Strategie di mercato per la gestione delle ferite bioattive, principali attori, opportunità di crescita, analisi e previsioni entro il 2031

Rapporto di analisi sulle dimensioni e le previsioni del mercato della gestione bioattiva delle ferite (2021-2031), quota globale e regionale, tendenze e opportunità di crescita. Copertura: per prodotto (sostituti cutanei bioingegnerizzati, medicazioni a base di collagene, medicazioni antimicrobiche, alginati e idrocolloidi), applicazione (ulcere da pressione, ulcere del piede diabetico, ulcere venose delle gambe, ustioni e ferite chirurgiche), utente finale (ospedali e cliniche, centri chirurgici ambulatoriali e altri) e geografia.

- Stato : Dati rilasciati

- Codice del report : TIPMD00002256

- Categoria : Scienze della vita

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : February 15, 2025

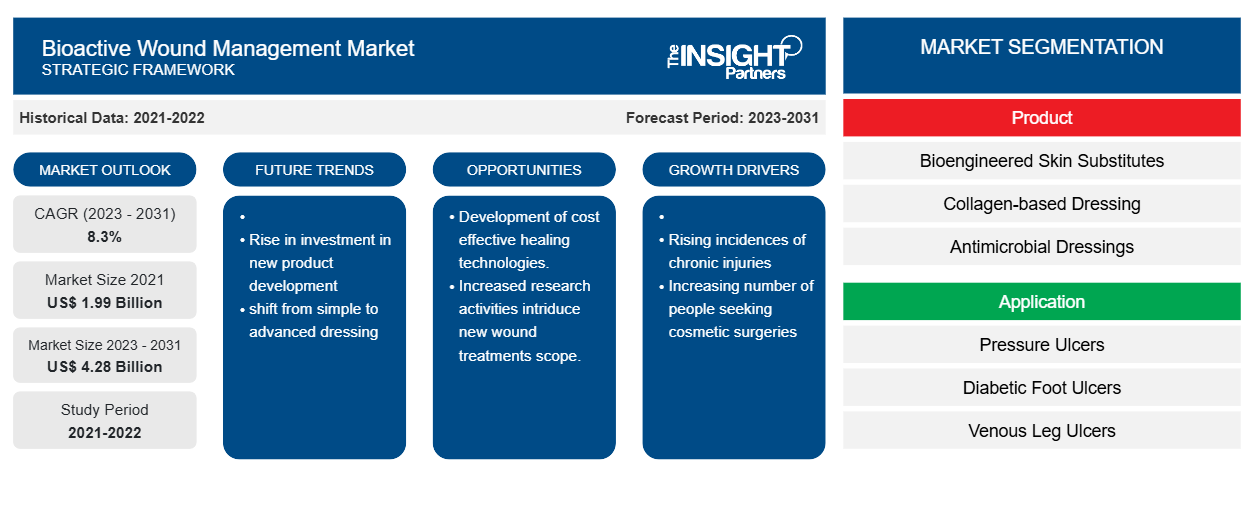

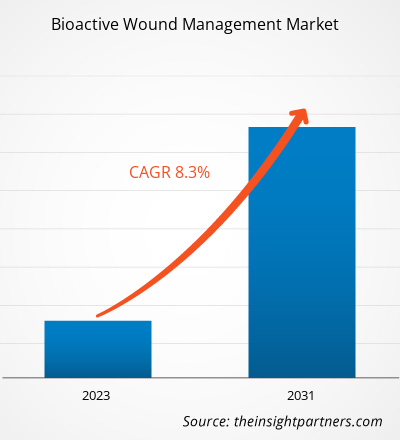

Si stima che il mercato della gestione bioattiva delle ferite abbia raggiunto 1,99 miliardi di dollari nel 2021 e XX miliardi di dollari nel 2023 e si prevede che raggiungerà i 4,28 miliardi di dollari entro il 2031; si stima che entro il 2031 registrerà un CAGR dell'8,3%. È probabile che la stampa 3D nella gestione della cura delle ferite rimanga una tendenza chiave del mercato della gestione bioattiva delle ferite. Bioactive Wound Management Market Size was estimated to be US$ 1.99 billion in 2021 and US$ XX billion in 2023 and is expected to reach US$ 4.28 billion by 2031; it is estimated to record a CAGR of 8.3% by 2031. 3D Printing in Wound Care Management is likely to remain a key Bioactive Wound Management Market Trend.

Analisi di mercato della gestione bioattiva delle ferite Wound Management Market Analysis

L'aumento dell'incidenza di lesioni croniche e un numero maggiore di interventi chirurgici stanno contribuendo alla crescita del mercato della gestione bioattiva delle ferite. A livello globale, si prevede che la prevalenza di infezioni del sito chirurgico aumenterà a causa del crescente numero di interventi chirurgici. Un aumento del numero di interventi chirurgici a livello globale è dovuto alla crescente prevalenza di varie malattie croniche. Secondo i dati forniti dai National Institutes of Health (NIH), ogni anno in Europa vengono eseguiti circa 20 milioni di interventi chirurgici importanti. Secondo la Dubai Health Authority (DHA), nel 2021 a Dubai sono stati eseguiti circa 159.000 interventi chirurgici. Secondo la stessa fonte, il numero di persone che hanno cercato interventi di chirurgia estetica a Dubai è raddoppiato da 223.507 nel 2020 a 583.909 nel 2022. I prodotti per la gestione bioattiva delle ferite consentono una rapida guarigione delle infezioni del sito chirurgico; si prevede che il numero crescente di interventi chirurgici aumenterà la domanda di questi prodotti nel prossimo futuro. bioactive wound management market growth. Globally, the prevalence of surgical site infection is anticipated to rise owing to the growing number of surgeries. An increase in the number of surgical procedures globally is due to the rising prevalence of various chronic diseases. According to data provided by the National Institutes of Health (NIH), ~20 million major surgeries are carried out each year in Europe. According to the Dubai Health Authority (DHA), ~159,000 surgeries were performed in Dubai in 2021. Per the same source, the number of people seeking cosmetic surgeries in Dubai doubled from 223,507 in 2020 to 583,909 in 2022. Bioactive wound management products enable rapid healing of surgical site infection; the increasing number of surgical procedures is projected to surge the demand for these products in the near future.

Panoramica del mercato della gestione bioattiva delle ferite Wound Management Market Overview

La regione nordamericana deteneva la quota maggiore del mercato della gestione bioattiva delle ferite. Il significativo aumento degli investimenti per lo sviluppo di nuovi prodotti e la presenza dei principali giganti farmaceutici nella regione sono probabilmente responsabili del predominio del mercato. I player nordamericani hanno una rete globale di centri di distribuzione che aiuta le aziende a raggiungere più sedi in tutto il mondo. Si prevede che la regione Asia-Pacifico sarà la regione in più rapida crescita tra tutte le altre regioni. Si prevede che la crescita del mercato della gestione bioattiva delle ferite sarà più rapida in paesi come India, Cina e Australia. Si prevede che la crescita del mercato in questi paesi sarà più rapida a causa della crescente prevalenza di ferite croniche , dell'aumento della popolazione diabetica e anziana e del miglioramento delle strutture sanitarie. Inoltre, la presenza di organismi di gestione attiva della cura delle ferite nella regione offre opportunità redditizie per la crescita del mercato.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, comprese parti di questo report, o analisi a livello nazionale, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato della gestione bioattiva delle ferite: Wound Management Market: approfondimenti strategici

-

Scopri le principali tendenze di mercato in questo rapporto.Questo campione GRATUITO includerà analisi di dati che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Driver e opportunità di mercato per la gestione bioattiva delle ferite Wound Management Market Drivers and Opportunities

Innovazione nei prodotti avanzati per la cura delle ferite per favorire il mercato

Sono in fase di sviluppo diverse tecnologie di guarigione delle ferite convenienti per soddisfare la crescente domanda. Gli sviluppi nella gestione delle ferite hanno portato a un passaggio da semplici medicazioni a prodotti avanzati per la cura delle ferite. Le medicazioni avanzate per ferite sono state progettate per creare un ambiente umido che favorisca la guarigione. I prodotti per la cura delle ferite a base di cheratina sono spesso utilizzati insieme a queste medicazioni per favorire la riepitelizzazione delle ferite. Questi prodotti facilitano una guarigione più rapida perché vengono assorbiti nelle ferite, il che elimina la necessità di cambiare frequentemente la medicazione. Inoltre, l'uso di materiali biologici di scaffold, tra cui una matrice extracellulare (ECM) intatta o singoli componenti dell'ECM, fornisce nuove opzioni terapeutiche che si concentrano sul microambiente della ferita e facilitano il rapido ripristino della pelle. re-epithelialization. These products facilitate faster healing by being absorbed into the wounds, which eliminates the need to frequently change the dressing. Furthermore, the usage of biological scaffold materials including an intact extracellular matrix (ECM) or individual components of the ECM provides new therapeutic options that focus on the wound microenvironment and facilitate rapid restoration of skin.

Di seguito sono menzionati alcuni progressi nei prodotti per la cura delle ferite:

•Integra Life Sciences offre un'ampia gamma di prodotti per la gestione delle ferite, come Integra Bilayer Wound Matrix, Integra Meshed Bilayer Wound Matrix e Integra Flowable Wound Matrix. Questi sono composti da collagene bovino reticolato, glicosaminoglicano e rivestimento in silicone. Sono utilizzati nella gestione di ferite parziali e a tutto spessore, ulcere da pressione, ulcere venose, ulcere diabetiche, ulcere vascolari croniche e ferite chirurgiche.

•Matristem (ACell Inc.) è un'impalcatura ECM naturale composta da UBM-ECM suino non reticolato. Il vantaggio principale dell'UBM-ECM rispetto ad altri prodotti ECM naturali è che trattiene il componente della membrana basale della vescica urinaria su una superficie dell'impalcatura biologica. La membrana basale funziona per ancorare i tessuti epiteliali all'ECM in organi come la pelle e i vasi sanguigni.

Aumento delle attività di ricerca per introdurre nuovi trattamenti per le ferite: un’opportunità

Le ferite croniche possono causare difficoltà ai chirurghi nel gestire efficacemente tali ferite, portando a ulteriori complicazioni. Con un numero crescente di pazienti che soffrono di ferite croniche, c'è una crescente necessità di un approccio sistematico al trattamento, che ha spinto l'adozione di cure basate sulle prove. Ricerche e sperimentazioni cliniche hanno dimostrato che l'uso di prodotti bioattivi per la cura delle ferite può migliorare la guarigione delle ferite umide. Gli enti governativi e le università di ricerca svolgono un ruolo attivo nel promuovere i progressi nella cura delle ferite e diverse organizzazioni di ricerca sono dedicate allo sviluppo di prodotti avanzati per la cura delle ferite. Ciò probabilmente creerà opportunità di crescita durante il periodo di previsione.

Di seguito sono riportati alcuni esempi a questo proposito:

- Nel luglio 2023, i ricercatori della Queen's University di Belfast hanno sviluppato un nuovo trattamento per le ulcere del piede diabetico (DFU) utilizzando una benda stampata in 3D nota come scaffold. Questa tecnologia innovativa combina nanoparticelle lipidiche e idrogel per creare scaffold personalizzati simili alla pelle che rilasciano sia un rilascio in massa che sostenuto di molecole caricate di antibiotici per trattare le DFU. Questa scoperta ha il potenziale per migliorare significativamente il trattamento delle ulcere diabetiche.

- Nel giugno 2023, i ricercatori dell'Università di Birmingham hanno presentato una nuova tecnica che ha dimostrato come l'argento possa conservare le sue proprietà antimicrobiche per periodi di tempo più lunghi quando impregnato in "vetro bioattivo". Si è scoperto che questa combinazione fornisce una protezione antimicrobica delle ferite più efficace e duratura rispetto alle alternative più convenzionali. Vetri bioattivi: una classe unica di biomateriali sintetici realizzati in silicone e utilizzati da diversi anni nell'innesto osseo.

Analisi della segmentazione del rapporto di mercato sulla gestione bioattiva delle ferite

I segmenti chiave che hanno contribuito alla derivazione dell'analisi di mercato della gestione bioattiva delle ferite sono il prodotto, l'applicazione e l'utente finale.

- In base al prodotto, il mercato della gestione bioattiva delle ferite è segmentato in sostituti cutanei bioingegnerizzati, medicazioni a base di collagene, medicazioni antimicrobiche, alginati e idrocolloidi. Il segmento degli alginati ha detenuto la quota di mercato maggiore nel 2023.

- Per applicazione, il mercato è segmentato in ulcere da pressione, ulcere del piede diabetico, ulcere venose delle gambe, ferite da ustione e ferite chirurgiche. Il segmento delle ferite da ustione ha detenuto la quota maggiore del mercato nel 2023.

- In termini di utenti finali, il mercato è segmentato in ospedali e cliniche, centri chirurgici ambulatoriali e altri. Il segmento ospedali e cliniche ha dominato il mercato nel 2023.

Analisi della quota di mercato della gestione bioattiva delle ferite per area geografica

L'ambito geografico del rapporto di mercato sulla gestione delle ferite bioattive è principalmente suddiviso in cinque regioni: Nord America, Asia Pacifico, Europa, Medio Oriente e Africa e Sud America/Sud e Centro America. Il Nord America ha dominato il mercato della gestione delle ferite bioattive. Si prevede che il mercato della gestione delle ferite bioattive negli Stati Uniti sarà il più grande e in più rapida crescita a causa di vari fattori. Pochi dei fattori trainanti includono la presenza di vari produttori di dispositivi medici che producono dispositivi e prodotti per la gestione delle ferite bioattive e il supporto del governo fornendo strumenti avanzati, tecnologia ed esperienza per una cura ottimale delle ferite. Le aziende negli Stati Uniti stanno aumentando la loro presenza seguendo strategie organiche e inorganiche. Ad esempio, nell'ottobre 2021, Medline Industries ha annunciato un investimento di 77,5 milioni di dollari USA per costruire un nuovo centro di distribuzione in Kansas. Pertanto, la crescente necessità negli Stati Uniti di medicazioni per ferite indica un'opportunità sostanziale per i principali attori di sviluppare la gestione della cura delle ferite con prodotti innovativi. Si prevede che l'Asia Pacifico crescerà con il CAGR più elevato nei prossimi anni.

Approfondimenti regionali sul mercato della gestione bioattiva delle ferite

Le tendenze regionali e i fattori che influenzano il mercato della gestione delle ferite bioattive durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di Insight Partners. Questa sezione discute anche i segmenti e la geografia del mercato della gestione delle ferite bioattive in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e America meridionale e centrale.

- Ottieni i dati specifici regionali per il mercato della gestione bioattiva delle ferite

Ambito del rapporto di mercato sulla gestione bioattiva delle ferite

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2021 | 1,99 miliardi di dollari USA |

| Dimensioni del mercato entro il 2031 | 4,28 miliardi di dollari USA |

| CAGR globale (2023-2031) | 8,3% |

| Dati storici | 2021-2022 |

| Periodo di previsione | 2023-2031 |

| Segmenti coperti |

Per Prodotto

|

| Regioni e Paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli attori del mercato della gestione bioattiva delle ferite: comprendere il suo impatto sulle dinamiche aziendali

Il mercato del mercato della gestione delle ferite bioattive sta crescendo rapidamente, spinto dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando le loro offerte, innovando per soddisfare le esigenze dei consumatori e capitalizzando sulle tendenze emergenti, il che alimenta ulteriormente la crescita del mercato.

La densità degli operatori di mercato si riferisce alla distribuzione di aziende o società che operano in un particolare mercato o settore. Indica quanti concorrenti (operatori di mercato) sono presenti in un dato spazio di mercato in relazione alle sue dimensioni o al valore di mercato totale.

Le principali aziende che operano nel mercato della gestione bioattiva delle ferite sono:

- MiMedx

- Integra LifeSciences

- Organogenesi

- Gruppo Regenix dei tessuti Plc

- Coloplast

- Società a responsabilità limitata Hartmann

Disclaimer : le aziende elencate sopra non sono classificate secondo un ordine particolare.

- Ottieni una panoramica dei principali attori del mercato della gestione bioattiva delle ferite

Notizie di mercato e sviluppi recenti sulla gestione bioattiva delle ferite

Il mercato della gestione bioattiva delle ferite viene valutato raccogliendo dati qualitativi e quantitativi dopo la ricerca primaria e secondaria, che include importanti pubblicazioni aziendali, dati di associazioni e database. Di seguito è riportato un elenco degli sviluppi nel mercato della gestione bioattiva delle ferite:

- A luglio 2022, Smith+Nephew ha introdotto l'app di supporto clinico WOUND COMPASS. Questa app è uno strumento digitale completo per i professionisti sanitari progettato per assistere nella valutazione delle ferite e nel processo decisionale, con l'obiettivo di ridurre la variazione della pratica. (Fonte: Smith+Nephew, 2022)

- A giugno 2022, Medline ha lanciato la sua Optifoam Gentle EX Foam Dressing. Il prodotto è progettato per aiutare a spostare la pressione quando utilizzato con il protocollo di prevenzione delle lesioni da pressione. Il prodotto presenta cinque strati unici per aiutare ad assorbire la forza di taglio e l'attrito e gestire l'umidità. (Fonte: Medline, 2022)

- Nel gennaio 2022, Convatec ha acquisito Triad Life Sciences Inc. L'acquisizione rafforza la posizione di Advanced Wound Care di Convatec negli Stati Uniti (Focus) e garantisce l'accesso a una piattaforma tecnologica complementare e innovativa (Innovation) che migliora la gestione avanzata delle ferite e i risultati per i pazienti. (Fonte: Convatec, 2022)

- A febbraio 2021, AxioBiosolutions ha ricevuto la certificazione CE dall'Europa per la sua linea MaxioCel di prodotti per la cura avanzata delle ferite di nuova generazione. Questa approvazione normativa consente ad Axio di entrare nel mercato della cura avanzata delle ferite in rapida crescita da 14 miliardi di USD a livello globale. (Fonte: AxioBiosolutions, 2021)

Copertura e risultati del rapporto di mercato sulla gestione bioattiva delle ferite

Il rapporto "Dimensioni e previsioni del mercato della gestione delle ferite bioattive (2021-2031)" fornisce un'analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni e previsioni del mercato a livello globale, regionale e nazionale per tutti i segmenti di mercato chiave coperti dall'ambito

- Dinamiche di mercato come fattori trainanti, vincoli e opportunità chiave

- Principali tendenze future

- Analisi dettagliata delle cinque forze PEST/Porter e SWOT

- Analisi di mercato globale e regionale che copre le principali tendenze di mercato, i principali attori, le normative e gli sviluppi recenti del mercato

- Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa di calore, i principali attori e gli sviluppi recenti

- Profili aziendali dettagliati

- Fabbro+Nipote

Mrinal è un'analista di ricerca esperta con oltre 8 anni di esperienza nella consulenza e nell'intelligence di mercato nel settore delle scienze biologiche. Grazie a una mentalità strategica e a un costante impegno verso l'eccellenza, ha maturato una profonda competenza nelle previsioni farmaceutiche, nella valutazione delle opportunità di mercato e nello sviluppo di benchmark di settore. Il suo lavoro è incentrato sulla fornitura di insight fruibili che consentono ai clienti di prendere decisioni strategiche consapevoli.

Il punto di forza di Mrinal risiede nella capacità di tradurre complessi set di dati quantitativi in business intelligence significative. Il suo acume analitico è fondamentale per definire strategie di go-to-market (GTM) e individuare opportunità di crescita nei settori farmaceutico e dei dispositivi medici. In qualità di consulente di fiducia, si concentra costantemente sulla semplificazione dei processi di flusso di lavoro e sulla definizione di best practice, promuovendo così l'innovazione e l'efficienza operativa per i suoi clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative