Analisi e previsioni di mercato della diagnostica per la malaria per dimensione, quota, crescita, tendenze 2030

Dimensioni e previsioni del mercato della diagnostica della malaria (2020-2030), quota globale e regionale, trend e opportunità di crescita. Copertura del rapporto di analisi: per tecnologia [microscopia, test diagnostici rapidi (RDT) e test diagnostici molecolari], utente finale (ospedali e cliniche, centri diagnostici e altri) e area geografica (Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e Sud e Centro America).

- Stato : Dati rilasciati

- Codice del report : TIPRE00007610

- Categoria : Scienze della vita

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : June 05, 2024

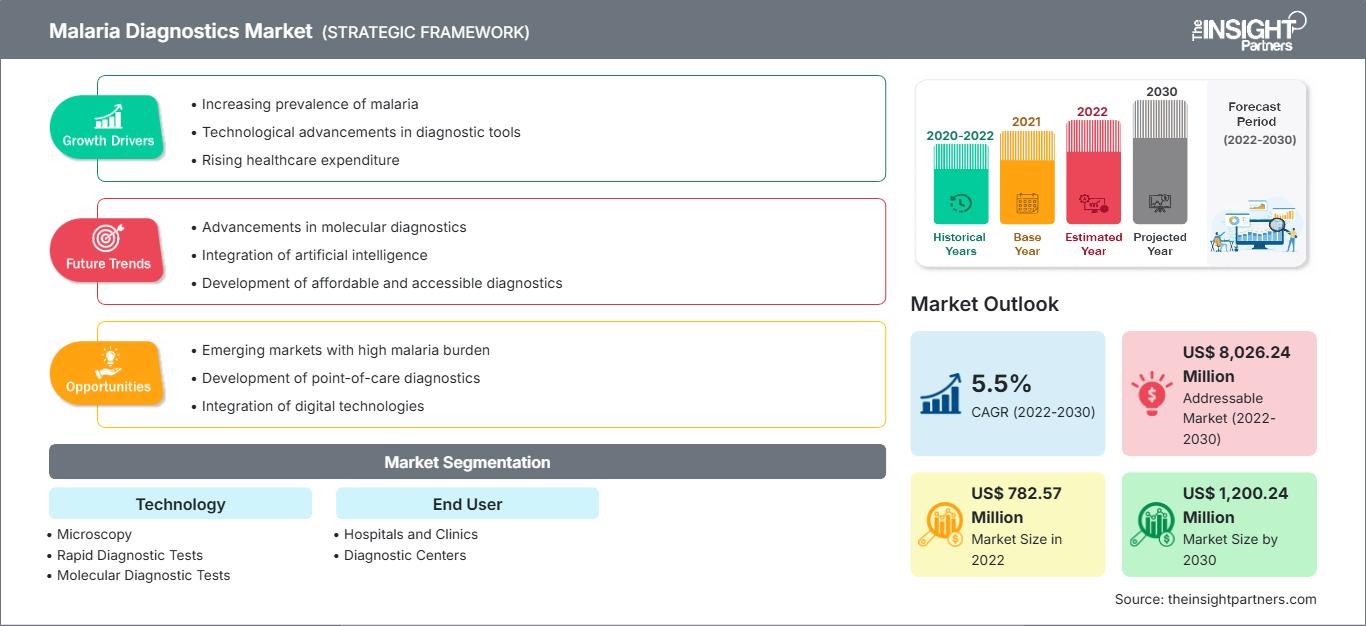

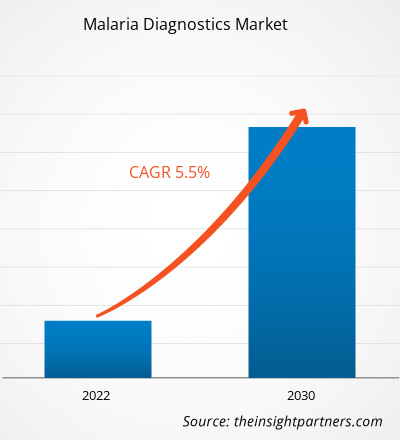

[Rapporto di ricerca] Si prevede che il mercato della diagnostica per la malaria crescerà da 782,57 milioni di dollari nel 2022 a 1.200,24 milioni di dollari entro il 2030; si stima che il mercato registrerà un CAGR del 5,5% tra il 2022 e il 2030.

Approfondimenti di mercato e analisi :

La malaria è una malattia potenzialmente letale causata dal parassita Plasmodium. Il mercato della diagnostica per la malaria è in crescita grazie all'elevata incidenza della malattia nei paesi a basso reddito e ai programmi di eliminazione della malaria implementati a livello globale da organizzazioni internazionali e nazionali. Il crescente lancio di strumenti diagnostici avanzati e l'intensificarsi delle attività di ricerca per terapie efficaci stanno ulteriormente contribuendo alla crescita del mercato.

Prima della pandemia di COVID-19, quasi un terzo delle nazioni endemiche stava progredendo verso gli obiettivi internazionali. Molte nazioni a bassa incidenza facevano parte dell'"Iniziativa Eliminazione 2025" dell'OMS, rappresentata da un gruppo di 25 nazioni che si impegnano a eliminare potenzialmente la malaria entro il 2025. D'altro canto, i progressi si sono fermati in circa un terzo dei paesi, mentre negli altri l'incidenza della malaria è aumentata. I paesi con un carico di malattia maggiore stanno mostrando una maggiore propensione a utilizzare i dati dei test diagnostici per stratificare e focalizzare interventi geograficamente adeguati, indipendentemente dalla continua importanza dei test e dello screening nei tentativi di eradicazione.

I casi e i decessi per malaria sono aumentati nel primo anno dell'epidemia di COVID-19 a causa di lievi interruzioni nella gestione dei casi e negli sforzi preventivi. Tuttavia, un possibile scenario peggiore – il raddoppio dei decessi per malaria – è stato evitato grazie agli sforzi congiunti dell'OMS, dei Programmi Nazionali per la Malaria e dei partner. Le difficoltà nell'ottenere le necessarie forniture antimalariche e l'incertezza su come la pandemia abbia influenzato le misure di gestione della malaria sono state determinanti.

Fattori della crescita:

La malaria, una delle malattie febbrili acute, è causata da parassiti del genere Plasmodium e si diffonde attraverso le zanzare femmine infette del genere Anopheles. Cinque specie di parassiti nell'uomo causano principalmente la malaria e due di queste specie – Plasmodium falciparum e P. vivax – sono considerate la minaccia maggiore. Inoltre, P. falciparum è il parassita della malaria più letale ed è il più diffuso nel continente africano. Inoltre, P. vivax è il parassita della malaria dominante nella maggior parte dei paesi al di fuori dell'Africa subsahariana. Secondo il World Malaria Report (WMR) 2020 dell'Organizzazione Mondiale della Sanità (OMS), sono stati segnalati 241 milioni di casi di malaria in tutto il mondo, rispetto ai 227 milioni di casi registrati nel 2019. Secondo la stessa fonte, il numero di decessi causati dalla malaria aumenta di 69.000 unità all'anno. Circa due terzi di questi decessi, ovvero 47.000, sono stati causati dalle interruzioni dei servizi sanitari durante la pandemia di COVID-19; il restante terzo dei decessi, ovvero 22.000, riflette una recente modifica nella metodologia dell'OMS per il calcolo della mortalità per malaria (indipendentemente dalle interruzioni dovute al COVID-19).

Nel 2020, circa il 95% dei casi globali e circa il 96% dei decessi causati dalla malaria sono stati segnalati nella regione africana dell'OMS, e circa l'80% dei decessi totali segnalati ha riguardato bambini di età pari o inferiore a 5 anni. Secondo il WMR 2021, il 2% del carico globale di malaria è stato registrato nei paesi del Sud-est asiatico, dove l'India ha rappresentato l'83% dei casi stimati di malaria e l'82% dei decessi associati alla malattia nel 2020. Pertanto, la crescente prevalenza della malaria in diverse regioni del mondo stimola la crescita del mercato della diagnostica per la malaria.

Sul mercato è disponibile un numero limitato di prodotti mRDT prequalificati dall'OMS che non sono Pf. Nonostante la disponibilità di un'ampia gamma di prodotti mRDT prequalificati dall'OMS, la domanda si concentra su un sottoinsieme preferito di prodotti e produttori specifici. Ciò limita la capacità del mercato di garantire la diversificazione dell'offerta, la sicurezza e la capacità produttiva. In linea con ciò, i produttori si trovano ad affrontare sfide come la bassa domanda di prodotti da parte di alcuni paesi, nonché la loro riluttanza e mancanza di interesse nell'adottare prodotti alternativi. L'adozione di marchi alternativi può essere innescata dal cambio di marchi selezionati per gli algoritmi nazionali o da implicazioni di costo.

Personalizza questo rapporto in base alle tue esigenze

Potrai personalizzare gratuitamente qualsiasi rapporto, comprese parti di questo rapporto, o analisi a livello di paese, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato della diagnostica della malaria: Approfondimenti strategici

-

Ottieni le principali tendenze chiave del mercato di questo rapporto.Questo campione GRATUITO includerà l'analisi dei dati, che vanno dalle tendenze di mercato alle stime e alle previsioni.

Segmentazione e ambito del rapporto:

Il mercato della diagnostica della malaria è segmentato in base alla tecnologia e all'utente finale. Il mercato della diagnostica della malaria, in base alla tecnologia, è suddiviso in microscopia, test diagnostici rapidi (RDT) e test diagnostici molecolari. Il segmento dei test diagnostici rapidi (RDT) ha detenuto la quota di mercato maggiore nel 2022 e si stima che registrerà il CAGR più elevato nel mercato tra il 2022 e il 2030. Il mercato della diagnostica della malaria, in base all'utente finale, è suddiviso in ospedali e cliniche, centri diagnostici e altri. Il segmento ospedali e cliniche ha detenuto la quota di mercato maggiore nel 2022. Si prevede che il segmento dei centri diagnostici registrerà il CAGR più elevato sul mercato tra il 2022 e il 2030.

Analisi segmentale:

Il mercato della diagnostica della malaria, in base alla tecnologia, è segmentato in microscopia, test diagnostici rapidi (RDT) e test diagnostici molecolari.

Il segmento dei test diagnostici rapidi (RDT) ha detenuto la quota di mercato maggiore nel 2022 e si prevede che registrerà il CAGR più elevato sul mercato tra il 2022 e il 2030. Dimostrando la presenza di parassiti della malaria nel sangue umano, i test diagnostici rapidi (RDT) aiutano nella diagnosi della malaria. Gli RDT offrono un'alternativa alla diagnosi clinica o alla microscopia, soprattutto in situazioni in cui l'accesso a servizi di microscopia di alta qualità è limitato. Plasmodium falciparum o P. vivax è l'unica specie che alcuni test diagnostici rapidi (RDT) possono identificare, ma altri possono identificare quattro specie: P. falciparum, P. vivax, P. malariae e P. ovale. Di solito, per il test si utilizza una puntura del dito.

Il mercato della diagnostica per la malaria, per utente finale, è segmentato in ospedali e cliniche, centri diagnostici e altri. Ospedali e cliniche si stanno evolvendo notevolmente con l'aumento del numero di pazienti in tutto il mondo. Offrono trattamenti altamente efficaci in contesti a basso costo. La crescente enfasi sull'utilizzo dei test diagnostici rapidi (RDT) per i loro rapidi tempi di risposta, i bassi costi e la comoda accessibilità è una delle cause principali del predominio delle cliniche nel mercato della diagnostica per la malaria.

Analisi regionale:

Il mercato globale della diagnostica per la malaria è segmentato geograficamente in Nord America, Europa, Asia-Pacifico, America meridionale e centrale e Medio Oriente e Africa. Grazie ai crescenti investimenti da parte di paesi sviluppati come gli Stati Uniti e gli Stati Uniti, all'aumento della popolazione di pazienti e alla crescente enfasi dell'Organizzazione Mondiale della Sanità (OMS) sulla riduzione del tasso di mortalità per malaria nei paesi africani, si prevede che la regione del Medio Oriente e dell'Africa manterrà la sua posizione dominante sul mercato nel periodo di previsione. Sulla base dei dati pubblicati dall'OMS a luglio 2022, è probabile che l'Africa subsahariana rappresenti circa il 95% dei casi di malattia e il 96% dei decessi.

Mercato della diagnostica della malariaLe tendenze regionali e i fattori che influenzano il mercato della diagnostica della malaria durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di The Insight Partners. Questa sezione illustra anche i segmenti e la geografia del mercato della diagnostica della malaria in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa, America meridionale e centrale.

Ambito del rapporto di mercato sulla diagnostica della malaria

| Attributo del rapporto | Dettagli |

|---|---|

| Dimensioni del mercato in 2022 | US$ 782.57 Million |

| Dimensioni del mercato per 2030 | US$ 1,200.24 Million |

| CAGR globale (2022 - 2030) | 5.5% |

| Dati storici | 2020-2022 |

| Periodo di previsione | 2022-2030 |

| Segmenti coperti |

By Tecnologia

|

| Regioni e paesi coperti |

Nord America

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato della diagnostica della malaria: comprendere il suo impatto sulle dinamiche aziendali

Il mercato della diagnostica per la malaria è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

- Ottieni il Mercato della diagnostica della malaria Panoramica dei principali attori chiave

Sviluppi del settore e opportunità future:

Di seguito sono elencati vari sviluppi strategici da parte dei principali attori che operano nel mercato della diagnostica della malaria:

- Nel febbraio 2022, il Kenya Medical Research Institute (KEMRI) ha lanciato Plasmochek per il test della malaria. Plasmochek è progettato per rilevare il plasmodium, un parassita responsabile della malaria. Il kit utilizza anticorpi specifici per la proteina II ricca di istidina del Plasmodium falciparum e lattato deidrogenasi del Plasmodium per rilevare le infezioni da malaria.

- Nel dicembre 2019, Access Bio e Global Good (un partner di collaborazione del primo) hanno sviluppato un nuovo test diagnostico rapido ultrasensibile (uRDT) che è cinque volte più sensibile nell'identificazione degli antigeni della proteina 2 ricca di istidina (HRP2) rispetto agli uRDT attualmente disponibili. Inoltre, sono stati creati diversi strumenti per migliorare la diagnosi della malaria.

Panorama competitivo e aziende chiave:

Access Bio., Inc.; Abbott Laboratories; Premier Medical Corporation Pvt. Ltd.; Sysmex Partec GmbH; bioMerieux; Beckman Coulter Inc.; Siemens Healthineers; Leica Microsystems GmbH; Nikon Corporation; Olympus Corporation; e Bio-Rad Laboratories Inc. sono le aziende di spicco nel mercato della diagnostica della malaria. Queste aziende si concentrano su nuove tecnologie, sull'aggiornamento dei prodotti esistenti e sull'espansione geografica per soddisfare la crescente domanda dei consumatori in tutto il mondo.

Mrinal è un'analista di ricerca esperta con oltre 8 anni di esperienza nella consulenza e nell'intelligence di mercato nel settore delle scienze biologiche. Grazie a una mentalità strategica e a un costante impegno verso l'eccellenza, ha maturato una profonda competenza nelle previsioni farmaceutiche, nella valutazione delle opportunità di mercato e nello sviluppo di benchmark di settore. Il suo lavoro è incentrato sulla fornitura di insight fruibili che consentono ai clienti di prendere decisioni strategiche consapevoli.

Il punto di forza di Mrinal risiede nella capacità di tradurre complessi set di dati quantitativi in business intelligence significative. Il suo acume analitico è fondamentale per definire strategie di go-to-market (GTM) e individuare opportunità di crescita nei settori farmaceutico e dei dispositivi medici. In qualità di consulente di fiducia, si concentra costantemente sulla semplificazione dei processi di flusso di lavoro e sulla definizione di best practice, promuovendo così l'innovazione e l'efficienza operativa per i suoi clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative