Crescita, dimensioni, quota, tendenze, analisi dei principali attori e previsioni del mercato del trattamento delle infezioni acquisite dall'ospedale fino al 2030

Rapporto di analisi sulle dimensioni e le previsioni del mercato del trattamento delle infezioni contratte in ospedale (2020-2030), quota globale e regionale, tendenze e opportunità di crescita. Copertura: per classe di farmaci (farmaci antibatterici, farmaci antivirali, farmaci antimicotici e altri), tipo di infezione (infezioni del tratto urinario, polmonite associata alla ventilazione, infezioni del sito chirurgico, infezioni del flusso sanguigno e altre infezioni ospedaliere), canale di distribuzione (farmacie ospedaliere, farmacie al dettaglio, e-commerce e altri) e area geografica (Nord America, Europa, Asia Pacifico, Sud e Centro America e Medio Oriente e Africa).

- Stato : Dati rilasciati

- Codice del report : TIPRE00029976

- Categoria : Scienze della vita

- Numero di pagine : 171

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : June 11, 2024

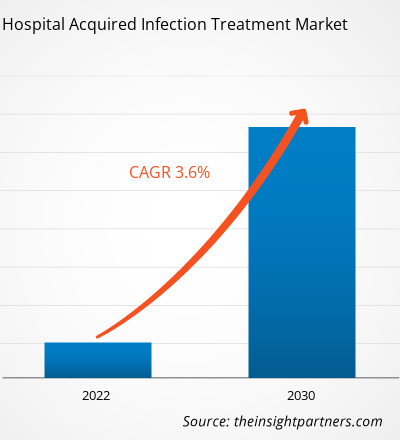

[Rapporto di ricerca] Si prevede che il mercato del trattamento delle infezioni acquisite in ospedale crescerà da 15.099,19 milioni di dollari nel 2022 a 19.978,39 milioni di dollari entro il 2030; si prevede che registrerà un CAGR del 3,6% dal 2022 al 2030.

Approfondimenti di mercato e opinioni degli analisti:

Le infezioni nosocomiali (HAI), note anche come infezioni nosocomiali, possono svilupparsi in vari contesti, tra cui ospedali, istituti di assistenza a lungo termine e ambulatoriali, e possono anche manifestarsi dopo la dimissione. Le HAI possono anche riguardare infezioni professionali che colpiscono gli operatori sanitari. I fattori chiave che guidano la crescita del mercato del trattamento delle infezioni nosocomiali sono l'elevata prevalenza di HAI e la crescente attenzione alla sicurezza dei pazienti e alla qualità dell'assistenza. Tuttavia, la minaccia della resistenza antimicrobica ostacola la crescita del mercato del trattamento delle infezioni nosocomiali .

Fattori trainanti e limiti della crescita:

Le infezioni del flusso sanguigno associate al catetere centrale, le infezioni del tratto urinario associate al catetere e la polmonite associata alla ventilazione sono alcuni esempi di infezioni correlate all'assistenza sanitaria (HAI). Queste infezioni, note come infezioni del sito chirurgico, possono verificarsi anche nei siti chirurgici. Secondo il rapporto dei Centers for Disease Control and Prevention (CDC) "2020 National and State Healthcare-Associated Infections Progress Report" pubblicato nel 2021, i casi di infezioni del flusso sanguigno associate al catetere centrale, batteriemia da Staphylococcus aureus resistente alla meticillina (MRSA) ed eventi associati alla ventilazione sono aumentati rispettivamente del 24%, 35% e 15% negli Stati Uniti tra il 2019 e il 2020.

Inoltre, secondo il rapporto di gennaio 2022 del National Healthcare Safety Network (NHSN), le infezioni del tratto urinario (UTI) sono il quinto tipo più comune di infezione associata all'assistenza sanitaria. Le UTI rappresentano oltre il 9,5% delle condizioni ospedaliere per acuti. L'infezione del tratto urinario associata al catetere (CAUTI) è causata dai cateteri urinari utilizzati per drenare l'urina dalla vescica. La CAUTI è una delle infezioni più frequenti tra i pazienti ospedalizzati con UTI. Secondo i Centers for Disease Control and Prevention (CDC), quasi il 75% delle infezioni è correlato a un catetere urinario. Durante la degenza ospedaliera, dal 15% al 25% dei pazienti ospedalizzati ha bisogno di utilizzare cateteri urinari. L'uso prolungato del catetere urinario è il fattore di rischio più importante per contrarre la CAUTI. Le complicazioni della CAUTI comportano sofferenza per il paziente, ricoveri ospedalieri prolungati, maggiori costi di trattamento e persino la morte.

Inoltre, secondo il CDC, le infezioni delle vie urinarie sono responsabili di oltre 13.000 decessi ogni anno. La cistite acuta non complicata causa circa sei giorni di disagio, con conseguenti circa 7 milioni di visite ambulatoriali ogni anno a un costo di 1,6 miliardi di dollari. Di conseguenza, il numero crescente di casi di infezioni ospedaliere comporta un notevole onere finanziario per il sistema sanitario. La crescente prevalenza di CAUTI, combinata con la crescente domanda di farmaci per il trattamento, sta spingendo il mercato.

Tuttavia, la resistenza antimicrobica rappresenta una sfida significativa per il trattamento delle infezioni ospedaliere, limitando l'efficacia degli agenti antimicrobici esistenti e rendendo necessario lo sviluppo di nuove strategie di trattamento e alternative antimicrobiche per combattere efficacemente i patogeni resistenti.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, comprese parti di questo report, o analisi a livello nazionale, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato del trattamento delle infezioni contratte in ospedale: approfondimenti strategici

-

Scopri le principali tendenze di mercato in questo rapporto.Questo campione GRATUITO includerà analisi di dati che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Segmentazione e ambito del report:

Il mercato globale del trattamento delle infezioni acquisite in ospedale è segmentato in base alla classe di farmaci, al tipo di infezione e al canale di distribuzione. In base alla classe di farmaci, il mercato del trattamento delle infezioni acquisite in ospedale è segmentato in farmaci antibatterici, farmaci antivirali , farmaci antimicotici e altri. In base al tipo di infezione, il trattamento delle infezioni acquisite in ospedale è differenziato in infezioni del tratto urinario, polmonite associata alla ventilazione, infezioni del sito chirurgico, infezioni del flusso sanguigno e altre infezioni ospedaliere. In base al canale di distribuzione, il mercato è segmentato in farmacie ospedaliere, farmacie al dettaglio, e-commerce e altri. Il mercato del trattamento delle infezioni acquisite in ospedale, in base alla geografia, è segmentato in Nord America (Stati Uniti, Canada e Messico), Europa (Germania, Francia, Italia, Regno Unito, Russia e resto d'Europa), Asia Pacifico (Australia, Cina, Giappone, India, Corea del Sud e resto dell'Asia Pacifico), Medio Oriente e Africa (Sudafrica, Arabia Saudita, Emirati Arabi Uniti e resto del Medio Oriente e Africa) e Sud e Centro America (Brasile, Argentina e resto del Sud e Centro America).

Analisi segmentale:

Il mercato del trattamento delle infezioni acquisite in ospedale, per classe di farmaci, è segmentato in farmaci antibatterici, farmaci antivirali, farmaci antimicotici e altri. Il segmento dei farmaci antibatterici ha detenuto la quota di mercato più grande nel 2022 e si prevede che registrerà il CAGR più elevato nel periodo 2022-2030.

Il mercato del trattamento delle infezioni acquisite in ospedale, per tipo di infezione, è segmentato in infezioni del tratto urinario , polmonite associata alla ventilazione, infezioni del sito chirurgico, infezioni del flusso sanguigno e altre infezioni ospedaliere. Il segmento delle infezioni del tratto urinario ha detenuto la quota di mercato più grande nel 2022. Tuttavia, si prevede che il segmento della polmonite associata alla ventilazione registrerà il CAGR più elevato dal 2022 al 2030.

Il mercato del trattamento delle infezioni acquisite in ospedale, per canale di distribuzione, è segmentato in farmacie ospedaliere, farmacie al dettaglio, e-commerce e altri. Nel 2022, il segmento delle farmacie ospedaliere ha detenuto la quota di mercato maggiore e si prevede che lo stesso segmento registrerà il CAGR più elevato nel periodo 2022-2030.

Analisi regionale:

In base alla geografia, il mercato globale del trattamento delle infezioni ospedaliere è suddiviso in cinque regioni chiave: Nord America, Europa, Asia Pacifico, Sud e Centro America, Medio Oriente e Africa.

Nel 2022, il Nord America deteneva la quota maggiore del mercato globale del trattamento delle infezioni acquisite in ospedale. Gli Stati Uniti hanno un'elevata prevalenza di HAI, che spinge la crescita del mercato del trattamento delle infezioni acquisite in ospedale. Secondo il CDC, in un dato giorno, circa 1 paziente ospedaliero su 31 ha almeno una HAI. Allo stesso modo, secondo l'Office of Disease Prevention and Health Promotion, le HAI e altre infezioni possono portare alla sepsi e causano circa 1,7 milioni di casi di malattia e 270.000 decessi all'anno negli Stati Uniti. Pertanto, l'elevata prevalenza di HAI tra le persone negli Stati Uniti alimenta la crescita del mercato del trattamento delle infezioni acquisite in ospedale.

Sviluppi del settore e opportunità future:

Di seguito sono elencate le varie iniziative intraprese dai principali attori che operano nel mercato globale del trattamento delle infezioni ospedaliere:

- A maggio 2023, Innoviva Specialty Therapeutics ha annunciato che la Food and Drug Administration (FDA) statunitense aveva approvato XACDURO (sulbactam per iniezione; durlobactam per iniezione), confezionato congiuntamente per uso endovenoso in pazienti di età pari o superiore a 18 anni per il trattamento della polmonite batterica acquisita in ospedale e della polmonite batterica associata alla ventilazione (HABP/VABP) causata da isolati sensibili del complesso Acinetobacter baumannii-calcoaceticus (Acinetobacter). Innoviva Specialty Therapeutics ha dichiarato di essere focalizzata sulla fornitura di terapie innovative in terapia intensiva e malattie infettive.

- Nel maggio 2023, i ricercatori dell'Indian Institute of Science Education and Research (IISER) di Pune e del Central Drug Research Institute (CSIR-CDRI) di Lucknow hanno annunciato di aver scoperto un potenziale nuovo antibiotico contro l'Acinetobacter baumannii, che causa frequentemente infezioni ospedaliere.

- Nel settembre 2020, Shionogi & Co Ltd ha annunciato che la FDA aveva approvato una domanda supplementare di nuovo farmaco (sNDA) per FETROJA (cefiderocol) per il trattamento di pazienti di età pari o superiore a 18 anni affetti da polmonite batterica nosocomiale e polmonite batterica associata alla ventilazione (HABP/VABP) causate da microrganismi Gram-negativi sensibili quali Enterobacter cloacae complex, Klebsiella pneumoniae, Acinetobacter baumannii complex, Escherichia coli, Pseudomonas aeruginosa e Serratia marcescens.

- Nel giugno 2020, Merck ha annunciato che la Food and Drug Administration (FDA) statunitense aveva approvato una domanda supplementare di nuovo farmaco (sNDA) per RECARBRIO (imipenem, cilastatina e relebactam) per il trattamento di pazienti di età pari o superiore a 18 anni affetti da polmonite batterica acquisita in ospedale e polmonite batterica associata alla ventilazione (HABP/VABP), causate da microrganismi Gram-negativi sensibili quali il complesso Acinetobacter calcoaceticus-baumannii, Klebsiella oxytoca, Klebsiella pneumoniae, Enterobacter cloacae, Escherichia coli, Haemophilus influenzae, Klebsiella aerogenes, Pseudomonas aeruginosa e Serratia marcescens.

Approfondimenti regionali sul mercato del trattamento delle infezioni contratte in ospedale

Le tendenze regionali e i fattori che influenzano il mercato del trattamento delle infezioni acquisite in ospedale durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di Insight Partners. Questa sezione discute anche i segmenti del mercato del trattamento delle infezioni acquisite in ospedale e la geografia in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e America meridionale e centrale.

- Ottieni i dati specifici regionali per il mercato del trattamento delle infezioni contratte in ospedale

Ambito del rapporto di mercato sul trattamento delle infezioni contratte in ospedale

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2022 | 15.099,19 milioni di dollari USA |

| Dimensioni del mercato entro il 2030 | 19.978,39 milioni di dollari USA |

| CAGR globale (2022-2030) | 3,6% |

| Dati storici | 2020-2022 |

| Periodo di previsione | 2022-2030 |

| Segmenti coperti |

Per classe di farmaci

|

| Regioni e Paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato del trattamento delle infezioni contratte in ospedale: comprendere il suo impatto sulle dinamiche aziendali

Il mercato del trattamento delle infezioni acquisite in ospedale sta crescendo rapidamente, spinto dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando le loro offerte, innovando per soddisfare le esigenze dei consumatori e capitalizzando sulle tendenze emergenti, il che alimenta ulteriormente la crescita del mercato.

La densità degli operatori di mercato si riferisce alla distribuzione di aziende o società che operano in un particolare mercato o settore. Indica quanti concorrenti (operatori di mercato) sono presenti in un dato spazio di mercato in relazione alle sue dimensioni o al valore di mercato totale.

Le principali aziende che operano nel mercato del trattamento delle infezioni nosocomiali sono:

- Merck & Co Inc

- Pfizer Inc

- AbbVie Inc

- Paratek Pharmaceuticals Inc

- Eugia Stati Uniti LLC

Disclaimer : le aziende elencate sopra non sono classificate secondo un ordine particolare.

- Ottieni una panoramica dei principali attori del mercato del trattamento delle infezioni contratte in ospedale

Scenario competitivo e aziende chiave:

Merck & Co Inc, Pfizer Inc, AbbVie Inc, Paratek Pharmaceuticals Inc, Eugia US LLC, Abbott Laboratories, Cumberland Pharmaceuticals Inc, Innoviva Specialty Therapeutics Inc, Cipla Ltd ed Eli Lilly and Company sono tra i principali attori che operano nel mercato del trattamento delle infezioni acquisite in ospedale. Queste aziende si concentrano su nuove tecnologie, progressi nei prodotti esistenti ed espansioni geografiche per soddisfare la crescente domanda dei consumatori in tutto il mondo e aumentare la loro gamma di prodotti nei portafogli specialistici.

Mrinal è un'analista di ricerca esperta con oltre 8 anni di esperienza nella consulenza e nell'intelligence di mercato nel settore delle scienze biologiche. Grazie a una mentalità strategica e a un costante impegno verso l'eccellenza, ha maturato una profonda competenza nelle previsioni farmaceutiche, nella valutazione delle opportunità di mercato e nello sviluppo di benchmark di settore. Il suo lavoro è incentrato sulla fornitura di insight fruibili che consentono ai clienti di prendere decisioni strategiche consapevoli.

Il punto di forza di Mrinal risiede nella capacità di tradurre complessi set di dati quantitativi in business intelligence significative. Il suo acume analitico è fondamentale per definire strategie di go-to-market (GTM) e individuare opportunità di crescita nei settori farmaceutico e dei dispositivi medici. In qualità di consulente di fiducia, si concentra costantemente sulla semplificazione dei processi di flusso di lavoro e sulla definizione di best practice, promuovendo così l'innovazione e l'efficienza operativa per i suoi clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative