori del settore.

Innovazione nelle terapie e nella diagnostica avanzate

I progressi nel campo delle biotecnologie, della diagnostica e delle terapie mirate stanno creando opportunità per le aziende di differenziarsi attraverso soluzioni specializzate. Gli investimenti in ricerca e sviluppo possono supportare la creazione di vaccini migliori, trattamenti di precisione e tecnologie per l'identificazione più rapida delle malattie. Gli operatori sanitari veterinari sono sempre più alla ricerca di prodotti che migliorino la precisione, riducano i tempi di trattamento e migliorino gli esiti per gli animali. Le collaborazioni strategiche tra aziende farmaceutiche, fornitori di tecnologia e organizzazioni di ricerca possono accelerare l'innovazione. Le aziende che si concentrano su piattaforme sanitarie integrate che combinano capacità diagnostiche, terapeutiche e di monitoraggio sono ben posizionate per soddisfare le esigenze in continua evoluzione dei clienti nel settore dell'allevamento e degli animali da compagnia.

Sviluppi recenti

- Gennaio 2026: Zoetis Inc. ha annunciato la continua espansione delle sue iniziative di innovazione nel settore della salute animale attraverso investimenti in diagnostica, soluzioni biologiche e funzionalità di sanità digitale, progettate per supportare veterinari e proprietari di animali in tutto il mondo. L'azienda ha posto l'accento sul miglioramento dell'individuazione e della gestione del trattamento delle malattie attraverso tecnologie integrate per applicazioni sanitarie destinate sia agli animali da compagnia che al bestiame.

- Settembre 2025: Elanco Animal Health Incorporated ha introdotto iniziative strategiche incentrate sul rafforzamento del proprio portafoglio di prodotti per la salute animale e sull'ampliamento dell'accesso alle soluzioni veterinarie. L'azienda ha continuato a investire in innovazione, partnership e sviluppo di prodotti per rispondere alle esigenze sanitarie in continua evoluzione degli animali da compagnia e da reddito.

- Marzo 2025: Boehringer Ingelheim International GmbH ha evidenziato i progressi compiuti nei suoi programmi di ricerca sulla salute animale, concentrandosi su vaccini, assistenza sanitaria preventiva e soluzioni per la gestione delle malattie. L'azienda ha continuato a sviluppare prodotti veterinari volti a migliorare la salute degli animali, supportando al contempo la produzione zootecnica sostenibile e la cura degli animali da compagnia in tutto il mondo.

Domande frequenti

Mrinal è un'analista di ricerca esperta con oltre 8 anni di esperienza nella consulenza e nell'intelligence di mercato nel settore delle scienze biologiche. Grazie a una mentalità strategica e a un costante impegno verso l'eccellenza, ha maturato una profonda competenza nelle previsioni farmaceutiche, nella valutazione delle opportunità di mercato e nello sviluppo di benchmark di settore. Il suo lavoro è incentrato sulla fornitura di insight fruibili che consentono ai clienti di prendere decisioni strategiche consapevoli.

Il punto di forza di Mrinal risiede nella capacità di tradurre complessi set di dati quantitativi in business intelligence significative. Il suo acume analitico è fondamentale per definire strategie di go-to-market (GTM) e individuare opportunità di crescita nei settori farmaceutico e dei dispositivi medici. In qualità di consulente di fiducia, si concentra costantemente sulla semplificazione dei processi di flusso di lavoro e sulla definizione di best practice, promuovendo così l'innovazione e l'efficienza operativa per i suoi clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative