Micro Data Center Market Size, Trends & Demand by 2034

Coverage: By Component [IT Infrastructure (Servers, Racks and Enclosures, Storage Systems, Networking Equipments, and Others), Connectivity and Cabling (Fiber Optic Cabling and Copper Cabling), Power Solutions (UPS Systems, Power Distribution Units (PDUs) and Others), Cooling Solutions, and Others], Organization Size (Large Enterprises and SMEs), End User (IT and Telecom, BFSI, Retail, Healthcare, Manufacturing, and Others), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America)

- Status : Published

- Report Code : TIPTE100000230

- Category : Technology, Media and Telecommunications

- No. of Pages : 404

- Available Report Formats :

- Last update date : March 04, 2026

2025 Market Size

US$ 10.93 Bn

Base year value

2034 Forecast

US$ 118.77 Bn

Projected by 2034

CAGR 2026-2034

30.2 %

Growth rate

Addressable Market

US$ 459.55 Bn

(2026-2034)

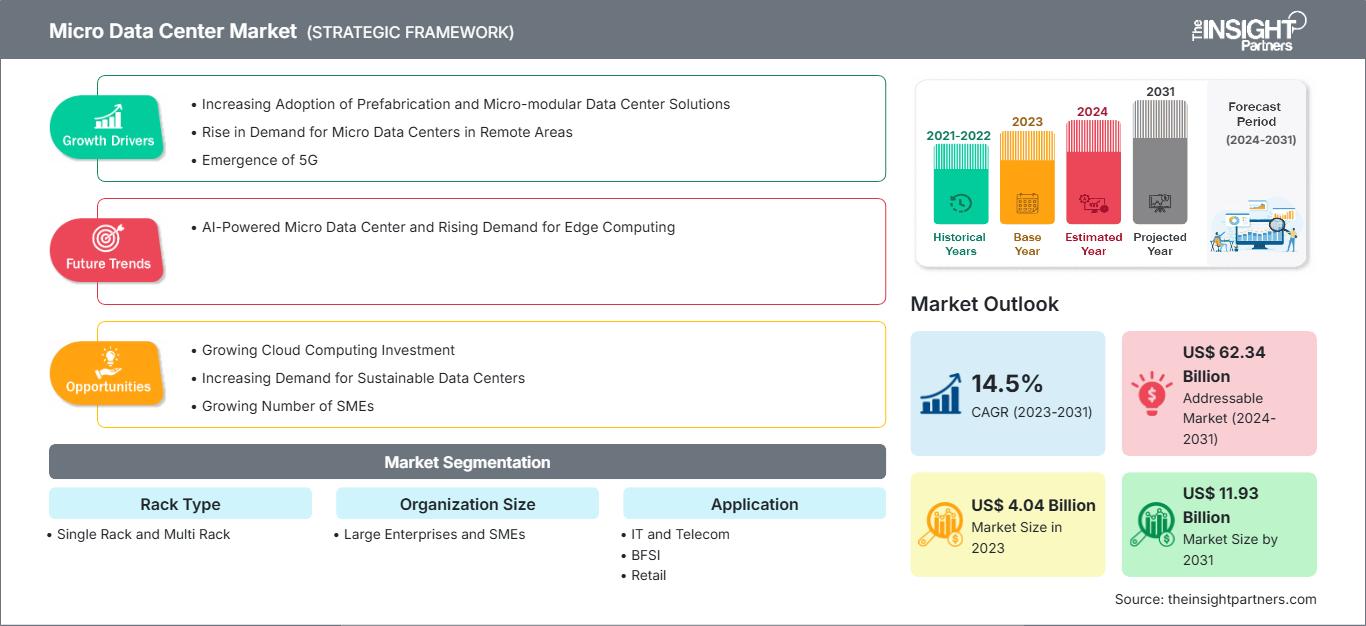

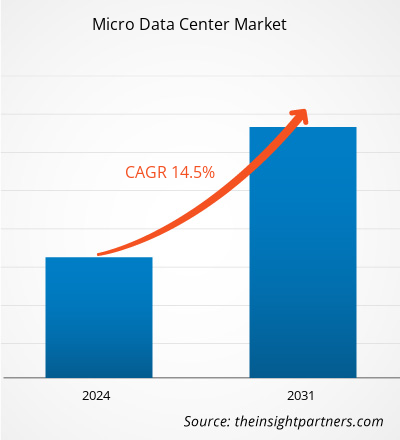

The Micro Data Center Market size is expected to reach US$ 118.77 billion by 2034 from US$ 10.93 billion in 2025. The market is anticipated to register a CAGR of 30.2% during 2026–2034.

Micro Data Center Market Analysis

The micro data center market is experiencing robust growth due to increasing demand for edge computing and rising data production, which requires data centers to process information closer to the source with low latency and fast access times. The demand for compact self-contained data center solutions is growing as enterprises expand their digital operations while implementing IoT and AI, and 5G-enabled applications in both urban and remote locations.

Micro Data Center Market Overview

Micro data centers are compact, self‑contained data processing and storage units designed to operate at the edge of networks, closer to where data is generated and consumed. They typically include integrated servers, networking, cooling, and power infrastructure packaged in a modular form factor that can be deployed rapidly in space‑constrained environments.

Market Research Highlights

- North America dominated the market with 45.6% share in 2025.

- Asia Pacific is poised to grow at a CAGR of 32.1% over the forecast period.

- United States market is projected to grow at a CAGR of 30.3% over the forecast period.

- By Component, the IT Infrastructure segment accounted for the largest market share of 35.8% in 2025.

- By IT Infrastructure Type, the Racks and Enclosures segment is anticipated to witness the fastest growth, registering a CAGR of 31.3% over the forecast period

- By Connectivity And Cabling Type, the Fiber Optic Cabling segment accounted for the largest market share of 67.6% in 2025.

- By Power Solutions Type, the Power Distribution Units (PDUs) segment is anticipated to witness the fastest growth, registering a CAGR of 32.1% over the forecast period

- By Organization Size, the Large Enterprises segment accounted for the largest market share of 64.9% in 2025.

- By End User, the IT and Telecom segment is anticipated to witness the fastest growth, registering a CAGR of 32.1% over the forecast period

- The report profiles key industry players such as Schneider Electric SE, Rittal GmbH & Co KG, Delta Electronics Inc, Eaton Corporation plc, Legrand SA, Panduit, Vertiv Group Corp., Cannon Technologies Ltd, Datwyler IT Infra GmbH, SCHÄFER Ausstattungssysteme GmbH, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Micro Data Center Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Micro Data Center Market Drivers and Opportunities

Market Drivers:

- Rising Edge Computing Demand: The rapid growth of IoT devices, AI-driven applications, and 5G networks is increasing the need for low-latency data processing closer to end users.

- Expansion of Remote and Distributed Operations: Enterprises operating branch offices, retail outlets, manufacturing sites, and telecom towers require compact and reliable micro data center solutions to support localized data processing.

- Business Continuity and Disaster Recovery Needs: Growing concerns over downtime, cyber risks, and service disruptions are driving the adoption of resilient and secure micro data center infrastructure.

- Digital Transformation and Hybrid IT Adoption: Organizations transitioning to hybrid cloud and distributed IT architectures are leveraging micro data centers for scalable, flexible, and efficient IT deployments.

Market Opportunities:

- AI-Driven Infrastructure Management: Integration of AI and machine learning enables predictive maintenance, automated workload optimization, and intelligent cooling management.

- Edge and 5G Network Expansion: The rollout of 5G infrastructure and increasing edge computing deployments create significant opportunities for compact and localized micro data center solutions.

- Adoption Across Industry Verticals: Sectors such as manufacturing, retail, healthcare, telecom, and BFSI are increasingly investing in micro data centers to support real-time analytics.

- Integration with IoT and Smart Systems: The proliferation of IoT devices and smart infrastructure generates continuous data streams, driving demand for micro data centers capable of processing data at the edge.

Micro Data Center Market Report Segmentation Analysis

The micro data center market is categorized into distinct segments to understand its structure, growth prospects, and emerging trends. Below is the standard segmentation approach used in industry reports:

By Component:

- IT Infrastructure: Includes integrated servers, storage, and networking equipment that form the core computing backbone of micro data center deployments.

- Connectivity and Cabling: Encompasses structured cabling, switches, and network components, ensuring seamless data transmission and reliable interconnection between systems.

- Power Solutions: Covers UPS systems, PDUs, batteries, and backup generators that provide a stable and uninterrupted power supply.

- Cooling Solutions: Comprises precision cooling, in-row cooling, and liquid cooling technologies designed to maintain optimal operating temperatures in compact environments.

- Others: Includes racks, enclosures, monitoring software, security systems, and fire suppression solutions supporting overall infrastructure management.

By Organization Size:

- Large Enterprises: Deploy micro data centers to support distributed operations, edge computing strategies, and high-volume data processing across multiple locations.

- SMEs: Adopt compact and cost-effective micro data centers to enhance IT capabilities, ensure business continuity, and support digital transformation initiatives.

By End User:

- IT and Telecom

- BFSI

- Retail

- Healthcare

- Manufacturing

- Others

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Micro Data Center Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 10.93 Billion |

| Market Size by 2034 | US$ 118.77 Billion |

| Global CAGR (2026 - 2034) | 30.2% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Component

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Micro Data Center Market Players Density: Understanding Its Impact on Business Dynamics

The Micro Data Center Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Micro Data Center Market Share Analysis by Geography

The micro data center market is experiencing strong global growth, driven by increasing edge computing adoption, rising data traffic, expansion of 5G networks, and the growing need for low-latency processing across industries. Organizations are deploying compact, modular data center solutions to support distributed IT environments, real-time analytics, and business continuity requirements.

The micro data center market growth differs in each region due to variations in micro data center awareness, regulatory frameworks, technology adoption, and enterprise investment capacity. Below is a summary of market share and trends by region:

North America:

Leads the market due to advanced digital infrastructure, strong presence of cloud service providers, high 5G deployment, and significant investments in edge computing and AI-driven applications. Enterprises prioritize distributed IT architectures to enhance resilience and performance.

Europe:

Growth is driven by Industry 4.0 initiatives, stringent data protection regulations, and increasing focus on energy-efficient and modular data center solutions. Adoption is strong across manufacturing, BFSI, and smart city projects.

Asia Pacific:

Expected to witness the fastest growth, supported by rapid urbanization, expanding telecom networks, increasing data consumption, and large-scale digital transformation initiatives in countries such as China, India, Japan, and Southeast Asia.

South and Central America:

Demonstrates steady growth due to expanding enterprise IT infrastructure, growing cloud adoption, and increasing investments in retail and telecom sectors.

Middle East & Africa:

Emerging adoption driven by smart city developments, digital economy initiatives, and investments in telecom and energy infrastructure, particularly in GCC countries.

Micro Data Center Market Players Density: Understanding Its Impact on Business Dynamics

High Market Density and Competition

Competition is intense due to the presence of major global players such as Eaton Corp Plc, Cannon Technologies Ltd, SCHÄFER Ausstattungssysteme GmbH, Rittal GmbH & Co KG, Delta Electronics Inc, Datwyler IT Infra GmbH, Schneider Electric SE, Intellinet Network Solutions, Panduit, Legrand SA, and Vertiv Group.

This high level of competition urges companies to stand out by offering:

- Modular and scalable infrastructure designs that enable rapid deployment and flexible capacity expansion

- Energy-efficient and intelligent power management systems to reduce operational costs and carbon footprint

Opportunities and Strategic Moves

- AI-driven infrastructure optimization – Leverage AI and analytics for predictive maintenance, automated workload balancing, intelligent cooling control, and improved energy efficiency.

- Edge and 5G ecosystem partnerships – Collaborate with telecom providers, cloud vendors, and system integrators to support distributed computing and ultra-low latency applications.

Disclaimer: The companies listed above are not ranked in any particular order.

Other companies analyzed during the course of research:

- Dell Technologies, Inc.

- EdgeMicro (EdgeConneX)

- Huawei Technologies Co., Ltd

- Canovate Group

- Zella DC

- Hanley Energy

- KSTAR Corporation

- Orbis Oy

Micro Data Center Market News and Recent Developments

- In April 2024, Vertiv (NYSE: VRT)—a global provider of critical digital infrastructure and continuity solutions—introduced the Vertiv SmartAisle 3, a micro modular data center system that utilizes the power of Artificial Intelligence (AI), providing enhanced intelligence and enabling efficient operations within the data center environment. Now available in Southeast Asia, Australia, and New Zealand, the SmartAisle 3 can be configured for up to 120 kW of total IT load. It is ideal for a wide range of industry applications, including banking, healthcare, government, and transportation.

- In March 2024, Eaton—an intelligent power management company—announced the launch of the SmartRack modular data center in North America. The data center is meant for organizations seeking to rapidly meet the growing requirements for edge computing, machine learning, and AI. These data centers can be deployed in a matter of days in facilities such as enterprise data centers, colocation data centers, manufacturing facilities, and warehouses.

Micro Data Center Market Report Coverage and Deliverables

The "Micro Data Center Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering below areas:

- Micro Data Center Market size and forecast at global, regional, and country levels for all the segments covered under the scope

- Micro Data Center Market trends, as well as dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Micro Data Center Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Micro Data Center market

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends