Endoscopy Device Market Growth and Analysis by 2031

Coverage: By Product (Endoscopes, Visualization Systems, Accessories, and Other Endoscopy Devices), Application (Gastroscopy, Laparoscopy, Arthroscopy, Urology Endoscopy, Bronchoscopy, Laryngoscopy, Otoscopy, and Others), End User (Hospitals, Ambulatory Surgical Centers, and Others), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America)

- Status : Data Released

- Report Code : TIPHE100000823

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : May 30, 2024

2024 Market Size

US$ 44.20 Bn

Base year value

2031 Forecast

US$ 66.46 Bn

Projected by 2031

CAGR 2025-2031

6.0 %

Growth rate

Addressable Market

US$ 393.27 Bn

(2025-2031)

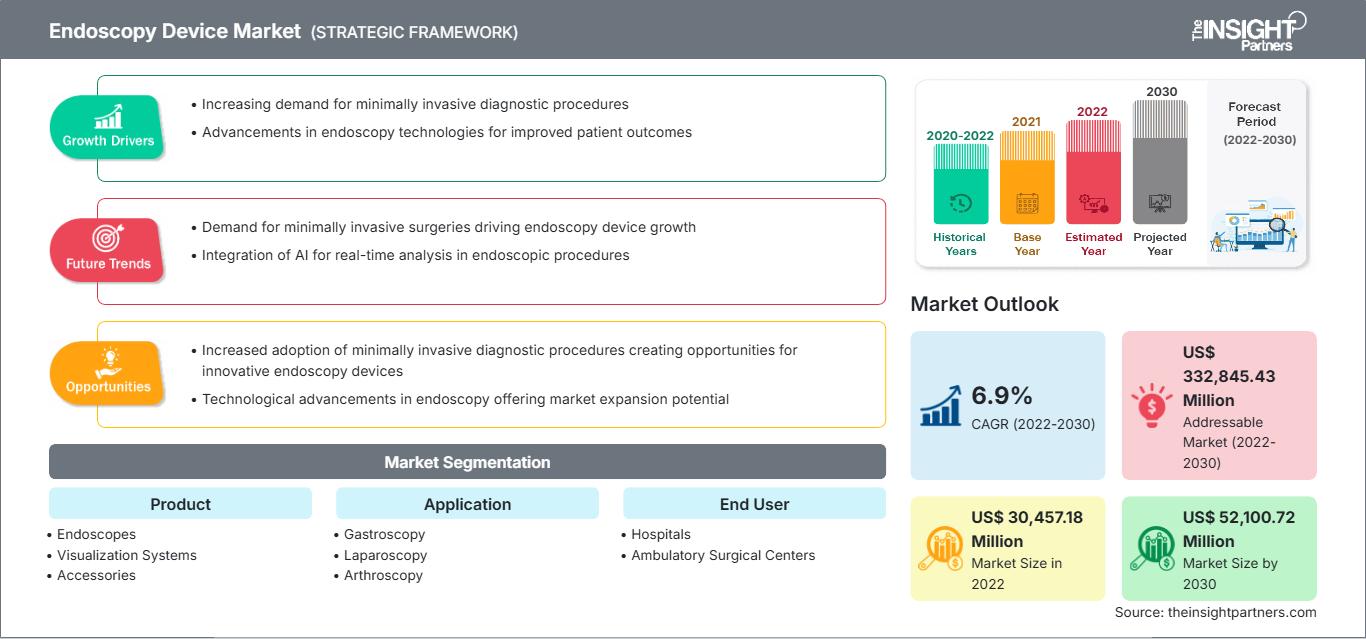

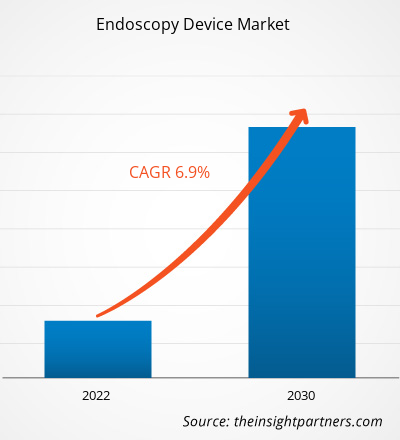

The Endoscopy Devices Market size is expected to reach US$ 66.46 billion by 2031. The market is anticipated to register a CAGR of 6.0% during 2025–2031.

Market Insights and Analyst View:

Endoscopy is a minimally invasive surgical procedure employed to visualize internal organs of the human body; it is also used in surgeries performed on various organs. The procedure is performed with the help of a small flexible tube known as an endoscope. This tube is attached to a camera, enabling a clear view of the organ to be observed. Based on the area to be examined, various types of scopes are available; a few of these are arthroscopes, bronchoscopes, laparoscopes, and hysteroscopes. Various other devices and instruments are used in an endoscopy procedure for better visualization, sterilization, and enhanced-quality imaging.

Growth Drivers:

Increasing Demand for Minimally Invasive Techniques

The growing demand for minimally invasive techniques in surgical procedures reflects a significant shift in medical practice and patient preferences. This trend is driven by the desire to minimize the invasiveness of procedures, reduce the associated risks, and promote faster recovery times. Endoscopy is a minimally invasive surgery procedure that involves a minimal incision size, shortened recovery time, and better visibility into the internal body cavity. A surgeon can visualize and work within the body cavity using an endoscope without making a large incision. Minimally invasive approaches typically involve smaller incisions, and the use of specialized instruments and technologies to access different organs, which can lead to shorter hospital stays and less scarring. Moreover, patients often experience less pain and a quicker return to their daily activities. Surgeons have embraced these techniques due to their potential benefits, and advancements in medical devices and surgical skills. As a result, healthcare institutions are investing in training their medical teams and acquiring the necessary equipment to meet the increasing demand for minimally invasive endoscopy surgeries, thereby providing patients with improved treatment options and enhanced overall healthcare experiences.

Market Research Highlights

- Global market for Endoscopy Device was valued at US$ 44.20 Billion in 2024

- Annual market size is expected to reach US$ 66.46 Billion by 2031

- Total addressable market (TAM) during 2025-2031 is projected to reach approximately US$ 393.27 Billion

- Market is anticipated to register a CAGR of 6% during the forecast period

- The United States represents a key market, supported by Increasing demand for minimally invasive diagnostic procedures, Advancements in endoscopy technologies for improved patient outcomes, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Increased adoption of minimally invasive diagnostic procedures creating opportunities for innovative endoscopy devices, Technological advancements in endoscopy offering market expansion potential are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Boston Scientific Corp, Medtronic Plc, Stryker Corp, Johnson & Johnson, Karl Storz SE & Co KG, Olympus Corp, Ambu AS, Conmed Corp, B Braun SE, PENTAX Medical, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Endoscopy Device Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Report Segmentation and Scope:

The “endoscopy device market” is segmented on the basis of product, application, and end user.Based on product, the market is segmented into endoscopes, visualization systems, accessories, and other endoscopy devices. The market for the endoscopes segment is further subsegmented into flexible endoscopes, rigid endoscopes, robot-assisted endoscopes, and capsule endoscopes. The endoscopy device market for the visualization systems segment is further segregated into wireless displays and monitors, light sources, video processors, endoscopic cameras, video recorders, video converters, carts, transmitters and receivers, camera heads, and other instruments. The market for the other endoscopy devices segment is further segmented as electronic instruments and mechanical instruments. The market for the accessories segment is subsegmented into cleaning brushes, overtubes, surgical dissectors, light cables, fluid flushing devices, needle holders/needle forceps, mouthpieces, biopsy valves, and others. By application, the endoscopy device market is segmented into gastroscopy, laparoscopy, arthroscopy, otoscopy, urology endoscopy, bronchoscopy, laryngoscopy, and other applications. The market, based on end user, is segmented into hospitals, ambulatory surgical centers, and others.

Segmental Analysis:

By product, the endoscopes segment held the largest share of the endoscopy device market in 2022. The visualization systemssegment is estimated to register the highest CAGR during 2022–2030. Visualization systems used in endoscopy procedures help in obtaining images and videos of enhanced quality. The visualization system in endoscopy procedures consists of components such as wireless displaysand monitors, light sources, video processors, endoscopic cameras, video recorders, video converters, carts, transmitters and receivers, camera heads, and other instruments. Boston Scientific Corporation and KARL STORZ SE & Co. KG provide visualization systems in the endoscope devices market.

In terms of application, the gastroscopy segment held the largest share of the endoscopy device market in 2022. Further, the laparoscopy segment is expected to record the highest CAGR during 2022–2030.Gastroscopy (also known as upper endoscopy) involves examining the upper gastrointestinal tract, which includes the esophagus, stomach, and duodenum (the beginning part of the small intestine). It is used to diagnose conditions such as ulcers, tumors, inflammation, and gastroesophageal reflux disease (GERD). Endoscopy devices designed for gastroscopy include flexible endoscopes with advanced imaging capabilities provided by high-definition cameras and optical enhancements.

Based on end user, the hospitals segment held the largest share of the endoscopy device market in 2022. It is further expected to register the highest CAGR in the market during 2022–2030. Hospitals encompass a wide spectrum of medical facilities, ranging from community hospitals to large academic medical centers. They serve as major end users of endoscopy devices. The demand for endoscopy devices within hospital settings is mainly driven by a high footfall of patients into these facilities, which can be attributed to factors such as comprehensive care delivery, inpatient and outpatient services, and advanced procedures and interventions. Hospitals are equipped to perform complex endoscopic procedures, including surgeries, advanced imaging, and specialized therapeutic endoscopy. Endoscopes are also used to examine the interior of hollow organs or cavities inside the body. A few endoscopic examinations are particularly performed in hospital settings. For instance, cystoscopies are typically performed in hospital outpatient settings. Ureteroscopy procedures for managing or removing kidney stones are performed in operating rooms. Similarly, most ENT endoscopies, such as examining a patient’s nose or throat to assess breathing problems or swallowing difficulties, are performed in inpatient and outpatient hospital settings.

Regional Analysis:

Based on geography, the endoscopy device market is segmented into Asia Pacific, Europe, the Middle East & Africa, North America, and South & Central America. In 2022, North America held the largest share of the global market. Asia Pacific is anticipated to register the highest CAGR in the endoscopy device market during 2022–2030.

The endoscopy device market in North America is split into the US, Canada, and Mexico. The US is the largest market for endoscopy device in this region. The market is majorly driven by the surging preference for minimally invasive surgeries and increasing prevalence of cancer. Other factors such as the introduction of advanced equipment in healthcare, a higher number of hospitals, and the implementation of strategic government policies also aid in promoting the expansion of the endoscopy device market. Additionally, the need for automated systems due to the increasing patient population and crunch of healthcare resources are expected to fuel the adoption of endoscopy systems in the US. Emphasis on using technologically advanced endoscopy devices equipped with high-definition cameras and light sources is also prominently expected to fuel the market growth during the estimated period.

Endoscopy Device Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 44.20 Billion |

| Market Size by 2031 | US$ 66.46 Billion |

| Global CAGR (2025 - 2031) | 6.0% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Product

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Endoscopy Device Market Players Density: Understanding Its Impact on Business Dynamics

The Endoscopy Device Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Industry Developments and Future Opportunities:

Various initiatives taken by key players operating in the endoscopy device market are listed below:

- In February 2023, Boston Scientific Corp announced that the FDA has approved its LithoVue Elite Single-Use Digital Flexible Ureteroscope System. It is the first ureteroscope system can monitor intrarenal pressure in real-time during ureteroscopy procedures. The LithoVue Elite Single-Use Digital Flexible Ureteroscope System comprises of StoneSmart Connect Console that has upgraded the device to offer upgraded image quality, control features, and streamlined integration.

- In September 2023, Ambu expanded its gastroenterology portfolio with the announcement of the Ambu aScope Gastro Large and Ambu aBox 2, two new larger-sized gastroscopy solutions that will be available in Europe. In addition to being the first gastroscope in the world with a 4.2 mm operating channel, which enables gastroenterologists to achieve strong suction performance during procedures in the ICU and endoscopy unit, the Ambu aScope Gastro Large is also the first endoscope ever manufactured of bioplastic materials.

- In September 2022, Medtronic plc announced that the US Food and Drug Administration has approved the Nexpowder endoscopic hemostasis system. The hemostasis system is supplied worldwide by Medtronic and is separately developed by NEXTBIOMEDICAL CO., LTD (Korea). Using a catheter with patented powder-coating technology, a noncontact, nonthermal, and nontraumatic hemostatic powder is sprayed to operate the Nexpowder system

- In September 2023, Stryker Corp announced the launch of the 1788 platform, which is the next generation of minimally invasive surgical cameras. The camera platform is enhanced with upgraded technology to be used in advanced surgery across multiple specialties. The camera provides a vibrant image with balanced lighting that improves visualization of blood flow and critical anatomy and can visualize multiple optical imaging agents.

Competitive Landscape and Key Companies:

Boston Scientific Corp, Medtronic Plc, Stryker Corp, Johnson & Johnson, Karl Storz SE & Co KG, Olympus Corp, Ambu AS, Conmed Corp, B Braun SE, and PENTAX Medical are among the prominent companies operating in the endoscopy device market. These companies focus on new technologies, existing products advancements, and geographic expansions to meet the globally growing consumer demand.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends