Stratégies de marché des équipements de protection individuelle militaires, principaux acteurs, opportunités de croissance, analyse et prévisions d’ici 2031

Analyse du marché des équipements de protection individuelle militaires (2021-2031), des parts mondiales et régionales, des tendances et des opportunités de croissance. Couverture du rapport : par équipement (gilets pare-balles, protection contre les matières dangereuses, vêtements ignifuges, autres) ; produits (gants, casques, bottes, lunettes, masques, autres) ; utilisateur final (armée de terre, armée de l'air, marine) ; et géographie.

- Statut : Données publiées

- Code du rapport : TIPTE100000687

- Catégorie : Aérospatiale et défense

- Nombre de pages : 150

- Formats de rapport disponibles :

- Date de dernière mise à jour : February 15, 2025

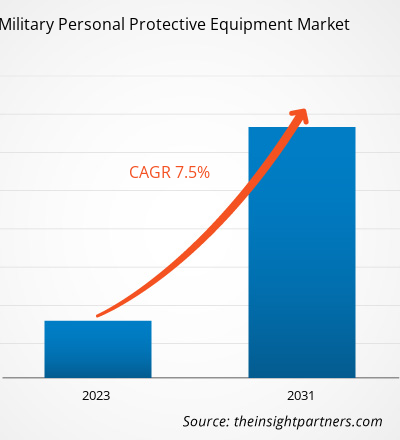

Le marché des équipements de protection individuelle militaires devrait atteindre 32,7 milliards de dollars d'ici 2031, contre 18,3 milliards de dollars en 2023. Le marché devrait enregistrer un TCAC de 7,5 % en 2023-2031. Les guerres en cours au Moyen-Orient et en Europe et l'augmentation des dépenses consacrées à la modernisation des équipements militaires et à la garantie de la sécurité du personnel militaire sont parmi les principaux facteurs qui stimulent le marché des équipements de protection individuelle militaires.

Analyse du marché des équipements de protection individuelle militaires

La croissance des équipements de protection individuelle militaires à travers le monde est principalement due à l'augmentation des budgets de défense et aux efforts croissants de modernisation des soldats. En outre, la demande croissante de divers équipements militaires augmente à mesure que les gouvernements du monde entier se concentrent de plus en plus sur la modernisation des soldats en raison des préoccupations croissantes en matière de sécurité. La complexité persistante et incertaine de l'environnement de sécurité international dans le monde devrait stimuler les dépenses de défense des autorités de la région au cours des cinq prochaines années. De plus, les entreprises du monde entier sont très impliquées dans la conception et la fourniture d'équipements de protection individuelle militaires, ce qui devrait à son tour stimuler la croissance du marché dans les années à venir. Parmi les entreprises engagées dans la conception d'équipements de protection individuelle militaires, on trouve Ceradyne (3M), Honeywell International, BAE Systems, DuPont et Ansell Ltd., entre autres.

Aperçu du marché des équipements de protection individuelle militaires

Français Ces dernières années, la demande d'équipements de protection individuelle militaire a augmenté en raison de la situation de guerre en Afghanistan, en Irak, en Libye et en Serbie. De plus, la production nucléaire croissante de l'Iran a intensifié les tensions militaires entre les États-Unis, Israël et l'Iran. La demande croissante d'équipements de protection avancés dans différentes forces militaires est un facteur majeur de croissance du marché des équipements de protection individuelle (EPI) militaires. Les cinq principaux dépensiers militaires en 2023 sont les États-Unis, la Chine, l'Inde, l'Arabie saoudite et la Russie, qui stimulent l'achat d'équipements de protection individuelle militaires dans ces pays. La demande d'équipements de protection individuelle militaire devrait être stimulée par les initiatives de modernisation des grands financiers de la défense à travers les États-Unis et par les menaces à la sécurité intérieure telles que le terrorisme organisé et le crime. De plus, une augmentation significative des tensions transfrontalières entre l'Inde, la Chine et le Pakistan stimule la croissance du marché des équipements de protection individuelle (EPI) militaires en Asie-Pacifique.

Personnalisez ce rapport en fonction de vos besoins

Vous bénéficierez d'une personnalisation gratuite de n'importe quel rapport, y compris de certaines parties de ce rapport, d'une analyse au niveau des pays, d'un pack de données Excel, ainsi que de superbes offres et réductions pour les start-ups et les universités.

Marché des équipements de protection individuelle militaires : informations stratégiques

-

Obtenez les principales tendances clés du marché de ce rapport.Cet échantillon GRATUIT comprendra une analyse de données, allant des tendances du marché aux estimations et prévisions.

Moteurs et opportunités du marché des équipements de protection individuelle militaires

Augmentation des dépenses militaires mondiales pour la modernisation des soldats

Le combat moderne conduit à plusieurs confrontations de scénarios de champ de bataille complexes ; ainsi, les soldats sont confrontés à une grande variété de menaces, telles que les engins explosifs improvisés (EEI) et les attaques de grenades propulsées par fusée. Ces menaces entraînent une augmentation de la demande de différents EPI, tels que les casques , les lunettes de vision nocturne, les gilets pare-balles et les vêtements, qui offrent une protection et une connaissance de la situation améliorées aux soldats. En outre, pour répondre à la demande de modernisation et de sécurité des soldats, les gouvernements et les associations du monde entier augmentent le financement et les dépenses consacrées aux infrastructures et équipements militaires. Selon l'Institut international de recherche sur la paix de Stockholm (SIPRI), en 2023, les dépenses militaires mondiales totales évaluées à 2 443 milliards de dollars américains sont passées de 2 240 milliards de dollars américains en 2022. Par conséquent, l'augmentation des dépenses militaires à travers le monde devrait stimuler le marché des équipements de protection individuelle militaires dans les années à venir.

Utilisation de matériaux avancés dans le développement d'équipements de protection militaire pour une meilleure sécurité

Les acteurs du marché, ainsi que le gouvernement, sont engagés dans la recherche et le développement (R&D) constants de nouveaux modèles d'EPI en utilisant des matériaux de qualité optimale et innovants pour faire face à la demande croissante des utilisateurs finaux. De plus, les fabricants se concentrent sur le développement de nouvelles technologies telles que les matériaux nanotechnologiques dans les gilets pare-balles pour offrir des gilets pare-balles flexibles et légers, ce qui profite à l'expansion du marché. Par exemple, certains des matériaux avancés proposés par la société 3M pour le développement d'équipements de protection individuelle militaire sont les matériaux réfléchissants 3M Scotchlite série 6755 et 3M Scotchlite série 8710, entre autres.

Le système MultiVisor en maille d'acier 3M PELTOR V4A-10P, 10 EA/caisse ; l'écran facial 3M PETG WE96S, 82580-00000, crosse plate, courte, transparente, 50 EA/caisse ; et le système de visière 3M PELTOR Brush Defender, V40AH9A-1P avec cache-oreilles H9A, 1 EA/caisse, entre autres, pour le développement du masque de protection. L'application de matériaux avancés et d'EPI efficaces nécessite un équilibre entre l'accomplissement d'une mission et le maintien de la tâche et la protection physiologique, psychologique et physique des soldats. L'intégration de matériaux et de technologies avancés comprend des revêtements ou des matériaux à haute perméabilité pour stimuler le transfert de chaleur par évaporation du corps et éviter la diffusion de produits chimiques toxiques sur la peau. Ainsi, l'utilisation de matériaux avancés dans le développement d'équipements de protection individuelle militaires devrait créer des opportunités pour les principaux acteurs opérant sur le marché.

Analyse de segmentation du rapport sur le marché des équipements de protection individuelle militaires

Les segments clés qui ont contribué à l’élaboration de l’analyse du marché des équipements de protection individuelle militaires sont les équipements, les produits et l’utilisateur final.

- En fonction de l'équipement, le marché des équipements de protection individuelle militaire a été divisé en gilets pare-balles, protection contre les matières dangereuses, vêtements ignifuges, etc. Le segment des gilets pare-balles détenait une part de marché plus importante en 2023.

- En fonction des produits, le marché des équipements de protection individuelle militaires a été divisé en gants, casques, bottes, lunettes, masques faciaux, etc. Le segment des casques détenait une part de marché plus importante en 2023.

- Sur la base de l'utilisateur final, le marché a été segmenté en forces terrestres, forces aériennes et marines. Le segment des forces terrestres a dominé le marché en 2023.

Analyse des parts de marché des équipements de protection individuelle militaires par zone géographique

La portée géographique du rapport sur le marché des équipements de protection individuelle militaires est principalement divisée en cinq régions : Amérique du Nord, Europe, Asie-Pacifique, Moyen-Orient et Afrique et Amérique du Sud.

L'Amérique du Nord a dominé le marché des équipements de protection individuelle militaire en 2023. La région Amérique du Nord comprend les États-Unis, le Canada et le Mexique. Les États-Unis et le Canada font partie des principaux pays d'Amérique du Nord qui investissent des sommes importantes dans leurs forces militaires. Les ministères de la Défense de ces pays ont constamment adopté diverses technologies de pointe pour fournir des technologies prêtes à l'emploi aux soldats. L'augmentation des dépenses militaires a eu une influence positive sur l'adoption des diverses technologies modernes, telles que les équipements de protection individuelle militaire. De plus, la demande de divers équipements militaires augmente à mesure que les gouvernements de la région nord-américaine se concentrent de plus en plus sur la modernisation des soldats en raison des préoccupations croissantes en matière de sécurité. La complexité persistante et incertaine de l'environnement de sécurité internationale dans le monde devrait stimuler les dépenses de défense des autorités de la région au cours des cinq prochaines années. En outre, l'accent accru mis par l'administration américaine sur l'amélioration de la protection et des capacités des soldats devrait être l'un des principaux moteurs de croissance des dépenses de défense dans les années à venir.

Aperçu régional du marché des équipements de protection individuelle militaires

Les tendances et facteurs régionaux influençant le marché des équipements de protection individuelle militaire tout au long de la période de prévision ont été expliqués en détail par les analystes d’Insight Partners. Cette section traite également des segments et de la géographie du marché des équipements de protection individuelle militaire en Amérique du Nord, en Europe, en Asie-Pacifique, au Moyen-Orient et en Afrique, ainsi qu’en Amérique du Sud et en Amérique centrale.

- Obtenez les données régionales spécifiques au marché des équipements de protection individuelle militaires

Portée du rapport sur le marché des équipements de protection individuelle militaires

| Attribut de rapport | Détails |

|---|---|

| Taille du marché en 2023 | 18,3 milliards de dollars américains |

| Taille du marché d'ici 2031 | 32,7 milliards de dollars américains |

| Taux de croissance annuel composé mondial (2023-2031) | 7,5% |

| Données historiques | 2021-2022 |

| Période de prévision | 2023-2031 |

| Segments couverts |

Par équipement

|

| Régions et pays couverts |

Amérique du Nord

|

| Leaders du marché et profils d'entreprises clés |

|

Densité des acteurs du marché des équipements de protection individuelle militaires : comprendre son impact sur la dynamique commerciale

Le marché des équipements de protection individuelle militaires connaît une croissance rapide, tirée par la demande croissante des utilisateurs finaux en raison de facteurs tels que l'évolution des préférences des consommateurs, les avancées technologiques et une plus grande sensibilisation aux avantages du produit. À mesure que la demande augmente, les entreprises élargissent leurs offres, innovent pour répondre aux besoins des consommateurs et capitalisent sur les tendances émergentes, ce qui alimente davantage la croissance du marché.

La densité des acteurs du marché fait référence à la répartition des entreprises ou des sociétés opérant sur un marché ou un secteur particulier. Elle indique le nombre de concurrents (acteurs du marché) présents sur un marché donné par rapport à sa taille ou à sa valeur marchande totale.

Les principales entreprises opérant sur le marché des équipements de protection individuelle militaires sont :

- Systèmes de protection Avon Inc.

- MKU Limitée

- Société américaine d'armure

- DuPont de Nemours, Inc.

- Honeywell International Inc.

- Deenside Ltd.

Avis de non-responsabilité : les sociétés répertoriées ci-dessus ne sont pas classées dans un ordre particulier.

- Obtenez un aperçu des principaux acteurs du marché des équipements de protection individuelle militaires

Actualités et développements récents du marché des équipements de protection individuelle militaire

Le marché des équipements de protection individuelle militaires est évalué en collectant des données qualitatives et quantitatives après des recherches primaires et secondaires, qui comprennent d'importantes publications d'entreprises, des données d'associations et des bases de données. Voici une liste des développements sur le marché des équipements de protection individuelle militaires et des stratégies :

- En septembre 2021, Leidos a remporté un contrat avec la Defense Advanced Research Projects Agency (DARPA). Grâce à ce contrat, Leidos développera une technologie pour des équipements de protection avancés destinés à l'armée américaine.

- En septembre 2021, SKYDEX s'est associé à ArmorSource. Ce partenariat visait à innover dans le domaine des technologies de casques pour protéger les communautés militaires et policières.

Rapport sur le marché des équipements de protection individuelle militaires et livrables

Le rapport « Taille et prévisions du marché des équipements de protection individuelle militaires (2021-2031) » fournit une analyse détaillée du marché couvrant les domaines ci-dessous :

- Taille du marché et prévisions aux niveaux mondial, régional et national pour tous les segments de marché clés couverts par le périmètre

- Dynamique du marché, comme les facteurs moteurs, les contraintes et les opportunités clés

- Principales tendances futures

- Analyse détaillée des cinq forces de Porter

- Analyse du marché mondial et régional couvrant les principales tendances du marché, les principaux acteurs, les réglementations et les développements récents du marché

- Analyse du paysage industriel et de la concurrence couvrant la concentration du marché, l'analyse de la carte thermique, les principaux acteurs et les développements récents

- Profils d'entreprise détaillés avec analyse SWOT

Naveen est un professionnel expérimenté des études de marché et du conseil, fort de plus de 9 ans d'expertise dans des projets personnalisés, syndiqués et de conseil. Actuellement vice-président associé, il a géré avec succès les parties prenantes tout au long de la chaîne de valeur des projets et a rédigé plus de 100 rapports de recherche et plus de 30 missions de conseil. Son expertise couvre des projets industriels et gouvernementaux, contribuant significativement à la réussite de ses clients et à la prise de décision fondée sur les données.

Naveen est titulaire d'un diplôme d'ingénieur en électronique et communication de la VTU, Karnataka, et d'un MBA en marketing et opérations de l'Université de Manipal. Membre actif de l'IEEE depuis 9 ans, il a participé à des conférences et des colloques techniques et s'est porté volontaire au niveau des sections et des régions. Avant d'occuper ce poste, il a travaillé comme consultant stratégique associé chez IndustryARC et comme consultant en serveurs industriels chez Hewlett Packard (HP Global).

- Analyse complète de la taille du marché et prévisions

- Analyse détaillée de la segmentation

- Évaluation approfondie de la dynamique du marché

- Aperçus par région et par pays

- Paysage concurrentiel et analyse comparative des entreprises

- Intelligence économique stratégique

Témoignages

Le rapport sur le marché des systèmes SCADA d'Insight Partners est complet et fournit des informations précieuses sur les tendances actuelles et les prévisions. L'équipe a fait preuve d'un grand professionnalisme, d'une grande réactivité et d'un grand soutien tout au long du projet. Nous sommes très satisfaits et recommandons vivement leurs services.

RAN KEDEM Partenaire, Reali Technologies LTDJ'ai demandé un rapport sur un marché logiciel très spécifique et l'équipe l'a produit en quelques jours. Les informations étaient très pertinentes et bien présentées. J'ai ensuite demandé des modifications et des ajouts au rapport. L'équipe a de nouveau été très réactive et j'ai reçu le rapport final en moins d'une semaine.

JEAN-HERVÉ JENN Président, Future AnalyticaNous avons collaboré avec The Insight Partners pour une importante étude de marché et des prévisions. Ils nous ont fourni une vision claire des opportunités et des risques, ce qui nous a aidés à élaborer nos plans. Leurs recherches étaient faciles à utiliser et basées sur des données solides. Elles nous ont permis de prendre des décisions éclairées et en toute confiance. Nous les recommandons vivement.

PIYUSH NAGPAL Vice-président principal, Feux de route mondiauxInsight Partners a réalisé une étude de marché pertinente et bien structurée, avec une solide expertise du domaine. Son équipe a fait preuve de professionnalisme et de réactivité tout au long du projet. Son site web convivial a facilité l'accès aux rapports sectoriels. Nous recommandons vivement ses services d'études fiables et de haute qualité.

YUKIHIKO ADACHI PDG, Bleu profond, LLC.C'est la première fois que j'achète une étude de marché auprès de The Insight Partners. J'étais un peu hésitant au début, mais j'ai consulté leur site web et me suis senti plus à l'aise pour prendre le risque d'acheter une étude de marché. Je suis entièrement satisfait de la qualité du rapport et du service client. J'avais plusieurs questions et commentaires concernant le rapport initial, mais après quelques échanges par e-mail avec leur analyste, je pense avoir obtenu un rapport qui pourra alimenter notre processus de planification stratégique. Merci beaucoup pour votre temps et pour avoir rendu cette expérience positive. Je recommanderai sans hésiter vos services et vous serez mon premier contact lorsque nous aurons besoin de données de marché supplémentaires.

JOHN SUZUKI Président-directeur général, administrateur du conseil d'administration, BK TechnologiesJe tiens à vous remercier pour votre soutien et le professionnalisme dont vous avez fait preuve lors du traitement de ma demande d'informations concernant le marché des dispositifs de diagnostic in vitro (DIV) pour les maladies infectieuses au Nigéria. J'apprécie votre patience, vos conseils et votre volonté d'offrir une réduction, ce qui nous a finalement permis de conclure un accord. Je me réjouis de collaborer à nouveau avec The Insight Partners, grâce à l'impression que vous m'avez laissée suite à cette première rencontre.

DR CHIJIOKE DIRECTEUR GÉNÉRAL D'ONYIA, PineCrest Healthcare Ltd.Raison d'acheter

- Prise de décision éclairée

- Compréhension de la dynamique du marché

- Analyse concurrentielle

- Connaissances clients

- Prévisions de marché

- Atténuation des risques

- Planification stratégique

- Justification des investissements

- Identification des marchés émergents

- Amélioration des stratégies marketing

- Amélioration de l'efficacité opérationnelle

- Alignement sur les tendances réglementaires