Digital Radiography in Chest Radiography Market Growth, Demand & Size by 2034

Coverage: by Product Type (CR Tech Digital X Ray System, and DR Tech Digital X Ray System); End Use (Hospitals, Diagnostic Centers, Specialty Clinics, and Others), and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00023280

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 08, 2026

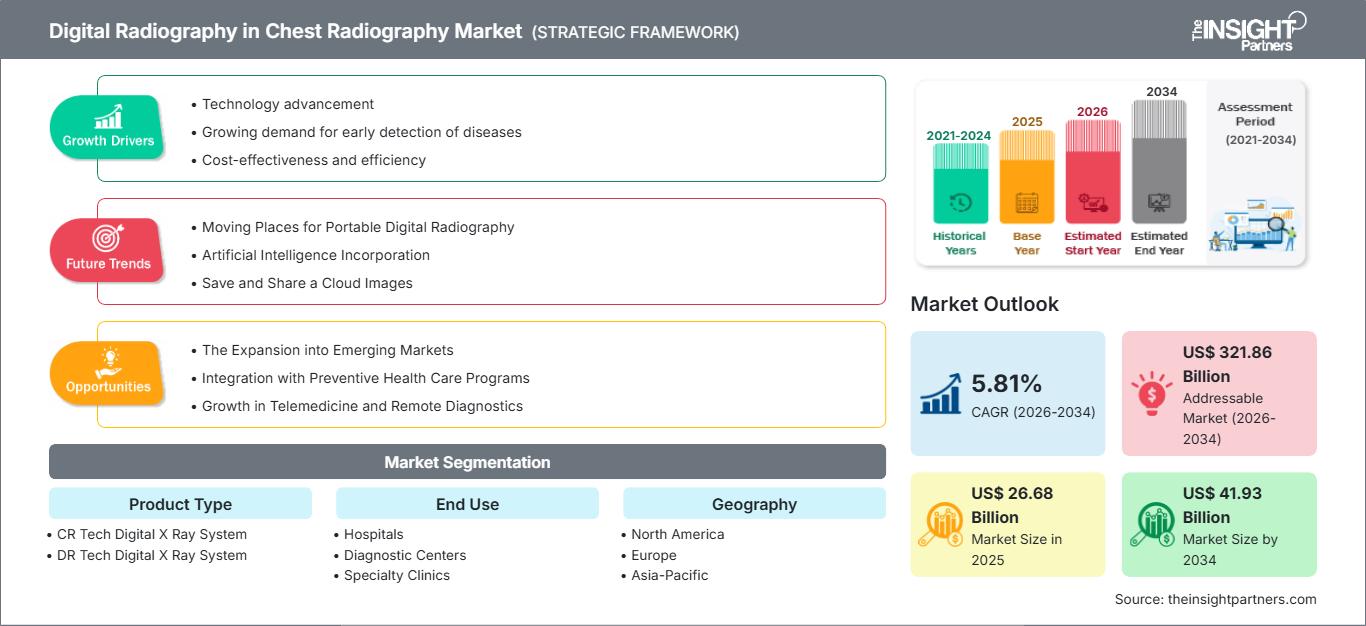

2025 Market Size

US$ 26.68 Bn

Base year value

2034 Forecast

US$ 41.93 Bn

Projected by 2034

CAGR 2026-2034

5.81 %

Growth rate

Addressable Market

US$ 321.86 Bn

(2026-2034)

The Digital Radiography in Chest Radiography market is becoming central to high-volume diagnostic imaging as providers prioritize faster acquisition, lower repeat rates, and consistent image quality. The market was valued at US$ 26.68 billion in 2025 and is projected to reach US$ 41.93 billion by 2034, advancing to a CAGR of 5.81% from 2026 to 2034. Growth is anchored in hospital modernization, chest disease screening, and broader migration from computed radiography to direct digital platforms.

North America remains structurally important for Digital Radiography in Chest Radiography market, with an estimated CAGR of 5.2%–5.8% through 2034. Demand is supported by replacement of aging radiography rooms, strong use of chest imaging in emergency and inpatient workflows, and pressure to improve technologist productivity. Integration with PACS, AI-enabled positioning support, and portable DR adoption are also reinforcing regional growth.

Digital Radiography in Chest Radiography Market Assessment and Insights

- North America: North America accounted for a 36–40% share in 2025 and is anticipated to expand at a CAGR of 5.3%–5.8% during 2026–2034. Advanced imaging infrastructure, increasing adoption of AI-enabled chest radiography solutions, and continued investments in digital healthcare technologies support regional Digital Radiography in Chest Radiography market leadership.

- U.S.: The U.S. represented 82–86% of the North American Digital Radiography in Chest Radiography market size in 2025 and is projected to register a CAGR of 5.4%–5.9% during 2026–2034, supported by widespread deployment of digital X-ray systems, healthcare infrastructure modernization, and growing use of AI-assisted diagnostic imaging.

- Europe: Europe held 25–29% of the Digital Radiography in Chest Radiography market share in 2025 and is expected to grow at a CAGR of 5.1%–5.6% during 2026–2034. Germany, the United Kingdom, and France remain the leading regional markets due to healthcare modernization, replacement of legacy imaging systems, and expanding digital hospital initiatives.

- Asia Pacific: Asia Pacific accounted for 24–28% of the Digital Radiography in Chest Radiography market share in 2025 and is forecast to expand at a CAGR of 6.4%–6.9% during 2026–2034. China, Japan, and India continue to drive regional growth through expanding healthcare infrastructure, increasing diagnostic imaging capacity, and broader adoption of digital radiography technologies.

- Largest Segment: Product – DR Tech Digital X-Ray System represented the largest Digital Radiography in Chest Radiography market segment and is expected to record a CAGR of 6.2%–6.7% during 2026–2034, reflecting superior image quality, reduced examination time, and seamless integration with digital healthcare workflows.

- High Growth Segment: End User – Diagnostic Centers is projected to grow at a CAGR of 6.5%–7.0% during 2026–2034, driven by rising outpatient imaging demand and continued investments in advanced diagnostic capabilities.

- Key companies analyzed in detail: GE HealthCare Technologies Inc.; Siemens Healthineers AG; Koninklijke Philips N.V.; Agfa-Gevaert NV; FUJIFILM Holdings Corporation; Angell Technology Co., Ltd.; Carestream Health, Inc.; Beijing Wandong Medical Technology Co., Ltd.; Canon Inc.; Konica Minolta, Inc.; Samsung Electronics Co., Ltd.; Shimadzu Corporation; Shenzhen Mindray Bio-Medical Electronics Co., Ltd.; Source-Ray, Inc.; and Hitachi, Ltd.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

The Digital Radiography in Chest Radiography Market report has moved from digitizing analog workflows toward optimizing chest imaging as a critical diagnostic gateway. Computed radiography helped facilities reduce film dependence, but direct digital radiography is increasingly preferred for faster throughput, lower retake burden, and better integration with image archives. Chest radiography’s role in respiratory, cardiac, emergency, and preoperative assessment keeps utilization resilient across care settings.

Over the forecast period, purchasing decisions will be shaped by productivity rather than hardware replacement alone. Hospitals and diagnostic centers are expected to prioritize systems that support automated positioning, dose management, mobile bedside imaging, and seamless interoperability. Vendors with scalable detector portfolios, service networks, and workflow software will be better positioned as providers balance capital constraints with rising chest imaging demand.

Digital Radiography in Chest Radiography Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 26.68 Billion |

| Market Size by 2034 | US$ 41.93 Billion |

| Global CAGR (2026 - 2034) | 5.81% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Digital Radiography in Chest Radiography Market Analysis

Demand for Digital Radiography in Chest Radiography highly depends on imaging volumes, urgency of treatment, and efficiency of workflows. Chest X-rays continue to be one of the most commonly performed imaging examinations due to their ability to facilitate rapid diagnosis of pneumonia, tuberculosis, COPD, trauma, heart failure, and post-operative complications. Digital technology shortens turnaround times and allows doctors to interpret images remotely through a network.

The value chain comprises producers of flat panel detectors, producers of X-ray generators, assemblers of digital radiography systems, providers of imaging software, distributors, service organizations, and users of health care. Hospitals often need integration into their IT infrastructure and reliable operation, whereas imaging centers require low costs per exam and high patient flow. Specialized clinics choose compact and mobile solutions when chest imaging contributes to specific treatment pathways.

Competition is defined by installed base strength, detector quality, software depth, and service responsiveness. GE Healthcare, Siemens Healthcare, Philips Healthcare, Fujifilm, Canon, Konica Minolta, Samsung, Shimadzu, Agfa HealthCare, Carestream Health, Hitachi, Mindray, Wandong Medical, Angell Technology, Land Wind, and Source Ray compete across premium, mid-range, and value-focused segments with differing regional intensity.

Investment is moving toward intelligent radiography rooms, portable DR fleets, retrofit detectors, and software that standardizes chest imaging quality across sites. Strategic positioning increasingly depends on helping providers manage staffing pressure, lower radiation exposure, and accelerate diagnosis. Vendors able to combine equipment financing, lifecycle service, and analytics-based workflow improvement are likely to gain preference in replacement cycles.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Digital Radiography in Chest Radiography Market: Strategic Insights

Regional Insights

North America Digital Radiography in Chest Radiography Market

North America is expected to post a CAGR of about 5.2%–5.8%, supported by high radiology utilization, mature hospital networks, and ongoing replacement of legacy rooms. Chest radiography is embedded in emergency departments, inpatient monitoring, pre-surgical evaluation, and respiratory care, making digital performance central to operational planning.

Regional buyers are prioritizing automation, dose consistency, and portable imaging for intensive care and isolation environments. Vendor competition is strong because large health systems often standardize procurement across multiple facilities. This favors suppliers with broad modality portfolios, cybersecurity-ready connectivity, and reliable field service coverage.

U.S. Digital Radiography in Chest Radiography Market

The US accounts for about 75%-80% of revenue generated in North America and is expected to grow at a CAGR close to 5.4%. The demand is driven by the volume of procedures, health system consolidation, and the increase in outpatient imaging.

Some of the leading vendors in North America include GE Healthcare, Siemens Healthcare, Philips Healthcare, Fujifilm, Canon, Konica Minolta, Samsung, Carestream Health, and Shimadzu. The US has seen a trend towards mobile DR in chest examination, use of AI to enhance quality assurance, and an efficient reporting process to avoid turnaround delays.

Europe Digital Radiography in Chest Radiography Market

Europe makes up about 22%–27% of global demand with a CAGR of around 4.8%–5.4% of the Digital Radiography in Chest Radiography market. Germany is at the top, driven by high standards of hospital infrastructure, procurement discipline, and imaging quality requirements. The rate of growth in the region is steady and not explosive due to the already existing digitalization of many systems.

Capacity-driven in the UK, the Digital Radiography in Chest Radiography market is determined by the need to relieve imaging providers in both public and private sectors of the pressure on capacity. The deployment of digital chest radiography technologies aims to reduce waiting times, increase efficiency, and support community imaging pathways. Digital chest radiography portable systems help with patient transport in hospitals and elderly care settings where transporting patients to radiology rooms is often ineffective.

Germany enjoys strong local engineering traditions, highly developed radiology departments, and the need for durable high-throughput systems. In France, Italy, and Spain, there is an improvement in digital access with hospital upgrades, private diagnostics networks, and respiratory disease management.

APAC Digital Radiography in Chest Radiography Market

APAC is the fastest-growing regional Digital Radiography in Chest Radiography market, with an estimated CAGR of 6.3%–7.1% and a global share range of 30%–35%. China leads regional demand due to large hospital networks, local manufacturing capacity, and continued investment in diagnostic infrastructure. Chest radiography volumes are substantial across both urban and lower-tier healthcare systems.

Japan and South Korea contribute through advanced technology adoption, aging populations, and strong emphasis on image quality. India is expanding through private diagnostic chains, public hospital modernization, and tuberculosis and respiratory disease screening needs. Australia shows stable replacement demand, particularly in hospitals seeking portable imaging and integrated digital workflows.

Industrial and policy drivers include domestic medical device production, universal health coverage expansion, and government-backed diagnostic access programs. Regional competition is broad, with global brands competing against value-oriented manufacturers such as Wandong Medical, Mindray, Angell Technology, and Land Wind. Buyers often balance affordability with service availability and detector reliability.

Middle East & Africa Digital Radiography in Chest Radiography Market

The Middle East & Africa Digital Radiography in Chest Radiography market is projected to grow at a CAGR of about 5.0%–5.7%, with Saudi Arabia leading regional adoption. Growth is linked to hospital construction, medical tourism, urban specialty care, and public health investment. Chest radiography remains a practical first-line imaging tool across emergency, infection, and occupational health use cases.

Saudi Arabia and the UAE are investing in digital hospitals and advanced diagnostic capacity as part of broader economic diversification. Energy-sector employment, industrial safety programs, and migrant workforce screening support routine chest imaging demand. Hospitals in these markets often seek premium systems with strong service support and enterprise connectivity.

South Africa and the rest of MEA show mixed adoption because procurement budgets and infrastructure readiness vary widely. Portable and retrofit DR solutions are relevant where facilities need digital capability without full room replacement. Infrastructure projects, private clinic expansion, and donor-supported diagnostic programs can create targeted opportunities for cost-effective systems.

Segmentation Analysis

Product Type

- CR Tech Digital X Ray System: CR systems remain relevant for cost-sensitive facilities transitioning from film, offering digital capture through cassette-based workflows while extending the useful life of existing radiography infrastructure.

- DR Tech Digital X Ray System: DR systems lead adoption because they provide faster image acquisition, lower repeat rates, improved workflow automation, and stronger suitability for high-volume chest imaging environments.

End Use

- Hospitals: Hospitals account for the strongest demand as chest radiography supports emergency care, inpatient monitoring, intensive care, preoperative assessment, and respiratory disease pathways requiring reliable high-throughput imaging.

- Diagnostic Centers: Diagnostic centers prioritize DR systems that improve exam speed, patient turnover, image consistency, and reporting connectivity across outpatient networks serving routine chest screening and referral-based imaging.

- Specialty Clinics: Specialty clinics adopt compact or mobile digital radiography where pulmonology, cardiology, occupational health, or urgent care workflows require immediate chest imaging without hospital referral delays.

Opportunity Snapshot

| End Use | Revenue Contribution | Trend Tag | Adoption Stage |

| Hospitals | High | Bedside Imaging | Mature |

| Diagnostic Centers | Medium | Throughput | Scaling |

| Specialty Clinics | Medium | Point Care | Scaling |

| Others | Low | Mobile Access | Emerging |

Digital Radiography in Chest Radiography Market Growth Drivers and Impact Analysis

Rising Chest Imaging Volumes Across Care Pathways

Among diagnostic methods, chest radiography remains highly practical for its speed, cost-effectiveness, and clinical utility. It is used in hospitals for emergency care, inpatient examinations, postoperative follow-ups, and patients with lung and heart-related complaints. In diagnostic clinics, this method is employed for referring patients, employment screening, and chronic disease management. As the number of patients increases, there is a need for technology that increases acquisition speed, minimizes repeat scans, and provides uniform results regardless of the technologist’s level of expertise. Digital radiography can easily meet this challenge, as it enables instant image review, rapid transfer to reporting software, and greater standardization. From a vendor's perspective, the best market opportunities lie in developing systems with high-quality hardware and workflow tools tailored to the intensity of chest imaging.

Shift From CR to DR for Faster Clinical Decisions

One of the most significant drivers of technology adoption in the market is the shift from the CR Tech Digital X-Ray System to the DR Tech Digital X-Ray System. While the former technology was instrumental in helping many facilities digitize at reduced costs, it had several shortcomings, including the need for cassette handling and relatively long processing time, which made it less productive in busy chest imaging departments. The advantages of the DR system include immediate image acquisition, low retake rates, and the ability to easily integrate the equipment with the radiology information system and PACS. Such benefits transform the business models of hospitals and diagnostic centers that need faster reporting and have relatively high volumes of chest imaging procedures. The effect of digital radiography on chest radiography is evident in replacement cycles, retrofitted detectors, and mobile DR systems.

Workflow Automation and Dose Optimization Priorities

The radiology departments continue to experience stress related to manpower shortages, increased imaging workload, and quality assurance across multiple locations. In chest radiography, minor misalignment can undermine diagnostic accuracy, while repeat exams increase costs, radiation dose, and patient discomfort. Systems that automate positioning, exposure, image processing, and quality control assist technologists in performing the exam consistently. Furthermore, there is increasing emphasis on dose management as hospitals become stricter in their governance of patient safety and regulations. The benefit goes beyond image quality, including reduced physical stress for staff, efficient use of space, and standardized processes within enterprise networks. Competitive advantage is thus shifting to workflow capabilities beyond detector technologies.

Digital Radiography in Chest Radiography Market Future Trends

AI-Assisted Acquisition and Quality Control

Artificial intelligence is increasingly being integrated at the image acquisition stage, reflecting key Digital Radiography in Chest Radiography Market trends by improving image quality before radiologist review. AI-enabled tools now support positioning guidance, exposure consistency, anatomical recognition, and automated quality assessment, particularly in emergency departments and at the bedside, where patient positioning is challenging. Forward-looking systems will likely combine acquisition assistance with worklist prioritization and structured quality metrics. The commercial implication is that buyers may evaluate radiography platforms based on measurable workflow benefits rather than just detector resolution. Vendors that can demonstrate reduced repeat exams, faster exam completion, and consistent chest image quality will have an advantage among hospital networks seeking operational resilience.

Expansion of Portable DR for Distributed Care

The use of portable digital radiography is becoming increasingly strategic as care delivery moves beyond fixed radiography rooms. Intensive care units, emergency bays, isolation units, operating recovery areas, and other similar locations require chest imaging without moving fragile patients. Lightweight detectors, built-in charge, positioning options, and onboard wireless capabilities can offer bedside imaging at near-room-quality using portable DR systems. In the long term, hospitals may integrate the management of their portable systems into a unified fleet of devices, with standardized tracking and imaging protocols. Such a trend would be favorable for both high-end mobile DR systems and retrofits of mobile X-ray devices into digital imaging machines.

Digital Radiography in Chest Radiography Market Opportunities

Retrofit DR Upgrades for Cost-Constrained Facilities

Many healthcare providers continue using radiography systems that remain clinically effective but fall short of modern digital workflow standards. Retrofit DR upgrades represent a valuable opportunity, supporting the Digital Radiography in Chest Radiography Market forecast by enabling facilities to enhance chest imaging productivity without replacing complete rooms or mobile units. This strategy would be quite useful for community hospitals, small imaging facilities, specialty clinics, and developing markets with tight capital budgets. Suppliers could position themselves based on detector longevity, ease of installation, training, services, and financing options. The rationale behind this investment is simple – more timely image availability and fewer repeat exams can reduce costs without changing current capabilities. Companies that provide solutions for chest imaging scenarios can capitalize on customers looking to modernize their facilities, without buying new equipment.

Integrated Solutions for Diagnostic Center Networks

Networks of diagnostic centers offer significant opportunities due to the need for standardized quality, guaranteed uptime, and fast throughput across multiple sites. Chest radiography may be a routine, high-volume procedure that affects patient satisfaction and referrals. Providers could add value by providing a suite of radiography solutions, maintenance services, remote management, detector handling, and software solutions for centralized reporting. The key consideration here is not the ownership of the equipment itself, but rather the throughput and image quality achievable. This will provide opportunities for managed services business models, lease arrangements, and even analytics-based preventive maintenance. Firms whose solutions align with the needs of growing networks can build long-term account positions, especially in APAC, the Middle East, and the private outpatient segment.

Recent Developments

- July 2025: GE HealthCare announced commercial availability of Definium Pace Select ET, a floor-mounted digital X-ray system designed for high-throughput environments, with automation, motorized workflow support, and AI-enabled positioning assistance intended to improve consistency and reduce technologist burden in routine radiography.

- January 2025: Siemens Healthineers showcased MULTIX Impact E at AOCR 2025, presenting a locally manufactured digital X-ray system for secondary care settings alongside MRI, CT, and ultrasound innovations. The launch context highlighted accessible imaging, lower radiation exposure, and workflow support for broader diagnostic coverage.

- July 2025: FUJIFILM Healthcare Americas launched FDR Go iQ, a portable digital radiography system for hospitals and ambulatory surgery centers. The system includes tube-head touchscreen controls, smart detector charging, positioning guidance, and bedside imaging features suited to mobile chest X-ray workflows.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends