Tamaño, crecimiento y tendencias del mercado de vidrio ultrafino hasta 2034

Tamaño del mercado de vidrio ultrafino y pronósticos (2021–2034), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por proceso de fabricación (flotación y fusión), aplicación (sustrato de semiconductores, pantallas planas y dispositivos de control táctil, acristalamiento automotriz y otros), industria de uso final (electrónica de consumo, automoción, medicina y atención médica y otros) y geografía.

- Estado : Datos publicados

- Código de informe : TIPRE00009965

- Categoría : Productos químicos y materiales

- Número de páginas : 150

- Formatos de informe disponibles :

- Fecha de última actualización : June 11, 2026

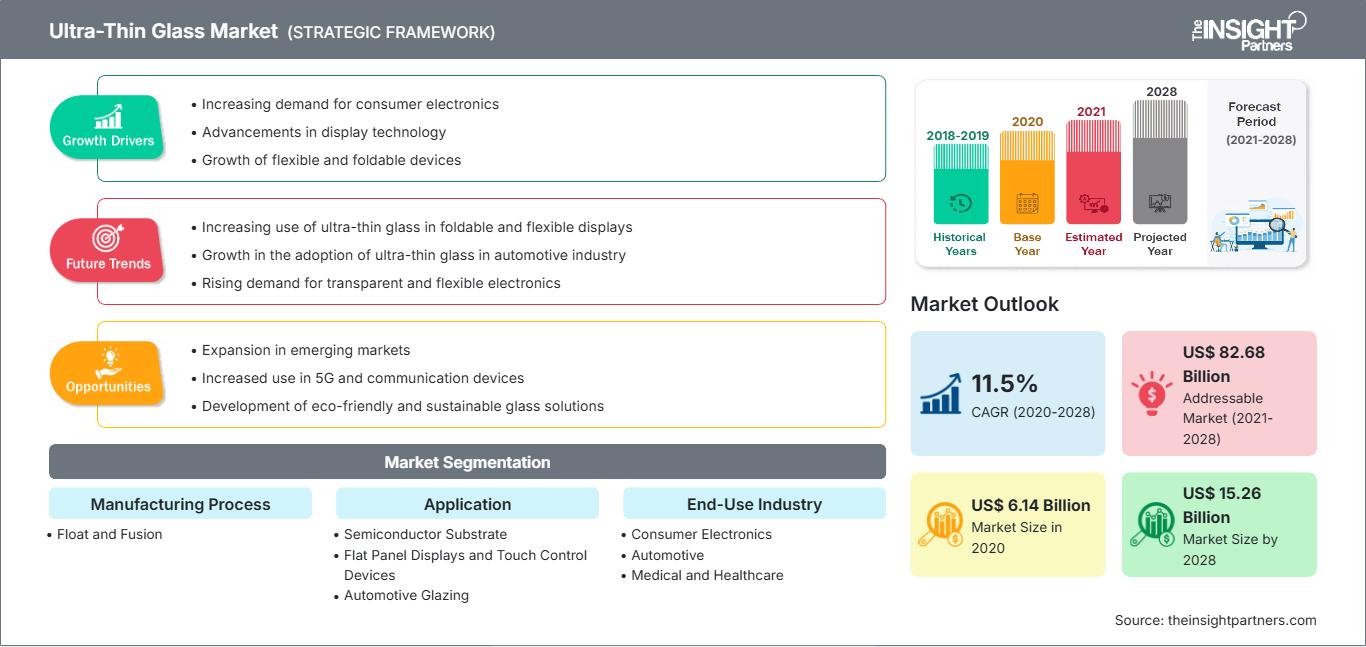

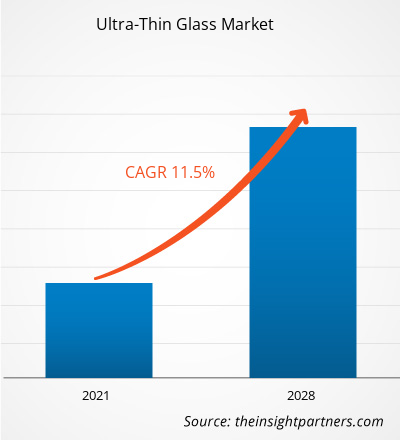

Se prevé que el mercado mundial de vidrio ultrafino alcance los 55.850 millones de dólares estadounidenses en 2034, frente a los 23.440 millones de dólares estadounidenses de 2025. Se espera que el mercado registre una tasa de crecimiento anual compuesta (CAGR) del 10,13 % durante el período de previsión 2026-2034.

Entre las principales dinámicas del mercado se incluyen un mayor interés global en componentes electrónicos ligeros y de alto rendimiento, una mayor concienciación de los consumidores sobre la durabilidad y resistencia a los arañazos superiores del vidrio frente a los polímeros plásticos, y un cambio significativo hacia arquitecturas de dispositivos plegables y flexibles. Además, se prevé que el mercado se beneficie de la creciente popularidad de los vehículos eléctricos con cabinas inteligentes integradas, la expansión de los requisitos de encapsulado de semiconductores para hardware 5G e IA, y la creciente incorporación de vidrio ultrafino en segmentos médicos de alto valor, como biosensores de diagnóstico y monitores de salud portátiles.

Análisis del mercado del vidrio ultrafino

El análisis del mercado de vidrio ultrafino muestra una tendencia hacia sustratos funcionales de alto valor, ya que los fabricantes priorizan la claridad óptica y la flexibilidad mecánica. El mercado se está diversificando hacia los sectores tradicionales de automoción y pantallas, basados en la tecnología de flotación, y hacia los mercados de alto crecimiento de estirado por fusión para electrónica plegable de alta gama. Están surgiendo oportunidades estratégicas en aplicaciones especializadas de semiconductores y biotecnología, donde la estabilidad térmica y la resistencia química superiores del vidrio ultrafino, en comparación con las alternativas orgánicas, ofrecen una clara ventaja competitiva. La expansión del mercado depende de la gestión del rendimiento durante el corte de precisión y de la integridad de los sistemas de manipulación automatizados para láminas ultrafrágiles. La diferenciación competitiva ahora destaca gracias a técnicas de refuerzo patentadas, como el templado químico por intercambio iónico, y la capacidad de proporcionar recubrimientos multifuncionales para la protección antirreflectante y contra las huellas dactilares. Este enfoque permite a los fabricantes de vidrio de primer nivel fijar precios más altos en un mercado que exige una precisión técnica extrema.

Panorama general del mercado del vidrio ultrafino

El vidrio ultrafino ha evolucionado desde aplicaciones de laboratorio especializadas hasta productos industriales de alta tecnología de uso generalizado. El mercado abarca vidrio de cubierta ultraflexible para teléfonos inteligentes, sustratos de alta frecuencia para el encapsulado de chips y acristalamiento ligero para las industrias aeroespacial y automotriz. Tanto los conglomerados globales de vidrio como las empresas especializadas en ciencia de materiales compiten en este mercado, utilizando técnicas de fabricación avanzadas para producir vidrio más delgado que un cabello humano. La creciente demanda de dispositivos electrónicos más elegantes y portátiles entre los consumidores expertos en tecnología de Asia-Pacífico y Norteamérica ha incrementado la popularidad del vidrio ultrafino como una solución de protección e interfaz de primera calidad. Asia-Pacífico lidera en ingresos debido a su consolidado centro de fabricación de productos electrónicos, mientras que Norteamérica avanza en aplicaciones aeroespaciales e innovación en dispositivos médicos. El mercado global está más desarrollado en regiones con altas concentraciones de producción de paneles de visualización, impulsado por la amplia disponibilidad de tecnologías OLED y Micro-LED. La competencia entre marcas está impulsando una mayor innovación en la composición del vidrio, lo que lleva a la inclusión de variantes especializadas de aluminosilicato y borosilicato. El mercado estadounidense es un centro neurálgico para la innovación en materiales, impulsado por un sólido ecosistema de semiconductores y una alta concentración de gigantes de la electrónica de consumo. La demanda interna se centra cada vez más en formatos plegables y en el empaquetado avanzado de semiconductores. Las inversiones estratégicas en instalaciones de fabricación locales están impulsando la adopción de sustratos de vidrio de alta precisión.

Personaliza este informe para adaptarlo a tus necesidades.

Obtén PERSONALIZACIÓN GRATUITAMercado del vidrio ultrafino: Perspectivas estratégicas

-

Descubra las principales tendencias del mercado que se recogen en este informe.Esta muestra GRATUITA incluirá análisis de datos, que abarcan desde tendencias de mercado hasta estimaciones y pronósticos.

Factores impulsores y oportunidades del mercado del vidrio ultrafino

Factores que impulsan el mercado:

- Rendimiento óptico y mecánico superior: El vidrio ultrafino ofrece mayor transparencia y una sensación táctil más refinada que las películas de plástico. Su resistencia al calor y a los productos químicos lo hace ideal para los rigurosos procesos de fabricación de las modernas pantallas de alta definición.

- Generalización de los formatos plegables: La expansión de la categoría de teléfonos inteligentes y portátiles plegables ha mantenido una alta demanda de componentes de vidrio flexible. A medida que los consumidores optan por dispositivos flexibles, el vidrio ultrafino continúa experimentando un crecimiento constante en volumen en comparación con las poliimidas plásticas.

- Expansión acelerada de las tecnologías 5G y de semiconductores: La transmisión de datos de alta frecuencia requiere sustratos con bajas pérdidas dieléctricas. El vidrio ultrafino se utiliza cada vez más en el encapsulado avanzado de semiconductores para dar soporte a la infraestructura de 5G y la computación de alta velocidad.

Oportunidades de mercado:

- Expansión hacia el acristalamiento automotriz y los interiores inteligentes: más allá de los dispositivos portátiles, el vidrio ultrafino ofrece importantes oportunidades en ventanas ligeras y pantallas curvas de gran tamaño para el salpicadero de los vehículos eléctricos de próxima generación.

- Crecimiento en los segmentos médico y biotecnológico: La formación de alianzas estratégicas entre fabricantes de vidrio y empresas de dispositivos médicos puede facilitar el acceso a segmentos de alto margen en el diagnóstico en el punto de atención, donde el vidrio ultrafino sirve como sustrato estable para chips microfluídicos.

- Diversificación hacia la energía sostenible: Existe una creciente oportunidad para que los productores se dirijan al sector de las energías renovables mediante el uso de vidrio ligero y flexible para sistemas fotovoltaicos integrados en edificios (BIPV) y cargadores solares portátiles.

Análisis de segmentación del informe de mercado de vidrio ultrafino

La cuota de mercado del vidrio ultrafino se analiza en diversos segmentos para comprender mejor su estructura, potencial de crecimiento y tendencias emergentes. A continuación, se muestra el enfoque de segmentación estándar utilizado en la mayoría de los informes del sector:

Por proceso de fabricación:

- Vidrio flotante: El principal motor de volumen, especialmente en los sectores de acristalamiento para automóviles y pantallas de gran formato, debido a la capacidad de producción en grandes volúmenes ya establecida y a la eficiencia en costes de producción de vidrios con espesores de hasta 0,1 mm.

- Fusión: Un segmento técnico de rápido crecimiento que produce vidrio con una calidad superficial y un control de espesor superiores. Cada vez se prefiere más para aplicaciones electrónicas de alta gama donde se requieren superficies impecables y sensibles al tacto sin necesidad de pulido adicional.

Mediante solicitud:

- Pantallas planas y dispositivos de control táctil: Sigue siendo el principal canal para el uso de vidrio ultrafino, beneficiándose de la demanda mundial de teléfonos inteligentes, tabletas y televisores de gama alta.

- Sustrato semiconductor: El segmento de aplicación de mayor crecimiento, especialmente para el empaquetado de chips de alta densidad y los interconectores, lo que permite la creación de componentes electrónicos más compactos y eficientes.

- Cristales para automóviles: Ofrecen una gama selecta pero creciente de aplicaciones para la reducción de peso y la mejora de la estética interior en el diseño de vehículos modernos.

- Otros: Incluye usos especializados en sensores, sustratos biotecnológicos y componentes de energía solar.

Por sector de uso final:

- Electrónica de consumo: El sector más grande, impulsado por el ciclo continuo de miniaturización de los dispositivos y el auge de la tecnología de pantallas plegables.

- Automoción: Un área de crecimiento significativo centrada en la reducción del peso en vacío de los vehículos y la mejora de la digitalización de los habitáculos.

- Medicina y atención sanitaria: Utiliza vidrio ultrafino para herramientas de diagnóstico de alta precisión, portaobjetos de microscopio y sensores médicos portátiles.

- Otros: Abarca la industria aeroespacial, la defensa y la fabricación industrial especializada.

Por geografía:

- América del norte

- Europa

- Asia Pacífico

- América del Sur y Central

- Oriente Medio y África

Alcance del informe de mercado sobre vidrio ultrafino

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2025 | 23.440 millones de dólares estadounidenses |

| Tamaño del mercado para 2034 | 55.850 millones de dólares estadounidenses |

| Tasa de crecimiento anual compuesta global (2026 - 2034) | 10,13% |

| Datos históricos | 2021-2024 |

| Período de pronóstico | 2026-2034 |

| Segmentos cubiertos |

Por proceso de fabricación

|

| Regiones y países incluidos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de los actores del mercado del vidrio ultrafino: comprender su impacto en la dinámica empresarial.

El mercado del vidrio ultrafino está experimentando un rápido crecimiento, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor concienciación sobre los beneficios del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

Análisis de la cuota de mercado del vidrio ultrafino por región geográfica

Se prevé que la región de Asia-Pacífico experimente el mayor crecimiento en los próximos años. Los mercados emergentes de Norteamérica y Europa también presentan numerosas oportunidades sin explotar para aplicaciones de vidrio de alta calidad en los sectores médico y automotriz.

El mercado del vidrio ultrafino está experimentando una transformación significativa, pasando de ser un componente electrónico especializado a un material versátil de alta tecnología. El crecimiento se ve impulsado por el aumento de la demanda de electrónica flexible y la expansión del sector automotriz de alta gama. A continuación, se presenta un resumen de la cuota de mercado y las tendencias por región:

1. América del Norte

- Cuota de mercado: Un segmento de nicho, pero en rápida expansión, impulsado por la temprana adopción de dispositivos plegables y aplicaciones aeroespaciales de alta gama.

-

Factores clave:

- Fuerte presencia de pioneros tecnológicos globales y un mercado consolidado de teléfonos inteligentes de lujo.

- Creciente demanda de interconectores de vidrio en el empaquetado de semiconductores impulsado por IA.

- Expansión de los sectores médico y de diagnóstico que requieren sustratos de vidrio de alta pureza.

- Tendencias: Importante inversión en aplicaciones biotecnológicas y la generalización del uso de vidrio ultrafino reforzado para dispositivos portátiles militares e industriales.

2. Europa

- Cuota de mercado: Posee una cuota sustancial, impulsada principalmente por la industria automotriz de élite de la región y el sector del vidrio arquitectónico sostenible.

-

Factores clave:

- Alta demanda de cristales ligeros y aerodinámicos por parte de los gigantes de la automoción en Alemania y Francia.

- Marco de investigación y desarrollo establecido para energías renovables y materiales de construcción energéticamente eficientes.

- Las estrictas normativas medioambientales están impulsando la reducción de peso en el transporte.

- Tendencias: Un enfoque estratégico en los principios de la economía circular, priorizando la reciclabilidad del vidrio delgado y su integración en sistemas fotovoltaicos integrados en edificios (BIPV).

3. Asia-Pacífico

- Cuota de mercado: Posee la mayor cuota a nivel mundial, gracias a los clústeres de fabricación de productos electrónicos más importantes del mundo en China, Corea del Sur, Taiwán y Japón.

-

Factores clave:

- Gran concentración de instalaciones de producción de paneles OLED y Micro-LED.

- Iniciativas gubernamentales para la autosuficiencia en semiconductores y la infraestructura 5G.

- La rápida urbanización está impulsando la demanda de tecnología de consumo de alta gama y ultradelgada.

- Tendencias: Un cambio estratégico hacia la producción localizada de vidrio ultrafino (UTG) para reducir la dependencia de la cadena de suministro, junto con una intensa inversión en I+D en la fabricación de vidrio para el corte de alto rendimiento.

4. América del Sur y Central

- Cuota de mercado: Mercado emergente con una creciente presencia manufacturera en Brasil y Chile.

-

Factores clave:

- Ampliación de las líneas de montaje para marcas regionales de electrónica de consumo.

- Modernización de la cadena de suministro de la industria automotriz para incluir interfaces interiores digitales.

- Tendencias: Aumento de la importación de láminas de vidrio de alta tecnología para el acabado local de teléfonos inteligentes y un incremento en la producción de sensores industriales especializados.

5. Oriente Medio y África

- Cuota de mercado: Mercado en desarrollo en transición hacia la producción industrial formalizada.

-

Factores clave:

- Inversiones estratégicas en ciudades (por ejemplo, NEOM) que requieren soluciones avanzadas de pantallas y acristalamiento.

- Crecimiento en el sector de la energía solar, en particular en el de los paneles ligeros de alta eficiencia.

- Tendencias: Implementación de modernos centros logísticos y de acabado para reducir la brecha entre la producción asiática y la demanda de EMEA.

Las principales empresas que operan en el mercado del vidrio ultrafino son:

- Corning Incorporated

- AGC Inc.

- Compañía de Vidrio Eléctrico Nippon, Ltd.

- SCHOTT AG

- Compañía Central de Vidrio, Ltd.

- CSG Holding Co., Ltd.

- Emerge Glass

- Compañía de Vidrio laminado Nippon, Ltd.

- Xinyi Glass Holdings Limited

- Compañía de Vidrio de Luoyang, Ltd.

Descargo de responsabilidad: Las empresas mencionadas anteriormente no están clasificadas en ningún orden en particular.

Noticias y novedades del mercado del vidrio ultrafino

- En noviembre de 2025, Alpen High Performance Products (Alpen) anunció una colaboración con Corning Incorporated, una de las empresas líderes mundiales en innovación en vidrio, cerámica y ciencia de los materiales. Gracias a esta colaboración, Alpen utilizará el vidrio Corning® Enlighten™ como panel central ultrafino para sus unidades de vidrio triple y cuádruple, lo que contribuirá a la comercialización de ventanas de última generación en el mercado estadounidense.

- En septiembre de 2025, Nippon Electric Glass Co., Ltd. anunció que su lámina de vidrio ultrafina Dinorex UTG™, diseñada exclusivamente para el refuerzo químico, se ha adoptado para la cubierta de la pantalla principal interna del último teléfono inteligente plegable de HONOR, el Magic V Flip2. HONOR es un fabricante de dispositivos inteligentes que está ganando rápidamente reconocimiento mundial.

Cobertura y entregables del informe de mercado de vidrio ultrafino

El informe "Tamaño y pronóstico del mercado de vidrio ultrafino (2021-2034)" proporciona un análisis detallado del mercado que abarca las siguientes áreas:

- Tamaño y pronóstico del mercado de vidrio ultrafino a nivel mundial, regional y nacional para todos los segmentos clave del mercado cubiertos en el alcance.

- Tendencias del mercado del vidrio ultrafino, así como la dinámica del mercado, tales como los factores impulsores, las limitaciones y las oportunidades clave.

- Análisis detallado PEST y FODA

- Análisis del mercado de vidrio ultrafino que abarca las principales tendencias del mercado, el marco global y regional, los principales actores, las regulaciones y los desarrollos recientes del mercado.

- Análisis del panorama industrial y de la competencia, que abarca la concentración del mercado, el análisis mediante mapas de calor, los principales actores y los desarrollos recientes en el mercado del vidrio ultrafino.

- Perfiles detallados de las empresas

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias