Lithium-ion Battery Dispersant Market Growth, Demand & Size by 2034

Lithium-ion Battery Dispersant Market Size and Forecasts (2021–2034), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage : by Dispersant Type (Block Copolymers, Naphthalene Sulfonates, Lignosulfonates); End-Use (Consumer Electronics, Electric Vehicles, Military, Industrial); and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00040478

- Category : Chemicals and Materials

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 15, 2026

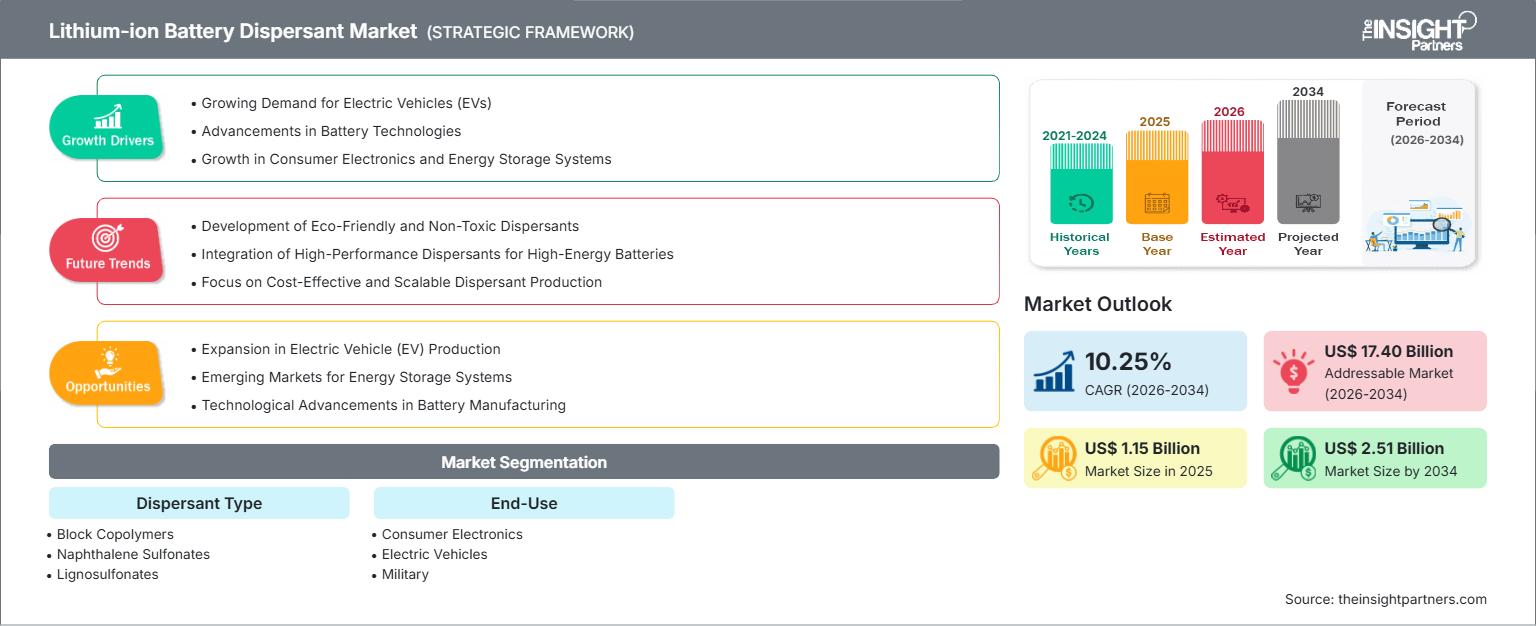

2025 Market Size

US$ 1.15 Bn

Base year value

2034 Forecast

US$ 2.51 Bn

Projected by 2034

CAGR 2026-2034

10.25 %

Growth rate

Addressable Market

US$ 17.40 Bn

(2026-2034)

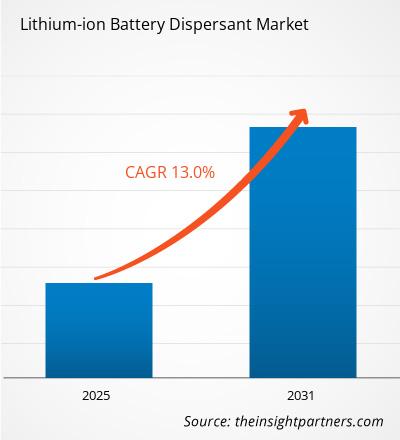

The lithium-ion battery dispersant market was valued at US$ 1.15 Billion in 2025 and is projected to reach US$ 2.51 Billion by 2034, registering a CAGR of 10.25% during 2026–2034. The industry benefits from an increase in global lithium-ion battery production, continuous innovations in electrode formulation technology, and investment in high-performing battery materials. Dispersant demand continues to grow due to improvements that battery producers look for such as slurry stability, increased conductivity, and higher efficiencies during the production process.

Investment in battery gigafactories, localization of supply chain of critical materials, and clean energy policy across North America will drive industrial growth. The lithium-ion battery dispersant market size in the region is expected to expand at a CAGR of 9.5–10.5% during the forecast period, supported by increasing electric vehicle production, stationary energy storage deployment, and sustained research into advanced electrode chemistries requiring highly efficient dispersant formulations.

Lithium-ion Battery Dispersant Market Assessment and Insights

- North America: Accounted for 29–33% share in 2025 and is expected to register a CAGR of 9.5–10.5% during 2026–2034, supported by rapid battery manufacturing expansion, government incentives, and localization of advanced battery material supply chains.

- US: Represented 74–78% of the North American market in 2025 and is projected to grow at a CAGR of 9.7–10.7% during 2026–2034, driven by domestic battery cell production, electric vehicle investments, and industrial-scale energy storage projects.

- Europe: Held 24–28% share in 2025 and is anticipated to grow at a CAGR of 9.3–10.3% during 2026–2034, with Germany, France, and the UK leading investments in sustainable battery manufacturing and localized supply chains.

- Asia Pacific: Accounted for 39–43% share in 2025 and is forecast to register the highest regional CAGR of 10.8–11.8% during 2026–2034, led by China, Japan, South Korea, and India through expanding battery production capacities.

- Largest Segment: Consumer Electronics accounted for 41–45% market share in 2025 and is expected to grow at a CAGR of 9.4–10.4% during 2026–2034, supported by continuous demand for smartphones, laptops, tablets, and wearable electronics.

- High Growth Segment: Electric Vehicles represented 30–34% market share in 2025 and is projected to register a CAGR of 11.4–12.4% during 2026–2034, owing to accelerating EV adoption and large-scale battery manufacturing investments.

- Key companies analyzed in detail: Ashland Inc., LG Chem Ltd., Huntsman Corporation, Evonik Industries AG, Kao Corporation, Borregaard ASA, The Lubrizol Corporation, Cargill, Incorporated, Artience Co., Ltd., and Toyo Ink SC Holdings Co., Ltd.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

Due to the increased demands on battery performance, dispersants have evolved from being mere process aids to becoming key functional ingredients in the production of lithium-ion batteries. Advances in slurry technology, accuracy in electrode coating, conductive additives, and binders have greatly improved the efficiency of the production process. There is more focus on dispersants that can keep particles stable with minimal changes in viscosity. These evolving production requirements continue to reshape the lithium-ion battery dispersant market growth across both established and emerging battery manufacturing hubs.

For the future, growth in capacity in Asia Pacific, North America, and Europe is anticipated to improve global supply chain stability, as well as providing specialty chemicals companies with business opportunities. Efforts in regulation that support the domestic manufacturing of batteries, sustainable material development efforts, and ongoing research into silicon anode and high nickel cathode chemistries will help drive innovation. In the race for high energy density and high throughput production, sophisticated dispersant chemistries will continue to gain importance.

Lithium-ion Battery Dispersant Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 1.15 Billion |

| Market Size by 2034 | US$ 2.51 Billion |

| Global CAGR (2026 - 2034) | 10.25% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Lithium-ion Battery Dispersant Market Analysis

The fast development of electrification in the transportation sector, consumer electronics, renewable energy, and industry drives the need for innovative battery materials. Advanced lithium-ion cells need to have highly stable electrode slurries to achieve proper coating, improved conductivity, and longevity of operation. As a result, specialized dispersants are needed to enhance the efficiency of the manufacturing process and minimize material losses. The expansion of the lithium-ion battery dispersant market is fueled by growing investments in battery gigafactories, popularity of high energy density chemistries, and higher requirements to electrode materials.

Battery manufacturing ecosystems have significantly developed in recent years. Manufacturers of chemicals cooperate with cathode material providers, producers of binders and conductive additives, cell producers, and scientific institutions in order to develop new slurries for next generation batteries. Advances in automation and quality control during the manufacturing process drive the need for dispersants that can provide uniform distribution of particles.

Key trends influencing the competitive structure of the lithium-ion battery dispersant market analysis comprise extensive R&D spending on innovative specialty chemicals, eco-friendly products, and manufacturing in different regions. Leading companies like Evonik Industries AG, Ashland Inc., Huntsman Corporation, LG Chem Ltd., Kao Corporation, Borregaard ASA, The Lubrizol Corporation, Artience Co., Ltd., Toyo Ink SC Holdings Co., Ltd., and Cargill, Incorporated are working towards augmenting their product lines with advanced formulation technology tailored to meet increasingly complex demands of battery manufacturing.

A rising trend in collaboration between battery manufacturers and specialty chemical producers has been observed, as companies require custom dispersants for new electrode materials. A considerable rise in spending on eco-friendly water-based formulations, efficient dispersion, and consistent processes has opened up new business opportunities along the value chain. Companies that provide specialized performance and technical expertise as well as regional presence are likely to gain competitive advantage due to fast-growing battery production worldwide.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Lithium-ion Battery Dispersant Market: Strategic Insights

Regional Insights

North America Lithium-Ion Battery Dispersant Market

North America accounted for 29–33% of the lithium-ion battery dispersant market share in 2025 and is projected to register a CAGR of 9.5–10.5% during 2026–2034. The regional market will be driven by large investments in battery manufacturing plants, domestic battery chain development through government incentives, and electric vehicles manufacturing. Due to the US Inflation Reduction Act and clean energy projects, battery materials localization is happening rapidly, and there will be a continual demand for quality dispersants in making electrodes.

This regional market will be reinforced by partnerships between specialty chemicals companies, battery cell manufacturers, research institutes, and automotive OEMs. The growing use of stationary battery energy storage systems and research on silicon-based anodes and nickel-based cathodes need quality dispersants that offer particle stability and ease of processability. These structural developments will help the region expand continuously during the forecast period.

U.S. Lithium-Ion Battery Dispersant Market

In 2025, the US occupied 74–78% share of the North American market and is projected to grow at a CAGR of 9.7–10.7% from 2026 to 2034. Growth in capacity of lithium-ion battery manufacturing plants, increasing use of electric vehicles, and supportive policies for localization of the battery supply chain further boost demand in the market. Major players are developing innovative technologies for the manufacture of batteries that need uniform slurry, which drives the usage of specialty dispersants.

The nation also houses some of the largest specialty chemical manufacturers and an active innovation environment consisting of universities, national laboratories, and battery developers. Commercial production of lithium-ion cells for cars, buses, consumer electronics, and stationary energy storage devices drives the demand for innovative materials used in the fabrication of batteries. Further investments in recycling of batteries and development of new battery technologies will drive future growth in the market.

Europe Lithium-Ion Battery Dispersant Market

Europe held a share of 24-28% of the total global market in 2025 and is projected to exhibit a CAGR of 9.3-10.3% in the 2026-2034 period. Germany continues to dominate the region owing to its strong presence in automotive manufacturing industry, substantial investment in battery cells, and strong knowledge of chemical industry. Growth in Europe's battery manufacturing continues to drive higher consumption of advanced dispersants to enhance the consistency and efficiency in electrode production.

The UK is enhancing its battery research through investments made in innovation centers for batteries along with commercialization programs for electric mobility and energy storage. France, Italy, and Spain are expanding battery manufacturing within their respective countries along with promoting sustainable battery materials manufacturing in their countries through industrial policies.

APAC Lithium-Ion Battery Dispersant Market

Asia Pacific accounted for 39–43% share of the global market in 2025 and is anticipated to record the highest regional CAGR of 10.8–11.8% between 2026 and 2034. China is driving regional demand due to its dominance in battery manufacturing, whereas Japan and South Korea continue to be major centers for the development of battery technologies.

India and Australia are driving regional growth with their battery manufacturing policies and initiatives related to the mining of minerals and electric vehicles ecosystem. Continuous investments along the battery value chain and growing exports of lithium-ion batteries will further drive the dominance of Asia Pacific during the forecast period.

Middle East & Africa Lithium-Ion Battery Dispersant Market

The Middle East & Africa market is projected to expand at a CAGR of 8.2–9.2% during 2026–2034. Saudi Arabia and the United Arab Emirates are investing in electric mobility, renewable energy storage, and industrial diversification strategies that encourage battery manufacturing and advanced materials development.

For South Africa, the strategic significance lies in the country’s mining industry and involvement in battery minerals supply chain, while in the Rest of the Middle East & Africa, there has been an increase in renewable energy infrastructure spending. With the increasing battery assembly in the selected countries, it is expected that demand for specialty dispersants will continue to rise in future.

Segmentation Analysis

Dispersant Type

The Dispersant Type segment is projected to register a CAGR of 10.1–11.1% during 2026–2034. Product innovation is increasingly focused on improving slurry homogeneity, reducing agglomeration, and enhancing electrode coating quality for high-energy-density batteries. The lithium-ion battery dispersant market scope continues to broaden as manufacturers develop formulations compatible with water-based processing, silicon-rich anodes, and advanced cathode materials while supporting higher production efficiency and longer battery service life.

- Block Copolymers: Widely adopted because of their excellent steric stabilization, compatibility with conductive additives, and ability to maintain consistent slurry viscosity during high-volume electrode manufacturing for advanced lithium-ion batteries.

- Naphthalene Sulfonates: Preferred for cost-effective dispersion performance in large-scale battery manufacturing, offering improved particle distribution, enhanced processing stability, and reliable coating uniformity across various electrode formulations.

- Lignosulfonates: Bio-based dispersants gaining attention due to their renewable origin, lower environmental impact, and compatibility with sustainable battery manufacturing practices while supporting effective particle stabilization during slurry preparation.

End-Use

The End-Use segment is anticipated to expand at a CAGR of 10.4–11.4% during 2026–2034. Expanding battery demand across transportation, electronics, defense, and industrial equipment continues to diversify dispersant consumption. Manufacturers increasingly customize formulations according to battery chemistry, production processes, and application-specific performance requirements, ensuring improved electrode consistency, enhanced electrochemical efficiency, and optimized manufacturing productivity.

- Consumer Electronics: Continues to represent the largest application base due to sustained production of smartphones, laptops, tablets, wearable devices, and portable electronics requiring reliable lithium-ion batteries with consistent performance characteristics.

- Electric Vehicles: Rapid electrification of passenger and commercial transportation significantly increases demand for advanced dispersants capable of supporting high-capacity battery cells, faster manufacturing processes, and improved cycle life.

- Military: Growing adoption of lightweight, high-energy rechargeable batteries for defense electronics, communication equipment, surveillance systems, and autonomous platforms creates opportunities for premium-performance dispersant formulations.

- Industrial: Expanding deployment of batteries in material handling equipment, backup power systems, robotics, renewable energy storage, and automated manufacturing supports increasing consumption of specialty battery processing materials.

Opportunity Snapshot

| End-Use | Revenue Contribution | Trend Tag | Adoption Stage |

| Consumer Electronics | High | Portable Devices | Mature |

| Electric Vehicles | High | Fast Charging | Scaling |

| Military | Low | Mission Power | Emerging |

| Industrial | Medium | Grid Storage | Scaling |

Lithium-ion Battery Dispersant Market Growth Drivers and Impact Analysis

Expansion of Global Electric Vehicle Battery Manufacturing

Investments around the world in battery production for electric vehicles are constantly on the rise, as governments set tighter emission standards for cars and auto companies work on expanding their electric strategies. The development of gigafactories in Asia Pacific, Europe, and North America causes an increase in the demand for sophisticated dispersants that can provide better slurry stability, coating quality, and manufacturing efficiency. Current battery technology demands careful dispersion of conductive materials and active ingredients in order to create batteries with higher energy and longevity. In order to manufacture batteries efficiently in large quantities with consistently high quality, dispersants become absolutely indispensable.

Advancements in High-Energy-Density Battery Chemistries

The shift towards cathode materials with high nickel content and anodes made of silicon, as well as advancements in lithium-ion battery chemistry, leads to the increased need for customized dispersants. High-end electrode materials possess more complicated features in terms of processibility, hence necessitating excellent stability of particles and optimal rheology of slurry composition. Companies are now looking for dispersants that can help maintain a stable dispersion under increasingly harsh conditions of production and offer better electrochemical performance. Such trends make it possible for battery manufacturers to increase their battery cycle life and enhance efficiency of charging.

Growing Adoption of Sustainable Battery Manufacturing Practices

The manufacture of batteries is gradually becoming more environmentally friendly to meet the needs of emerging sustainability targets and guidelines. Processes that utilize aqueous electrode processing, environmentally-friendly manufacturing technologies, and sustainable resources are driving the development of environmentally friendly dispersants based on biomass. Chemical companies have been developing products that enable them to decrease solvent usage but retain high processing efficiency and excellent quality electrodes. With the rise of the importance of sustainability as a purchasing criterion in the battery supply chain, such companies will have a competitive advantage in the market.

Lithium-ion Battery Dispersant Market Future Trends

Increasing Adoption of Water-Based Electrode Processing

The growing lithium ion battery dispersant market trends have become indicative of the shift within the industry toward a water based electrode production process that not only reduces the environmental footprint but increases safety in the work environment. The specialty chemical companies are producing dispersants that are specially formulated for water based processing, which will allow for uniform distribution of particles and consistent slurry viscosity in addition to large scale production.

Integration of Artificial Intelligence into Battery Manufacturing

It is anticipated that innovations in artificial intelligence, process monitoring, and digital manufacturing technologies will bring about changes in the manufacturing of batteries in the next few years. Companies are increasingly using predictive analytics in order to ensure consistency of the slurry and improve the quality in the production processes. It is anticipated that suppliers of dispersants will increasingly work with battery manufacturers to formulate products suitable for digitally driven manufacturing processes.

Lithium-ion Battery Dispersant Market Opportunities

Emerging Battery Manufacturing Investments in Developing Economies

Expansion of manufacturing investments in battery manufacturing in India, Southeast Asia, Eastern Europe, and certain Middle Eastern countries offers substantial opportunities for specialty chemical providers for future growth. Incentives from governments, increase in the production of electric vehicles, and localization of battery manufacturing drive construction of new manufacturing plants which will require highly effective dispersing additives. Lithium-ion battery dispersants Market Forecast suggests that companies that build their manufacturing capacities, establish technical centers, and develop joint R&D programs will have an opportunity to serve rapidly developing battery industries and develop stable client base.

Development of Customized Specialty Dispersant Solutions

The increasing diversity of battery chemistry provides chances for companies that have the capacity to provide extremely tailored formulations for dispersants. More and more battery makers are looking for dispersants that are designed especially for silicon anode batteries, lithium iron phosphate batteries, high-nickel cathodes, and solid-state battery technology. Companies that focus on formulating and developing products in collaboration with their customers can stand out due to improved performance and increased customer interaction.

Recent Developments

- April 2026: H.I.G. Capital (“H.I.G.”), a global alternative investment firm with $74 billion of capital under management, completed the acquisition of Inventus Power (“Inventus” or the “Company”), a global provider of advanced battery and power systems.

- February 2026: Aqua Metals, Inc. (NASDAQ: AQMS), a pioneer in clean metals recycling and refining, and American Battery Factory (ABF), a lithium iron phosphate (LFP) battery cell manufacturer, announced a proposed strategic collaboration focused on advancing a more competitive, domestic battery materials supply chain through recycling and circular manufacturing.

- January 2026: Chinese battery giant CATL and EV maker NIO signed a five-year strategic cooperation agreement to develop battery technology, swapping network resources and global market share. On the technology front, the companies will focus on jointly developing batteries that have long cycle life, as well as battery swapping technologies.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends