Strategie di mercato della farina biologica, principali attori, opportunità di crescita, analisi e previsioni entro il 2031

Dimensioni e previsioni del mercato della farina biologica (2021-2031), quota globale e regionale, trend e opportunità di crescita. Copertura del rapporto di analisi: per tipo di prodotto (farina di frumento, farina d'avena, farina di mais, farina di riso e altri), categoria (convenzionale e senza glutine), canale di distribuzione (supermercati e ipermercati, minimarket, vendita al dettaglio online e altri).

- Stato : Edito

- Codice del report : TIPRE00017870

- Categoria : Cibo e bevande

- Numero di pagine : 223

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : June 14, 2024

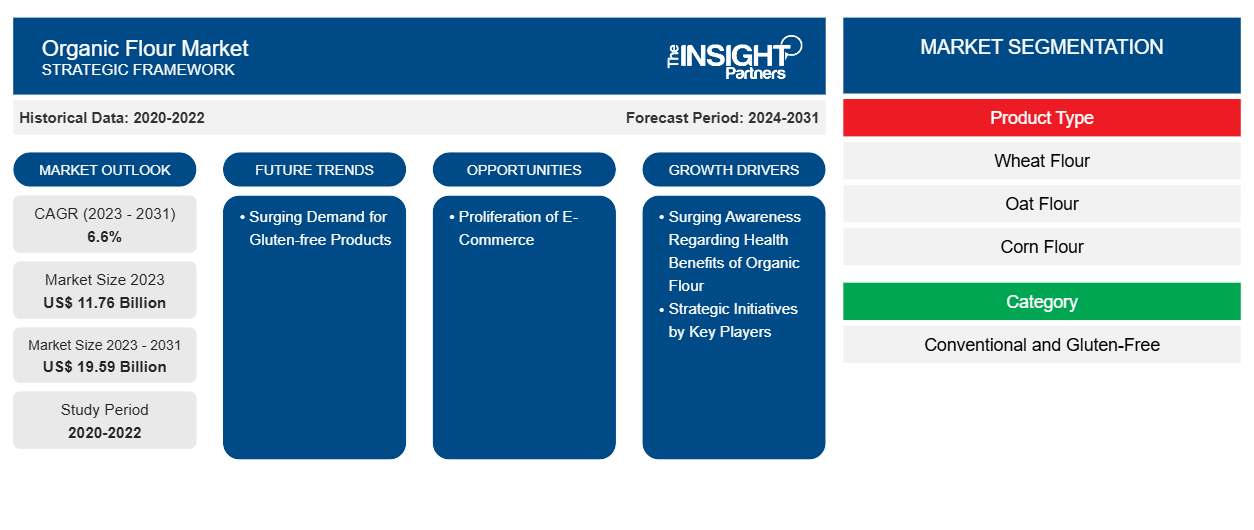

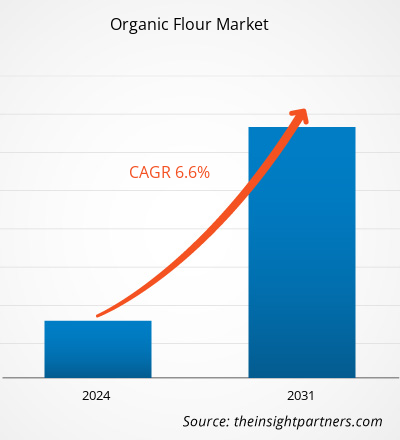

Si prevede che il mercato della farina biologica crescerà da 11,76 miliardi di dollari nel 2023 a 19,59 miliardi di dollari entro il 2031; si stima che registrerà un CAGR del 6,6% dal 2023 al 2031.CAGR of 6.6% from 2023 to 2031.

Approfondimenti di mercato e opinioni degli analisti:

La domanda di farina biologica è aumentata perché i consumatori stanno diventando più attenti alla salute e cercano prodotti biologici. La farina biologica è prodotta da cereali coltivati senza pesticidi tossici, fertilizzanti sintetici o tecniche di ingegneria genetica. La sua domanda è aumentata a causa delle crescenti preferenze dei consumatori per prodotti alimentari più sani, rispettosi dell'ambiente e prodotti eticamente. Inoltre, il ricco valore nutrizionale e i potenziali benefici per la salute degli alimenti biologici hanno contribuito all'aumento della domanda. Questa impennata fa parte della tendenza più ampia nel settore degli alimenti biologici, che ha visto una crescita significativa negli ultimi anni. Inoltre, a causa di una crescente consapevolezza della sostenibilità ambientale, molti consumatori stanno optando per prodotti biologici per supportare pratiche agricole più ecologiche che danno priorità alla salute del suolo e alla biodiversità. Inoltre, il desiderio di supportare gli agricoltori locali e i piccoli produttori e di offrire trasparenza nella produzione alimentare contribuisce alla crescente domanda di farina biologica.

Fattori di crescita e sfide:

Iniziative strategiche come fusioni e acquisizioni, partnership, lanci di campagne e lanci di prodotti intrapresi da vari attori del mercato per rafforzare le proprie posizioni e capitalizzare le opportunità emergenti dovrebbero contribuire alla crescita delle dimensioni del mercato della farina biologica . Ad esempio, nel 2020, ADM ha acquisito il restante 50% delle azioni della società britannica di macinazione della farina biologica Gleadell Agriculture Ltd. Questa acquisizione ha consentito ad ADM di espandere la propria presenza nel mercato della farina biologica e rafforzare le proprie capacità di filiera. Anche i lanci di campagne mirati a sensibilizzare e istruire i consumatori sui vantaggi della farina biologica svolgono un ruolo fondamentale nel guidare la crescita del mercato. Gli attori chiave spesso investono in campagne di marketing che evidenziano i vantaggi nutrizionali, la sostenibilità ambientale e gli standard qualitativi della farina biologica. Queste campagne aiutano a creare domanda, a modellare le preferenze dei consumatori e a differenziare i prodotti di farina biologica dalle alternative convenzionali. Queste campagne includono pubblicità digitale , promozioni sui social media e contenuti educativi per sensibilizzare i consumatori sui vantaggi dell'utilizzo della farina biologica nella cottura e nella cucina.

I lanci di prodotti sono essenziali per mantenere la competitività e soddisfare le preferenze dei consumatori in continua evoluzione nel mercato della farina biologica. I principali attori innovano e introducono continuamente nuovi prodotti di farina biologica su misura per specifiche esigenze dietetiche, preferenze di gusto e occasioni. Ad esempio, le varianti di farina biologica senza glutine soddisfano i consumatori con intolleranza o sensibilità al glutine, mentre le farine speciali come la farina di mandorle o la farina di cocco attraggono i consumatori attenti alla salute che cercano ingredienti alternativi per la cottura. Ad esempio, nel 2021, Hodgson Mill ha introdotto una nuova linea di farina biologica, tra cui farina integrale biologica, farina multiuso biologica e farina per dolci biologica, per soddisfare i consumatori che cercano alternative biologiche per le loro esigenze di cottura e dimostrare l'impegno di Hodgson Mill nel soddisfare la crescente domanda di opzioni di farina biologica. Inoltre, diverse aziende stanno entrando nel mercato biologico lanciando prodotti come la farina biologica.

Si prevede che le conformità normative associate alla farina biologica, come gli standard rigorosi e i processi di certificazione imposti dalle autorità di regolamentazione, tra cui l'USDA e il Regolamento biologico dell'UE, limiteranno la crescita del mercato globale della farina biologica. L'acquisizione della certificazione biologica comporta ispezioni complete, documentazione e aderenza a specifiche pratiche di agricoltura biologica, tutte cose che richiedono un notevole investimento di tempo e denaro da parte dei produttori. Questo processo esaustivo può fungere da deterrente per i produttori più piccoli o quelli con risorse limitate, ostacolando la capacità di entrare o espandersi nel mercato della farina biologica.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, comprese parti di questo report, o analisi a livello nazionale, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato della farina biologica: approfondimenti strategici

-

Scopri le principali tendenze di mercato in questo rapporto.Questo campione GRATUITO includerà analisi di dati che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Segmentazione e ambito del report:

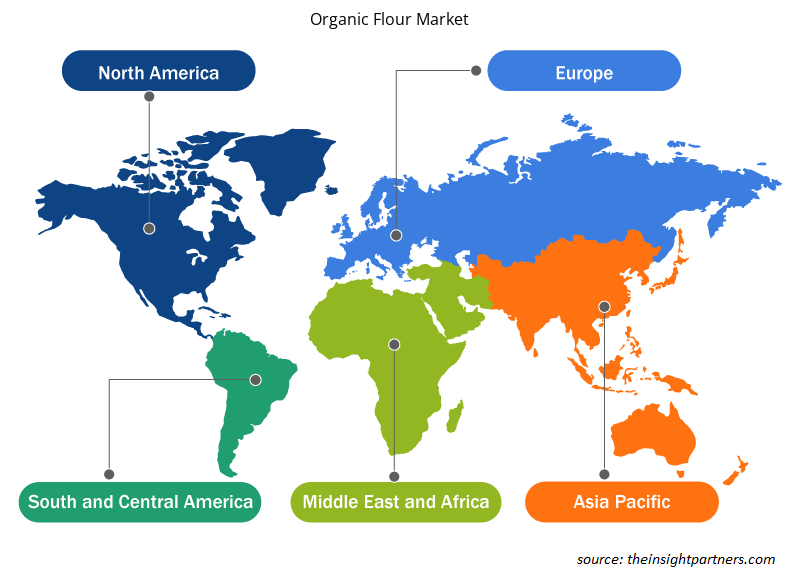

L'"Analisi del mercato globale della farina biologica" è stata eseguita considerando i seguenti segmenti: tipo di prodotto, categoria, canale di distribuzione e geografia. In base al tipo di prodotto, il mercato della farina biologica è segmentato in farina di frumento, farina d'avena, farina di mais, farina di riso e altri. In base alla categoria, il mercato è segmentato in convenzionale e senza glutine. In base al canale di distribuzione, il mercato è segmentato in supermercati e ipermercati, minimarket, vendita al dettaglio online e altri. L'ambito geografico del rapporto sul mercato della farina biologica si concentra su Nord America (Stati Uniti, Canada e Messico), Europa (Germania, Francia, Italia, Regno Unito, Russia e resto d'Europa), Asia Pacifico (Australia, Cina, Giappone, India, Corea del Sud e resto dell'Asia Pacifico), Medio Oriente e Africa (Sudafrica, Arabia Saudita, Emirati Arabi Uniti e resto di Medio Oriente e Africa) e Sud e Centro America (Brasile, Argentina e resto di Sud e Centro America).

Analisi segmentale:

In base al tipo di prodotto, il mercato è segmentato in farina di grano, farina di avena, farina di mais, farina di riso e altri. In base al tipo, si prevede che il segmento senza glutine detiene una quota di mercato significativa della farina biologica entro il 2030. La farina senza glutine è progettata per le persone affette da celiachia o sensibilità al glutine e per coloro che optano per una dieta senza glutine. La domanda di prodotti con dichiarazioni senza glutine è aumentata in modo significativo a causa della crescente prevalenza di disturbi correlati al glutine e di una tendenza più ampia alla consapevolezza della salute. Secondo Beyond Celiac, 1 americano su 133, ovvero circa l'1% della popolazione, soffre di celiachia negli Stati Uniti. La consapevolezza della celiachia ha portato molti consumatori a cercare alternative senza glutine, creando un mercato sostanziale per prodotti che soddisfano le restrizioni dietetiche. Inoltre, la percezione che le opzioni senza glutine possano essere più sane ha ampliato la base di consumatori oltre coloro che soffrono di condizioni mediche, contribuendo alla crescita sostenuta del mercato della farina biologica per il segmento senza glutine.

Analisi regionale:

In base alla geografia, il mercato è segmentato in cinque regioni chiave: Nord America, Europa, Asia Pacifico, Sud e Centro America e Medio Oriente e Africa. In termini di fatturato, il Nord America ha dominato la quota di mercato globale della farina biologica. Il mercato in Nord America ha rappresentato circa 2.900 milioni di $ USA nel 2023. Si prevede che il mercato della farina biologica dell'Asia Pacifico crescerà al CAGR più elevato durante il periodo di previsione. L'Asia Pacifico sta vivendo una rapida urbanizzazione e un cambiamento negli stili di vita dei consumatori. I consumatori urbani cercano la farina biologica come ingrediente fondamentale per pane fatto in casa, dolci e altri prodotti da forno. Inoltre, il passaggio alla cottura casalinga è stato accelerato da fattori come la pandemia di COVID-19, che ha spinto più consumatori a esplorare la cucina e la cottura a casa. Di conseguenza, la domanda di farina biologica come ingrediente versatile e nutriente per la cottura è cresciuta notevolmente nell'Asia Pacifico, supportando l'espansione del mercato.

L'Asia Pacifica ospita diversi paesaggi agricoli e pratiche agricole tradizionali, offrendo ampie opportunità per la produzione di farina biologica. Paesi come India, Cina e Australia hanno assistito a un aumento delle iniziative di agricoltura biologica supportate da politiche governative che promuovono l'agricoltura sostenibile e programmi di certificazione biologica. Questo crescente interesse per l'agricoltura biologica ha aumentato la disponibilità di cereali e farine biologiche prodotte nella regione. La crescente consapevolezza della salute e del benessere sta guidando la crescita del mercato della farina biologica nell'Asia Pacifica.

L'Europa è un altro importante contributore, con una quota di mercato globale di oltre il 30%. I consumatori in tutta Europa sono sempre più preoccupati per la sicurezza alimentare, la sostenibilità ambientale e l'impatto delle pratiche agricole sulla salute pubblica. Ciò ha portato a una crescente preferenza per i prodotti biologici, tra cui la farina. I consumatori in Europa cercano attivamente farina biologica prodotta senza pesticidi sintetici, erbicidi o OGM, considerandola un'opzione molto più sicura e rispettosa dell'ambiente rispetto alla farina convenzionale. Questo passaggio verso la farina biologica è anche guidato dal cambiamento degli stili di vita dei consumatori e dalle preferenze alimentari, con molti europei che optano per scelte alimentari più sane e naturali.

Approfondimenti regionali sul mercato della farina biologica

Le tendenze regionali e i fattori che influenzano il mercato della farina biologica durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di Insight Partners. Questa sezione discute anche i segmenti e la geografia del mercato della farina biologica in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e Sud e Centro America.

- Ottieni i dati specifici regionali per il mercato della farina biologica

Ambito del rapporto sul mercato della farina biologica

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2023 | 11,76 miliardi di dollari USA |

| Dimensioni del mercato entro il 2031 | 19,59 miliardi di dollari USA |

| CAGR globale (2023-2031) | 6,6% |

| Dati storici | 2020-2022 |

| Periodo di previsione | 2024-2031 |

| Segmenti coperti |

Per tipo di prodotto

|

| Regioni e Paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità dei player del mercato della farina biologica: comprendere il suo impatto sulle dinamiche aziendali

Il mercato della farina biologica sta crescendo rapidamente, spinto dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando le loro offerte, innovando per soddisfare le esigenze dei consumatori e capitalizzando sulle tendenze emergenti, il che alimenta ulteriormente la crescita del mercato.

La densità degli operatori di mercato si riferisce alla distribuzione di aziende o società che operano in un particolare mercato o settore. Indica quanti concorrenti (operatori di mercato) sono presenti in un dato spazio di mercato in relazione alle sue dimensioni o al valore di mercato totale.

Le principali aziende che operano nel mercato della farina biologica sono:

- Azienda alimentare locale

- Bob's Red Mill Cibi naturali

- Azienda di panificazione King Arthur

- koRo

- C/O di Betterbody Foods

- FWP Matthews Ltd

Disclaimer : le aziende elencate sopra non sono classificate secondo un ordine particolare.

- Ottieni una panoramica dei principali attori del mercato della farina biologica

Sviluppi del settore e opportunità future:

Le previsioni di mercato della farina biologica possono aiutare gli stakeholder a pianificare le loro strategie di crescita. Di seguito sono riportate le iniziative intraprese dai principali attori che operano nel mercato della farina biologica:

- Nel 2022, la principale azienda lattiero-casearia GCMMF, che commercializza i suoi prodotti con il marchio Amul, ha annunciato l'ingresso nel mercato degli alimenti biologici con il lancio della farina di grano biologica. Il primo prodotto lanciato in questo portafoglio è "Amul Organic Whole Wheat Atta".

Scenario competitivo e aziende chiave:

Hometown Food Company, Bob's Red Mill Natural Foods, Betterbody Foods C/O, FWP Matthews Ltd, Shipton Mill Ltd, W and H Marriage and Sons Limited, Gilchesters Organics e Anita's Organic Grain & Flour Mill Ltd. sono tra i principali attori profilati nel report di mercato della farina biologica. Gli attori che operano nel mercato globale si concentrano sulla fornitura di prodotti di alta qualità per soddisfare la domanda dei clienti. Stanno inoltre adottando varie strategie come il lancio di nuovi prodotti, l'espansione della capacità, le partnership e le collaborazioni per rimanere competitivi sul mercato.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative