Tendencias, participación y demanda del mercado de terapias contra el cáncer de próstata hasta 2034

Tamaño y pronóstico del mercado de terapias para el cáncer de próstata (2021-2034), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por tipo de terapia (terapia hormonal, quimioterapia, terapia dirigida, inmunoterapia y otras), usuario final (hospitales, clínicas especializadas y otros) y geografía.

- Estado : Datos publicados

- Código de informe : TIPRE00003423

- Categoría : Ciencias de la vida

- Número de páginas : 150

- Formatos de informe disponibles :

- Fecha de última actualización : April 01, 2026

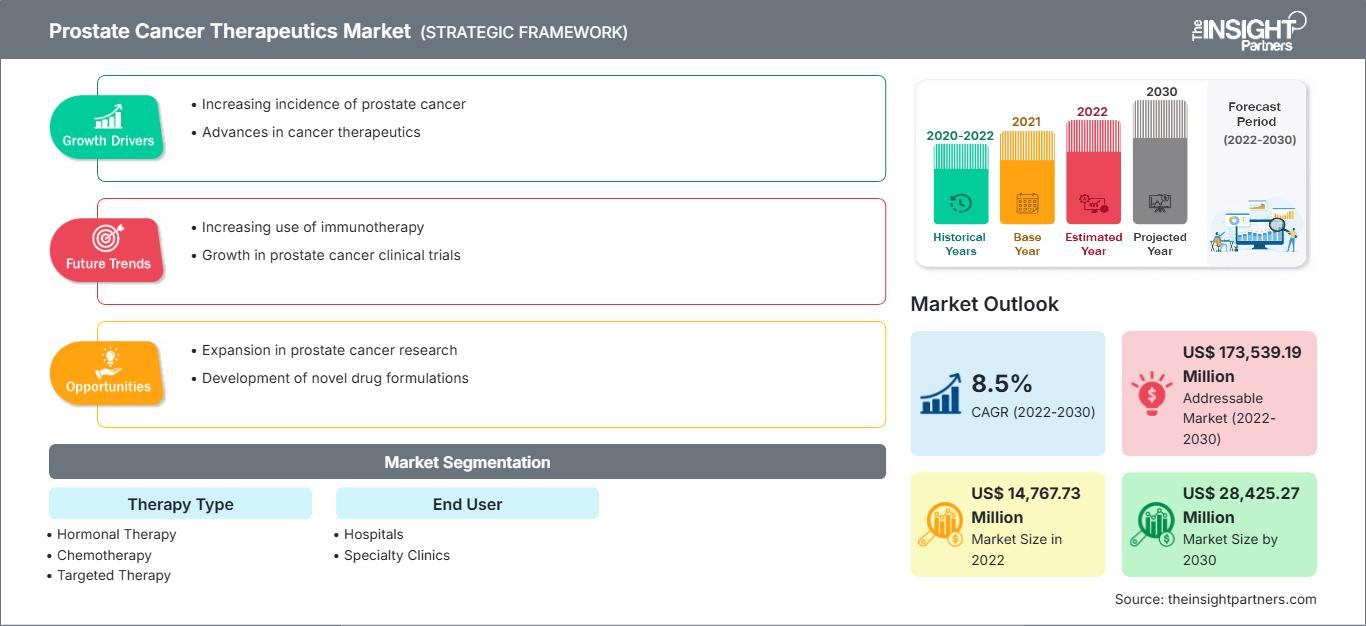

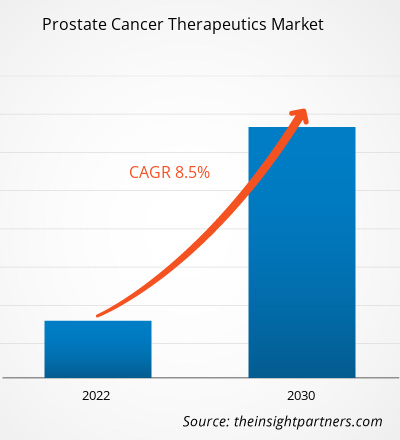

Se prevé que el mercado mundial de tratamientos para el cáncer de próstata alcance los 55.050 millones de dólares estadounidenses en 2034, frente a los 21.800 millones de dólares estadounidenses de 2025. Se espera que el mercado registre una tasa de crecimiento anual compuesta (CAGR) del 10,84% durante el período de previsión 2026-2034.

Entre las principales dinámicas del mercado se incluyen el envejecimiento de la población masculina mundial, el aumento de la incidencia del cáncer de próstata metastásico resistente a la castración (CPRCm) y un cambio significativo hacia la oncología de precisión y las terapias con radioligandos. Además, se prevé que el mercado se beneficie de la creciente adopción de terapias combinadas, la ampliación de las aprobaciones regulatorias para indicaciones de tratamiento en etapas tempranas y la integración del perfil genómico para personalizar los regímenes terapéuticos de cada paciente.

Análisis del mercado de terapias para el cáncer de próstata

El análisis del mercado de terapias para el cáncer de próstata destaca una transición hacia intervenciones dirigidas y personalizadas, a medida que la comunidad médica busca superar la resistencia a las terapias tradicionales de privación de andrógenos. Las tendencias de adquisición indican una creciente preferencia por los agentes hormonales orales de nueva generación y los radiofármacos avanzados que ofrecen una eficacia superior con perfiles de seguridad manejables. Están surgiendo oportunidades estratégicas en los entornos pre-taxano y no metastásico, donde la intervención temprana con inhibidores potentes puede retrasar significativamente la progresión de la enfermedad y mejorar la supervivencia general. El análisis también señala que el éxito del mercado depende cada vez más de los diagnósticos complementarios, que identifican mutaciones genéticas específicas como BRCA1/2, lo que permite la implementación de alto margen de los inhibidores de PARP. La diferenciación competitiva ahora se centra en la secuencia del tratamiento, proporcionando una hoja de ruta clínica clara que maximiza la duración de cada línea de terapia y minimiza la toxicidad acumulativa para el paciente.

Panorama general del mercado de terapias para el cáncer de próstata

El tratamiento del cáncer de próstata está evolucionando, pasando de depender de la quimioterapia de amplio espectro a un ecosistema diverso de agentes específicos para cada mecanismo de acción. Si bien la terapia hormonal sigue siendo la base del tratamiento, el panorama incorpora rápidamente inmunoterapias, terapias alfa dirigidas y activadores biespecíficos de células T. Tanto las grandes farmacéuticas multinacionales como las empresas biotecnológicas en fase clínica impulsan la innovación, especialmente en el desarrollo de la teranóstica, que combina el diagnóstico por imagen con la administración terapéutica. A medida que los sistemas sanitarios globales se orientan hacia la atención basada en el valor, se observa un mayor interés en terapias que ofrezcan no solo mayores tasas de supervivencia, sino también una mejor calidad de vida. Norteamérica y Europa siguen siendo los principales centros de ingresos debido a las altas tasas de detección precoz. Sin embargo, la región de Asia-Pacífico está emergiendo como un motor de crecimiento fundamental para las exportaciones de alto volumen de fármacos oncológicos genéricos y biosimilares. Por ejemplo, el mercado estadounidense representa el mayor mercado individual para el tratamiento del cáncer de próstata, caracterizado por una infraestructura sanitaria sofisticada y la pronta adopción de medicamentos innovadores. Una sólida cartera de ensayos clínicos y un alto acceso de los pacientes a centros oncológicos especializados sustentan el crecimiento del mercado. Las políticas de reembolso favorables y la defensa enérgica de la detección temprana y las pruebas genómicas están configurando cada vez más el panorama.

Personaliza este informe para adaptarlo a tus necesidades.

Obtén PERSONALIZACIÓN GRATUITAMercado de tratamientos para el cáncer de próstata: Perspectivas estratégicas

-

Descubra las principales tendencias del mercado que se recogen en este informe.Esta muestra GRATUITA incluirá análisis de datos, que abarcan desde tendencias de mercado hasta estimaciones y pronósticos.

Factores impulsores y oportunidades del mercado de terapias para el cáncer de próstata

Factores que impulsan el mercado:

- Expansión de la terapia con radioligandos dirigidos: El éxito de agentes como el Lutecio-177-PSMA-617 ha revolucionado el tratamiento de las etapas avanzadas del cáncer. Estas terapias administran radiación localizada directamente a las células cancerosas, lo que representa una opción eficaz para los pacientes que han agotado los tratamientos hormonales y citotóxicos tradicionales.

- Aumento de la población geriátrica y de la prevalencia de enfermedades: Dado que el riesgo de cáncer de próstata aumenta significativamente después de los 50 años, el cambio demográfico mundial hacia una población de mayor edad está creando un grupo de pacientes en expansión natural, lo que requiere un manejo terapéutico a largo plazo.

- Avances en pruebas genómicas y de biomarcadores: La integración del perfil genético permite a los médicos identificar los factores moleculares específicos que impulsan el tumor de un paciente. Este cambio hacia la medicina de precisión está impulsando la demanda de fármacos especializados como los inhibidores de PARP y los inhibidores de puntos de control inmunitario.

Oportunidades de mercado:

- Ampliación de la indicación a tratamientos en fases iniciales: Existe un importante potencial de crecimiento al trasladar fármacos superventas ya consolidados de las fases avanzadas de tratamiento de última línea a los tratamientos de primera línea para enfermedades sensibles a las hormonas, lo que aumenta exponencialmente la población de pacientes elegibles y la duración del tratamiento.

- Desarrollo de formulaciones orales y fáciles de usar para el paciente: Existe una gran demanda de comprimidos orales de administración diaria que reduzcan la necesidad de infusiones hospitalarias. Mejorar el cumplimiento del tratamiento por parte del paciente mediante métodos de administración convenientes representa una importante ventaja competitiva para los fabricantes.

- Penetración en los mercados emergentes de APAC y LAMEA: A medida que mejora la infraestructura sanitaria en regiones como China e India, existen grandes oportunidades para establecer alianzas estratégicas que permitan introducir carteras de productos oncológicos de alto valor a poblaciones de clase media en rápido crecimiento.

Análisis de segmentación del informe de mercado de terapias para el cáncer de próstata

La cuota de mercado de los tratamientos para el cáncer de próstata se analiza en diversos segmentos para comprender mejor su estructura, potencial de crecimiento y tendencias emergentes. A continuación, se muestra el enfoque de segmentación estándar utilizado en la mayoría de los informes del sector:

Por tipo de terapia:

- Terapia hormonal: Sigue siendo el segmento fundamental, utilizado como tratamiento de primera línea para suprimir los niveles de andrógenos; domina el volumen de mercado debido a su uso a largo plazo en múltiples etapas de la enfermedad.

- Quimioterapia: Tradicionalmente utilizada para casos metastásicos avanzados, este segmento sigue siendo relevante para pacientes con perfiles de enfermedad agresivos y resistentes a las hormonas.

- Terapia dirigida: Un segmento de alto crecimiento centrado en vías moleculares específicas, como los inhibidores de PARP para pacientes con mutaciones en genes de reparación del ADN.

- Inmunoterapia: Un campo emergente que aprovecha el sistema inmunitario del cuerpo para combatir las células cancerosas, y que se muestra prometedor en subgrupos específicos de pacientes resistentes al tratamiento.

Por el usuario final:

- Hospitales: El entorno principal para la administración de terapias complejas, en particular aquellas que requieren centros de infusión especializados o instalaciones de medicina nuclear para radiofármacos.

- Clínicas especializadas: Su popularidad está en aumento debido a su enfoque en la atención oncológica personalizada y la administración ambulatoria eficiente de terapias orales e inyectables.

- Otros: Incluye institutos de investigación académica y centros de atención domiciliaria donde se realizan el mantenimiento y la monitorización a largo plazo.

Por geografía:

- América del norte

- Europa

- Asia Pacífico

- América del Sur y Central

- Oriente Medio y África

Alcance del informe de mercado sobre terapias para el cáncer de próstata

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2025 | 21.800 millones de dólares estadounidenses |

| Tamaño del mercado para el período 2026-2034 | 55.050 millones de dólares estadounidenses |

| Tasa de crecimiento anual compuesta global (2026 - 2034) | 10,84% |

| Datos históricos | 2021-2024 |

| Período de pronóstico | 2026-2034 |

| Segmentos cubiertos |

Por tipo de terapia

|

| Regiones y países incluidos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de los actores del mercado de terapias para el cáncer de próstata: comprender su impacto en la dinámica empresarial.

El mercado de tratamientos para el cáncer de próstata está experimentando un rápido crecimiento, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor concienciación sobre los beneficios del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

Análisis de la cuota de mercado de los tratamientos para el cáncer de próstata por región geográfica.

Se prevé que la región de Asia-Pacífico experimente el mayor crecimiento en los próximos años. Los mercados emergentes de América del Sur y Central, Oriente Medio y África también ofrecen numerosas oportunidades sin explotar para la expansión de los fabricantes de fármacos oncológicos y los proveedores de diagnóstico.

El mercado de tratamientos para el cáncer de próstata está experimentando una transformación significativa, pasando de un enfoque hormonal estándar a un modelo de medicina de precisión altamente especializado. El crecimiento se debe a la creciente prevalencia de casos resistentes al tratamiento, al aumento de la prescripción basada en la genómica y a la expansión del sector de radiofármacos de alto valor. A continuación, se presenta un resumen de la cuota de mercado y las tendencias por región:

América del norte

- Cuota de mercado: Domina el mercado global, gracias a una sofisticada infraestructura oncológica y a la mayor tasa de adopción mundial de terapias innovadoras.

-

Factores clave:

- Alta prevalencia de la enfermedad y cribado: Los sólidos programas nacionales de cribado y la elevada concienciación pública dan lugar a un volumen significativo de casos diagnosticados que requieren un tratamiento a largo plazo.

- Adopción temprana de fármacos innovadores: Ciclos de aprobación rápidos por parte de la FDA y alta disposición de los médicos para prescribir radioligandos e inhibidores de PARP de reciente lanzamiento.

- Panorama favorable en materia de reembolsos: La cobertura integral de los seguros y el apoyo gubernamental a los tratamientos oncológicos de alto coste garantizan un amplio acceso de los pacientes a terapias de primera calidad.

- Tendencias: Mayor énfasis clínico en la intensificación del tratamiento mediante terapias triples y una transición hacia la administración oral una vez al día para mejorar la adherencia del paciente.

Europa

- Cuota de mercado: Posee la segunda mayor cuota, gracias a los sistemas sanitarios centralizados y al estricto cumplimiento de las directrices clínicas en países como Alemania, Francia y el Reino Unido.

-

Factores clave:

- Crecimiento demográfico geriátrico: El rápido envejecimiento de la población masculina está impulsando una demanda constante tanto de terapias hormonales de primera línea como de mantenimiento.

- Iniciativas sólidas de salud pública: Las hojas de ruta oncológicas respaldadas por los gobiernos priorizan la intervención temprana y el acceso equitativo a la atención oncológica avanzada en toda la UE.

- Colaboraciones sólidas entre el ámbito académico y la industria: una alta concentración de instituciones de investigación que se asocian con gigantes farmacéuticos para impulsar los ensayos clínicos locales y la innovación terapéutica.

- Tendencias: Un cambio estratégico hacia la contención de costes mediante el uso de biosimilares de alta calidad y un énfasis creciente en las Evaluaciones de Tecnologías Sanitarias (ETS) para la fijación de precios de nuevos productos.

Asia-Pacífico

- Cuota de mercado: Se ha identificado como la región de mayor crecimiento, impulsada por los cambios en los estilos de vida y la modernización de los sistemas de atención médica en China, Japón e India.

-

Factores clave:

- Aumento del gasto sanitario: Inversiones gubernamentales masivas en infraestructuras hospitalarias inteligentes y centros oncológicos especializados para dar cabida al creciente volumen de pacientes.

- Mejorar la alfabetización sanitaria: Las crecientes poblaciones de clase media buscan opciones de tratamiento más avanzadas y occidentalizadas, que vayan más allá de la atención básica genérica.

- Expansión estratégica del mercado: Los líderes farmacéuticos mundiales están formando cada vez más alianzas locales y acuerdos de licencia para sortear los obstáculos regulatorios regionales.

- Tendencias: Gran dependencia de las plataformas de comercio electrónico para la distribución de medicamentos especializados y un aumento considerable de los contratos B2B para la producción de terapias oncológicas avanzadas.

América del Sur y Central

- Cuota de mercado: Un mercado emergente con un sector especializado en crecimiento en países como Brasil, Argentina y Chile.

-

Factores clave:

- Modernización de los centros sanitarios: Transición de los sistemas básicos de salud pública a redes especializadas de oncología en los principales centros urbanos.

- Mayor concienciación sobre el diagnóstico precoz: Aumento de las campañas de salud digital que fomentan los controles periódicos de la salud de la próstata entre los hombres mayores de 50 años.

- Adopción de la dieta mediterránea y cambios en el estilo de vida: creciente interés por el bienestar integral y la atención preventiva entre los segmentos urbanos de altos ingresos.

- Tendencias: Crecimiento de las clínicas oncológicas especializadas y la introducción gradual de terapias dirigidas avanzadas a medida que se simplifican los procesos regulatorios locales.

Oriente Medio y África

- Cuota de mercado: Un mercado en desarrollo centrado en la transición de los modelos sanitarios tradicionales a la producción comercial formalizada y de alta tecnología.

-

Factores clave:

- Enfoque gubernamental en el turismo médico: Inversiones estratégicas en ciudades sanitarias (en particular en el CCG) para brindar tratamientos oncológicos de primer nivel a nivel local.

- Alta demanda de formulaciones de acción prolongada: Preferencia por terapias hormonales inyectables estables y de acción prolongada, adecuadas para diversos climas regionales.

- Agricultura inteligente y nutrición: Implementación de tecnologías sanitarias modernas para mejorar la seguridad alimentaria local y los estándares nutricionales para pacientes con cáncer.

- Tendencias: Implementación de tecnologías modernas de cadena de frío y refrigeración para formalizar la entrega de medicamentos oncológicos sensibles a la temperatura y suplementos pediátricos/geriátricos con alto contenido nutricional.

Alta densidad de mercado y competencia

La competencia se intensifica debido a la presencia de líderes consolidados como Johnson & Johnson, Astellas Pharma, Bayer y Novartis. Empresas biotecnológicas especializadas y fabricantes regionales de genéricos también contribuyen a un panorama diverso y en rápida expansión.

Este entorno competitivo impulsa a los proveedores a diferenciarse a través de:

- Validación de regímenes combinados: Demostrar que el uso de múltiples agentes (por ejemplo, terapia hormonal y dirigida) supera significativamente a la monoterapia.

- Precision Companion Diagnostics: Desarrollo de kits de prueba patentados que identifican a los pacientes con mayor probabilidad de responder a un medicamento específico de alto costo.

- Resiliencia de la cadena de suministro: especialmente en el caso de los radiofármacos, donde la corta vida media de los isótopos requiere una logística altamente coordinada y justo a tiempo.

Oportunidades y movimientos estratégicos

- Adquisiciones estratégicas de plataformas biotecnológicas: Las grandes empresas están adquiriendo compañías más pequeñas con plataformas patentadas de degradación de proteínas o de activación de células T para renovar sus carteras de productos en fases avanzadas.

- Implementación de evidencia del mundo real (RWE, por sus siglas en inglés): Utilización de datos de la práctica clínica para respaldar la ampliación de las indicaciones y demostrar la seguridad a largo plazo ante los organismos reguladores y las aseguradoras.

Las principales empresas que operan en el mercado de terapias para el cáncer de próstata son:

- Astella Pharma Inc.

- Johnson & Johnson Services Inc

- Eli Lilly y Compañía

- Bayer AG

- Sanofi

- Merck KGaA

- AstraZeneca

- Novartis AG

- AbbVie

- Bristol Myers Squibb

Descargo de responsabilidad: Las empresas mencionadas anteriormente no están clasificadas en ningún orden en particular.

Noticias y novedades recientes del mercado de tratamientos para el cáncer de próstata

- En diciembre de 2025, Johnson & Johnson completó la adquisición de Halda Therapeutics OpCo, Inc. por 3050 millones de dólares en efectivo. Mediante esta estrategia, la compañía integró la plataforma patentada RIPTAC™ (Regulated Induced Proximity TArgeting Chimera) de Halda para fortalecer su cartera de tratamientos orales dirigidos. Esta adquisición consolidó significativamente el liderazgo mundial de la compañía en el mercado de terapias para el cáncer de próstata al incorporar candidatos innovadores en fase clínica diseñados para combatir la resistencia al tratamiento en tumores sólidos.

- En junio de 2025, Bayer anunció que la Administración de Alimentos y Medicamentos de los Estados Unidos (FDA) aprobó su inhibidor oral del receptor de andrógenos, NUBEQA® (darolutamida), para el tratamiento de pacientes adultos con cáncer de próstata metastásico sensible a la castración (mCSPC). Esta importante expansión en el mercado de terapias para el cáncer de próstata se produjo tras los resultados positivos del ensayo pivotal de fase III ARANOTE, que demostró que NUBEQA más terapia de privación de andrógenos (TPA) redujo el riesgo de progresión radiográfica o muerte en un 46 % en comparación con un placebo más TPA.

Cobertura y entregables del informe de mercado de terapias para el cáncer de próstata

El informe "Tamaño y pronóstico del mercado de terapias para el cáncer de próstata (2021-2034)" proporciona un análisis detallado del mercado que abarca las siguientes áreas:

- Tamaño y pronóstico del mercado de terapias para el cáncer de próstata a nivel mundial, regional y nacional para todos los segmentos clave del mercado cubiertos en el alcance.

- Tendencias del mercado de terapias para el cáncer de próstata, así como la dinámica del mercado, tales como factores impulsores, limitaciones y oportunidades clave.

- Análisis detallado PEST y FODA

- Análisis del mercado de terapias para el cáncer de próstata, que abarca las principales tendencias del mercado, el marco global y regional, los principales actores, las regulaciones y los desarrollos recientes del mercado.

- Análisis del panorama de la industria y de la competencia, que abarca la concentración del mercado, el análisis de mapas de calor, los principales actores y los desarrollos recientes en el mercado de terapias para el cáncer de próstata.

- Perfiles detallados de las empresas

Mrinal es una experimentada analista de investigación con más de 8 años de experiencia en inteligencia de mercado y consultoría en ciencias de la vida. Con una mentalidad estratégica y un firme compromiso con la excelencia, ha desarrollado una amplia experiencia en pronósticos farmacéuticos, evaluación de oportunidades de mercado y desarrollo de indicadores de referencia para la industria. Su trabajo se centra en brindar información práctica que permita a los clientes tomar decisiones estratégicas informadas.

La principal fortaleza de Mrinal reside en convertir conjuntos de datos cuantitativos complejos en inteligencia de negocios significativa. Su perspicacia analítica es fundamental para definir estrategias de salida al mercado (GTM) y descubrir oportunidades de crecimiento en los sectores farmacéutico y de dispositivos médicos. Como consultora de confianza, se centra constantemente en optimizar los procesos de flujo de trabajo y establecer las mejores prácticas, impulsando así la innovación y la eficiencia operativa para sus clientes.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias