Rapport sur le marché des pièces de rechange automobiles du commerce électronique 2028 par segments, géographie, dynamique, développements récents et perspectives stratégiques

Prévisions du marché des pièces détachées automobiles en ligne jusqu'en 2028 - Impact de la COVID-19 et analyse mondiale par type de produit [freinage (plaquettes de frein, composants hydrauliques et visserie, rotor et tambour), direction et suspension (rotules, biellettes de direction, biellettes de barre stabilisatrice, roulements/joints et autres), moyeux, cardans, joints universels, joints d'étanchéité, filtres, bougies d'allumage et autres] et type de consommateur (B2B et B2C)

- Statut : Publié

- Code du rapport : TIPRE00007013

- Catégorie : Automobile et transport

- Nombre de pages : 206

- Formats de rapport disponibles :

- Date de dernière mise à jour : June 17, 2024

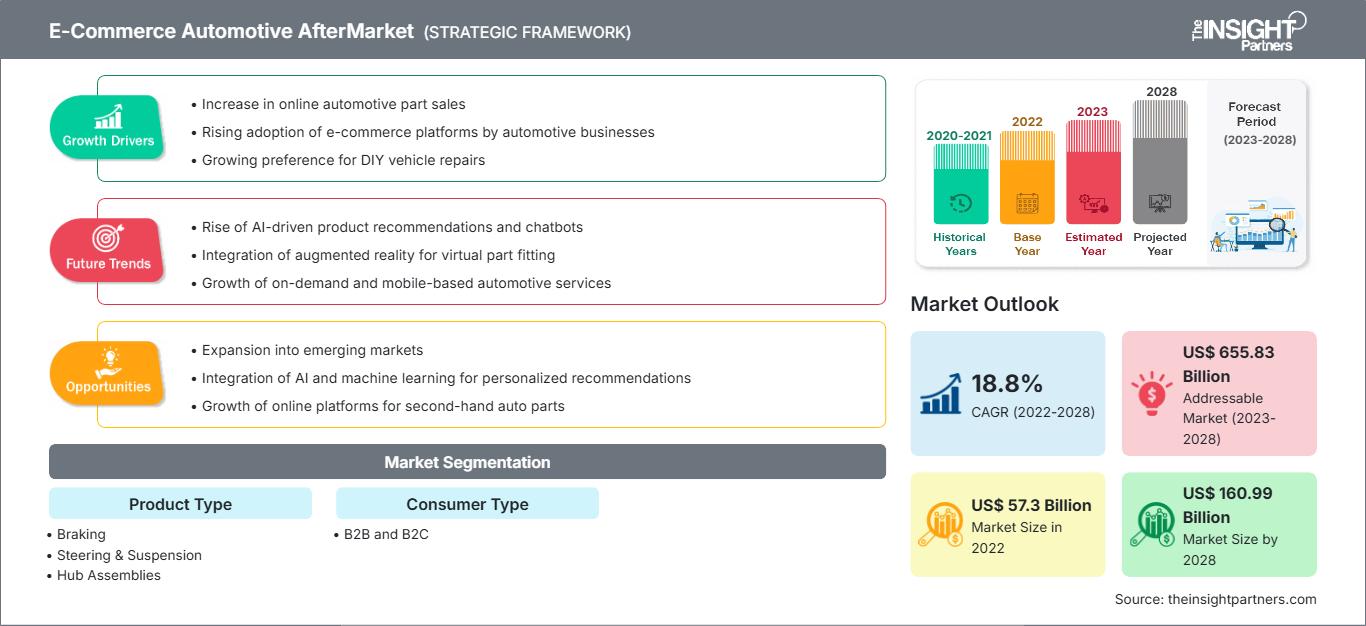

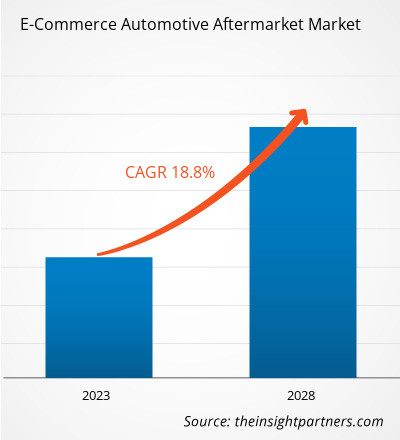

Le marché des pièces détachées automobiles en ligne devrait passer de 57 301,1 millions de dollars américains en 2022 à 1 60 985,4 millions de dollars américains en 2028. Il devrait croître à un TCAC de 18,8 % de 2022 à 2028.

L'Amérique du Nord dispose d'une industrie automobile développée en raison de la production continue de véhicules commerciaux. Français Selon le rapport 2021 de l'Organisation Internationale des Constructeurs d'Automobiles (OICA), les États-Unis ont produit 7 604 154 véhicules utilitaires en 2021, 6 895 604 en 2020 et 8 367 239 en 2019. De même, le Canada a produit 826 767 véhicules utilitaires en 2021, 1 048 942 en 2020 et 1 455 215 en 2019, selon le rapport 2021 de l'OICA. Le Mexique a produit un total de 2 437 411 véhicules utilitaires en 2021, 2 209 121 en 2020 et 2 604 080 en 2019, selon le même rapport. Les États-Unis, le Canada et le Mexique sont en tête du segment de la production de véhicules utilitaires à l'échelle mondiale, selon les statistiques de l'OICA. Ainsi, la production continue de véhicules utilitaires dans la région soutient la croissance du marché des pièces détachées automobiles en ligne en Amérique du Nord.

Impact de la pandémie de COVID-19 sur le marché des pièces détachées automobiles en ligne

En Amérique du Nord, les États-Unis, le Canada et le Mexique ont connu une augmentation significative du nombre de cas de COVID-19. De nombreuses usines de fabrication ont été fermées, les municipalités fonctionnaient au ralenti et les activités des industries de l'automobile et des semi-conducteurs ont été interrompues en 2020, après le début de la pandémie de COVID-19. Dans la région, l'interruption de la chaîne de valeur causée par la fermeture de diverses installations de production et entrepôts aux États-Unis et au Canada en raison de la pandémie de COVID-19 a eu un impact immédiat sur la demande à court terme, l'infrastructure logistique et les stocks de produits. Cependant, l'industrie automobile a continué de croître grâce aux services uniques offerts par les canaux en ligne en termes d'entretien, de réparation et de remplacement. Avant le début de la pandémie de COVID-19, le commerce électronique était en pleine expansion. Cependant, la pandémie a accru le nombre de consommateurs américains utilisant les plateformes en ligne, les encourageant à dépenser davantage. Ces activités ont généré une part importante des revenus grâce à la pénétration d'un écosystème de commerce électronique bien organisé qui permet aux équipementiers automobiles de se lancer dans des ventes de pièces détachées en ligne. En avril 2021, les ventes de composants, de pièces et d'accessoires automobiles sur le marché de la rechange automobile en ligne aux États-Unis et au Canada ont augmenté de plus de 60 % par rapport à 2020.

Vous bénéficierez d’une personnalisation sur n’importe quel rapport - gratuitement - y compris des parties de ce rapport, ou une analyse au niveau du pays, un pack de données Excel, ainsi que de profiter d’offres exceptionnelles et de réductions pour les start-ups et les universités

Marché du commerce électronique des pièces détachées automobiles: Perspectives stratégiques

-

Obtenez les principales tendances clés du marché de ce rapport.Cet échantillon GRATUIT comprendra une analyse de données, allant des tendances du marché aux estimations et prévisions.

Analyse du marché des pièces détachées automobiles en ligne

Augmentation du nombre de consommateurs bricoleurs et de réparateurs indépendants

Amazon et eBay proposent des livraisons le jour même de pièces détachées automobiles dans de nombreux endroits. Ils entretiennent des relations commerciales avec quelques grands fabricants de pièces détachées, tels que Robert Bosch GmbH, Denso Corp., Magna International Inc., Continental AG et ZF Friedrichshafen AG, qui proposent des services d'installation. Les fournisseurs traditionnels de pièces détachées automobiles savent que les clients qui achètent des pièces détachées automobiles pour le bricolage seraient les premiers à migrer vers les sites de commerce électronique plutôt que vers les fournisseurs traditionnels. Maintenir une relation commerciale stable avec les commerçants et les techniciens est donc une stratégie unique pour rester compétitif. Les équipements standard des véhicules les plus récents incluent des capteurs pour détecter les changements de voie, des caméras à 360° et des technologies nécessitant l'assistance d'experts.

Dans le contexte du « DIFM », les consommateurs possédant des voitures haut de gamme devraient dépendre des entreprises de réparation automobile et des mécaniciens. Par exemple, Advance Auto Parts utilise le commerce électronique pour cibler spécifiquement ces segments de marché en leur fournissant des fonctionnalités d'aide à la conduite. Le marché des pièces détachées automobiles en ligne doit continuer à exploiter les marchés numériques B2C (entreprise à consommateur) et B2B (entreprise à entreprise) ainsi que les chaînes d'approvisionnement en pleine expansion qui les soutiennent, car les concurrents continuent de conquérir ce marché lucratif. Par conséquent, l'adoption croissante de l'achat en ligne de composants automobiles dans le secteur automobile en ligne devrait créer de nouvelles opportunités sur ce marché.

Analyses du marché par type de produit

En fonction du type de produit, le marché des pièces détachées automobiles en ligne est segmenté en freinage (plaquettes de frein, composants hydrauliques et quincaillerie, rotor et tambour), direction et suspension (rotules, biellettes de direction, biellettes de barre stabilisatrice, roulements/joints, etc.), et ensembles moyeux, joints universels, joints statiques, filtres, bougies d'allumage, etc. En 2021, les autres segments ont dominé le marché des pièces détachées automobiles en ligne, représentant la plus grande part de marché.

Analyse du marché par type de consommateur

Selon le type de consommateur, le marché des pièces détachées automobiles en ligne est segmenté en B2B et B2C. En 2021, le segment B2C a dominé le marché des pièces détachées automobiles en ligne, représentant une part de marché plus importante.

Les acteurs du marché adoptent des stratégies, telles que des fusions, des acquisitions et des initiatives commerciales, pour maintenir leur position sur le marché des pièces détachées automobiles en ligne. Voici quelques développements des principaux acteurs :

- En mars 2022, DENSO Aftermarket, filiale spécialisée dans les pièces détachées automobiles de DENSO, important fabricant de composants d'origine (OE), a remporté le très convoité prix du Fournisseur de l'année 2021, décerné par GroupAuto International, une importante centrale d'achat mondiale.

- En septembre 2020, LKQ Corporation a finalisé l'accord précédemment annoncé de vente de ses participations dans deux grossistes tchèques de pièces automobiles à Swiss Automotive Group AG. Les conditions de la transaction n'ont pas été divulguées.

Commerce électronique : Pièces détachées automobiles

Marché des pièces détachées automobiles en ligneLes tendances et facteurs régionaux influençant le marché des pièces détachées automobiles en ligne tout au long de la période de prévision ont été analysés en détail par les analystes de The Insight Partners. Cette section aborde également les segments et la répartition géographique du marché des pièces détachées automobiles en ligne en Amérique du Nord, en Europe, en Asie-Pacifique, au Moyen-Orient et en Afrique, ainsi qu'en Amérique du Sud et en Amérique centrale.

Portée du rapport sur le marché des pièces détachées automobiles en ligne| Attribut de rapport | Détails |

|---|---|

| Taille du marché en 2022 | US$ 57.3 Billion |

| Taille du marché par 2028 | US$ 160.99 Billion |

| TCAC mondial (2022 - 2028) | 18.8% |

| Données historiques | 2020-2021 |

| Période de prévision | 2023-2028 |

| Segments couverts |

By Type de produit

|

| Régions et pays couverts |

Amérique du Nord

|

| Leaders du marché et profils d'entreprises clés |

|

Densité des acteurs du marché des pièces détachées automobiles en ligne : comprendre son impact sur la dynamique commerciale

Le marché de l'après-vente automobile en ligne connaît une croissance rapide, portée par une demande croissante des utilisateurs finaux, due à des facteurs tels que l'évolution des préférences des consommateurs, les avancées technologiques et une meilleure connaissance des avantages du produit. Face à cette demande croissante, les entreprises élargissent leur offre, innovent pour répondre aux besoins des consommateurs et capitalisent sur les nouvelles tendances, ce qui alimente la croissance du marché.

- Obtenez le Marché du commerce électronique des pièces détachées automobiles Aperçu des principaux acteurs clés

Alibaba Group Holding Limited ; Amazon.com, Inc. ; AutoZone, Inc. ; Shopee365 ; CATI SpA ; eBay Inc. ; LKQ Corporation ; The Pep Boys ; CarParts.com, Inc ; et Denso Corporation sont des acteurs clés du marché.

Naveen est un professionnel expérimenté des études de marché et du conseil, fort de plus de 9 ans d'expertise dans des projets personnalisés, syndiqués et de conseil. Actuellement vice-président associé, il a géré avec succès les parties prenantes tout au long de la chaîne de valeur des projets et a rédigé plus de 100 rapports de recherche et plus de 30 missions de conseil. Son expertise couvre des projets industriels et gouvernementaux, contribuant significativement à la réussite de ses clients et à la prise de décision fondée sur les données.

Naveen est titulaire d'un diplôme d'ingénieur en électronique et communication de la VTU, Karnataka, et d'un MBA en marketing et opérations de l'Université de Manipal. Membre actif de l'IEEE depuis 9 ans, il a participé à des conférences et des colloques techniques et s'est porté volontaire au niveau des sections et des régions. Avant d'occuper ce poste, il a travaillé comme consultant stratégique associé chez IndustryARC et comme consultant en serveurs industriels chez Hewlett Packard (HP Global).

- Analyse complète de la taille du marché et prévisions

- Analyse détaillée de la segmentation

- Évaluation approfondie de la dynamique du marché

- Aperçus par région et par pays

- Paysage concurrentiel et analyse comparative des entreprises

- Intelligence économique stratégique

Témoignages

Le rapport sur le marché des systèmes SCADA d'Insight Partners est complet et fournit des informations précieuses sur les tendances actuelles et les prévisions. L'équipe a fait preuve d'un grand professionnalisme, d'une grande réactivité et d'un grand soutien tout au long du projet. Nous sommes très satisfaits et recommandons vivement leurs services.

RAN KEDEM Partenaire, Reali Technologies LTDJ'ai demandé un rapport sur un marché logiciel très spécifique et l'équipe l'a produit en quelques jours. Les informations étaient très pertinentes et bien présentées. J'ai ensuite demandé des modifications et des ajouts au rapport. L'équipe a de nouveau été très réactive et j'ai reçu le rapport final en moins d'une semaine.

JEAN-HERVÉ JENN Président, Future AnalyticaNous avons collaboré avec The Insight Partners pour une importante étude de marché et des prévisions. Ils nous ont fourni une vision claire des opportunités et des risques, ce qui nous a aidés à élaborer nos plans. Leurs recherches étaient faciles à utiliser et basées sur des données solides. Elles nous ont permis de prendre des décisions éclairées et en toute confiance. Nous les recommandons vivement.

PIYUSH NAGPAL Vice-président principal, Feux de route mondiauxInsight Partners a réalisé une étude de marché pertinente et bien structurée, avec une solide expertise du domaine. Son équipe a fait preuve de professionnalisme et de réactivité tout au long du projet. Son site web convivial a facilité l'accès aux rapports sectoriels. Nous recommandons vivement ses services d'études fiables et de haute qualité.

YUKIHIKO ADACHI PDG, Bleu profond, LLC.C'est la première fois que j'achète une étude de marché auprès de The Insight Partners. J'étais un peu hésitant au début, mais j'ai consulté leur site web et me suis senti plus à l'aise pour prendre le risque d'acheter une étude de marché. Je suis entièrement satisfait de la qualité du rapport et du service client. J'avais plusieurs questions et commentaires concernant le rapport initial, mais après quelques échanges par e-mail avec leur analyste, je pense avoir obtenu un rapport qui pourra alimenter notre processus de planification stratégique. Merci beaucoup pour votre temps et pour avoir rendu cette expérience positive. Je recommanderai sans hésiter vos services et vous serez mon premier contact lorsque nous aurons besoin de données de marché supplémentaires.

JOHN SUZUKI Président-directeur général, administrateur du conseil d'administration, BK TechnologiesJe tiens à vous remercier pour votre soutien et le professionnalisme dont vous avez fait preuve lors du traitement de ma demande d'informations concernant le marché des dispositifs de diagnostic in vitro (DIV) pour les maladies infectieuses au Nigéria. J'apprécie votre patience, vos conseils et votre volonté d'offrir une réduction, ce qui nous a finalement permis de conclure un accord. Je me réjouis de collaborer à nouveau avec The Insight Partners, grâce à l'impression que vous m'avez laissée suite à cette première rencontre.

DR CHIJIOKE DIRECTEUR GÉNÉRAL D'ONYIA, PineCrest Healthcare Ltd.Raison d'acheter

- Prise de décision éclairée

- Compréhension de la dynamique du marché

- Analyse concurrentielle

- Connaissances clients

- Prévisions de marché

- Atténuation des risques

- Planification stratégique

- Justification des investissements

- Identification des marchés émergents

- Amélioration des stratégies marketing

- Amélioration de l'efficacité opérationnelle

- Alignement sur les tendances réglementaires