Crescita, dimensioni, quota, tendenze, analisi dei principali attori del mercato del cloud distribuito e previsioni fino al 2031

Dimensioni e previsioni del mercato del cloud distribuito (2021-2031), quota globale e regionale, trend e opportunità di crescita. Copertura del rapporto di analisi: per applicazione (Edge Computing, Content Delivery, Internet of Things e altri), servizio (Sicurezza dei dati, Archiviazione dati, Networking e altri), dimensione aziendale (Grandi imprese e PMI), settore verticale (BFSI, Sanità, Vendita al dettaglio ed e-commerce, Produzione, IT e telecomunicazioni, Energia e servizi di pubblica utilità, Media e intrattenimento, Pubblica amministrazione e difesa e altri) e area geografica.

- Stato : Edito

- Codice del report : TIPRE00018589

- Categoria : Tecnologia, media e telecomunicazioni

- Numero di pagine : 152

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : August 14, 2024

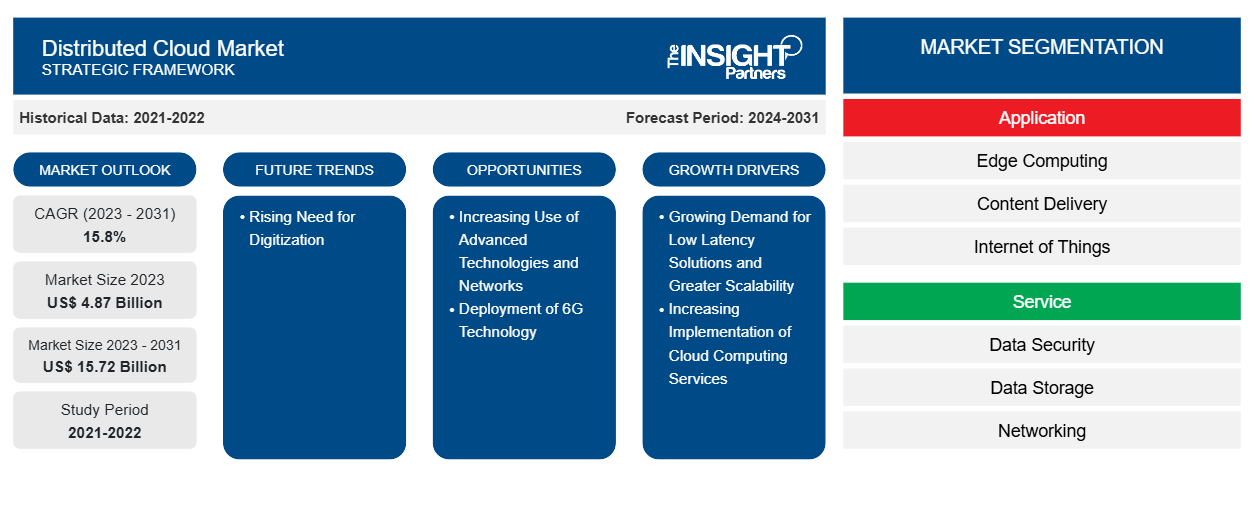

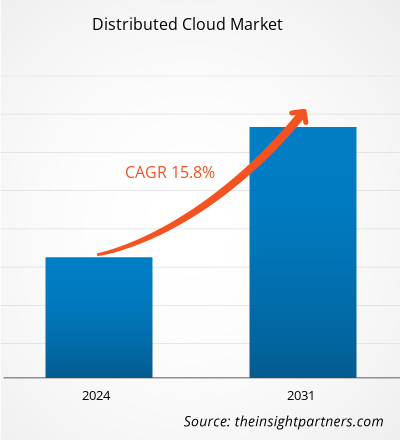

Si prevede che la dimensione del mercato del cloud distribuito raggiungerà i 15,72 miliardi di dollari entro il 2031, rispetto ai 4,87 miliardi di dollari del 2023. Si prevede che il mercato registrerà un CAGR del 15,8% nel periodo 2023-2031. La crescente necessità di digitalizzazione porterà probabilmente nuove tendenze nel mercato.

Analisi del mercato del cloud distribuito

La crescita del mercato del cloud distribuito è attribuita alla crescente domanda di soluzioni a bassa latenza e maggiore scalabilità. Il cloud computing distribuito aumenta anche la reattività dei servizi trasferendo le attività di elaborazione più vicino all'utente finale. Inoltre, la crescente implementazione di servizi di cloud computing in diversi settori, come l'automobile, l'istruzione, la finanza, la vendita al dettaglio, l'immobiliare, l'agricoltura, i media e l'intrattenimento, guida il mercato. Inoltre, si prevede che la crescente richiesta di digitalizzazione e distribuzione della tecnologia 6G alimenterà il mercato del cloud distribuito nei prossimi anni. Nell'area Asia-Pacifico, si registra un notevole aumento della crescita e degli investimenti nel cloud computing, con una crescita prevista nei ricavi dei servizi di cloud pubblico. La Cina è riconosciuta come il più grande mercato di cloud pubblico nella regione. Le principali aziende di infrastrutture come servizio (IaaS) come Alibaba Cloud e Huawei hanno sede in Cina. Inoltre, i governi dell'area Asia-Pacifico stanno mostrando sempre più interesse per le soluzioni di cloud sovrano a causa di sconvolgimenti geopolitici, crescenti minacce informatiche, mutevoli leggi sulla protezione dei dati e cambiamenti nelle politiche commerciali digitali.

Panoramica del mercato del cloud distribuito

L'architettura di un cloud distribuito coinvolge più cloud che aiutano a soddisfare i requisiti di conformità e le esigenze di prestazioni, oltre a supportare l'edge computing pur essendo gestiti centralmente da un provider di cloud pubblico. La crescita dell'Internet of Things (IoT) e dell'edge computing sono stati un importante motore per le implementazioni cloud distribuite. Le applicazioni di intelligenza artificiale (AI) che spostano grandi quantità di dati da posizioni edge al cloud richiedono che i servizi cloud siano il più vicino possibile alle posizioni edge; inoltre, lo spostamento delle risorse cloud nella posizione edge stessa può aumentare significativamente le prestazioni per queste applicazioni.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, comprese parti di questo report, o analisi a livello nazionale, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato del cloud distribuito: approfondimenti strategici

-

Scopri le principali tendenze di mercato in questo rapporto.Questo campione GRATUITO includerà analisi di dati che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Driver e opportunità del mercato del cloud distribuito

Crescente domanda di soluzioni a bassa latenza e maggiore scalabilità per favorire il mercato

Bassa latenza è una rete informatica migliorata per elaborare un elevato volume di messaggi di dati con il minimo ritardo. Queste reti sono destinate a supportare funzioni che richiedono un accesso quasi in tempo reale a dati in rapida evoluzione. Il cloud computing distribuito riduce la latenza e aumenta la reattività dei servizi trasferendo le attività di elaborazione più vicino all'utente finale. I dati vengono quindi gestiti localmente anziché su un server centralizzato, sviluppando un'esperienza utente superiore. Inoltre, varie aziende hanno offerto offerte cloud distribuite per soddisfare le esigenze di bassa latenza. Ad esempio, a settembre 2023, Oracle ha ampliato le sue offerte cloud distribuite per soddisfare le diverse esigenze delle organizzazioni e la crescente domanda globale di servizi Oracle Cloud Infrastructure (OCI). Oracle Database Azure e MySQL HeatWave Lakehouse su AWS sono le nuove aggiunte al cloud distribuito di OCI. Di conseguenza, le aziende ottengono una maggiore flessibilità per distribuire servizi cloud ovunque, affrontando al contempo numerosi requisiti di privacy dei dati, sovranità dei dati e bassa latenza, consentendo l'accesso a oltre 100 servizi progettati per eseguire qualsiasi carico di lavoro.

Distribuzione della tecnologia 6G

6G è accettato per offrire una latenza nell'intervallo dei microsecondi. Ciò consente ai servizi cloud distribuiti di eseguire attività di elaborazione in tempo reale come realtà aumentata (AR), realtà virtuale (VR) e guida autonoma con un'efficienza senza precedenti. Diverse aziende offrono sistemi cloud e di comunicazione distribuiti 6G. Ad esempio, Next G Alliance (NGA) offre un sistema cloud e di comunicazione distribuiti. NGA ha sviluppato questo sistema per la visione 6G nordamericana. Intende rendere i sistemi 6G un cloud ad ampia area con abbondante elaborazione e distribuzione del carico di lavoro tra dispositivi, data center e nodi di rete. Il sistema cloud e di comunicazione distribuiti 6G è un passo verso capacità di sistema di comunicazione e di elaborazione congiunte che non sono state raggiunte in 4G e 5G sulla cloudificazione della rete e l'edge computing. Pertanto, si prevede che l'implementazione della tecnologia 6G offra diverse opportunità per la crescita del mercato del cloud distribuito durante il periodo di previsione.

Analisi della segmentazione del rapporto sul mercato del cloud distribuito

I segmenti chiave che hanno contribuito alla derivazione dell'analisi del mercato del cloud distribuito sono applicazione, servizio, impresa, dimensione e settore verticale.

- In base all'applicazione, il mercato del cloud distribuito è suddiviso in edge computing, content delivery, Internet of Things e altri. Il segmento edge computing ha detenuto la quota di mercato maggiore nel 2023. L'edge computing è uno schema di elaborazione distribuita che avvicina le applicazioni aziendali alle fonti di dati, come i server edge locali o i dispositivi IoT. Ciò si traduce in tempi di risposta migliorati, insight più rapidi e una migliore disponibilità di larghezza di banda.

- In base al servizio, il mercato è segmentato in sicurezza dei dati, archiviazione dati, networking e altri. Il segmento dell'archiviazione dati ha detenuto la quota maggiore del mercato nel 2023. I servizi di archiviazione dati implicano l'implementazione di misure per archiviare e gestire in modo sicuro i dati in diversi ambienti cloud. Ciò comprende l'affrontare preoccupazioni come garantire la disponibilità dei dati, la perdita di controllo sui dati e la necessità di solide strategie di backup e ripristino dei dati.

- In termini di dimensioni aziendali, il mercato è diviso in grandi aziende e PMI. Il segmento delle grandi aziende ha detenuto una quota significativa del mercato nel 2023. Le grandi aziende utilizzano il modello di elaborazione distribuita per distribuire efficacemente varie fasi dei loro processi aziendali su una rete di computer, in genere strutturata in livelli di presentazione, applicazione e dati. Le grandi aziende stanno adottando sempre più strategie multi-cloud, distribuendo le loro esigenze di elaborazione su più provider cloud per evitare di essere bloccate in un singolo fornitore e rafforzare la loro resilienza.

- In base al settore verticale, il mercato del cloud distribuito è suddiviso in BFSI, sanità, commercio al dettaglio ed e-commerce, produzione, IT e telecomunicazioni, energia e servizi di pubblica utilità, media e intrattenimento, governo e difesa e altri. Il settore BFSI sta sempre più capitalizzando il potenziale della tecnologia cloud distribuita per affrontare sfide cruciali e promuovere l'innovazione. Questo settore affronta costantemente la minaccia imminente di attacchi informatici, la necessità di semplificare la raccolta dei dati dei clienti mantenendo l'integrità dei dati e la pressante necessità di aderire a rigorosi standard e normative di sicurezza.

Analisi della quota di mercato del cloud distribuito per area geografica

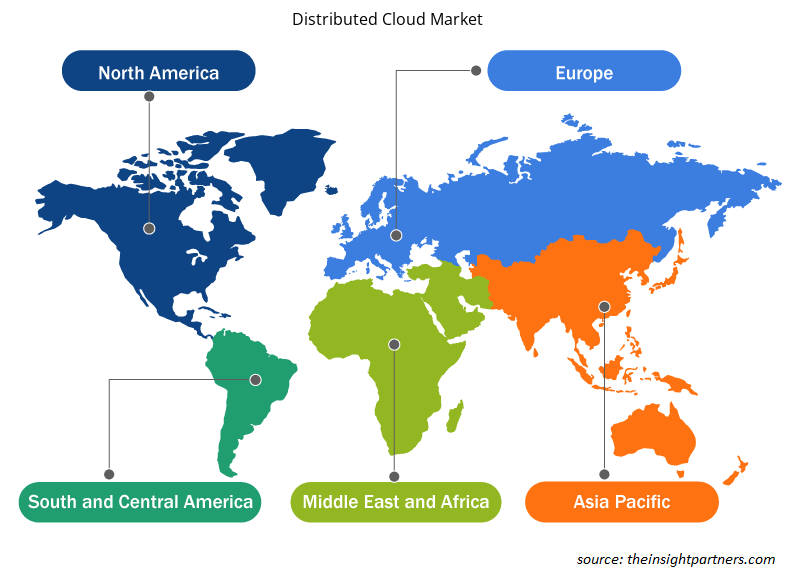

L'ambito geografico del rapporto sul mercato del cloud distribuito è suddiviso principalmente in cinque regioni: Nord America, Asia Pacifico, Europa, Medio Oriente e Africa, Sud e Centro America.

In Nord America, si prevede una crescita significativa nel mercato del cloud distribuito a causa delle maggiori attività di abilitazione del cloud e delle tendenze all'interno del mercato del cloud. Il cloud distribuito consente alle aziende di trasferire dati di qualsiasi dimensione senza costi aggiuntivi e può garantire la sovranità dei dati rispettando il Regolamento generale sulla protezione dei dati (GDPR). Fornisce un data lake alimentato dall'intelligenza artificiale che centralizza i dati per migliorare la qualità dell'analisi predittiva. Può essere utilizzato in diversi scenari, come produzione, IoT, apprendimento automatico e imaging.

Un mix eterogeneo di tecnologie e normative definisce il settore del cloud computing distribuito in Europa. Le tecnologie cloud si stanno espandendo, con conseguente adozione eterogenea di tecnologie cloud nei paesi dell'UE. L'UE sta compiendo notevoli sforzi per consentire la transizione verso l'edge e creare servizi cloud ed edge compatibili per sostenere l'istituzione di spazi dati europei unificati. Inoltre, c'è un'enfasi sulla garanzia della residenza dei dati, sul controllo del personale operativo e sulla riduzione al minimo degli effetti delle sfide giurisdizionali, in particolare nei settori regolamentati, tramite mezzi come l'European Cybersecurity Certification Scheme (EUCS) per i servizi cloud.

Approfondimenti regionali sul mercato del cloud distribuito

Le tendenze regionali e i fattori che influenzano il Distributed Cloud Market durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di Insight Partners. Questa sezione discute anche i segmenti e la geografia del Distributed Cloud Market in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e Sud e Centro America.

- Ottieni i dati specifici regionali per il mercato del cloud distribuito

Ambito del rapporto sul mercato del cloud distribuito

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2023 | 4,87 miliardi di dollari USA |

| Dimensioni del mercato entro il 2031 | 15,72 miliardi di dollari USA |

| CAGR globale (2023-2031) | 15,8% |

| Dati storici | 2021-2022 |

| Periodo di previsione | 2024-2031 |

| Segmenti coperti |

Per applicazione

|

| Regioni e Paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli attori del mercato del cloud distribuito: comprendere il suo impatto sulle dinamiche aziendali

Il mercato del Distributed Cloud Market sta crescendo rapidamente, spinto dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando le loro offerte, innovando per soddisfare le esigenze dei consumatori e capitalizzando sulle tendenze emergenti, il che alimenta ulteriormente la crescita del mercato.

La densità degli operatori di mercato si riferisce alla distribuzione di aziende o società che operano in un particolare mercato o settore. Indica quanti concorrenti (operatori di mercato) sono presenti in un dato spazio di mercato in relazione alle sue dimensioni o al valore di mercato totale.

Le principali aziende che operano nel mercato del cloud distribuito sono:

- Nuvola di Alibaba

- Servizi Web Amazon, Inc.

- IBM

- Oracolo

- Microsoft

Disclaimer : le aziende elencate sopra non sono classificate secondo un ordine particolare.

- Ottieni una panoramica dei principali attori del mercato del cloud distribuito

Notizie e sviluppi recenti sul mercato del cloud distribuito

Il mercato del cloud distribuito viene valutato raccogliendo dati qualitativi e quantitativi dopo la ricerca primaria e secondaria, che include importanti pubblicazioni aziendali, dati associativi e database. Di seguito sono elencati alcuni degli sviluppi nel mercato del cloud distribuito:

- Cloud Software Group Inc. e Microsoft Corp. hanno annunciato che stanno rafforzando la loro collaborazione attraverso un accordo di partnership strategica di otto anni. L'accordo rafforzerà la collaborazione go-to-market per la piattaforma desktop e applicazioni virtuali Citrix® e supporterà lo sviluppo di nuove soluzioni cloud e AI con una roadmap di prodotto integrata. Inoltre, Cloud Software Group si impegnerà per 1,65 miliardi di dollari nel cloud Microsoft e nelle sue capacità di AI generativa.

(Fonte: Microsoft, sito Web aziendale, aprile 2024)

- Oracle, Microsoft e OpenAl collaborano per estendere la piattaforma Microsoft Azure Al a Oracle Cloud Infrastructure (OCI) per fornire capacità aggiuntiva per OpenAl. Le funzionalità AI appositamente progettate di OCI consentono a startup e aziende di creare e addestrare modelli in modo più rapido e affidabile ovunque nel cloud distribuito di Oracle.

(Fonte: Oracle, sito Web aziendale, giugno 2024)

Copertura e risultati del rapporto sul mercato del cloud distribuito

Il rapporto “Dimensioni e previsioni del mercato del cloud distribuito (2021-2031)” fornisce un’analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni e previsioni del mercato cloud distribuito a livello globale, regionale e nazionale per tutti i segmenti di mercato chiave coperti dall'ambito

- Tendenze del mercato del cloud distribuito e dinamiche di mercato come driver, vincoli e opportunità chiave

- Analisi dettagliata delle cinque forze PEST/Porter e SWOT

- Analisi del mercato del cloud distribuito che copre le principali tendenze del mercato, il quadro globale e regionale, i principali attori, le normative e i recenti sviluppi del mercato

- Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa di calore, i principali attori e gli sviluppi recenti per il mercato del cloud distribuito

- Profili aziendali dettagliati

Ankita è una dinamica professionista della ricerca di mercato e della consulenza con oltre 8 anni di esperienza nei settori della tecnologia, dei media, dell'ICT, dell'elettronica e dei semiconduttori. Ha guidato e portato a termine con successo oltre 100 incarichi di consulenza e ricerca per clienti globali come Microsoft, Oracle, NEC Corporation, SAP, KPMG ed Expeditors International. Le sue competenze principali includono la valutazione del mercato, l'analisi dei dati, le previsioni, la formulazione di strategie, l'intelligence competitiva e la redazione di report.

Ankita è esperta nella gestione di cicli di progetto completi, dalla progettazione di proposte pre-vendita e discussioni con i clienti fino alla fornitura di insight fruibili post-vendita. È esperta nella gestione di team interfunzionali, nella strutturazione di moduli di ricerca complessi e nell'allineamento delle soluzioni agli obiettivi aziendali specifici del cliente. Le sue eccellenti capacità di comunicazione, leadership e presentazione le hanno permesso di fornire costantemente risultati orientati al valore in contesti di mercato in rapida evoluzione.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative