Clinical Trial Imaging Market Analysis and Opportunities by 2028

Clinical Trial Imaging Market Forecast to 2028 - Industry Analysis By Modality [Tomography, Magnetic Resonance Imaging (MRI), Ultrasound, Positron Emission Tomography (PET), X-Ray, Echocardiography, and Others], Offering (Operational Imaging Services, Imaging Software, Read Analysis Services, Trial Design and Consulting Services, and Others), and End User [Contract Research Organizations (CROs), Pharmaceutical and Biotechnology Companies, Academic and Research Institutes, and Others]

- Status : Published

- Report Code : TIPHE100001201

- Category : Life Sciences

- No. of Pages : 186

- Available Report Formats :

- Last update date : June 12, 2024

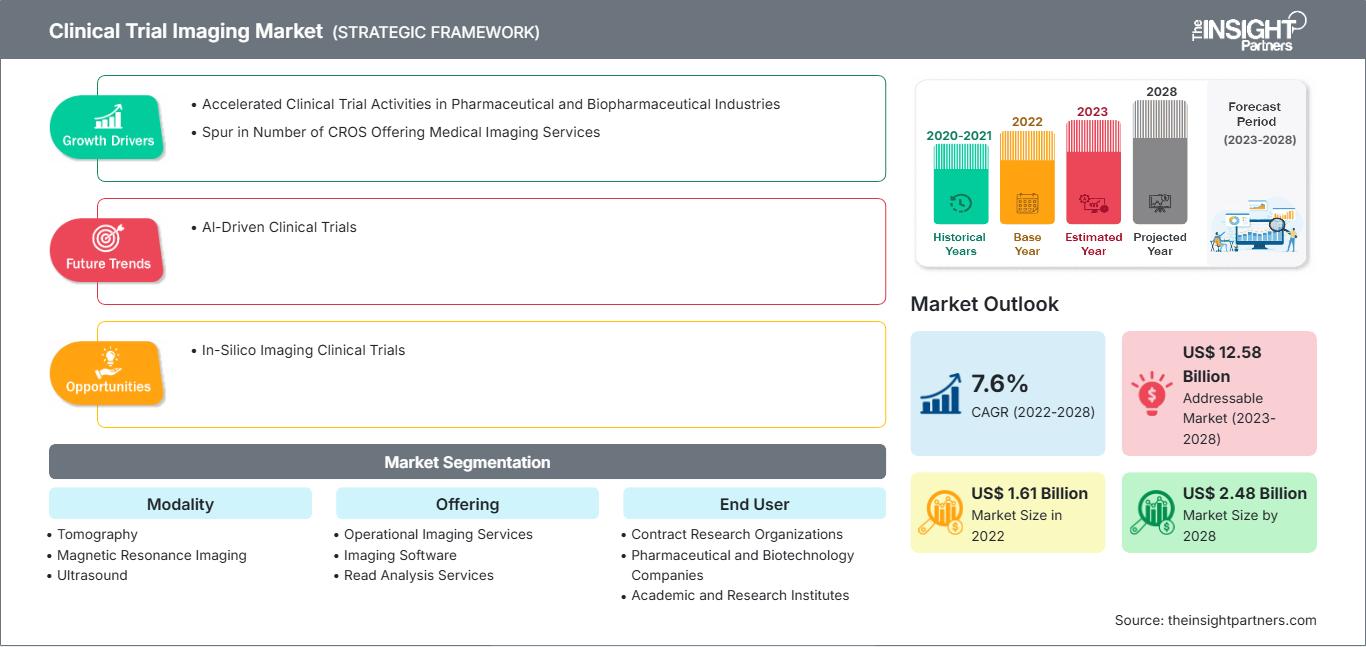

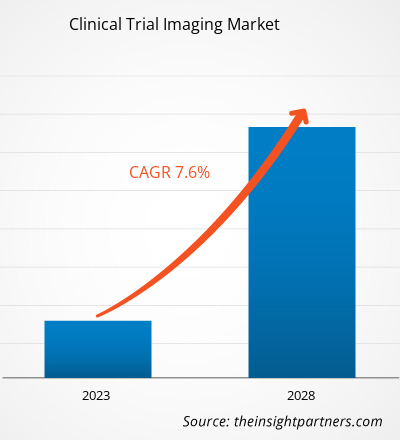

2022 Market Size

US$ 1.61 Bn

Base year value

2028 Forecast

US$ 2.48 Bn

Projected by 2028

CAGR 2023-2028

7.6 %

Growth rate

Addressable Market

US$ 12.58 Bn

(2023-2028)

[Research Report] The clinical trial imaging market size is expected to reach US$ 2,480.32 million by 2028 from US$ 1,610.70 million in 2022; it is estimated to record a CAGR of 7.6% from 2023 to 2028.

Market Insights and Analyst View:

Clinical trial imaging is a research study conducted with people who volunteer to take part. The study mainly aims to determine the value of imaging procedures for detecting, diagnosing, guiding, or monitoring the treatment of disease. Some image interpretation processes may include the use of test images intermixed among the clinical trial images such that readers are intermittently tested as to the proficiency and/or consistency in their reads. Failure to sustain proficiency may result in replacement of a reader with another trained and qualified reader. Rapid increase in utilization of imaging endpoints in multicenter clinical trials, the amount of data and workflow complexity have also increased. A Clinical Trial Imaging Management System (CTIMS) is required to comprehensively support imaging processes in clinical trials as to follow a seamless workflow and also improve patient outcomes. Key regulatory requirements of CTIMS were extracted through a thorough review of many related regulations and guidelines including International Conference on Harmonization-GCP E6, FDA 21 Code of Federal Regulations parts 11 and 820, Good Automated Manufacturing Practice, and Clinical Data Interchange Standards Consortium.

Growth Drivers and Challenges:

Clinical research organizations (CROs) assist in the successful implementation of clinical trials through the services offered using high-quality facilities and deep subject matter expertise. CROs have begun acting as a backbone of the clinical trial industry through their efficient and cost-effective operations that benefit trial sponsors. For example, on an average, CROs take 30% lesser time than in-house activity to conduct and complete clinical trials.

With the rising number of CROs leading to high competition, some of these businesses offer specialized imaging services, thus emerging as imaging CROs (iCROs). Keosys Medical Imaging and Medica Group PLC are the iCROs examples. The total number of clinical trials has doubled since 2010, and the use of imaging modalities in these trials has increased by almost 500%. Per a report by KEOSYS MEDICAL IMAGING company, iCROs allocate 7.5–10% of their budgets for imaging, which helps them optimize their workflow to manage every step of the process from image acquisition to interpretation. These CROs offer key knowledge insights in areas such as site qualification for imaging, acquisition of standardized images, and determination of read designs and criteria, thereby contributing to the growth of the global clinical trial imaging market.

Market Assessment and Insights

- North America dominated the market with 40.8% share in 2022.

- Asia Pacific is poised to grow at a CAGR of 8.2% over the forecast period.

- United States market is projected to grow at a CAGR of 8% over the forecast period.

- By Modality, the Tomography segment accounted for the largest market share of 38.1% in 2022.

- By Offering, the Imaging Software segment is anticipated to witness the fastest growth, registering a CAGR of 8.2% over the forecast period

- By End User, the Contract Research Organizations segment accounted for the largest market share of 45.4% in 2022.

- The report profiles key industry players such as ICON Plc, Medpace Holdings Inc, BioTelemetry Inc, VIDA Diagnostics Inc, Calyxt Inc, eResearch Technology Inc, NEWTONE TECHNOLOGIES, Medical Metrics Inc, WCG Clinical Inc, Radiant Sage LLC, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Clinical Trial Imaging Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Clinical trials help determine if a new form of treatment or prevention, such as a new drug, diet, or medical device, is safe and effective. The trials are mainly carried out during drug development. According to the data provided by the National Library of Medicine (NLM), ~52,000 new studies were registered with NLM (ClinicalTrials.gov) in 2020, which increased to ~58,000 in 2023. In January 2023, the NLM reported 38,837 active clinical trials in the US and 105,172 active trials worldwide. According to European Medicine Agency, in the European Union (EU), ~4,000 clinical trials are authorized annually, of which about 60% of clinical trials are associated with the pharmaceutical industry. An increasing number of clinical trials for developing different effective treatments due to the rising prevalence of chronic diseases globally is fuelling the growth of the clinical trial imaging market.

Further, clinical trials are increasingly becoming complex procedures, owing to which proper execution and overseeing of the operation occurring in research-based organizations has become crucial. To avoid errors due to improper execution, research-based organizations are outsourcing clinical trials to develop their products. Clinical research organizations (CROs) assist in successfully implementing clinical trials through the services offered using high-quality facilities and deep subject matter expertise. CROs have begun acting as a backbone of the clinical trial industry through their efficient and cost-effective operations benefitting trial sponsors. According to the blog published on Thermo Fisher Scientific, in 2022, ~3 out of 4 clinical trials were carried out by CROs to reassure the clinical programs of drug developers, provide a wealth of expertise, drive time and cost efficiencies, and deliver customized, high-quality data. Thus, the development of cost-effective solutions and decreasing errors in CROs during the drug development process are driving the clinical trial market growth, which in turn is increasing the clinical trials imaging market.

The pharmaceutical industry is one of the most R&D-intensive industries globally. The value of medicines is becoming increasingly important as pharmaceutical companies are keen to ensure that R&D achieves their intended goal. Over the last decade, the number of new drugs approved yearly has also increased. Per the Food and Drug Administration (FDA) approved 37 new drugs annually in 2022. Efforts are being made to achieve greater effectiveness and efficiency in fulfilling patients' needs. The research-based industry allocates ~15–20% of revenues to R&D activities and invests more than US$ 50 billion in R&D annually. Globally, the US is a leading country in R&D investments, producing over half of the world’s new molecules in the past decade. As per the European Federation of Pharmaceutical Industries and Associations (EFPIA), in 2019, North America accounted for 48.7% of global pharmaceutical sales. The US accounted for 62.3% of sales of new medicines launched during 2014–2019. R&D is a significant and essential part of the business of pharmaceutical companies as it enables them to come up with new molecules for various therapeutic applications with significant medical and commercial potential.

R&D Investments by Major Pharmaceuticals Companies

Company |

R&D Investment in 2021 (US$ Billion) |

R&D Investment in 2022 (US$ Billion) |

|

Takeda Pharmaceutical Co Ltd |

4.2 |

4.6 |

|

Pfizer Inc |

10.3 |

11.4 |

|

Grifols SA |

404.57 |

427.05 |

Note: Current conversion rate is considered for presenting the currencies.

Source: Annual Reports and The Insight Partners Analysis

R&D expenditure is done to discover, examine, and produce new products; upfront payments; ; improve existing outcomes; and demonstrate product efficacy and regulatory compliance before launch. The R&D investments differ as per the need and demand for clinical trials. The cost includes materials, supplies used, and salaries, along with the cost of developing quality control.

The companies mentioned above and hospitals are investing in developing products to treat various diseases and disorders, such as immunological disorders. In June 2021, Takeda announced ADVANCE-1, a randomized, placebo-controlled, double-blind Phase 3 clinical trial that evaluate HYQVIA [Immune Globulin Infusion 10% (Human) with Recombinant Human Hyaluronidase] to maintain treatment of chronic inflammatory demyelinating polyradiculoneuropathy (CIDP), that will meet its primary endpoint. Thus, increasing R&D investments by companies coupled with the advanced pharmaceutical industry are fueling the clinical trials imaging market growth.

For pharmaceutical and biopharmaceutical companies, active participation in clinical research is rewarding but demanding, and medical imaging is becoming an integral part of the research. However, the unique technical specifications and administrative aspects of clinical trial and imaging modalities vary substantially from standard-of-care imaging, thus burdening an established clinical infrastructure at investigational sites. Failure to comply with such clinical requirements results in the generation of noncredible data, need for repetitive imaging, and removal of patient enrollment for the trial. Further, the lack of appropriate infrastructure at investigational sites may hinder the efforts made by CROs to address such challenges. Clinical trial imaging equipment seeks hefty investments of resources from stakeholders. For example, drug or device investigational sites must meet clinical trial requirements and infrastructure, maintain superiority in patient care, and guarantee trial integrity. Moreover, clinical trial sponsors must acknowledge the burden of clinical trial imaging by providing support for the development of necessary local infrastructure for meeting the abovementioned requirements. The Quantitative Imaging Biomarkers Alliance by the Radiologic Society of North America seeks to define standard imaging protocols and workflows, ensuring consistency in the examination of images for producing quantifiable clinical trial results. Thus, high investments and standardized infrastructure requirements impede the growth of the global clinical trial imaging market.

Report Segmentation and Scope:

The “Global Clinical Trial Imaging Market” is segmented based on modality, offering, end user, and geography. Based on modality, the clinical trial imaging market is segmented into tomography, ultrasound, positron emission tomography, X-ray, echocardiography, magnetic resonance imaging, and others. Based on offering, the clinical trial imaging market is segmented into trial design consulting services, read analysis services, operational imaging services, imaging software, and others. Based on end user, the clinical trial imaging market is segmented into pharmaceutical & biopharmaceutical companies, contract research organizations, and academic & government research institutes, and others. The clinical trial imaging market based on geography is segmented into North America (the US, Canada, and Mexico), Europe (Germany, France, Italy, the UK, Russia, and Rest of Europe), Asia Pacific (Australia, China, Japan, India, South Korea, and Rest of Asia Pacific), the Middle East & Africa (South Africa, Saudi Arabia, the UAE, and Rest of the Middle East & Africa), and South & Central America (Brazil, Argentina, and Rest of South & Central America).

Segmental Analysis:

The global clinical trial imaging market, offering, has been segmented into trial design consulting services, read analysis services, operational imaging services, imaging software, and others. Operational imaging services segment held the largest share in 2021 and is expected to continue a similar trend during the forecast period. Operational imaging services include imaging modalities such as MRI, CT, ultrasound, PET, and SPECT for therapeutic applications such as neurology, oncology, cardiovascular diseases, gastroenterology, musculoskeletal disorders, and medical devices used to conduct clinical trials. Clinical imaging, a non-invasive method of research, has a number of advantages for the advancement of medical science in general, as well as clinical studies in particular. As a consequence, there is a strong and growing trend to incorporate novel imaging technologies deeply into clinical trials, making them a fundamental element of biotech, pharmaceuticals, and medical devices.

Also, choosing the right read design is crucial when executing imaging in a trial. The read design refers to the number and type of readers used to capture and interpret the images. Reducing variability leads to crucial challenges in image capture and analysis since trials can include imageries obtained from various imaging modalities, requiring a review by experts such as radiologists, pathologists, and cardiologists. The type of read design used is paramount to reduce bias when interpreting medical images in clinical trials. Single reads, double reads, and double reads with adjudicators are the three primary types of read designs. The image is interpreted only by one reader in a single read. In a double read, two or more readers interpret it. Large trials may require multiple readers due to a heavy workload. Ideally, one (or two in the case of a double-read design) reader(s) will review all the images of the same patient throughout the study. Multiple readers reviewing different imaging time points of the same patient may result in additional variations. An oncology trial, for instance, usually involves the following stages: initial screening for lesion selection and measurement before treatment, the sequential selection and measurement of a lesion at each follow-up imaging visit, and the assessment of incremental radiological response at each time point.

Keosys Medical Imaging offers web-based imaging and reading software for applications in clinical trials to limit reader subjectivity; increase measurement and quantification accuracy; and improve overall operational efficiency, data quality, and traceability. An advanced lesion management system and specialized applications for different therapeutic areas are included in the reading software offered by Keosys. The reading software is FDA 510 (k) cleared and ISO 13485 (Medical Devices) compliant.

Based on modality, the clinical trial imaging market is into tomography, ultrasound, positron emission tomography, X-ray, echocardiography, magnetic resonance imaging, and others. Tomography segment held the largest share in 2021 and is expected to continue a similar trend during the forecast period. In tomography, shadows of superimposed structures are blurred by a moving X-ray tube that is used for X-ray imaging. Computed tomography (CT) scan imaging used in research and clinical trials combines X-ray images taken from different angles, followed by computer processing to provide cross-sectional images of bones, blood vessels, and soft tissues. Linear and nonlinear tomography systems operate in a similar way—a tube moves in one direction, while a film cassette moves in the opposite direction, centered around a fulcrum in both techniques.

The introduction of new imaging methods or the refinement of existing methods requires accurate timing in relation to specific disease treatment. Scheduling imaging at an apt time is essential for correctly interpreting the subject’s anatomy. In hospitals, it helps effectively administer treatments such as surgery, radiation therapy, or chemotherapy while monitoring the patient's toxicity and morbidity. Clinical research in the field of oncology relies heavily on imaging, and scanning procedures performed at certain durations, intensities, and frequencies are fundamental to the trial protocols.

Advanced imaging metrics with CT scans are used extensively in new drug development and cancer research. It is the most used imaging modality for research related to advanced cancer types, affecting the neck, chest, abdomen, or pelvis.

Regional Analysis:

Based on geography, the clinical trial imaging market is segmented into five key regions: North America, Europe, Asia Pacific, South & Central America, and the Middle East & Africa. In 2021, North America held the largest share of the clinical trial imaging market followed by Europe. The US has emerged as a leading clinical research destination. Nearly half of the total clinical trials conducted globally are conducted in the US. Additionally, most pharma research companies prefer to perform clinical trials in the US owing to established medical infrastructure, fast approval timelines, a favorable regulatory framework, and accepted clinical trial generated data globally. A World Health Organisation (WHO) report states that the US registered the highest number of clinical trials (157,618) in 2021.

The following table illustrates the number of clinical trials registered in the US with the number of total patients recruited in them, along with the percentage share of the US for the said parameters in the world.

2023 |

Registered Clinical Trial Studies |

Patient Recruited in Studies |

|

US |

139,632 (31% of the global studies) |

20,680 (32% of the worldwide headcount) |

Source: ClinicalTrial.gov report

Innovative products launched by companies for applications in clinical trials further boost the growth of the clinical trial imaging market in the US. Medical Metrics, a CRO providing imaging services for clinical trials, offers "Assessa." This product assists in the improvement of decision-making in drug discovery and related clinical studies, particularly in the discovery of drugs for neurological disorders, such as dementia; cognitive impairment; and Alzheimer's, Schizophrenia, Parkinson's Disease, and other memory-related diseases. The rising number of clinical trials in the US favors the growth of the clinical trial imaging market in the country.

Clinical Trial Imaging Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 1.61 Billion |

| Market Size by 2028 | US$ 2.48 Billion |

| Global CAGR (2022 - 2028) | 7.6% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2028 |

| Segments Covered |

By Modality

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Clinical Trial Imaging Market Players Density: Understanding Its Impact on Business Dynamics

The Clinical Trial Imaging Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Industry Developments and Future Opportunities:

Various initiatives taken by key players operating in the global clinical trial imaging market are listed below:

- In December 2022, Tata Consultancy Services (TCS) (BSE: 532540, NSE: TCS) announced that the TCS ADD Connected Clinical Trials platform for decentralized trials, has won the India Pharma Award 2022 in the category, Excellence in Ancillary Pharma Services.

- In October 2021, Medidata, a Dassault Systèmes company, announced that Rave Imaging, the company’s cloud-based, secure clinical trial imaging management platform, has reached a significant milestone, having supported more than 1,000 imaging studies. Rave Imaging, built on the Medidata Unified Platform, processes more than 100 million images per year. The technology provides real-time visibility into all imaging-related trial activities across all Rave Imaging trials to enhance study efficiency.

Competitive Landscape and Key Companies:

The clinical trial imaging market majorly consists of players such as eResearch Technology Inc, Calyx Inc, ICON PLC, VIDA Diagnostics Inc, WCG Clinical Inc, BioTelemetry Inc, Medical Metrics Inc, Medpace Holdings Inc, Radiant Sage LLC, and IXICO plc. The companies have been implementing various strategies that have helped their growth and, in turn, have brought about various changes in the market. The companies have utilized organic strategies (such as launches, expansion, and product approvals) and inorganic strategies (such as product launches, partnerships, and collaborations).

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends