Australia and New Zealand Remote Healthcare Market Growth Drivers and Forecast by 2028

Historic Data: 2019-2020 | Base Year: 2021 | Forecast Period: 2022-2028Australia and New Zealand Remote Healthcare Market Forecast to 2028 - COVID-19 Impact and Country Analysis By Service (Real Time Virtual Health, Remote Patient Monitoring, and Tele-ICUs); and End-User (Healthcare Providers, Patients, Payers, Employer Groups and Government Organizations)

- Report Date : Dec 2022

- Report Code : TIPRE00029787

- Category : Technology, Media and Telecommunications

- Status : Published

- Available Report Formats :

- No. of Pages : 132

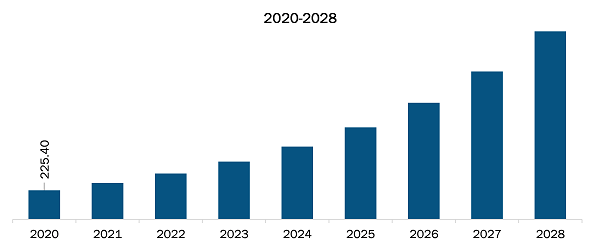

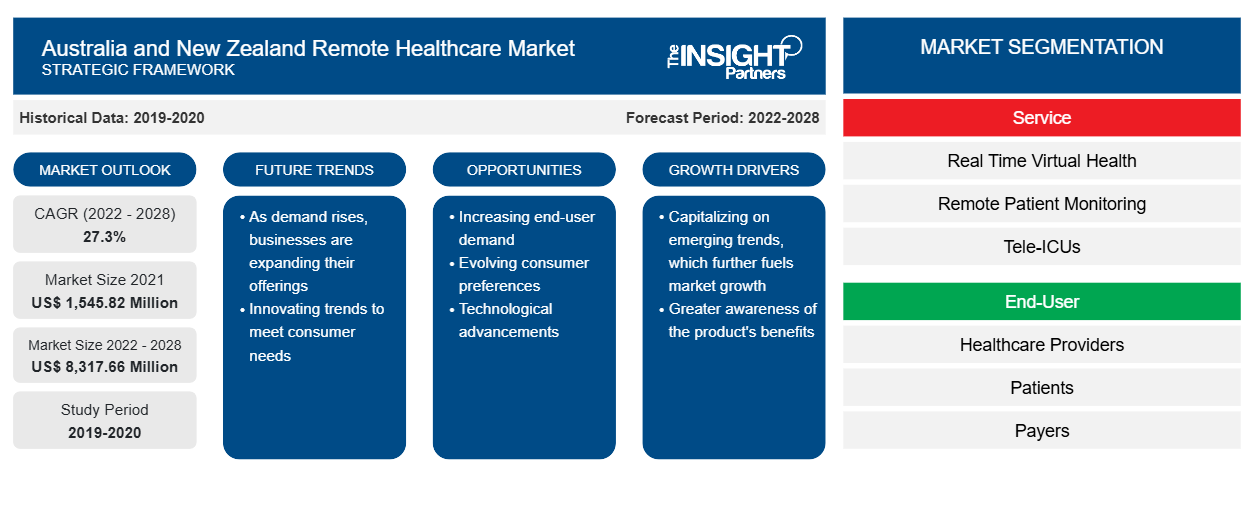

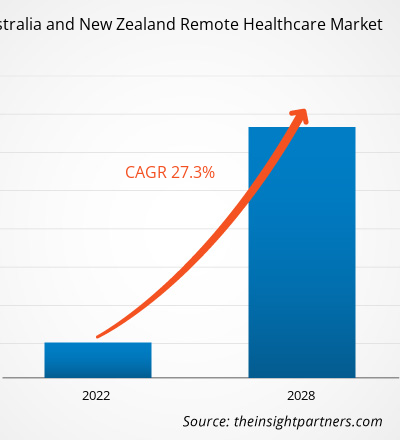

The Australia and New Zealand remote healthcare market was valued at US$ 1,545.82 million in 2021 and is expected to reach US$ 8,317.66 million by 2028; it is anticipated to record a CAGR of 27.3% from 2022 to 2028.

Remote health is revolutionizing the healthcare industry and can be seen as a subset of healthcare IT that offers medical assistance to remotely located patients. It is a telemedicine service that minimizes hospital visits and reduces patient waiting time. Moreover, it allows constant monitoring of the patient's condition and performs preventive and control check-ups outside medical facilities. This form of care is done using mobile devices which measure vital signs.

The growth of the Australia and New Zealand remote healthcare market is attributed to the factors such as rise in the use of telehealth and virtual care during the COVID-19 pandemic and increase in investment in telehealth. However, data safeguarding concerns are hampering the market growth.

New Zealand Remote Healthcare Market Revenue and Forecast to 2028 (US$ Million)

- This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Market Insights

Increase in Number of Digital Health Users

People in Australia and New Zealand are already using digital apps, tools, and services as the preferred way to manage their personal and professional lives. Telehealth remains a constant part of Australia’s health system, which has enhanced access to quality health care for Australians. More than 100 million telehealth services have been provided to 17 million Australians since March 2020. Digital health is an umbrella term indicating a range of technologies that can be used to treat patients and gather and share a person’s health information. Digital health includes mobile health, electronic prescribing, electronic health records, telemedicine and telehealth, and robotics and artificial intelligence.

According to the Australian Digital Health Agency (ADHA) statistics, the number of records with data in them on My Health Record grew from 5.39 million in January 2019 to 22.31 million in December 2021, with more than 537 million documents uploaded. Monthly views of content on the platform were 476% higher between July and December 2021 (6.08 million avg/month) compared with pre-pandemic views from March 2019 to February 2020 (1.06 million avg/month).

Now and in the future, high-quality digital information remains an important aspect of health care. In particular, improving standardizing and health data development could lead to better information to use and share within the health care system. Thus, the improving user experience in digital health is expected to catalyze the growth of the Australia and New Zealand remote healthcare market.

The COVID-19 outbreak positively impacted the growth of the remote healthcare market in Asia Pacific. The Government of Australia expanded Australians' access to telehealth in March 2020 to minimize the risk of community transmission. Over 200 telehealth services were made permanently available. The MBS video and telephone services are available nationally from medical specialists, GPs, and other health professionals. In July 2022, a new temporary telehealth service was introduced that allows longer telephone consultations for patients who have received a positive COVID-19 test. Also, virtual health care (VHC) COVID-19 home monitoring for patients with mild to moderate illness was adopted as a central strategy in Australia to reduce pressure away from acute health systems. Thus, the growing government support for remote patient monitoring for the treatment of COVID-19 is supporting the Australia and New Zealand remote healthcare market.

Service-Based Insights

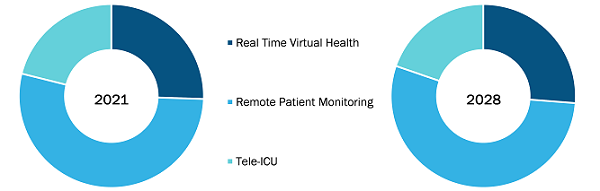

Based on service, the remote healthcare market is segmented into real time virtual health, remote patient monitoring, and tele-ICUs. The remote patient monitoring segment held the largest market share in 2021. However, the real time virtual health segment is anticipated to register the highest CAGR in the market during the forecast period (2022–2028). Remote patient monitoring (RPM) is a method of healthcare delivery through digital health platforms that enables patients to be evaluated outside traditional healthcare settings, in their homes, or community. RPM can significantly reduce a patient's time in the hospital and allow them to recover under monitoring at home. RPM is especially effective for chronic conditions such as heart disease, chronic obstructive pulmonary disease (COPD), and asthma. Also, a rise in product development is likely to favor the market growth. During the pandemic, “COVIDWatch” was developed by the University of Pennsylvania's health system. It is an RPM program that uses automated twice-daily short message service questionnaires to track symptoms.

Australia and New Zealand Remote Healthcare Market, by Service – 2021 and 2028

- This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Based on end user, the remote healthcare market is segmented into healthcare providers, patients, payers, and employer groups & government organizations. The healthcare providers segment held the largest share of the market in 2021. However, the payers segment is anticipated to register the highest CAGR in the market during the forecast period (2022–2028).

Customize This Report To Suit Your Requirement

You will get customization on any report - free of charge - including parts of this report, or country-level analysis, Excel Data pack, as well as avail great offers and discounts for start-ups & universities

Australia and New Zealand Remote Healthcare Market: Strategic Insights

- Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

You will get customization on any report - free of charge - including parts of this report, or country-level analysis, Excel Data pack, as well as avail great offers and discounts for start-ups & universities

Australia and New Zealand Remote Healthcare Market: Strategic Insights

- Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Product launches and approvals are the commonly adopted strategies by companies to expand their global footprints and product portfolios. Various companies in the Australia and New Zealand remote healthcare market focus on the collaboration strategy to expand their clientele, which, in turn, helps them maintain their brand name across the world.

The Australia and New Zealand remote healthcare market is segmented based on service and end user. Based on service, the market is segmented into real time virtual health, remote patient monitoring, and tele-ICU. In terms of end user, the market is segmented into healthcare providers, patients, payers, and employer groups and government organizations.

Company Profiles

- BIOTRONIK SE & Co KG

- Koninklijke Philips NV

- Hicuity Health Inc

- Medtronic Plc

- American Well Corp

- Teladoc Health Inc

- BioTelemetry Inc

- Abbott Laboratories

- GE HealthCare

- Siemens Healthcare GmbH

Australia and New Zealand Remote Healthcare Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2021 | US$ 1,545.82 Million |

| Market Size by 2028 | US$ 8,317.66 Million |

| CAGR (2022 - 2028) | 27.3% |

| Historical Data | 2019-2020 |

| Forecast period | 2022-2028 |

| Segments Covered |

By Service

|

| Regions and Countries Covered | Australia

|

| Market leaders and key company profiles |

|

Australia and New Zealand Remote Healthcare Market Players Density: Understanding Its Impact on Business Dynamics

The Australia and New Zealand Remote Healthcare Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

- Get the Australia and New Zealand Remote Healthcare Market top key players overview

Frequently Asked Questions

What is remote healthcare?

What are the driving factors for the Australia and New Zealand remote healthcare market?

Who are the major players in Australia and New Zealand remote healthcare market?

What will be the CAGR of the Australia and New Zealand remote healthcare market during the forecast period?

What was the estimated Australia and New Zealand remote healthcare market size in 2021?

What are the growth estimates for the Australia and New Zealand remote healthcare market till 2028?

Which segment is dominating the Australia and New Zealand remote healthcare market based on service?

Which country accounts for major market share in 2021 in Australia and New Zealand remote healthcare market?

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Get Free Sample For

Get Free Sample For