Industrial Valve Market Size, Share & Trends by 2034

Coverage: By Type (Ball Valves, Butterfly Valves, Safety Valves, Control Valves, Check Valves, Plug Valves, and Others), Size (Upto 5 Inches, 6–5 Inches,16–24 Inches, and Above 25 Inches), Class (150, 300, 400, 600, 800, 900,1500, and 2500), and Industry (Oil and Gas, LNG, Water Treatment, Power and Energy, Chemical and Petrochemical, and Others)

- Status : Published

- Report Code : TIPMC00002517

- Category : Manufacturing and Construction

- No. of Pages : 310

- Available Report Formats :

- Last update date : April 17, 2026

2025 Market Size

US$ 69.24 Bn

Base year value

2034 Forecast

US$ 101.14 Bn

Projected by 2034

CAGR 2025-2034

4.3 %

Growth rate

Addressable Market

US$ 773.72 Bn

(2025-2034)

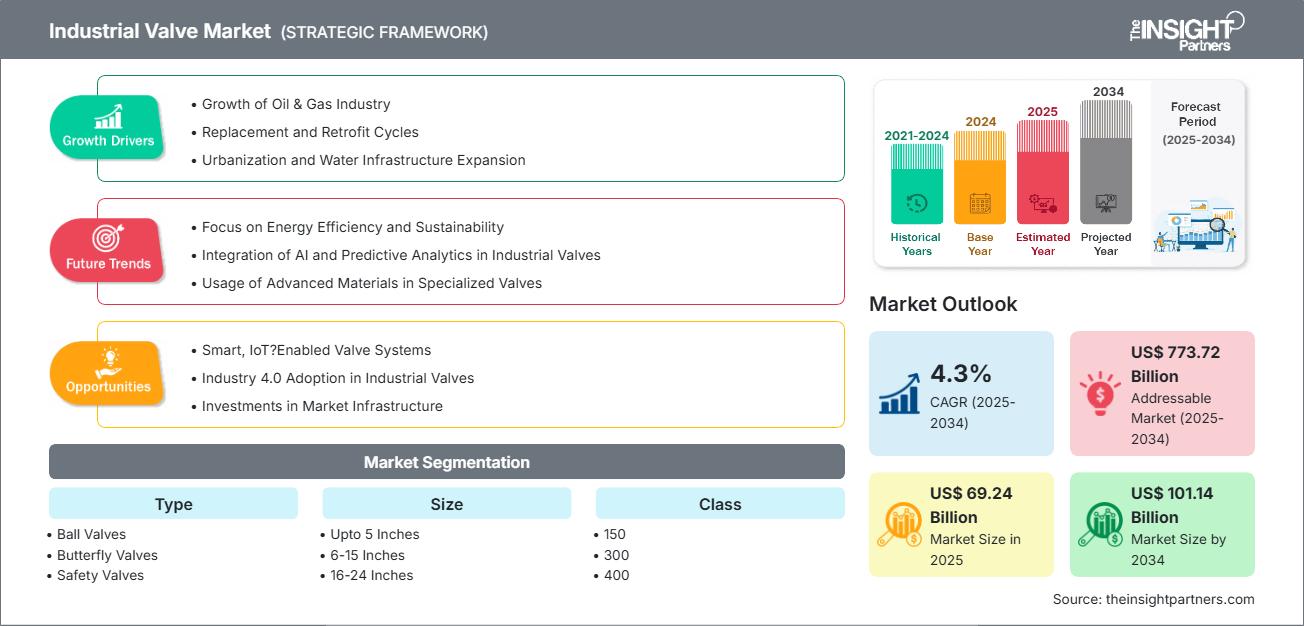

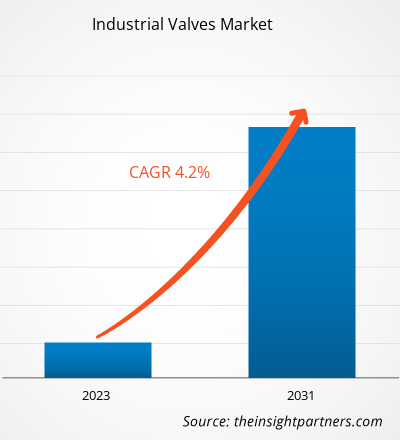

The industrial valve market size is projected to reach US$ 101.14 billion by 2034, from US$ 69.24 billion in 2025. The market is expected to register a CAGR of 4.3% during 2026–2034.

Industrial Valve Market Analysis

The market is driven by factors such as growing industrialization, infrastructure expansion, adoption of automation and Industry 4.0 technologies, rising energy efficiency and sustainability standards, and replacement of aging infrastructure. Increasing demand from emerging markets, coupled with investments in advanced and high-performance valve solutions, is further fueling market growth.

Industrial Valve Market Overview

The industrial valve market consists of the design, manufacturing, and distribution of valves used to control, regulate, and direct the flow of fluids, gases, and slurries across a variety of industry sectors. The valve is a critical component in industrial systems for safe, efficient and reliable operation. Ball valves, gate valves, globe valves, butterfly valves, check valves and control valves are some of the popular types of valves. Each type of valve has unique characteristics that can be optimized for specific flow control operations, pressures, and temperatures.

The value of industrial valves arises from their ability to maintain system integrity, to help prevent leaks, to help regulate pressure in the processes, and to enable efficient process operations. Valves are extremely versatile and are used extensively in the oil and gas, petrochemicals, power generation, water and wastewater management, chemicals, pharmaceuticals and food and beverage processing sectors. In these industries, valves play a major role in ensuring operational safety, maintaining product quality, and complying with environmental regulatory standards.

Market Research Highlights

- Asia Pacific dominated the market with 40.1% share in 2025.

- Asia Pacific is poised to grow at a CAGR of 4.9% over the forecast period.

- United States market is projected to grow at a CAGR of 4.1% over the forecast period.

- By Type, the Control Valves segment accounted for the largest market share of 26.4% in 2025.

- By Size, the 6-15 Inches segment is anticipated to witness the fastest growth, registering a CAGR of 5% over the forecast period

- By Class, the 150 segment accounted for the largest market share of 29.5% in 2025.

- By Industry, the Water Treatment segment is anticipated to witness the fastest growth, registering a CAGR of 5.8% over the forecast period

- The report profiles key industry players such as Emerson Electric Co, SLB Limited, Spirax Group plc, Circor International Inc, Flowserve Corp, Velan Inc, The Weir Group PLC, Crane Co, Neway Valve (Suzhou) Co.,Ltd, KITZ Corporation, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Industrial Valve Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Industrial Valve Market Drivers and Opportunities

Market Drivers:

- Growth of Oil & Gas Industry: Industrial valves play a crucial role in regulating, directing, and controlling the flow of liquids and gases across different stages of energy production and distribution.

- Replacement and Retrofit Cycles: Valves experience wear and tear, corrosion, and performance degradation, which can compromise safety, efficiency, and compliance with modern standards. As a result, industries are increasingly investing in replacements to maintain operational reliability.

- Urbanization and Water Infrastructure Expansion: As cities grow and populations increase, there is a corresponding need for reliable water supply, wastewater management, and sewage systems.

- Automation and Process Efficiency Needs: Industrial automation trends are increasing the adoption of actuated and smart ball valves to improve operational efficiency and reduce manual intervention.

- Stringent Environmental and Safety Regulations: Governments mandate emission control and leakage prevention, pushing industries to adopt advanced, high-integrity valve systems.

Market Opportunities:

- Smart and IoT‑Enabled Valve Systems: Smart valves integrate advanced sensors, machine learning, and connectivity to provide precise control over flow, pressure, and resource distribution.

- Industry 4.0 Adoption in Industrial Valves: The incorporation of intelligent systems, sensors, and advanced data analytics through Industry 4.0 enables manufacturers to optimize production processes, improve product quality, and reduce the risk of human error.

- Investments in Market Infrastructure: Emerging markets—particularly in Asia Pacific—present substantial opportunities for the industrial valve market due to large-scale capital investment in infrastructure projects.

- Pipeline Modernization and Infrastructure Upgrades: Aging infrastructure replacement and new pipeline installations create steady long-term demand.

- Customization and Application-Specific Solutions: Increasing demand for tailored valves for niche industries (semiconductors, specialty chemicals) offers high-margin opportunities.

Industrial Valve Market Report Segmentation Analysis

The industrial valve market is segmented into distinct categories to provide a detailed understanding of its type, size, class, and industry specifications:

By Type:

- Ball Valve: Ball valves are widely used in industrial applications due to their simple design, reliability, and strong sealing performance.

- Butterfly Valve: Butterfly valves are quarter-turn valves known for their compact design, lightweight structure, and cost efficiency. They are commonly used in water distribution, wastewater treatment, HVAC systems, and certain chemical processing operations.

- Safety Valves: Safety valves are critical components designed to protect equipment, systems, and personnel by automatically releasing excess pressure. These valves are widely used in industries such as oil and gas, power generation, chemicals, and manufacturing, where pressure buildup can lead to hazardous situations.

- Control Valves: Control valves are used to regulate flow, pressure, temperature, and fluid levels within industrial processes. They play a crucial role in automation systems by responding to signals from controllers to adjust process conditions in real time.

- Check Valves: Check valves are non-return valves designed to allow fluid flow in one direction while preventing backflow. They operate automatically without the need for manual intervention, using pressure differences to open and close.

- Plug Valves: Plug valves are quarter-turn valves that use a cylindrical or tapered plug to control fluid flow. They are known for their simple design, quick operation, and ability to provide tight shutoff.

- Others: The “Others” segment in the industrial valve market includes a variety of specialized valves such as gate valves, diaphragm valves, needle valves, and pinch valves. These valves are designed to meet specific application requirements that may not be fully addressed by mainstream valve types.

By Size:

- Upto 5 Inches

- 6-15 Inches

- 16-24 Inches

- Above 25 Inches

By Class:

- 150

- 300

- 400

- 600

- 800

- 900

- 1500

- 2500

By Industry:

- Oil and Gas

- LNG

- Water Treatment

- Power and Energy

- Chemical and Petrochemical

- Others

By Geography:

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Industrial Valve Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 69.24 Billion |

| Market Size by 2034 | US$ 101.14 Billion |

| Global CAGR (2025 - 2034) | 4.3% |

| Historical Data | 2021-2024 |

| Forecast period | 2025-2034 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Industrial Valve Market Players Density: Understanding Its Impact on Business Dynamics

The Industrial Valve Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Industrial Valve Market Share Analysis by Geography

Asia Pacific—a key automotive manufacturing hub—is witnessing the fastest market growth. Emerging markets in Latin America, the Middle East, and Africa offer numerous untapped opportunities for industrial valve providers.

The industrial valve market experiences varying growth rates across different regions. Below is a summary of market share and trends by region:

1. North America

- Strong investments in oil and gas infrastructure, shale exploration, and pipeline modernization drive industrial valve demand. Increasing adoption of automation, smart valves, and strict environmental regulations further accelerate market growth.

- Growing focus on water and wastewater treatment upgrades, alongside aging infrastructure replacement, boosts valve adoption. Digitalization trends, including IIoT-enabled monitoring systems, enhance efficiency, safety, and predictive maintenance across industries.

2. Europe

- Stringent environmental regulations and decarbonization goals are driving the adoption of advanced valves in renewable energy, hydrogen projects, and emission control systems, particularly across chemical, power generation, and industrial processing sectors.

- The expansion of energy transition initiatives, including offshore wind and green hydrogen, drives demand. An emphasis on high-quality engineering standards and lifecycle efficiency is promoting the adoption of smart, corrosion-resistant, and energy-efficient valve technologies.

3. Asia Pacific

- Rapid industrialization, urbanization, and infrastructure development in countries such as China and India drive large-scale demand for industrial valves across power, water treatment, oil and gas, and manufacturing sectors.

- Rising investments in smart factories and automation technologies boost the adoption of intelligent valves. Additionally, increasing environmental awareness and regulatory tightening support growth in wastewater management and clean energy applications.

4. South and Central America

- Expansion of oil and gas exploration activities, particularly offshore developments, drives valve demand. Mining sector growth contributes significantly, requiring robust valves for handling abrasive and high-pressure environments.

- Improving infrastructure in water treatment and energy sectors supports adoption. Increasing foreign investments and gradual industrial modernization encourage uptake of automated and efficient valve systems across emerging economies.

5. Middle East and Africa

- Dominance of oil and gas sector, including upstream and downstream expansions, remains the primary driver. Mega projects in refining, petrochemicals, and pipelines significantly increase demand for durable, high-performance industrial valves.

- Growing investments in desalination plants and water infrastructure due to water scarcity boost valve adoption. Diversification efforts into renewable energy and industrial sectors further create new opportunities for advanced valve technologies.

High Market Density and Competition

Competition is strong due to the presence of established players such as Emerson Electric Co (US), Flowserve Corp (US), and SLB Limited (US). Regional and niche providers such as Crane Co (US) and KITZ Corporation (Japan) also add to the competitive landscape across different regions.

A highly competitive environment drives companies to offer unique products and services, including:

- Vertical integration and scale

- Technological partnership

- Geographic footprint

Opportunities and Strategic Moves

- Consolidation through mergers and acquisitions

- Investments in automation

- Diversifying into high-growth verticals

- Sustainability and eco-friendly solutions

Major Companies operating in the Industrial Valve Market are:

- Emerson Electric Co (US)

- Flowserve Corp (US)

- SLB Limited (US)

- Crane Co (US)

- KITZ Corporation (Japan)

- Velan Inc (Canada)

- Spirax Group plc (UK)

- The Weir Group PLC (Scotland)

- Circor International Inc (US)

- Neway Valve (Suzhou) Co.,Ltd (China)

Other companies analyzed during the course of research:

- KSB SE & Co. KGaA

- AVK Holdings

- The Lee Company

- RED-WHITE VALVE CORP.

- Alsco Industrial Products

- JLX VALVE

- Curtiss-Wright

- LUMACO SANITARY VALVES

- IPEX Group of Companies

- Xylem, Inc.

- Motion Industries, Inc.

- Schenck Process Holding GmbH

- Alfa Laval Inc.

- EBARA Technologies, Inc.

- Pentair

- Stäubli International AG

- Barnes Group Inc.

- TRIVACO Tristate Valves & Controls, Inc

- Bi-Torq Valve Automation

- PARKER HANNIFIN CORP

Disclaimer: The companies listed above are not ranked in any particular order.

Industrial Valve Market News and Recent Developments

- Crane Fluid Systems Supports the Redevelopment of 7 Millbank in London: In December 2025, Crane Fluid Systems supported the redevelopment of 7 Millbank in London, supplying Skanska UK with a comprehensive range of valves and engineered solutions for the project.

- Emerson Introduces the Anderson Greenwood Type 84 Pressure Relief Valve (PRV): In Febraury 2025, Emerson Electric Co introduced the Anderson Greenwood Type 84 Pressure Relief Valve (PRV), specially designed to protect tanks and vessels used in hydrogen and other high-pressure gas applications. With Arlon 3000XT thermoplastic seating and ASME SA-479 Type S21800 stainless steel spindle material, the Type 84 PRV delivers exceptional leaktight performance, resistance to embrittlement, optimum seat tightness, high reliability, and long service life.

Industrial Valve Market Report Coverage and Deliverables

The "Industrial Valve Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering below areas:

- Industrial valve market size and forecast at global, regional, and country levels for all the segments covered under the scope

- Industrial valve market trends, as well as dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Industrial valve market analysis covering key trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the industrial valve market

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends