Demanda, tendencias y pronóstico del mercado de gestión de activos de software para 2034

Tamaño y pronóstico del mercado de gestión de activos de software (2021-2034), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por componente (soluciones y servicios), tipo de implementación (local y en la nube), tamaño de la organización (pymes y grandes empresas) y sector vertical (servicios financieros, TI y telecomunicaciones, manufactura, comercio minorista y bienes de consumo, gobierno, atención médica y ciencias de la vida, medios de comunicación y entretenimiento, y otros).

- Estado : Datos publicados

- Código de informe : TIPRE00012382

- Categoría : Tecnología, medios y telecomunicaciones

- Número de páginas : 150

- Formatos de informe disponibles :

- Fecha de última actualización : March 17, 2026

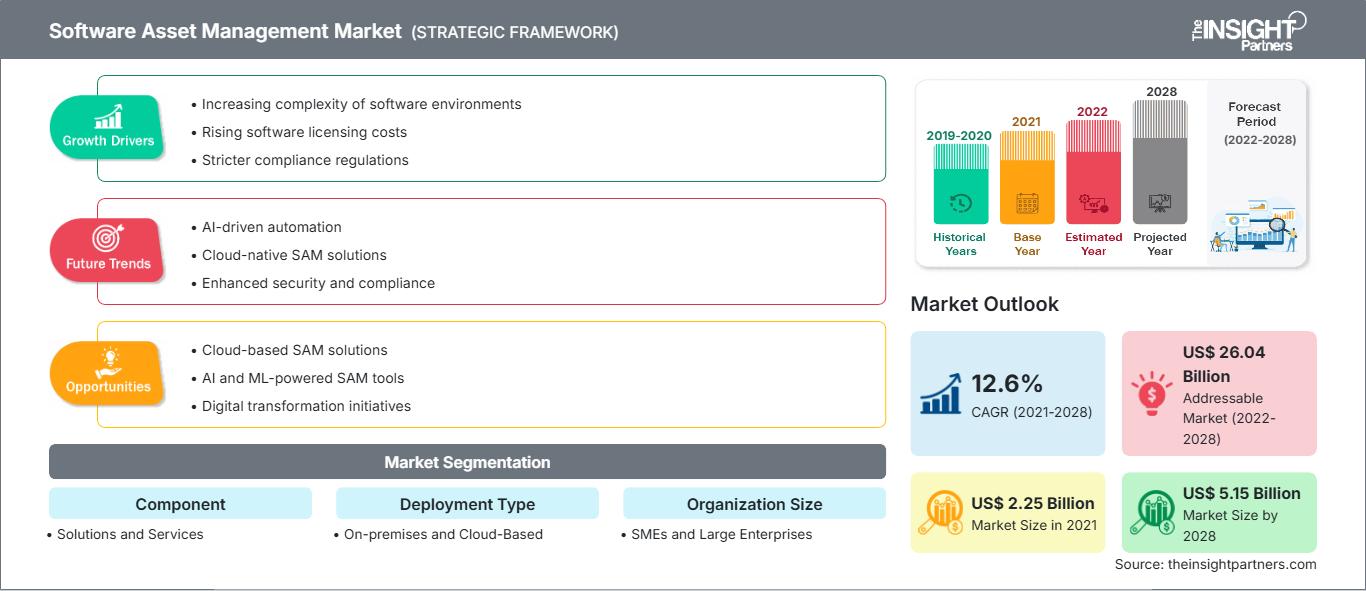

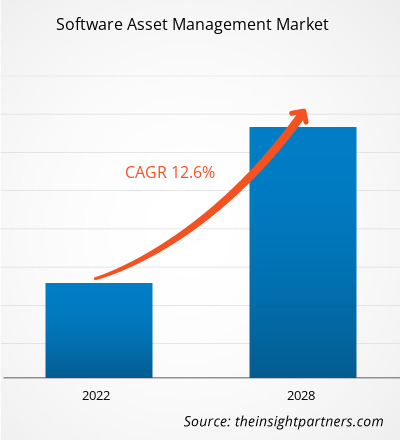

Se prevé que el mercado global de gestión de activos de software alcance los 8.500 millones de dólares estadounidenses en 2034, frente a los 2.800 millones de dólares estadounidenses en 2025. Se espera que el mercado registre una tasa de crecimiento anual compuesta (CAGR) del 13,88 % durante el período de pronóstico 2026-2034.

Entre las principales dinámicas del mercado se incluyen la creciente complejidad de las infraestructuras de TI híbridas y multinube, las normativas de cumplimiento más estrictas de los principales proveedores de software y un mayor enfoque corporativo en la reducción de desperdicios y la optimización del gasto en TI. Además, se espera que el mercado se beneficie de la integración de la inteligencia artificial para el modelado predictivo de licencias, la rápida expansión de los modelos de entrega basados en SaaS y la creciente convergencia de la gestión de activos de software con la ciberseguridad para mitigar las vulnerabilidades en la cadena de suministro de software.

Análisis del mercado de gestión de activos de software

El análisis del mercado de gestión de activos de software muestra un cambio estratégico: de una defensa reactiva ante auditorías a una optimización de costes proactiva basada en IA. El mercado apunta a una gestión de licencias tradicional en las instalaciones para sistemas heredados y a una gestión SaaS de alto crecimiento para empresas nativas de la nube. Están surgiendo oportunidades estratégicas en segmentos especializados como FinOps y la detección de TI en la sombra, donde la mayor complejidad de las compras de software descentralizadas, en comparación con las centralizadas, ofrece una clara ventaja competitiva para las herramientas automatizadas avanzadas. El análisis también señala que la expansión del mercado depende de una integración perfecta con las plataformas de gestión de servicios de TI y de la precisión de los datos en tiempo real para la asignación de licencias. La diferenciación competitiva ahora destaca por una marca que resalta la detección automatizada, el manejo ético de datos y la capacidad de rastrear el uso del software desde su implementación hasta su retirada. Este enfoque permite a los proveedores de software cobrar precios más altos en un mercado con numerosos proveedores de servicios especializados.

Descripción general del mercado de gestión de activos de software

Las soluciones de gestión de activos de software han evolucionado desde herramientas administrativas especializadas hasta productos de gobernanza estratégica de uso generalizado. La gestión de activos de software incluye la conciliación automatizada de licencias, la optimización de costes en la nube y módulos de preparación para auditorías. Tanto las empresas tecnológicas globales como las startups especializadas compiten en este mercado, utilizando modelos de entrega como instalaciones locales y suscripciones en la nube. La creciente demanda de transformación digital entre las empresas de Norteamérica y Europa, centradas en la salud y la eficiencia, ha impulsado la popularidad de la gestión de activos de software como una solución fundamental para la mitigación de riesgos. Norteamérica lidera en ingresos gracias a su consolidada cultura de cumplimiento corporativo, mientras que Asia-Pacífico avanza en la adopción digital y la innovación en el sector minorista. El mercado estadounidense es el más desarrollado, impulsado por las frecuentes auditorías de software y la amplia disponibilidad de plataformas de gestión avanzadas. La competencia entre marcas fomenta una mayor variedad de funcionalidades y la inclusión de análisis avanzados como la previsión predictiva y la corrección automatizada.

Personaliza este informe para adaptarlo a tus necesidades.

Obtén PERSONALIZACIÓN GRATUITAMercado de gestión de activos de software: Perspectivas estratégicas

-

Descubra las principales tendencias del mercado que se recogen en este informe.Esta muestra GRATUITA incluirá análisis de datos, que abarcan desde tendencias de mercado hasta estimaciones y pronósticos.

Factores impulsores y oportunidades del mercado de gestión de activos de software

Factores que impulsan el mercado:

- Mayor complejidad y entornos de TI híbridos: Las empresas operan en diversas plataformas, incluyendo entornos locales, SaaS y nubes públicas. Esta complejidad dificulta el seguimiento manual del uso, lo que impulsa la necesidad de soluciones automatizadas.

- Auditorías más estrictas a proveedores y mayor presión para el cumplimiento normativo: Los principales proveedores de software están intensificando las auditorías para recuperar ingresos. Las herramientas de gestión de activos de software ofrecen la visibilidad necesaria para evitar fuertes sanciones por incumplimiento y riesgos legales.

- Optimización de los presupuestos de TI: A medida que los costes del software representan una mayor proporción de los gastos operativos, las organizaciones utilizan estas herramientas para identificar el software que no se utiliza y eliminar las suscripciones no utilizadas con el fin de mejorar la eficiencia financiera.

Oportunidades de mercado:

- Expansión hacia los servicios gestionados para pymes: Más allá de las grandes empresas, existe una importante oportunidad para proporcionar servicios de gestión de activos de software a pequeñas y medianas empresas que carecen de experiencia interna.

- Integración con marcos de ciberseguridad: La gestión de los activos de software ofrece oportunidades para mejorar la seguridad mediante la identificación del software que ha llegado al final de su ciclo de vida y garantizando que todas las aplicaciones estén actualizadas y autorizadas.

- Análisis predictivo impulsado por IA: Existe una creciente oportunidad para que los proveedores se dirijan a industrias específicas mediante funciones de IA que predicen las necesidades futuras de software y sugieren niveles de licencia óptimos basados en datos históricos.

Análisis de segmentación del informe de mercado de gestión de activos de software

Se analiza la cuota de mercado de la gestión de activos de software en diversos segmentos para comprender mejor su estructura, potencial de crecimiento y tendencias emergentes. A continuación, se muestra el enfoque de segmentación estándar utilizado en los informes del sector:

Por componente:

- Soluciones: El principal motor de volumen, incluidas las plataformas para la gestión de licencias, el descubrimiento y el seguimiento del inventario, se beneficia de las cadenas de suministro empresariales ya establecidas.

- Servicios: Un nicho de mercado en rápido crecimiento que responde a la necesidad de experiencia especializada en defensa ante auditorías y consultoría estratégica para negociaciones complejas con proveedores.

Por tipo de despliegue:

- Basado en la nube: El segmento de mayor crecimiento, especialmente para la gestión de la proliferación de SaaS y los entornos de trabajo remoto, que permite una visibilidad en tiempo real de las operaciones globales.

- En las instalaciones del cliente: Sigue siendo un canal principal para industrias altamente reguladas como el gobierno y el sector bancario y financiero, que priorizan la soberanía de los datos y el control local.

Por tamaño de organización:

- Grandes empresas: Poseen la mayor cuota de mercado debido a sus enormes carteras de software y al alto riesgo financiero asociado al incumplimiento normativo.

- Pymes: Se prevé que registren la mayor tasa de crecimiento, ya que las empresas más pequeñas reconocen los beneficios del control de costes y abandonan el seguimiento manual.

Por sector industrial:

- BFSI: Sector líder debido a los intensos requisitos regulatorios y a la necesidad de gestionar ecosistemas de software financiero complejos.

- Informática y telecomunicaciones: Segmento de alto volumen que aprovecha la gestión de activos de software para optimizar vastos inventarios de software y respaldar la entrega rápida de servicios.

- Fabricación: Se centra en la optimización de la infraestructura de TI y la integración de la gestión de software con los sistemas de automatización industrial.

- Comercio minorista y bienes de consumo: Impulsado por la necesidad de gestionar plataformas de comercio electrónico y software de punto de venta, al tiempo que se optimizan las herramientas de experiencia del cliente.

- Gobierno: Implementar marcos para garantizar la transparencia en las inversiones en software financiadas con los contribuyentes y la visibilidad de los departamentos gubernamentales.

- Sector sanitario y ciencias de la vida: Creciente demanda de gestión de software médico crítico y garantía del cumplimiento de la normativa de protección de datos.

- Medios de comunicación y entretenimiento: Gran énfasis en sistemas eficientes de gestión de contenidos y gestión de derechos digitales.

Por geografía:

- América del norte

- Europa

- Asia Pacífico

- América del Sur y Central

- Oriente Medio y África

Alcance del informe de mercado de gestión de activos de software

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2025 | 2.800 millones de dólares estadounidenses |

| Tamaño del mercado para 2034 | 8.500 millones de dólares estadounidenses |

| Tasa de crecimiento anual compuesta global (2026 - 2034) | 13,88% |

| Datos históricos | 2021-2024 |

| Período de pronóstico | 2026-2034 |

| Segmentos cubiertos |

Por componente

|

| Regiones y países incluidos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de los actores del mercado de gestión de activos de software: comprender su impacto en la dinámica empresarial.

El mercado de gestión de activos de software está experimentando un rápido crecimiento, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor concienciación sobre los beneficios del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

Análisis de la cuota de mercado de la gestión de activos de software por región geográfica

Se prevé que la región de Asia-Pacífico experimente el mayor crecimiento en los próximos años. Los mercados emergentes de América del Sur y Central, Oriente Medio y África también ofrecen numerosas oportunidades sin explotar para la expansión de proveedores de software de gestión de alta gama y empresas de servicios gestionados.

El mercado de gestión de activos de software está experimentando una transformación significativa, pasando de ser una función administrativa a una prioridad estratégica global. El crecimiento se ve impulsado por la creciente prevalencia del SaaS, el aumento del gasto en la nube y la expansión de la gobernanza digital. A continuación, se presenta un resumen de la cuota de mercado y las tendencias por región:

1. América del Norte

- Cuota de mercado: Posee la mayor cuota a nivel mundial, impulsada por un entorno de TI maduro y una alta concentración de sedes de empresas Fortune 500.

-

Factores clave:

- Creciente preferencia empresarial por los marcos de trabajo FinOps para gestionar el gasto en software nativo de la nube.

- Generalización de una gobernanza centrada en el cumplimiento normativo en sectores de alta gama como el financiero y el sanitario.

- Ciclos de auditoría de proveedores más estrictos y una alta adopción a nivel nacional de herramientas de descubrimiento avanzadas basadas en inteligencia artificial.

- Tendencias: La expansión de las plataformas de gestión SaaS y la adopción exitosa de las normas ISO 19770-1 para atraer a las partes interesadas centradas en la gobernanza.

2. Europa

- Cuota de mercado: Posee una cuota significativa, sustentada en ecosistemas regulatorios arraigados y estrictas normativas de protección de datos como el RGPD.

-

Factores clave:

- Alta demanda de soberanía de datos y gestión localizada de activos en Alemania, Francia y el Reino Unido.

- Infraestructura de procesamiento establecida para la conciliación de licencias tradicionales en las instalaciones.

- Gran énfasis en las tecnologías de la información y la sostenibilidad, con especial atención al consumo energético del software.

- Tendencias: Un cambio estratégico hacia la priorización de la gestión de activos de software (SAM) nativa de la nube para administrar ecosistemas híbridos, con un enfoque cada vez mayor en los servicios gestionados para superar la escasez de mano de obra cualificada a nivel local.

3. Asia-Pacífico

- Cuota de mercado: La región de mayor crecimiento, con India y China como principales impulsores de la adopción digital y la migración a la nube.

-

Factores clave:

- Existe una enorme base de consumidores en el sudeste asiático que buscan infraestructura de software como servicio (SaaS) y aplicaciones móviles premium y localizadas.

- Las iniciativas gubernamentales de la India digital y las ciudades inteligentes se centraron en software de gobernanza de alto valor.

- La rápida urbanización ha propiciado una preferencia por el software empresarial, los aperitivos y las herramientas de estilo occidental.

- Tendencias: Gran dependencia de los contratos SAM y B2B con enfoque móvil para el análisis avanzado de datos en los sectores de manufactura y tecnología financiera.

4. América del Sur y Central

- Cuota de mercado: Mercado emergente con un sector de TI artesanal en auge en países como Brasil y Chile.

-

Factores clave:

- Aumentar la concienciación sobre la superioridad operativa de SAM para la resiliencia de las empresas medianas.

- Modernización de los departamentos informáticos locales para convertirlos en centros digitales de nivel comercial que den servicio a los centros urbanos.

- Tendencias: Crecimiento de los proveedores de servicios gestionados especializados y la introducción de la gestión de activos de software localizada para cadenas minoristas regionales.

5. Oriente Medio y África

- Cuota de mercado: Mercado en desarrollo con profundas raíces en la gestión local de recursos, en transición hacia la producción comercial formalizada de TI.

-

Factores clave:

- Presencia tradicional de la gestión de software y de las prácticas financieras regionales.

- Inversiones estratégicas en la transformación digital del sector público.

- Tendencias: Implementación de técnicas modernas de extracción de datos, mediante el descubrimiento automatizado y la eliminación de código no conforme, para formalizar el mercado informal de software.

Alta densidad de mercado y competencia

La competencia se intensifica debido a la presencia de líderes consolidados como Flexera, ServiceNow y Snow Software. Expertos regionales y empresas especializadas como Certero y Aspera, junto con innovadores como Zylo y BetterCloud, también contribuyen a un panorama diverso y en rápida expansión.

Este entorno competitivo impulsa a los proveedores a diferenciarse a través de:

- Imagen de marca funcional: Posicionar la gestión de activos de software como una herramienta superior de gestión de riesgos, haciendo hincapié en su papel en la ciberseguridad y la recuperación de costes.

- Diversificación de productos: Ofrecemos más que solo el seguimiento de licencias, incluyendo la monitorización de un entorno de TI saludable al estilo probiótico y la remediación automatizada de alta gama.

- Control de la cadena de suministro: Gestionar todo el ciclo de vida, desde la adquisición hasta la eliminación, para garantizar la calidad y cumplir con los estándares éticos.

Oportunidades y movimientos estratégicos

- Asóciate con plataformas de FinOps y seguridad: Aprovecha la creciente demanda de gestión integrada de costes y seguridad en los mercados de Asia-Pacífico y Norteamérica.

- Incorporar IA y optimización autónoma: atraer a los millennials y a los líderes de la Generación Z, conscientes del medio ambiente y de las finanzas, que buscan alternativas digitales éticas y fáciles de configurar.

Las principales empresas que operan en el mercado de gestión de activos de software son:

- Corporación Microsoft

- IVANTI

- SOFTWARE DE NIEVE

- BMC SOFTWARE, INC.

- CERTERO

- FLEXERA

- Corporación IBM

- MICRO ENFOQUE

- SERVICIO AHORA

- BROADCOM, INC.

Descargo de responsabilidad: Las empresas mencionadas anteriormente no están clasificadas en ningún orden en particular.

Noticias y novedades del mercado de gestión de activos de software

- En enero de 2026, IBM anunció IBM Sovereign Core, el primer software del sector preparado para IA y con capacidad de soberanía, diseñado para que empresas, gobiernos y proveedores de servicios construyan, implementen y administren entornos soberanos preparados para IA. Organizaciones de todo el mundo se enfrentan a la creciente necesidad de ejercer control sobre su infraestructura tecnológica. Impulsadas por la evolución de las normativas y la necesidad de una gobernanza auditable, las empresas y los gobiernos buscan entornos autogestionados donde mantengan una autoridad operativa completa, especialmente al implementar cargas de trabajo de IA que intensifican las preocupaciones sobre la soberanía.

- En julio de 2025, Flexera anunció el lanzamiento de Flexera One SaaS Management, la solución más completa del sector para el descubrimiento, la optimización y el control de SaaS. Esta solución de última generación combina las ventajas de las aplicaciones de gestión de SaaS de Flexera y Snow, lo que permite a las organizaciones obtener una visibilidad completa de las aplicaciones SaaS y las herramientas de IA, ahorrar costes y mitigar riesgos.

Cobertura y entregables del informe de mercado de gestión de activos de software

El informe "Tamaño y pronóstico del mercado de gestión de activos de software (2021-2034)" proporciona un análisis detallado del mercado que abarca las siguientes áreas:

- Tamaño y pronóstico del mercado de gestión de activos de software a nivel global, regional y nacional para todos los segmentos clave del mercado cubiertos en el alcance.

- Tendencias del mercado de gestión de activos de software, así como dinámicas del mercado como factores impulsores, limitaciones y oportunidades clave.

- Análisis detallado PEST y FODA

- Análisis del mercado de gestión de activos de software que abarca las principales tendencias del mercado, el marco global y regional, los principales actores, las regulaciones y los desarrollos recientes del mercado.

- Análisis del panorama de la industria y de la competencia, que abarca la concentración del mercado, el análisis de mapas de calor, los principales actores y los desarrollos recientes en el mercado de gestión de activos de software.

- Perfiles detallados de las empresas

Ankita es una profesional dinámica en investigación de mercados y consultoría con más de 8 años de experiencia en los sectores de tecnología, medios de comunicación, TIC, electrónica y semiconductores. Ha liderado y ejecutado con éxito más de 100 proyectos de consultoría e investigación para clientes globales como Microsoft, Oracle, NEC Corporation, SAP, KPMG y Expeditors International. Sus principales competencias incluyen la evaluación de mercado, el análisis de datos, la previsión, la formulación de estrategias, la inteligencia competitiva y la redacción de informes.

Ankita es experta en la gestión de ciclos completos de proyecto, desde el diseño de propuestas de preventa y las conversaciones con los clientes hasta la entrega de información práctica posventa. Es experta en la gestión de equipos multifuncionales, la estructuración de módulos de investigación complejos y la alineación de soluciones con los objetivos de negocio específicos del cliente. Sus excelentes habilidades de comunicación, liderazgo y presentación le han permitido obtener constantemente resultados orientados al valor en entornos de mercado dinámicos y en constante evolución.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias