Rapporto sull’analisi delle quote e delle dimensioni del mercato delle alternative ai prodotti lattiero-caseari | Previsioni 2031

Rapporto di analisi sulle dimensioni e le previsioni del mercato delle alternative ai latticini (2021-2031), quota globale e regionale, tendenze e opportunità di crescita. Copertura: per fonte (soia, mandorle, cocco, avena e altri), tipo di prodotto (latte, gelato, yogurt, formaggio e altri), canale di distribuzione (supermercati e ipermercati, minimarket, vendita al dettaglio online e altri) e area geografica.

- Stato : Dati rilasciati

- Codice del report : TIPRE00004533

- Categoria : Cibo e bevande

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : May 16, 2024

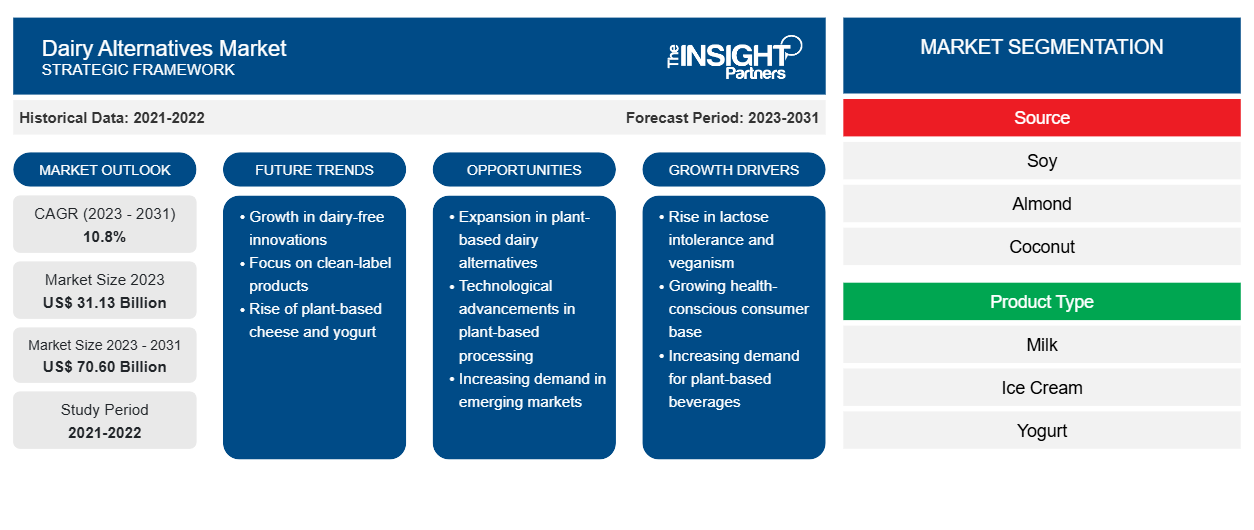

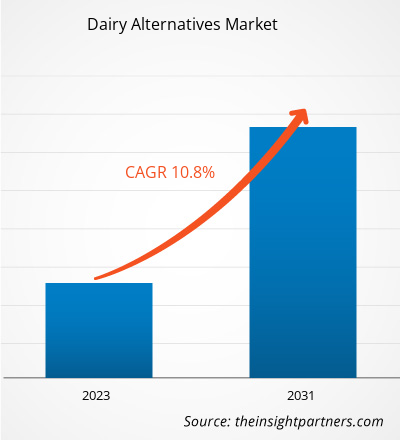

Si prevede che la dimensione del mercato delle alternative ai latticini raggiungerà i 70,60 miliardi di dollari entro il 2031, rispetto ai 31,13 miliardi di dollari del 2023. Si prevede che il mercato registrerà un CAGR del 10,8% nel periodo 2023-2031. È probabile che la crescente domanda di alternative funzionali ai latticini rimanga una tendenza chiave nel mercato.

Analisi di mercato delle alternative ai latticini

La popolazione vegana è cresciuta in modo significativo negli ultimi anni. Secondo Veganuary (un'organizzazione non-profit che incoraggia le persone in tutto il mondo a diventare vegane per l'intero mese di gennaio), più di 620.000 persone si sono iscritte alla campagna Veganuary nel 2022 e le registrazioni sono aumentate del 200% negli ultimi 3 anni. Le persone stanno passando sempre più a una dieta vegana a causa delle crescenti preoccupazioni per la salute e la sostenibilità. L'industria del bestiame è uno dei principali contributori alle emissioni totali di gas serra antropogenici. Secondo la Food and Agriculture Organization (FAO), l'industria mondiale del bestiame emette 7,1 gigatonnellate di anidride carbonica all'anno, pari al 14,5% di tutte le emissioni di gas serra causate dall'uomo. Il settore lattiero-caseario è responsabile del 30% delle emissioni totali del bestiame.

Molti studi hanno dimostrato che passare a una dieta vegana può ridurre significativamente le emissioni di anidride carbonica. Secondo il dott. Fredrik Hedenus, professore alla Chalmers University of Technology, Svezia, e coautore di un articolo di ricerca sul consumo di carne e latticini, pubblicato sulla rivista "Climate Change", ridurre il consumo di carne e latticini può essere fondamentale per riportare l'inquinamento climatico agricolo a livelli accettabili.

Inoltre, molte organizzazioni, come le Nazioni Unite, PETA e Good Food Institute, credono che il veganismo possa aiutare a salvare il pianeta dalla crisi climatica. La consapevolezza riguardo agli effetti dannosi dell'industria del bestiame sull'ambiente sta aumentando tra i consumatori. Il consumo di prodotti lattiero-caseari di origine vegetale aiuta a ridurre al minimo l'impronta di carbonio, a risparmiare acqua e altre risorse naturali e a ridurre l'impatto ambientale complessivo. Pertanto, i consumatori stanno rapidamente passando a prodotti lattiero-caseari e a base di carne di origine vegetale. Questo fattore sta guidando in modo significativo il mercato delle alternative ai latticini.

Panoramica del mercato delle alternative ai latticini

Le alternative ai latticini come latte, yogurt, gelato, formaggio e burro sono fatte di latte di soia, latte di piselli e latte di cocco. Il latte di soia è più conveniente di altri latti vegetali e fornisce una quantità di proteine simile a quella del latte intero. I consumatori sono molto propensi a prodotti a base vegetale o vegan-friendly a causa delle crescenti preoccupazioni per la salute e della crescente consapevolezza del benessere degli animali. I prodotti a base vegetale sono generalmente percepiti come alternative più sane. Inoltre, l'allevamento di bovini da latte sta avendo un impatto negativo sull'ambiente generale, portando al cambiamento climatico. Questo fattore sta anche influenzando la crescita del mercato delle alternative ai latticini.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, comprese parti di questo report, o analisi a livello nazionale, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato delle alternative ai latticini: approfondimenti strategici

-

Scopri le principali tendenze di mercato in questo rapporto.Questo campione GRATUITO includerà analisi di dati che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Driver e opportunità di mercato per le alternative ai latticini

L'aumento dell'incidenza dell'intolleranza al lattosio favorisce il mercato

Secondo il National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK), una media del 68% della popolazione mondiale è intollerante al lattosio . Secondo il National Institute of Health (NIH), l'intolleranza al lattosio è piuttosto comune nella popolazione adulta dell'Asia orientale, colpendo il 75-95% delle persone in queste comunità. Inoltre, la carenza congenita di lattosio è ampiamente osservata in Asia Pacifico e Africa. Pertanto, paesi come Cina, Giappone, Corea del Sud e Taiwan sono potenziali mercati per le alternative ai latticini.

I prodotti lattiero-caseari di origine vegetale hanno una consistenza, cremosità e consistenza simili ai prodotti lattiero-caseari convenzionali. Sono arricchiti con nutrienti, come proteine e calcio, per soddisfare i requisiti nutrizionali giornalieri dei consumatori. Pertanto, la crescente prevalenza di intolleranza al lattosio e allergie al latte tra i consumatori sta guidando il mercato delle alternative ai latticini.

Numero crescente di lanci di nuovi prodotti per offrire enormi opportunità di crescita

I produttori di alternative ai latticini stanno investendo in modo significativo nell'innovazione di prodotto per attrarre un vasto gruppo di consumatori. La strategia di innovazione di prodotto offre un vantaggio competitivo ai player che operano nel mercato, aumentando la loro redditività. I produttori di alternative ai latticini offrono prodotti certificati biologici, non OGM, senza glutine, clean-label e senza allergeni per soddisfare le nuove esigenze dei clienti. Inoltre, poiché i consumatori sono diventati attenti alla salute , preferiscono prodotti ipocalorici e a basso contenuto di grassi. Pertanto, i produttori di latticini di origine vegetale offrono prodotti non zuccherati e a basso contenuto di zucchero. Ad esempio, a febbraio 2021, Hasla Foods ha lanciato lo yogurt al latte d'avena senza zucchero in un formato famiglia da 24 once. Il prodotto contiene solo 90 calorie a porzione e non ha zuccheri aggiunti. A giugno 2021, la stessa azienda ha ampliato la sua presenza al dettaglio rendendo i suoi prodotti disponibili in 160 negozi National Grocers by Vitamin Cottage negli Stati Uniti.

Inoltre, i produttori stanno sperimentando diverse fonti di latte vegetale, come orzo, piselli, canapa, semi di chia, banane e anacardi. Ad esempio, Take Two Foods, uno dei principali produttori di latte vegetale, offre latte d'orzo arricchito di nutrienti, che ha un portafoglio completo di nutrienti, come proteine, fibre, calcio e grassi insaturi. Si prevede che tali strategie forniranno opportunità redditizie al mercato delle alternative ai latticini durante il periodo di previsione.

Analisi della segmentazione del rapporto di mercato sulle alternative ai latticini

I segmenti chiave che hanno contribuito alla derivazione dell'analisi di mercato delle alternative ai latticini sono la fonte, il tipo di prodotto e il canale di distribuzione.

- In base alla fonte, il mercato delle alternative ai latticini è suddiviso in soia, mandorle, cocco, avena e altri. Il segmento della soia ha detenuto la quota di mercato maggiore nel 2023. Si prevede che la soia acquisirà popolarità tra gli anziani e le consumatrici negli Stati Uniti, poiché include isoflavoni, che si dice riducano il rischio di malattie cardiache e cancro al seno. La soia contiene anche fitoestrogeni, un ormone che funziona in modo simile agli estrogeni nelle donne. Il consumo di alternative ai latticini a base di soia è popolare tra le donne come terapia alternativa per aumentare i livelli di estrogeni. La soia è ricca di nutrienti e ha un alto contenuto proteico rispetto ad altre alternative ai latticini; pertanto, la popolarità della soia per i suoi benefici culmina nel guidare il mercato per il segmento durante il periodo di previsione.

In termini di canale di distribuzione, il mercato è suddiviso in supermercati e ipermercati, minimarket, vendita al dettaglio online e altri. Il segmento supermercati e ipermercati ha dominato il mercato nel 2023. Supermercati e ipermercati sono grandi esercizi commerciali al dettaglio che offrono un'ampia gamma di generi alimentari, generi alimentari, bevande e altri articoli per la casa. Prodotti di vari marchi sono disponibili a prezzi ragionevoli in questi negozi, consentendo agli acquirenti di trovare rapidamente il prodotto giusto. Inoltre, questi negozi offrono sconti interessanti, molteplici opzioni di pagamento e un'esperienza piacevole per il cliente. Supermercati e ipermercati si concentrano sulla massimizzazione delle vendite dei prodotti per aumentare i loro margini di profitto. I produttori di latticini vegetali di solito preferiscono vendere i loro prodotti tramite supermercati e ipermercati a causa dell'elevato traffico ricevuto da questi negozi. La crescente urbanizzazione, l'aumento della popolazione operaia e i prezzi competitivi aumentano la popolarità di supermercati e ipermercati nelle regioni sviluppate e in via di sviluppo.

Analisi della quota di mercato delle alternative ai latticini per area geografica

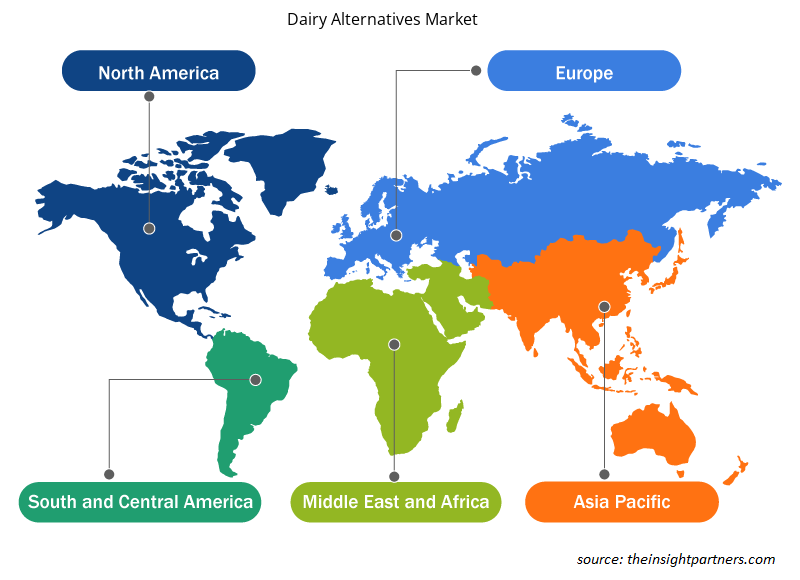

L'ambito geografico del rapporto sul mercato delle alternative ai latticini è suddiviso principalmente in cinque regioni: Nord America, Asia Pacifico, Europa, Medio Oriente e Africa e Sud America/Sud e Centro America.

Il mercato delle alternative ai latticini dell'Asia Pacifica ha detenuto la quota di mercato più ampia nel 2023. Negli ultimi anni, il consumo di alternative al latte è aumentato costantemente a causa del crescente numero di persone intolleranti al lattosio e delle preoccupazioni per la salute relative ad antibiotici e ormoni della crescita che si trovano spesso nel latte vaccino. La ricerca condotta da Rakuten nel 2021 ha mostrato che l'87% dei consumatori in Cina aveva provato il latte vegetale, il 50% aveva provato altri sostituti del latte, il 42% aveva provato la carne vegetale e il 32% aveva provato i sostituti vegani delle uova. Inoltre, la stessa ricerca ha rilevato che il 3% degli intervistati consuma solo alimenti vegetali. Pertanto, il mercato delle alternative ai latticini sta crescendo a causa della crescente domanda di prodotti lattiero-caseari vegetali dovuta alla crescente prevalenza di intolleranza al lattosio nell'Asia Pacifica.

Approfondimenti regionali sul mercato delle alternative ai latticini

Le tendenze regionali e i fattori che influenzano il Dairy Alternatives Market durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di Insight Partners. Questa sezione discute anche i segmenti e la geografia del Dairy Alternatives Market in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e Sud e Centro America.

- Ottieni i dati specifici regionali per il mercato delle alternative ai latticini

Ambito del rapporto di mercato sulle alternative ai latticini

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2023 | 31,13 miliardi di dollari USA |

| Dimensioni del mercato entro il 2031 | 70,60 miliardi di dollari USA |

| CAGR globale (2023-2031) | 10,8% |

| Dati storici | 2021-2022 |

| Periodo di previsione | 2023-2031 |

| Segmenti coperti |

Per fonte

|

| Regioni e Paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli attori del mercato delle alternative ai latticini: comprendere il suo impatto sulle dinamiche aziendali

Il mercato dei prodotti alternativi ai latticini sta crescendo rapidamente, spinto dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando le loro offerte, innovando per soddisfare le esigenze dei consumatori e capitalizzando sulle tendenze emergenti, il che alimenta ulteriormente la crescita del mercato.

La densità degli operatori di mercato si riferisce alla distribuzione di aziende o società che operano in un particolare mercato o settore. Indica quanti concorrenti (operatori di mercato) sono presenti in un dato spazio di mercato in relazione alle sue dimensioni o al valore di mercato totale.

Le principali aziende che operano nel mercato delle alternative ai latticini sono:

- SoleOpta

- Coltivatori di diamanti blu

- Nestlé SA

- Danone SA

- Oatly Inc

- Aziende agricole Califia, LLC

Disclaimer : le aziende elencate sopra non sono classificate secondo un ordine particolare.

- Ottieni una panoramica dei principali attori del mercato delle alternative ai latticini

Notizie e sviluppi recenti sul mercato delle alternative ai latticini

Il mercato delle alternative ai latticini viene valutato raccogliendo dati qualitativi e quantitativi post-ricerca primaria e secondaria, che includono importanti pubblicazioni aziendali, dati di associazioni e database. Di seguito è riportato un elenco degli sviluppi nel mercato dei disturbi del linguaggio e della parola:

- Il marchio di latte vegetale milkadamia entra nel settore refrigerato e dimostra che "less is more" con il debutto della sua linea di latte di macadamia e miscele artigianali biologiche che salta i riempitivi e le gomme comuni in molte bevande non casearie e risponde a una crescente domanda di opzioni più simili a quelle fatte in casa. (Fonte: Alternative al latte - Milkadamia, comunicato stampa/sito Web aziendale/newsletter, 2024)

- Califia Farms ha lanciato Califia Farms Complete, un latte vegetale cremoso con nove nutrienti essenziali, otto grammi di proteine, tutti e nove gli amminoacidi essenziali e metà dello zucchero del latte vaccino, ha affermato l'azienda. (Fonte: Dairy Alternatives Califia Farms LLC, comunicato stampa/sito Web aziendale/newsletter, 2024)

Copertura e risultati del rapporto sul mercato delle alternative ai latticini

Il rapporto “Dimensioni e previsioni del mercato delle alternative ai latticini (2023-2031)” fornisce un’analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni e previsioni del mercato a livello globale, regionale e nazionale per tutti i segmenti di mercato chiave coperti dall'ambito

- Dinamiche di mercato come fattori trainanti, vincoli e opportunità chiave

- Principali tendenze future

- Analisi dettagliata delle cinque forze PEST/Porter e SWOT

- Analisi di mercato globale e regionale che copre le principali tendenze di mercato, i principali attori, le normative e gli sviluppi recenti del mercato

- Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa di calore, i principali attori e gli sviluppi recenti

- Profili aziendali dettagliati

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative