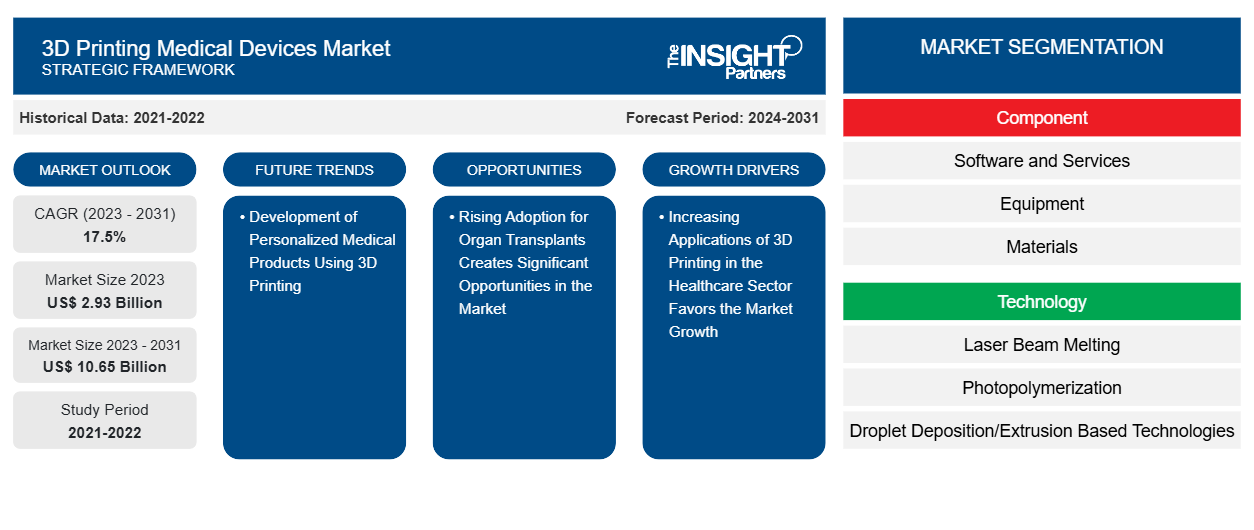

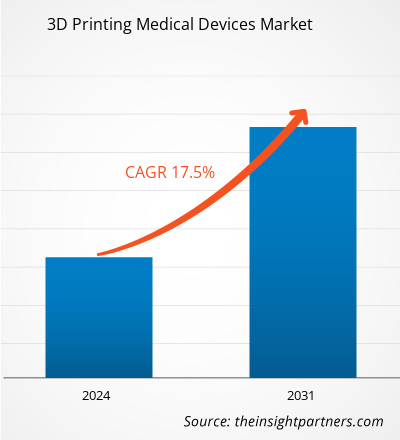

The 3D printing medical devices market size is projected to reach US$ 10.65 billion by 2031 from US$ 2.93 billion in 2023. The market is expected to register a CAGR of 17.5% during 2023–2031. The development of personalized medical products using 3D printing will likely remain a key trend in the market.

3D Printing Medical Devices Market Analysis

The market for medical devices made with 3D printing is well-established. The rising use of 3D printing in the healthcare sector drives adoption and contributes to the market's overall expansion. The increasing number of organ transplant procedures has increased the demand for 3D printing medical devices. Such a bolstering element affects the expansion of the market as a whole. Shortly, creating customized medical products through 3D printing will present a profitable prospect for market expansion.

3D Printing Medical Devices Market Overview

In recent decades, implantable medical devices have seen an increase in the use of 3D printing technology because of its accuracy and capacity for optimal material utilization. The traumatology, orthopedic surgery, and dentistry fields stand to gain the most from these instruments. No matter how complicated, implantable medical devices of any shape can be produced using 3D printing technology without experiencing processing problems. It can resolve issues about creating and producing intricate implantable medical devices. Implantable medical devices that are personalized and customized can also be made using the 3D printing process.

The second most prevalent dental condition worldwide is tooth decay. With only slight variations depending on gender, orthodontic issues are common in both genders. The potential for customized products is driving advances in 3D printing for medical and dental applications, cost savings on small-scale productions, ease of sharing and processing patient image data, and improvements in education. Limited publications are available on applications in the specialties of periodontics and endodontics. The 3D printing technique primarily focuses on oral surgery and prosthodontics applications, followed by orthodontics. Surgeons can perform operations on a realistic physical anatomy model with advanced image processing due to the clinical use of 3D printing technology.

Customize This Report To Suit Your Requirement

You will get customization on any report - free of charge - including parts of this report, or country-level analysis, Excel Data pack, as well as avail great offers and discounts for start-ups & universities

3D Printing Medical Devices Market: Strategic Insights

- Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

You will get customization on any report - free of charge - including parts of this report, or country-level analysis, Excel Data pack, as well as avail great offers and discounts for start-ups & universities

3D Printing Medical Devices Market: Strategic Insights

- Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

3D Printing Medical Devices Market Drivers and Opportunities

Increasing Applications of 3D Printing in the Healthcare Sector Favors the Market Growth.

A wide range of medical devices with intricate geometry or features corresponding to a patient's specific anatomy are produced using 3D printers. A standard design prints a few devices, after which numerous replicas of the same device are created. The patient-specific imaging data is used to develop additional devices, also called patient-matched or patient-specific devices. The intended use of printed goods and the printer's ease of use are two considerations for choosing 3D printing technology. The most popular technology for 3D printing medical devices is powder bed fusion. This method works with various materials, including nylon and titanium, used in medical devices. Using CT and MRI scans, 3D printing makes creating tactile reference models specific to each patient inexpensive and easy. By offering a different viewpoint, these models assist doctors in better preparing for surgeries, significantly reducing the time and money needed for the actual procedure in an operating room. Patients may gain from this through increased satisfaction, decreased anxiety, and accelerated recovery.

Furthermore, introducing novel biocompatible materials for 3D printing in medicine facilitates the creation of fresh surgical instruments and methods, all aimed at enhancing the surgical experience for patients. Sterilable fixation trays, contouring templates, and implant sizing models are among the instruments that can be produced via 3D printing. These can be used to size implants in the operating room before the initial cut, saving surgeons time and enhancing accuracy during intricate procedures.

Rising Adoption for Organ Transplants Creates Significant Opportunities in the Market

The use of 3D printing technology in organ transplantation has become increasingly advantageous. 3D bioprinters have undergone numerous iterations and enhancements to satisfy quality requirements and expectations. As a result, creating and developing 3D printers is constantly evolving, with a broader range of applications. By speeding up the production of medical devices, 3D printers help save lives. They aid in resolving the issues of organ donor scarcity and recipient organ rejection. It also enables medical professionals to treat a large number of patients quickly. Without easily accessible environments that provide blood, oxygen, and vital nutrients, organs cannot survive. It is possible to create secure environments for transplanted organs using 3D printing technology. Because they are bio-printed instead of castrated, 3D printers significantly impact organ replacement in the medical field. This reduces the time spent looking for suitable donors. Therefore, the result is anticipated to have substantial positive effects on society, especially regarding quality of life. Promising uses of 3D bioprinting include the creation of artificial tissues and organs, which could completely transform the field of regenerative medicine.

3D Printing Medical Devices Market Report Segmentation Analysis

Key segments that contributed to deriving the 3D printing medical devices market analysis are component, technology, application, and end user.

- Based on components, the 3D printing medical devices market is divided into software and services, equipment, and materials. The equipment segment held the most significant market share in 2023.

- By technology, the market is categorized into laser beam melting, photopolymerization, droplet deposition/extrusion-based technologies, and electron beam melting. The photopolymerization segment held the largest share of the market in 2023.

- By application, the market is segmented into custom prosthetics and implants, tissue engineering products, surgical guides, surgical instruments, wearable medical devices, hearing aids, standard prosthetics and implants, and others. The custom prosthetics and implants segment held the largest share of the market in 2023.

- By end user, the market is segmented into hospitals and surgical centres, dental and orthopaedic centres, medical device companies, academic and research institutes, pharmaceutical and biotechnology companies, and others. The hospitals and surgical centers segment held the largest share of the market in 2023.0

3D Printing Medical Devices Market Share Analysis by Geography

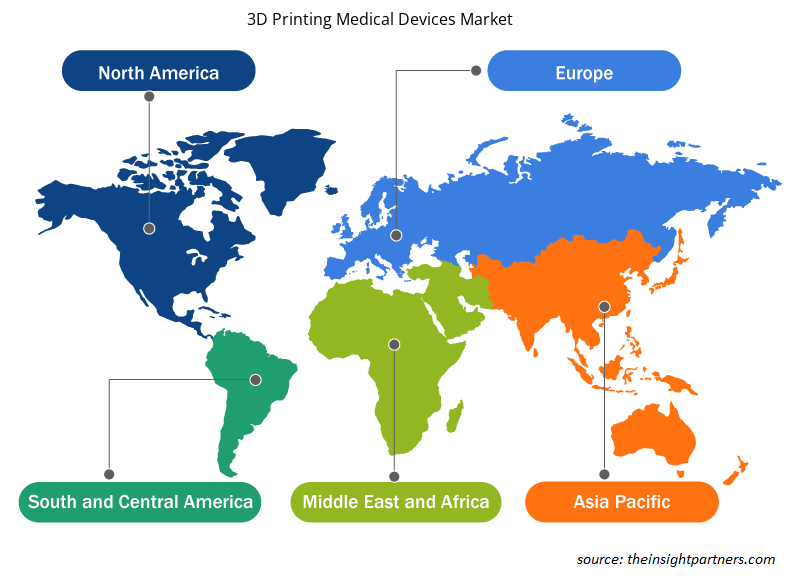

The geographic scope of the 3D printing medical devices market report is mainly divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

North America consists of three countries: the US, Canada, and Mexico. The US is the largest market for 3D printing medical devices, followed by Canada and Mexico. Nearly 200,000 amputations are done annually in the United States alone, and prosthetic replacements or alterations can be costly and time-consuming, with prices ranging from $5,000 to $50,000. Since prosthetics are such individualized devices, each must be made to order or tailored to the wearer's specifications. These days, AM technology is frequently utilized to create prosthetic components tailored to each patient's anatomy, ensuring a perfect fit. AM is used in places where prosthetics come into contact with patients because of its capacity to create intricate geometries from various materials. AM technology has developed a wide range of products, from comfortable prosthetic leg connections to intricate, highly customized facial prosthetics for cancer patients.

Organovo, a US-based medical laboratory and research company, has experimented with printing intestinal and liver tissue to aid in the in vitro study of organs and developing drugs for specific diseases. The company announced pre-clinical data in May 2018 regarding the liver tissue's functionality in a type 1 tyrosinemia program. Tyrosine is an amino acid that the body cannot metabolize because of an enzyme deficiency.

3D Printing Medical Devices Market Regional Insights

The regional trends and factors influencing the 3D Printing Medical Devices Market throughout the forecast period have been thoroughly explained by the analysts at Insight Partners. This section also discusses 3D Printing Medical Devices Market segments and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America.

- Get the Regional Specific Data for 3D Printing Medical Devices Market

3D Printing Medical Devices Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2023 | US$ 2.93 Billion |

| Market Size by 2031 | US$ 10.65 Billion |

| Global CAGR (2023 - 2031) | 17.5% |

| Historical Data | 2021-2022 |

| Forecast period | 2024-2031 |

| Segments Covered |

By Component

|

| Regions and Countries Covered | North America

|

| Market leaders and key company profiles |

3D Printing Medical Devices Market Players Density: Understanding Its Impact on Business Dynamics

The 3D Printing Medical Devices Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Market players density refers to the distribution of firms or companies operating within a particular market or industry. It indicates how many competitors (market players) are present in a given market space relative to its size or total market value.

Major Companies operating in the 3D Printing Medical Devices Market are:

- EOS GmbH Electro Optical Systems

- Renishaw PLC

- Stratasys Ltd.

- 3D Systems, Inc.

- EnvisionTech, Inc.

- Concept Laser Gmbh (General Electric)

Disclaimer: The companies listed above are not ranked in any particular order.

- Get the 3D Printing Medical Devices Market top key players overview

3D Printing Medical Devices Market News and Recent Developments

The 3D printing medical devices market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the developments in the 3D printing medical devices market are listed below:

- Align Technology, Inc. a leading global medical device company that designs, manufactures, and sells the Invisalign system of clear aligners, iTero intraoral scanners, and exocadCAD/CAM software for digital orthodontics and restorative dentistry, announced that it has completed the acquisition of privately-held Cubicure GmbH, a pioneer in direct 3D printing solutions for polymer additive manufacturing that develops, produces, and distributes innovative materials, equipment, and processes for novel 3D printing solutions. (Source: Align Technology, Inc., Press Release, January 2024)

3D Printing Medical Devices Market Report Coverage and Deliverables

The “3D Printing Medical Devices Market Size and Forecast (2021–2031)” report provides a detailed analysis of the market covering below areas:

- 3D printing medical devices market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- 3D printing medical devices market trends as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST/Porter’s Five Forces and SWOT analysis

- 3D printing medical devices market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments.

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the 3D printing medical devices market

- Detailed company profiles

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

- Dried Blueberry Market

- Hand Sanitizer Market

- Point of Care Diagnostics Market

- Procedure Trays Market

- Semiconductor Metrology and Inspection Market

- Batter and Breader Premixes Market

- Underwater Connector Market

- Fixed-Base Operator Market

- Artificial Intelligence in Defense Market

- Electronic Signature Software Market

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Component, Technology, Application, and End-User

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

Argentina, Australia, Brazil, Canada, China, France, Germany, India, Italy, Japan, Mexico, Saudi Arabia, South Africa, South Korea, Spain, UAE, United Kingdom, US

Frequently Asked Questions

Which are the leading players operating in the 3D printing medical devices market?

EOS GmbH Electro Optical Systems, Proadways Group, Renishaw PLC, Stratasys Ltd., EnvisionTech, Inc., Concept Laser Gmbh (General Electric), 3T RPD Ltd., 3D Systems, Inc., SLM Solution Group AG, CELLINK

What is the expected CAGR of the 3D printing medical devices market?

The market is expected to register a CAGR of 17.5% during 2023–2031.

Which region dominated the 3D printing medical devices market in 2023?

North America dominated the 3D printing medical devices market in 2023

What are the driving factors impacting the 3D printing medical devices market?

Key factors driving the market are the high incidence of dental and orthopedic conditions and increasing applications of 3d printing in the healthcare sector.

What are the future trends of the 3D printing medical devices market?

The development of personalized medical products using 3D printing will likely remain a key trend in the market.

Get Free Sample For

Get Free Sample For