Asia Pacific Data Center Cooling Market Analysis and Forecast by Size, Share, Growth, Trends 2031

Asia Pacific Data Center Cooling Market Size and Forecast (2021 - 2031), Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (Air Cooling and Liquid Cooling), Component (Air Conditioning System, Chillers, Air Handling Units, Cooling Towers, Heat Exchangers, Humidifiers, and Others), Cooling Type (Room Based Cooling, Row Based Cooling, and Rack Based Cooling), Data Center Type (Hyperscale Data Center, Colocation Data Center, Wholesale Data Center, and Enterprise Data Center), and Industry Vertical (IT and Telecom, BFSI, Healthcare, Manufacturing, Government and Defense, Media and Entertainment, Retail, Energy, and Others)

Historic Data: 2021-2023 | Base Year: 2024 | Forecast Period: 2025-2031- Status : Published

- Report Code : TIPRE00043278

- Category : Technology, Media and Telecommunications

- No. of Pages : 213

- Available Report Formats :

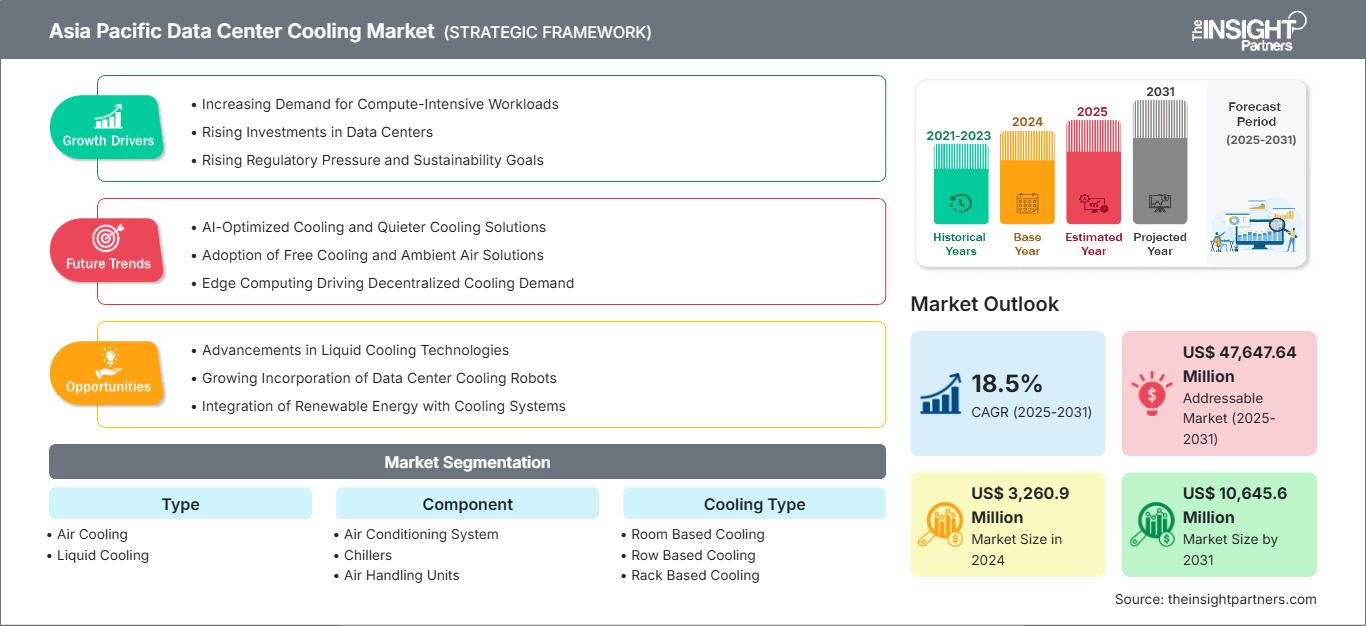

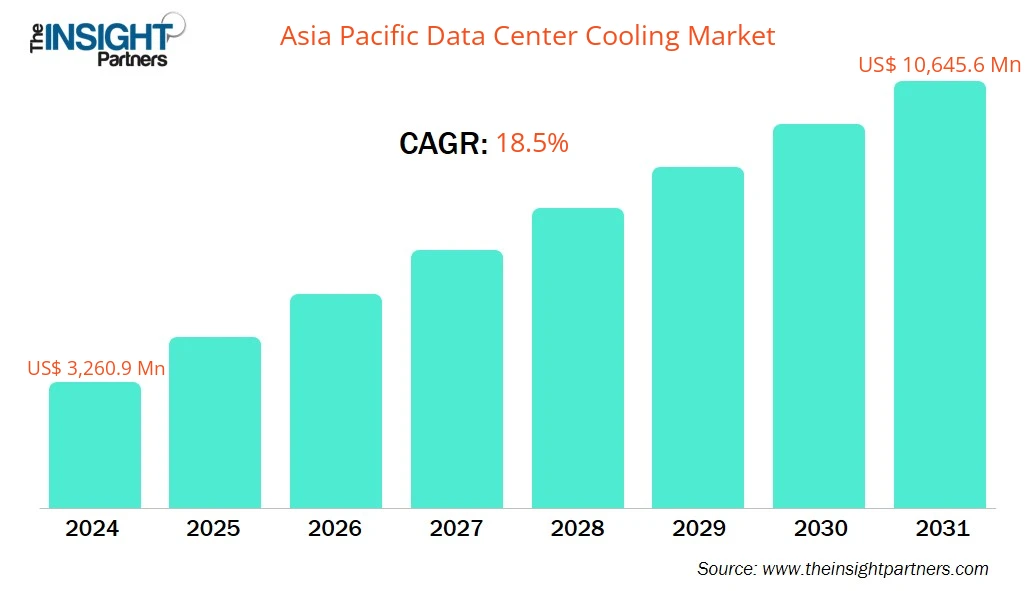

The Asia Pacific Data Center Cooling Market size is expected to reach US$ 10,645.6 Million by 2031 from US$ 3,260.9 Million in 2024. The market is estimated to record a CAGR of 18.5% from 2025 to 2031.

Executive Summary and Asia Pacific Data Center Cooling Market Analysis:

In September 2021, Vantage Data Centers, a prominent global provider of hyperscale data center campuses, expanded into the Asia Pacific market through two acquisitions, marking a significant development in the region's data center industry. The expansion is supported by a substantial equity capital addition of US$1.5 billion, contributed by DigitalBridge Investment Management and other existing Vantage investors. The expansion enables Vantage to offer data center services across several key cities in the Asia Pacific, including Tokyo, Osaka, Melbourne, Hong Kong, and Kuala Lumpur. This move is specifically aimed at catering to the needs of hyperscale, cloud, and large enterprise customers in the region. Vantage's entry into these markets is expected to have a substantial impact on the growth of the data center cooling market in the Asia Pacific.

The requirement for sustainable and energy-efficient cooling solutions is becoming increasingly prominent in the Asia Pacific. With cooling needs representing a significant portion of total data center energy demand, there is a growing emphasis on transitioning from air-based cooling to more efficient liquid cooling systems. This shift is driven by the benefits of reduced operational costs and environmental impact, as well as the ease of maintenance and self-containment of liquid cooling systems.

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONAsia Pacific Data Center Cooling Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Asia Pacific Data Center Cooling Market Segmentation Analysis:

- By Type, the Asia Pacific Data Center Cooling Market is segmented into Air Cooling and Liquid Cooling. The Air Cooling segment dominated the market in 2024.

- By Component, the Asia Pacific Data Center Cooling Market is segmented into Air Conditioning System, Chillers, Air Handling Units, Cooling Towers, Heat Exchangers, Humidifiers, and Others. The Air Conditioning System segment dominated the market in 2024.

- By Cooling Type, the Asia Pacific Data Center Cooling Market is segmented into Room Based Cooling, Row Based Cooling, and Rack Based Cooling. The Room Based Cooling segment dominated the market in 2024.

- By Data Center Type, the Asia Pacific Data Center Cooling Market is segmented into Hyperscale Data Center, Colocation Data Center, Wholesale Data Center, and Enterprise Data Center. The Hyperscale Data Center segment dominated the market in 2024.

- By Industry Vertical, the Asia Pacific Data Center Cooling Market is segmented into IT and Telecom, BFSI, Healthcare, Manufacturing, Government and Defense, Media and Entertainment, Retail, Energy, and Others. The IT and Telecom segment dominated the market in 2024.

Asia Pacific Data Center Cooling Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 3,260.9 Million |

| Market Size by 2031 | US$ 10,645.6 Million |

| CAGR (2025 - 2031) | 18.5% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

Asia Pacific

|

| Market leaders and key company profiles |

|

Asia Pacific Data Center Cooling Market Players Density: Understanding Its Impact on Business Dynamics

The Asia Pacific Data Center Cooling Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Asia Pacific Data Center Cooling Market Outlook

Liquid cooling has emerged as an optimal solution to meet the requirements of the high-performance computing (HPC) and data center industries. By negating the necessity for continuous air circulation, liquid cooling markedly diminishes utility consumption, thereby enhancing the energy efficiency of the facility. Liquid cooling technologies have emerged as a popular solution, with ~40% of data centers utilizing it. Companies are forming strategic partnerships to participate in the advancements of liquid cooling technologies. For instance, Mitsubishi Heavy Industries, Ltd. (MHI) and ZutaCore, Inc. formed a strategic partnership in September 2023 to advance sustainable liquid cooling solutions for the data industry to achieve energy efficiency and zero emissions. This collaboration involves MHI's investment in ZutaCore and a white-label sales agreement, combining ZutaCore's HyperCool dielectric direct-liquid-cooling technology with MHI's extensive product line and technological expertise at a global scale. ZutaCore's HyperCool technology is a waterless, direct-on-chip liquid cooling solution that aims to bridge the gap between data industry sustainability and ever-increasing computing power. It delivers 10x more computing, a 50% total cost of ownership (TCO) reduction, and 100% heat reuse, as well as reducing CO2 emissions. This technology is designed to move large amounts of heat off the chip effectively and safely, with no practical limit to heat dissipation. It also aims to reduce the consumption of scarce resources, including energy, water, and land, while reducing capital and operating expenses. This partnership aims to expedite the growth of sustainable liquid cooling solutions crucial for energy efficiency. The comprehensive solution provided by this collaboration offers unprecedented benefits to high-performance computing workloads, server densification, and data center sustainability.

In 2024, STULZ, a global mission-critical air conditioning specialist, unveiled the CyberCool CMU, a cutting-edge coolant management and distribution unit (CDU) designed to optimize heat exchange efficiency in liquid cooling solutions. This innovative unit is set to be launched at Data Centre World Frankfurt 2024, scheduled in May, from 22nd to 23rd, at Messe Frankfurt. The CyberCool CMU is engineered to offer industry-leading levels of energy efficiency, flexibility, and reliability within a small footprint while providing precise control over an entire liquid cooling system. This development aligns with the ongoing efforts to address the escalating heat challenges in data centers and support the evolving demands of various sectors. Thus, advancements in liquid cooling technologies are expected to create lucrative opportunities for the data center cooling market growth in the coming years.

Asia Pacific Data Center Cooling Market Country Insights

By country, the Asia Pacific Data Center Cooling Market is segmented into China, India, Australia, Japan, South Korea, and the Rest of APAC. China held the largest share in 2024.

Shanghai, Beijing, Guangzhou, Shenzhen, and Chengdu are a few of the largest and most significant cities in China concerning data center infrastructure and colocation services. According to BAXTEL, China currently has 92 facilities, with Equinix leading as the top provider with 8 sites, closely followed by iAdvantage (SUNeVision) with 7 facilities. Notably, the most popular facilities in China include Equinix Hong Kong HK1 and Global Switch Hong Kong. The country is exploring innovative solutions, such as leveraging ocean cooling to reduce the cost of cooling data centers and decrease the consumption of traditional energy sources. The demand for data center cooling in China is growing dynamically, driven by the increasing adoption of cloud computing, big data analytics, artificial intelligence, and the Internet of Things (IoT). As a result, the rising adoption of cooling solutions such as economizer systems, liquid cooling systems, control systems, air conditioning, chilling units, and cooling towers to address the evolving needs of various industries is fueling the market growth in China.

Asia Pacific Data Center Cooling Market Company Profiles

Some of the key players operating in the market include Schneider Electric SE, Fujitsu Ltd, Rittal GmbH & Co KG, Delta Electronics Inc, Mitsubishi Corp, Daikin Industries Ltd, Carrier Global Corp, Vertiv Group Corp., Asetek, Inc, and Stulz SpA.

These players are adopting various strategies such as expansion, product innovation, and mergers and acquisitions to provide innovative products to their consumers and increase their market share.

Asia Pacific Data Center Cooling Market Research Methodology

The following methodology has been followed for the collection and analysis of data presented in this report:

Secondary Research

The research process begins with comprehensive secondary research, utilizing internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

- Company websites, annual reports, financial statements, broker analyses, and investor presentations

- Industry trade journals and other relevant publications

- Government documents, statistical databases, and market reports

- News articles, press releases, and webcasts specific to companies operating in the market

Note:

All financial data included in the Company Profiles section has been standardized to US$. For companies reporting in other currencies, figures have been converted to US$ using the relevant exchange rates for the corresponding year.Primary Research

The Insight Partners conducts a significant number of primary interviews each year with industry stakeholders and experts to validate its data analysis and gain valuable insights. These research interviews are designed to:

- Validate and refine findings from secondary research

- Enhance the expertise and market understanding of the analysis team

- Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects

Primary research is conducted via email interactions and telephone interviews, encompassing various markets, categories, segments, and sub-segments across different regions. Participants typically include:

- Industry stakeholders: Vice Presidents, Business Development Managers, Market Intelligence Managers, and National Sales Managers

- External experts: Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Unlock Exclusive Report Discounts

Enquire Now

Get Free Sample For

Get Free Sample For