Informe de mercado de Gestión de derechos de infraestructura en la nube (CIEM) 2031 por segmentos, geografía, dinámica, desarrollos recientes e ideas estratégicas

Tamaño y pronóstico del mercado de gestión de derechos de infraestructura en la nube (CIEM) (2021-2031), análisis de participación global y regional, tendencias y oportunidades de crecimiento. Cobertura del informe: por componente (solución y servicios), tamaño de la organización (grandes empresas y pymes), usuario final (TI y telecomunicaciones, atención médica, BFSI, fabricación, comercio minorista y electrónico, entre otros) y geografía.

- Estado : Publicada

- Código de informe : TIPRE00039034

- Categoría : Tecnología, medios y telecomunicaciones

- Número de páginas : 183

- Formatos de informe disponibles :

- Fecha de última actualización : August 27, 2024

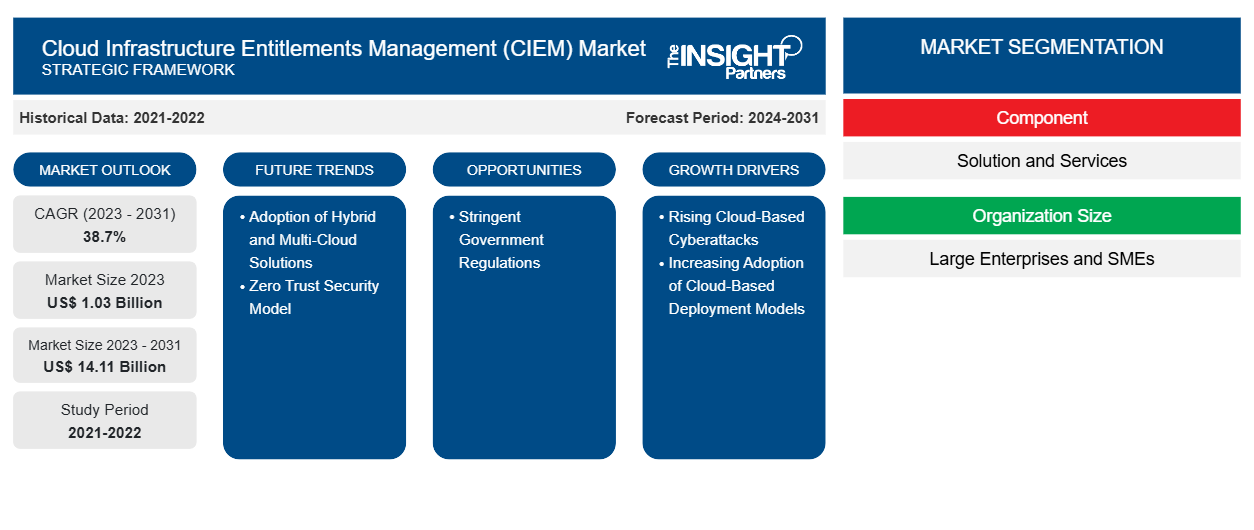

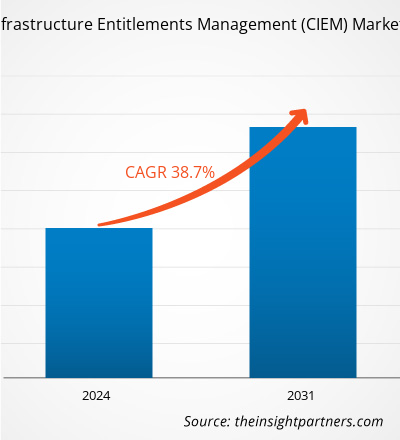

Se espera que el tamaño del mercado de gestión de derechos de infraestructura en la nube (CIEM) alcance los 14.110 millones de dólares estadounidenses en 2031, frente a los 1.030 millones de dólares estadounidenses en 2023. Se estima que el mercado registrará una CAGR del 38,7 % durante el período 2023-2031. Es probable que traigan nuevas tendencias al mercado.

Análisis del mercado de gestión de derechos de infraestructura en la nube (CIEM)

La necesidad de gestión de derechos de infraestructura en la nube (CIEM) está siendo impulsada por la creciente necesidad de las empresas de mejorar su seguridad en la nube. El uso creciente de soluciones y servicios en la nube, proyectos de transformación digital y un mayor número de ciberataques basados en la nube son algunos de los factores que impulsan el mercado. La pandemia de COVID-19 provocó que muchas empresas cambiaran de la computación local a la computación en la nube, lo que llevó a la expansión del mercado de gestión de derechos de infraestructura en la nube (CIEM) . El informe incluye perspectivas de crecimiento debido a las tendencias actuales del mercado de gestión de derechos de infraestructura en la nube (CIEM) y su impacto previsible durante el período de pronóstico.

Descripción general del mercado de gestión de derechos de infraestructura en la nube (CIEM)

La gestión de derechos de infraestructura en la nube (CIEM), o las soluciones de gestión de derechos de infraestructura en la nube o las soluciones de gestión de permisos en la nube, es una solución de seguridad en la nube que mitiga el riesgo de violaciones de datos en entornos de nube pública. Las soluciones de gestión de derechos de infraestructura en la nube están desarrolladas específicamente para gestionar los privilegios de forma estricta y consistente en entornos complejos y dinámicos. Las soluciones de gestión de derechos de infraestructura en la nube supervisan continuamente los permisos y la actividad de las entidades para evitar derechos excesivos. Las principales funciones de CIEM son la visibilidad de los derechos, la corrección de los permisos, el análisis avanzado y el cumplimiento normativo.

Personalice este informe según sus necesidades

Obtendrá personalización en cualquier informe, sin cargo, incluidas partes de este informe o análisis a nivel de país, paquete de datos de Excel, así como también grandes ofertas y descuentos para empresas emergentes y universidades.

Mercado de gestión de derechos de infraestructura en la nube (CIEM): perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Impulsores y oportunidades del mercado de gestión de derechos de infraestructura en la nube (CIEM)

Aumento de los ciberataques basados en la nube

La adopción de la computación en la nube ha ganado una tracción masiva en los últimos años con actores clave como Amazon, Google y Microsoft. La computación en la nube ha alterado la forma en que las empresas usan, almacenan y comparten datos e información. Sin embargo, todo lo que opera digitalmente inevitablemente se convertirá en un objetivo de los actores cibernéticos. El cambio de las organizaciones hacia la computación en la nube ha creado nuevas vías para que los ciberdelincuentes exploten vulnerabilidades, comprometan datos y causen estragos en organizaciones de todos los tamaños. Los datos almacenados en el entorno de la nube son más vulnerables que los datos en servidores locales. La configuración incorrecta, las cuentas de usuario comprometidas, las vulnerabilidades de las API, la actividad interna maliciosa y otras se encuentran entre las principales causas de los ciberataques de computación en la nube. En los últimos años, la cantidad de ataques a las plataformas en la nube ha aumentado rápidamente. Los ciberataques basados en la nube representaron el 20% de todos los ciberataques en 2020, lo que convierte a las plataformas basadas en la nube en el tercer entorno cibernético más atacado. En enero de 2020, Microsoft anunció que una de sus bases de datos en la nube había sufrido una vulneración en diciembre de 2019, lo que dio lugar a la exposición de 250 millones de entradas, incluidas direcciones de correo electrónico, direcciones IP y detalles de casos de soporte. La gestión de derechos de infraestructura en la nube (CIEM) es una solución de seguridad en la nube automatizada que mitiga el riesgo de vulneraciones de datos en entornos de nube pública mediante la implementación de la seguridad en la nube. Por tanto, el aumento de los ciberataques basados en la nube impulsa el crecimiento del mercado de gestión de derechos de infraestructura en la nube.

Regulaciones gubernamentales estrictas

Diversas regulaciones gubernamentales e industriales exigen que las empresas cumplan con estrictos controles de seguridad. En un escenario como este, la gestión de los derechos de infraestructura en la nube es un aspecto crucial de la estrategia de ciberseguridad de una organización. En industrias como la atención médica, las finanzas y el gobierno que manejan datos confidenciales, las organizaciones de todos los tamaños deben cumplir con regulaciones complejas como GDPR, HIPAA, PCI-DSS y SOX para proteger los datos confidenciales de los consumidores y las empresas. El incumplimiento de estas regulaciones puede dar lugar a fuertes multas y dañar la reputación de la organización. Por ejemplo, el Reglamento General de Protección de Datos (GDPR), establecido en 2018, impone multas que van desde US$ 21,68 millones (EUR 20 millones) o el 4% de los ingresos anuales globales de la empresa, lo que sea mayor. De manera similar, las multas por violaciones de la Ley de Portabilidad y Responsabilidad del Seguro Médico (HIPAA) pueden llegar a US$ 1,5 millones por infracción. La Comisión de Bolsa y Valores (SEC) impone multas que van desde decenas de miles hasta millones de dólares. Las multas por infracciones de la Administración de Seguridad y Salud Ocupacional (OSHA) pueden llegar a los 134.937 dólares estadounidenses por infracción, mientras que las infracciones de la Ley de Prácticas Corruptas en el Extranjero (FCPA) pueden requerir una multa de un total de 25 millones de dólares estadounidenses o más. La Agencia de Protección Ambiental (EPA) puede multar hasta 50.000 dólares estadounidenses por día por infracción. Las empresas de todo el mundo se han enfrentado a enormes multas debido a la violación de estas regulaciones. Por ejemplo, según una encuesta de 500 organizaciones de todo el mundo realizada por Kaspersky, la pérdida media de una empresa por una infracción es de 551.000 dólares estadounidenses, de los cuales la pérdida media de las pequeñas y medianas empresas por una infracción es de 38.000 dólares estadounidenses. Por lo tanto, las organizaciones deben implementar soluciones de gestión de derechos de infraestructura en la nube para cumplir con estrictas regulaciones gubernamentales como PCI DSS, CCPA, HIPAA, SOX y GDPR, lo que brinda oportunidades lucrativas para el crecimiento del mercado.

Informe de mercado sobre gestión de derechos de infraestructura en la nube (CIEM) Análisis de segmentación

Los segmentos clave que contribuyeron a la derivación del análisis del mercado de gestión de derechos de infraestructura en la nube (CIEM) son el componente, el tamaño de la organización, el usuario final y la geografía.

- Según los componentes, el mercado se divide en soluciones y servicios. El segmento de soluciones dominó el mercado en 2023.

- En términos de tamaño de la organización, el mercado se divide en grandes empresas y pymes. El segmento de las grandes empresas dominó el mercado en 2023.

- Según el usuario final, el mercado está segmentado en TI y telecomunicaciones, atención médica, fabricación, BFSI, comercio minorista y comercio electrónico, entre otros. El segmento de TI y telecomunicaciones tuvo una mayor participación en el mercado en 2023.

Análisis de la cuota de mercado de la gestión de derechos de infraestructura en la nube (CIEM) por geografía

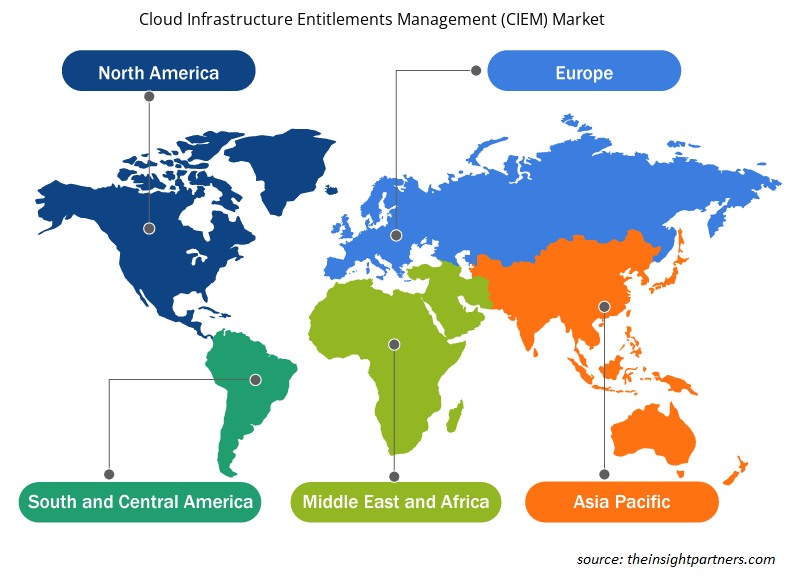

El mercado de gestión de derechos de infraestructura en la nube (CIEM) está segmentado en cinco regiones principales: América del Norte, Europa, Asia Pacífico (APAC), Oriente Medio y África (MEA) y América del Sur y Central. América del Norte dominó el mercado en 2023, seguida de Europa y APAC.

América del Norte es una de las regiones de más rápido crecimiento en términos de innovaciones tecnológicas y adopción de tecnologías avanzadas. La creciente infraestructura de TI de la región y el cambio acelerado a los servicios en la nube requieren medidas de seguridad avanzadas. En 2023, América del Norte tenía la mayor participación de mercado en el mercado de gestión de derechos de infraestructura en la nube (CIEM). La creciente prevalencia de los servicios móviles y el creciente número de violaciones de seguridad vinculadas al abuso de identidad y acceso privilegiado contribuyen a la adopción de soluciones CIEM en la región. Las soluciones CIEM en América del Norte tienen como objetivo gestionar identidades y privilegios en entornos de nube. Su objetivo es comprender los derechos de acceso que existen en los entornos de nube y multinube y luego identificar y mitigar el riesgo de los derechos.

Perspectivas regionales del mercado de gestión de derechos de infraestructura en la nube (CIEM)

Los analistas de Insight Partners explicaron en detalle las tendencias y los factores regionales que influyen en el mercado de gestión de derechos de infraestructura en la nube (CIEM) durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de gestión de derechos de infraestructura en la nube (CIEM) en América del Norte, Europa, Asia Pacífico, Oriente Medio y África, y América del Sur y Central.

- Obtenga datos regionales específicos para el mercado de gestión de derechos de infraestructura en la nube (CIEM)

Alcance del informe de mercado sobre gestión de derechos de infraestructura en la nube (CIEM)

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2023 | 1.030 millones de dólares estadounidenses |

| Tamaño del mercado en 2031 | US$ 14,11 mil millones |

| CAGR global (2023 - 2031) | 38,7% |

| Datos históricos | 2021-2022 |

| Período de pronóstico | 2024-2031 |

| Segmentos cubiertos |

Por componente

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado de gestión de derechos de infraestructura en la nube (CIEM): comprensión de su impacto en la dinámica empresarial

El mercado de gestión de derechos de infraestructura en la nube (CIEM) está creciendo rápidamente, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor conciencia de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían sus ofertas, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

La densidad de actores del mercado se refiere a la distribución de las empresas o firmas que operan dentro de un mercado o industria en particular. Indica cuántos competidores (actores del mercado) están presentes en un espacio de mercado determinado en relación con su tamaño o valor total de mercado.

Las principales empresas que operan en el mercado de gestión de derechos de infraestructura en la nube (CIEM) son:

- Microsoft

- Redes de Palo Alto

- Tecnologías de software de Check Point Ltd.

- CrowdStrike Holdings Inc

- Software CyberArk Ltd.

- Radware Ltd

Descargo de responsabilidad : Las empresas enumeradas anteriormente no están clasificadas en ningún orden particular.

- Obtenga una descripción general de los principales actores clave del mercado de gestión de derechos de infraestructura en la nube (CIEM)

Noticias y desarrollos recientes del mercado de gestión de derechos de infraestructura en la nube (CIEM)

El mercado de gestión de derechos de infraestructura en la nube (CIEM) se evalúa mediante la recopilación de datos cualitativos y cuantitativos posteriores a la investigación primaria y secundaria, que incluye publicaciones corporativas importantes, datos de asociaciones y bases de datos. A continuación, se enumeran algunos de los desarrollos en el mercado de gestión de derechos de infraestructura en la nube (CIEM):

- Lacework anunció el lanzamiento de la capacidad de gestión de derechos en la nube para su plataforma de protección de aplicaciones nativa de la nube (CNAPP). Con este nuevo conjunto de capacidades, las organizaciones pueden aplicar el principio del mínimo privilegio al crear, implementar, usar y administrar servicios de infraestructura en la nube. (Fuente: Lacework, comunicado de prensa, junio de 2023)

- Tenable anunció la adquisición de Ermetic, Ltd. Con esta adquisición, Tenable y Ermetic ayudarán a las organizaciones a abordar algunos de los desafíos más difíciles en materia de ciberseguridad. (Fuente: Tenable, comunicado de prensa, octubre de 2023)

- Uptycs anunció el lanzamiento de capacidades de gestión de derechos de infraestructura en la nube (CIEM) que fortalecen su oferta de gestión de la postura de seguridad en la nube (CSPM). Además, Uptycs anunció la compatibilidad de CSPM con Google Cloud Platform (GCP) y Microsoft Azure, así como la cobertura de cumplimiento de PCI. Estas nuevas capacidades brindan a los equipos de seguridad y gobernanza, riesgo y cumplimiento un monitoreo continuo de los servicios en la nube, las identidades y los derechos para reducir su riesgo de ataques en la nube. (Fuente: Uptycs, comunicado de prensa, mayo de 2022)

Informe de mercado sobre gestión de derechos de infraestructura en la nube (CIEM) y resultados finales

El informe "Tamaño y pronóstico del mercado de gestión de derechos de infraestructura en la nube (CIEM) (2021-2031)" proporciona un análisis detallado del mercado que cubre las áreas mencionadas a continuación:

- Tamaño y pronóstico del mercado de gestión de derechos de infraestructura en la nube (CIEM) a nivel global, regional y nacional para todos los segmentos clave del mercado cubiertos por el alcance

- Tendencias del mercado de gestión de derechos de infraestructura en la nube (CIEM), así como dinámica del mercado, como impulsores, restricciones y oportunidades clave

- Análisis PEST y FODA detallados

- Análisis del mercado de gestión de derechos de infraestructura en la nube (CIEM) que abarca las tendencias clave del mercado, el marco global y regional, los principales actores, las regulaciones y los desarrollos recientes del mercado

- Análisis del panorama de la industria y de la competencia que abarca la concentración del mercado, el análisis de mapas de calor, los actores destacados y los desarrollos recientes para el mercado de gestión de derechos de infraestructura en la nube (CIEM)

- Perfiles detallados de empresas

Ankita es una profesional dinámica en investigación de mercados y consultoría con más de 8 años de experiencia en los sectores de tecnología, medios de comunicación, TIC, electrónica y semiconductores. Ha liderado y ejecutado con éxito más de 100 proyectos de consultoría e investigación para clientes globales como Microsoft, Oracle, NEC Corporation, SAP, KPMG y Expeditors International. Sus principales competencias incluyen la evaluación de mercado, el análisis de datos, la previsión, la formulación de estrategias, la inteligencia competitiva y la redacción de informes.

Ankita es experta en la gestión de ciclos completos de proyecto, desde el diseño de propuestas de preventa y las conversaciones con los clientes hasta la entrega de información práctica posventa. Es experta en la gestión de equipos multifuncionales, la estructuración de módulos de investigación complejos y la alineación de soluciones con los objetivos de negocio específicos del cliente. Sus excelentes habilidades de comunicación, liderazgo y presentación le han permitido obtener constantemente resultados orientados al valor en entornos de mercado dinámicos y en constante evolución.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias