Glioma Treatment Market Key Players and Forecast by 2030

Coverage: By Disease (Astrocytoma, Oligoastrocytoma, and Oligodendroglioma), Treatment Type (Surgery, Chemotherapy, Radiation Therapy, and Others), Grade (Low Grade and High Grade), End User (Hospital & Clinics and Ambulatory Surgical Center), and Geography

- Status : Published

- Report Code : TIPRE00029993

- Category : Life Sciences

- No. of Pages : 182

- Available Report Formats :

- Last update date : June 13, 2024

2022 Market Size

US$ 4.14 Bn

Base year value

2030 Forecast

US$ 8.29 Bn

Projected by 2030

CAGR 2023-2030

9.1 %

Growth rate

Addressable Market

US$ 49.99 Bn

(2023-2030)

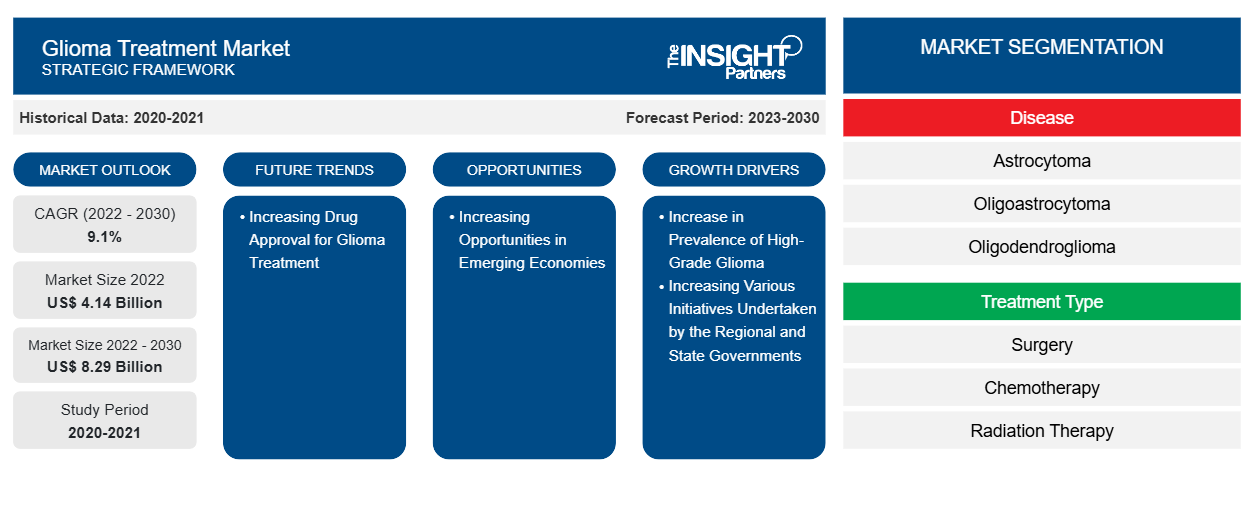

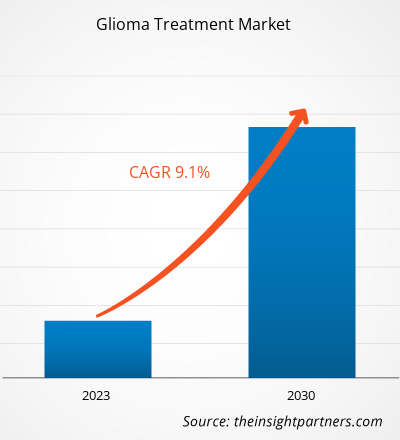

[Research Report] The glioma treatment market revenue was valued at US$ 4,139.0 million in 2022 and the glioma treatment market size are projected to reach US$ 8,291.3 million by 2030. It is expected to register a CAGR of 9.1% during 2022–2030.

Market Insights and Analyst View:

Glioma is a condition that covers a broad spectrum of brain and spinal cord tumors that concern the glial cells in the brain function and can be fatal depending on the location and severity of the tumor. Astrocytoma, brainstem gliomas, ependymoma, mixed gliomas, oligodendrogliomas, and optic pathway gliomas are the various types of gliomas. Common glioma symptoms include headache, nausea, vomiting, confusion, and a decline in brain function. Glioma can be treated in a variety of ways which include radiation therapy for glioma, chemotherapy, glioma-targeted therapy, and surgery. Effective treatment of glioma may be available from late clinical pipeline drugs.

Growth Drivers and Opportunities:

Initiatives by Regional and State Governments to Provide Patients Access to Treatment

In December 2021, the Patient Access Network (PAN) Foundation and the American Brain Tumor Association announced a new partnership to support persons with glioblastoma by offering financial assistance for services worth up to US$ 1,600 per year for patients. Moreover, leading companies in the glioma treatment market focus on launching new products and developing existing ones. In December 2020, CNS Pharmaceuticals, Inc. announced the authorization of the use of berubicin by the Food and Medication Administration to treat patients with glioblastoma multiforme. In addition, the Food and Medication Administration designated LP-184 by Lantern Pharma Inc. as an orphan medication in August 2021 for treating glioblastoma multiforme and other malignant gliomas. A webinar on glioblastoma multiforme (GBM) and the potential of Lantern Pharma's LP-184 for treating GBM and other types of brain cancer was also held in May 2020. Thus, efforts made by regional and state governments to provide patients access to novel treatments accelerate the glioma treatment market growth.

Advancements in Healthcare Sector in Emerging Economies

Brazil, Russia, India, China, and South Africa (BRICS) are among the fastest-growing economies in the world. The healthcare sectors in these countries, as well as other developing economies, are projected to expand rapidly in the coming years. The expected growth is ascribed to changes in customer demand, an increase in awareness about healthcare services, and a continuous rise in the aging population. The global brain cancer diagnostics market is likely to grow significantly in the coming years with the proliferation of the healthcare sector. Further, increased government spending on healthcare facilities and consumer purchasing power contribute to the growth of the healthcare sector in developing countries.

Asian countries are witnessing continuous growth in their scientific capabilities, owing to the ongoing clinical research studies, centralized healthcare institutions, well-qualified and highly motivated workforces, and excellent clinical trial facilities. Further, many countries in Asia Pacific have a large and diverse patient pool, with ~60% of the global population residing in the region. Treatment guidelines prepared by regulatory bodies in the US and EU are followed in Asia Pacific for treating diseases, which offers solid prospects for significant and rapid patient recruitment. Thus, the growing healthcare sector in developing countries in Asia Pacific creates better opportunities for the glioma treatment market players to expand their business.

Market Research Highlights

- North America dominated the market with 52.7% share in 2022.

- Asia Pacific is poised to grow at a CAGR of 9.3% over the forecast period.

- United States market is projected to grow at a CAGR of 9.2% over the forecast period.

- By Diseases, the Astrocytoma segment accounted for the largest market share of 71.7% in 2022.

- By Treatment Type, the Surgery segment is anticipated to witness the fastest growth, registering a CAGR of 9.7% over the forecast period

- By Grade, the High Grade segment accounted for the largest market share of 79.5% in 2022.

- By Low Grade, the Grade II segment is anticipated to witness the fastest growth, registering a CAGR of 7.7% over the forecast period

- By High Grade, the Grade IV segment accounted for the largest market share of 65.3% in 2022.

- By End Users, the Hospital segment is anticipated to witness the fastest growth, registering a CAGR of 9.2% over the forecast period

- The report profiles key industry players such as F. Hoffmann-La Roche Ltd, Pfizer Inc, Merck & Co Inc, Amneal Pharmaceuticals Inc, Teva Pharmaceutical Industries Ltd, Biocon Ltd, Amgen Inc, Sun Pharmaceutical Industries Ltd, Karyopharm Therapeutics Inc, Arbor Pharmaceuticals LLC, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Glioma Treatment Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Report Segmentation and Scope:

The “Global Glioma Treatment Market” is segmented into disease, treatment type, grade, end user, and geography. Based on disease, the glioma treatment market is segmented into astrocytoma, oligoastrocytoma, and oligodendroglioma. Based on treatment type, the glioma treatment market is segmented into surgery, chemotherapy, radiation therapy, and others. The global glioma treatment market, by grade, is bifurcated into low grade and high grade. In 2022, the high grade segment held a larger share of the market. The glioma treatment market, by end user, is bifurcated into hospital & clinics and ambulatory surgical centers. Geographically, the glioma treatment market is segmented into North America (the US, Canada, and Mexico), Europe (Germany, France, Italy, the UK, Russia, and Rest of Europe), Asia Pacific (Australia, China, Japan, India, South Korea, and Rest of Asia Pacific), Middle East & Africa (South Africa, Saudi Arabia, the UAE, and Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and Rest of South & Central America).

Segmental Analysis:

Based on disease, the glioma treatment market is segmented into astrocytoma, oligoastrocytoma, and oligodendroglioma. In 2022, the astrocytoma segment held the largest share of the market and is estimated to record at a significant CAGR of 9.4% during 2022–2030. Astrocytomas, also called malignant gliomas, are often developed in the brain’s cerebral hemispheres. Anaplastic astrocytoma is a type of rare malignant brain tumor. Astrocytomas tumors develop from astrocytes, star-shaped brain cells. Astrocytes and similar cells are called glial cells, and the tissue they form is called glial tissue, which is developed in the brain or spinal cord. Tumors that arise from glial tissues include astrocytomas are referred to as gliomas. The symptoms of anaplastic astrocytomas vary depending on the tumor site and size. The line of treatment for anaplastic astrocytoma is maximal surgical removal, followed by a radiation therapy. The line of treatment may include a combination of neurosurgery, radiation therapy, or chemotherapy.

Avid Bioservices, Inc.; Merck Sharp & Dohme Corp.; Mylan N.V, Novartis AG; and F. Hoffmann-La Roche Ltd. are among the noteworthy players offering products that are used in glioma treatment. An upsurge in activities to raise public awareness of this condition and its treatment, coupled with the increasing prevalence of this disease, are among the major factors fueling the glioma treatment market growth. In addition, companies operating in the market for the anaplastic astrocytoma segment may derive growth opportunities from growing R&D efforts and new, untapped market segments.

Based on treatment type, the glioma treatment market is segmented into surgery, chemotherapy, radiation therapy, and others. The other treatments include targeted drug therapy, electric and magnetic fields, and combination therapies. In 2022, the surgery segment held the largest share of the glioma treatment market. It is further estimated to register a significant CAGR of 9.7% during 2022–2030. Surgery is the most preferred technique as it removes the tumor completely. Computed tomography (CT) scan and magnetic resonance imaging (MRI) help neurosurgeons to locate and precisely remove the tumor of the brain or spinal cord. Surgeons perform craniotomy surgical procedures by opening the skull to reach the tumor site. Surgical procedures provide the ability to reduce the amount of solid tumor tissue within the brain; remove the cells located in the center of a tumor, which may be resistant to radiation and/or chemotherapy; and reduce intracranial pressure. By providing a debulking of tumors, surgical procedures can prolong the lives of some patients and improve the quality of remaining life.

The global glioma treatment market, by grade, is bifurcated into low grade and high grade. In 2022, the high grade segment held a larger share of the market. It is further estimated to record a significant CAGR of 9.4% during 2022–2030. High-grade gliomas are graded as a 3 or 4, indicating they are more aggressive and grow more rapidly into the brain or spinal cord, which makes their diagnosis and treatment difficult. High-grade gliomas may not be curable. Surgery, radiation, and targeted therapies can slow tumor growth and help ease symptoms. As there are no curative treatments for most types of high-grade glioma, many people are encouraged to participate in a clinical trial. Multiple research studies are underway to gain better understanding of high-grade tumors to develop more effective treatments or therapies. High-grade gliomas are the second most common type of malignant (cancerous) brain tumor in children.

The glioma treatment market, by end user, is bifurcated into hospital & clinics and ambulatory surgical centers. In 2022, the hospital & clinics segment held a larger share of the market and is estimated to register a significant CAGR of 9.2% during 2022–2030. Hospitals and clinics serve as primary healthcare centers by employing qualified medical and healthcare personnel to offer convenient services and the best care to patients. Glioma treatment offered by a majority of hospitals is covered under insurance policies, which encourages patients to receive treatments in hospitals. Also, post-operative care is offered in the best possible manner to prevent further complications. As all the services are offered under one roof, hospitals are largely preferred across the world. Moreover, the availability of multiple hospitals in the countries allows patients to choose from different options for their treatments. Exposure to global trends, increasing disposable incomes, and hassle-free reimbursement processes are among the common factors that are resulting in the increasing number of visits to hospitals by brain cancer patients, followed by an upsurge in the number of brain cancer procedures being performed. Infrastructure available in hospitals can be utilized to provide high-quality care for various brain cancer cases as they have access to advanced medical devices. The hospitals segment is estimated to hold a considerable share in the glioma treatment market as the majority of patients in emerging and developed countries prefer approaching hospitals to get treated for health-related problems. Further, the increasing number of hospitals, adoption of advanced diagnostic platforms, and growing accessibility of hospitals in developing nations would offer lucrative opportunities for the growth of the glioma treatment market for the hospitals segment during 2022–2030.

Regional Analysis:

Geographically, the glioma treatment market is segmented into North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America. The glioma treatment market in Europe is segmented into France, Germany, Italy, Spain, the UK, and the Rest of Europe. The region holds the second-largest share of the global market, which can be attributed to the increasing number of brain tumor cases, technological advancements in brain tumor treatments in France, the increasing prevalence of neurological disorders in the UK, and surging healthcare investments in Germany. The healthcare sector in the UK has access to well-developed advanced medical technologies and devices. According to the United Kingdom National Health Service, more than 11,000 people are diagnosed with brain tumors in the UK each year, of which nearly 50% of tumors are cancerous. As per the Globocan 2020 data, the UK recorded about 7,697 new cases of brain and central nervous system cancer. As a result of the burgeoning incidence, several private and government organizations are investing in cancer research. As per the written evidence related to brain tumor and childhood cancer research from Cancer Research UK (BCCR0001), released in April 2021, Cancer Research UK has committed US$ 35.45 million since 2018 to encourage brain tumor research through funding calls for brain tumor research and launching centers of excellence and a radiation research network. The center invested US$ 15.20 million in brain tumor research, and US$ 11.12 million in cancer research affecting children and adolescents in 2019–2020 to become one of the largest research funders in the field of brain tumors across the UK.

Europe has a well-developed healthcare system that offers world-class diagnosis and treatment services for various medical conditions. Besides, the development in infrastructure is expected to raise the demand for technologically advanced medical practices in hospitals. The country in European Union spends nearly 10.9% of its GDP on the healthcare system. Therefore, the rise in healthcare developments is likely to benefit the glioma treatment market growth in Europe during 2022–2030. The region has high per capita income and advanced healthcare infrastructure, which translates into demand for a broad range of cutting-edge medical treatments and diagnoses.

Russia, Poland, Austria, Switzerland, Sweden, Norway, Denmark, Belgium, and the Netherlands are among the major countries in the Rest of Europe. The increasing number of cancer cases leading to the demand for glioma treatment and the growing number of hospitals using new technologically advanced healthcare facilities are likely to pose significant growth opportunities for the glioma treatment market in the Rest of Europe. Population growth, economic prosperity, a rise in the number of cigarette smokers (a risk factor for brain cancer), and a surge in demand for faster diagnosis along with improvements in diagnostics devices are among the key factors driving the glioma treatment market in the Rest of Europe.

Industry Developments and Future Opportunities:

Various initiatives taken by key players operating in the global glioma treatment market are listed below:

- In July 2023, F. Hoffmann-La Roche developed RG-6156, which is under clinical development and currently in Phase I for Glioblastoma Multiforme (GBM). EGFRvIII x CD3 (RG6156) is a T cell bispecific antibody that binds to EGFRvIII on tumor cells and CD3 on T cells. EGFRvIII is an activating EGFR mutation leading to increased tumorigenicity and is expressed in around 30% of glioblastoma (GBM).

- In October 2022, Amneal launched first biosimilar with ALYMSYS (bevacizumab-maly) in the US. ALYMSYS (bevacizumab-maly) in the US is a vascular endothelial growth factor inhibitor indicated for the treatment of recurrent glioblastoma in adults along with other cancer treatment.

- In August 2021, Azurity Pharmaceuticals acquired Arbor Pharmaceuticals. The combined company, operating as Azurity, will have a portfolio of products serving the unmet needs of patients in the cardiovascular, central nervous system, endocrinological, gastrointestinal, and institutional markets.

Glioma Treatment Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 4.14 Billion |

| Market Size by 2030 | US$ 8.29 Billion |

| Global CAGR (2022 - 2030) | 9.1% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By Disease

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Glioma Treatment Market Players Density: Understanding Its Impact on Business Dynamics

The Glioma Treatment Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

COVID-19 Impact:

During the pre-COVID scenario, continuous research and development activities were carried out for the effective treatment of glioma including surgical resection followed by radio chemotherapy and chemotherapy for patients’ higher survival rate. Major players in the market with funding from the National Institute of Health were focusing on various growth strategies; for instance, R&D in nanotechnology for the options for glioma treatment. These activities were delayed for certain period, as the focus of treatment changed after the COVID-19 outbreak.

The COVID-19 pandemic disrupted healthcare systems, leading to concerns about its subsequent impact on non-COVID disease conditions. Cancer diagnosis and treatment are time-sensitive and are likely to be significantly affected by these conditions. The activities of each cancer discipline have been adversely affected by the COVID-19 pandemic. In addition, childhood malignant brain tumors are characterized by rapid growth and require early diagnosis and appropriate treatment. Therefore, delaying or modifying treatment can compromise its effectiveness and reduce patient survival. Due to the fear and pressure of SARS CoV2 infection, changes in the decision-making process of children with brain tumors may have a negative impact on their final outcome to certain extent.

Competitive Landscape and Key Companies:

Some of the prominent players operating in the global glioma treatment market are F. Hoffmann-La Roche Ltd; Arbor Pharmaceuticals, LLC; Merck and Co., Inc.; Sun Pharmaceutical Industries Ltd; Amgen Inc.; Teva Pharmaceutical Industries Ltd.; Pfizer Inc.; Amneal Pharmaceuticals, LLC; Karyopharm Therapeutics, Inc.; and Bristol Mayers Squibb Company. These companies focus on new product launches and geographical expansions to meet the growing consumer demand worldwide and increase their product range in specialty portfolios. They have a widespread global presence, which provides them to serve a large set of customers and subsequently increases their market share. The report offers trend analysis of the glioma treatment market outlook emphasizing various parameters such as technological advancements, market dynamics, and competitive landscape analysis of leading market players across the globe.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends