Aerospace & Defense Power Connector Market Overview and Growth by 2027

Aerospace & Defense Power Connector Market Forecast to 2027 - Analysis by Current Rating (5-40 Amp, >40-80 Amp, >80-150 Amp, >150-300 Amp, >300-600 Amp, >600-900 Amp); Connector Shape (Rectangular and Circular); Application (Aerospace, Military Ground Vehicle, Body-worn Equipment, and Naval Ships)

- Status : Published

- Report Code : TIPRE00010500

- Category : Aerospace and Defense

- No. of Pages : 206

- Available Report Formats :

- Last update date : June 18, 2024

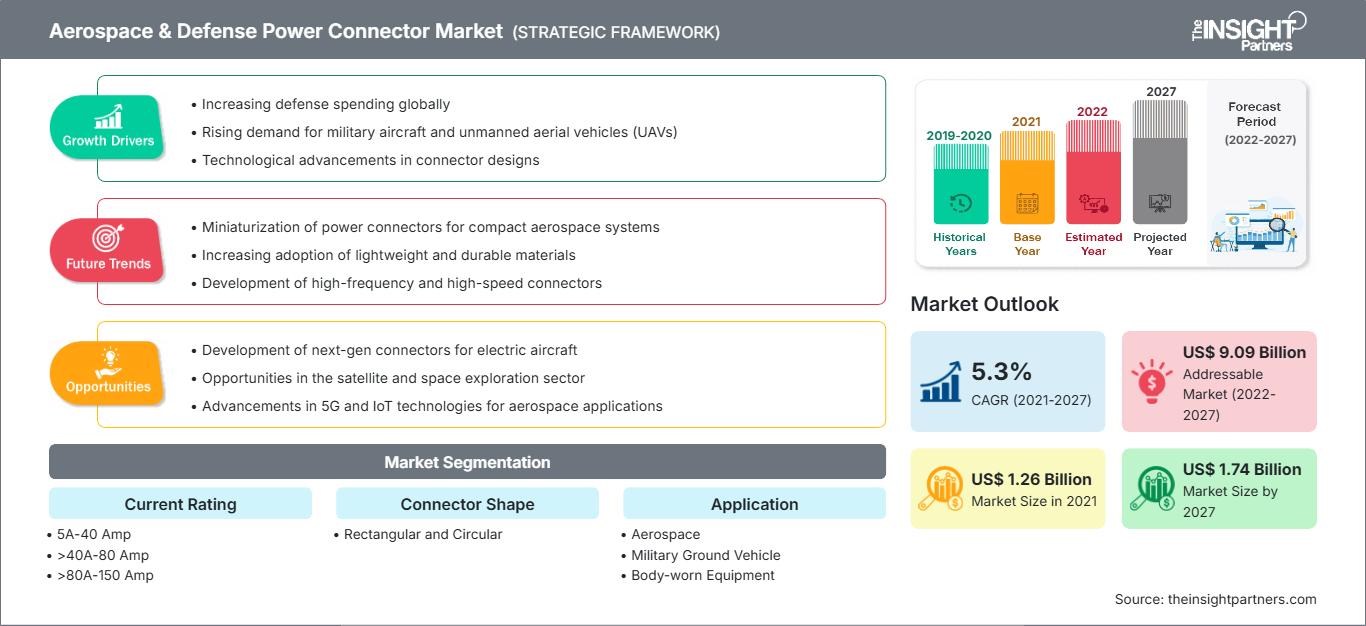

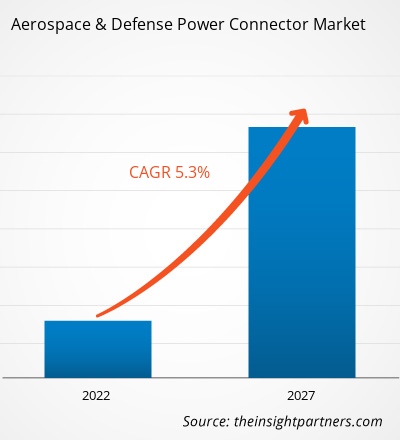

2021 Market Size

US$ 1.26 Bn

Base year value

2027 Forecast

US$ 1.74 Bn

Projected by 2027

CAGR 2022-2027

5.3 %

Growth rate

Addressable Market

US$ 9.09 Bn

(2022-2027)

The Aerospace & defense power connector market is expected to grow from US$ 1,262.71 million in 2021 to US$ 1,737.78 million by 2027. The Aerospace & defense power connector market is expected to grow at a CAGR of 5.3% during the forecast period of 2021 to 2027.

The global aircraft manufacturing industry is experiencing substantial growth due to the increasing demand for commercial and military aircraft worldwide. The growing disposable incomes in developing countries and the presence of top players such as Boeing and Airbus are some of the factors that are driving the demand of these aircraft. In a global scenario, commercial airplanes are anticipated to maintain a continuous growth over the coming years, regardless of several challenges faced by the commercial airlines such as uncertain fuel prices and other regulatory changes in various countries. In addition to this, the growing investments in defense equipment across countries are expected to drive the demand for military aircraft during the forecast period of 2020 to 2027. The growing production of aircraft demand for integration of advanced equipment such as engine control, avionics, cabin system, and in-flight entertainment system, which requires power connectors in order to supply power to these systems. Power connectors are designed to meet the aerospace and defense standards. All these factors are anticipated to fuel the demand for power connectors in various geographies and offer future growth opportunities for Aerospace & Defense Power Connector market players operating in the global market.

The aircraft production industry is heavily dependent on manual labor despite robotic technology. In the wake of strong lockdown regulations imposed by several countries, the aircraft-manufacturing sector is experiencing a significantly lower number of labors in respective aircraft and component manufacturing facilities. Since the aircraft-manufacturing sector is majorly concentrated in North America and Europe, and the two regions are facing a tremendous challenge in maintaining its manufacturing pace with the outbreak. The European countries manufacture various aircraft components and defense equipment and vehicles. However, a majority of European countries are challenged continuously growing outbreak. The plane makers across the globe are witnessing a severe downfall in component procurement. The downfall in the production of aircraft components is a result of a labor shortage.

The market for aerospace & defense power connector has been segmented on the basis of current rating, connector shape, application, and geography. Based on current rating, the market has been segmented into 5Amps to 40Amps, >40Amps to 80Amps, >80Amps to 150Amps, >150Amps to 300Amps, >300Amps to 600Amps, >600 to 900Amps. 5Amps to 40Amps segment represented the largest share of the overall market throughout the forecast period. Based on the connector shape, the market has been segmented into rectangular and circular. Based on the application, the market is segmented into aerospace, military ground vehicles, body-worn equipment, and naval ships. The aerospace segment is further bifurcated into the engine control system, avionics, cabin equipment, and others. Geographically, the market is segmented into five major regions— North America, Europe, Asia Pacific (APAC), Middle East and Africa (MEA), and South America (SAM).

Market Assessment and Insights

- North America dominated the market with 36.3% share in 2019.

- APAC is poised to grow at a CAGR of 7.2% over the forecast period.

- United States market is projected to grow at a CAGR of 4.2% over the forecast period.

- By Current Rating, the 5 Amps to 40 Amps segment accounted for the largest market share of 23.9% in 2019.

- By Connector Shape, the Circular segment is anticipated to witness the fastest growth, registering a CAGR of 5.5% over the forecast period

- By Application, the Aerospace segment accounted for the largest market share of 32.6% in 2019.

- By Aerospace, the Avionics segment is anticipated to witness the fastest growth, registering a CAGR of 7.2% over the forecast period

- The report profiles key industry players such as Eaton Corporation plc, Molex LLC, TE Connectivity Ltd, Amphenol Corp, ITT Inc, Fischer Connectors SA, Ametek Inc, Radiall, Arrow Electronics Inc, Collins Aerospace, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Aerospace & Defense Power Connector Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Aerospace & Defense Power Connector Market Insights

Stimulating Demand for Soldier Modernization

The rising battlefield scenarios are demanding the militaries to equip the soldiers with advanced technologies. The militaries around the globe are highly focused on optimizing soldier protection with efficient body armor and personal protection. Various technologically advanced countries such as China and the US are swiftly modernizing its armed forces, also highly investing in research and development for advanced defense technology. They are also conducting research into a broad range of defense-related technology, such as Artificial Intelligence (AI), robotics, quantum information sciences, and biometrics. The government is highly inclined toward investing billions in military and defense equipment; for instance, as per Stockholm International Peace Research Institute (SIPRI), in 2019, global military expenditure rose to US$ 1917 billion, it includes expenditure on current military forces and activities, arms and equipment purchases, military construction, research and development, and command and support.

Current Rating -Based Market Insights

The market players operating in the aerospace & defense power connector market offer their products with different current ratings, in order to match the demands of customers. The power connectors have a wider range of applications, and every application demands for different connectors with varying amperage. The aerospace & defense power connector market has been analyzed on the basis of various current ratings, which include 5Amps to 40Amps, >40Amps to 80Amps, >80Amps to 150Amps, >150Amps to 300Amps, >300Amps to 600Amps, and >600Amps to 900Amps.

Connector Shape -Based Market Insights

When it comes to electrical devices, a consistent and reliable power supply is crucial. The selection of an appropriate power connector completely depends on the nature of the application and also on the customer’s specific requirements. Ranging from high-voltage versions and specific standards to design diversity, the power connectors portfolio offers a broad, practical selection for fulfilling user’s individual application objectives. There are wide range of rectangular and cylindrical products for the usage in high amperage, high power applications.

Application -Based Market Insights

The power connectors are used heavily on various applications across the aerospace sector and defense sector. The power connectors are essential components on aircraft, military ground vehicles, naval ships, and body-worn equipment. The presence of large numbers of aerospace and defense contractors across the globe allows the power connector market players to experience significant demand for their products, which catalyzes the aerospace & defense power connector market year-on-year.

Players operating in the Aerospace & defense power connector market focus on strategies, such as market initiatives, acquisitions, and product launches, to maintain their positions in the Aerospace & defense power connector market. A few developments by key players of the Aerospace & defense power connector market are:

In February 2020, AMETEK announced the completion of a significant hermetic connector production expansion, thereby reducing the lead time by around 35% for products that have been in short supply for over a year. Equipment, Facilities, and personnel at their Ohio and California sites have been increased.

In July 2020, Radiall expanded its EPX™ Series with the addition of the newer iEPX connector, a weight-optimized EPXB2 disconnect shell that features an integrated strain relief and a press-in EMI backshell and supports quicker, more cost-effective integration into aircraft systems.

Aerospace & Defense Power Connector

Aerospace & Defense Power Connector Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2021 | US$ 1.26 Billion |

| Market Size by 2027 | US$ 1.74 Billion |

| Global CAGR (2021 - 2027) | 5.3% |

| Historical Data | 2019-2020 |

| Forecast period | 2022-2027 |

| Segments Covered |

By Current Rating

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Aerospace & Defense Power Connector Market Players Density: Understanding Its Impact on Business Dynamics

The Aerospace & Defense Power Connector Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Aerospace & Defense Power Connector Market – by Component

- 5Amps to 40Amps

- >40Amps to 80Amps

- >80Amps to 150Amps

- >150Amps to 300Amps

- >300Amps to 600Amps

- >600Amps to 900Amps

Aerospace & Defense Power Connector Market – by Connector Shape

- Rectangular

- Circular

Aerospace & Defense Power Connector Market – by Application

- Aerospace

- Military Ground Vehicle

- Body-worn Equipment

- Naval Ships

Aerospace & Defense Power Connector Market – by Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Russia

- UK

- Italy

- Rest of Europe

- Asia Pacific (APAC)

- China

- India

- Japan

- Australia

- South Korea

- Rest of APAC

- MEA

- Saudi Arabia

- UAE

- South Africa

- Rest of MEA

- SAM

- Brazil

- Rest of SAM

Aerospace & Defense Power Connector Market – Company Profiles

- AMETEK. Inc.

- Amphenol Corporation

- Arrow Electronics, Inc.

- Collins Aerospace (Raytheon Technologies Corporation)

- Eaton Corporation plc

- Fischer Connectors SA

- ITT Corporation

- Molex, LLC

- Radiall

- TE Connectivity

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends