Military Special Vehicles Market Size, Trends & Demand by 2034

Coverage: By Application (Ground Support Handling, Tactical Warfare, ISR, Military Transportation, and Others), Technology (Autonomous Vehicles and Manual Driven Vehicles), and Geography

- Status : Published

- Report Code : TIPRE00043438

- Category : Aerospace and Defense

- No. of Pages : 223

- Available Report Formats :

- Last update date : May 28, 2026

2025 Market Size

US$ 1.54 Bn

Base year value

2034 Forecast

US$ 2.58 Bn

Projected by 2034

CAGR 2026-2034

5.9 %

Growth rate

Addressable Market

US$ 18.66 Bn

(2026-2034)

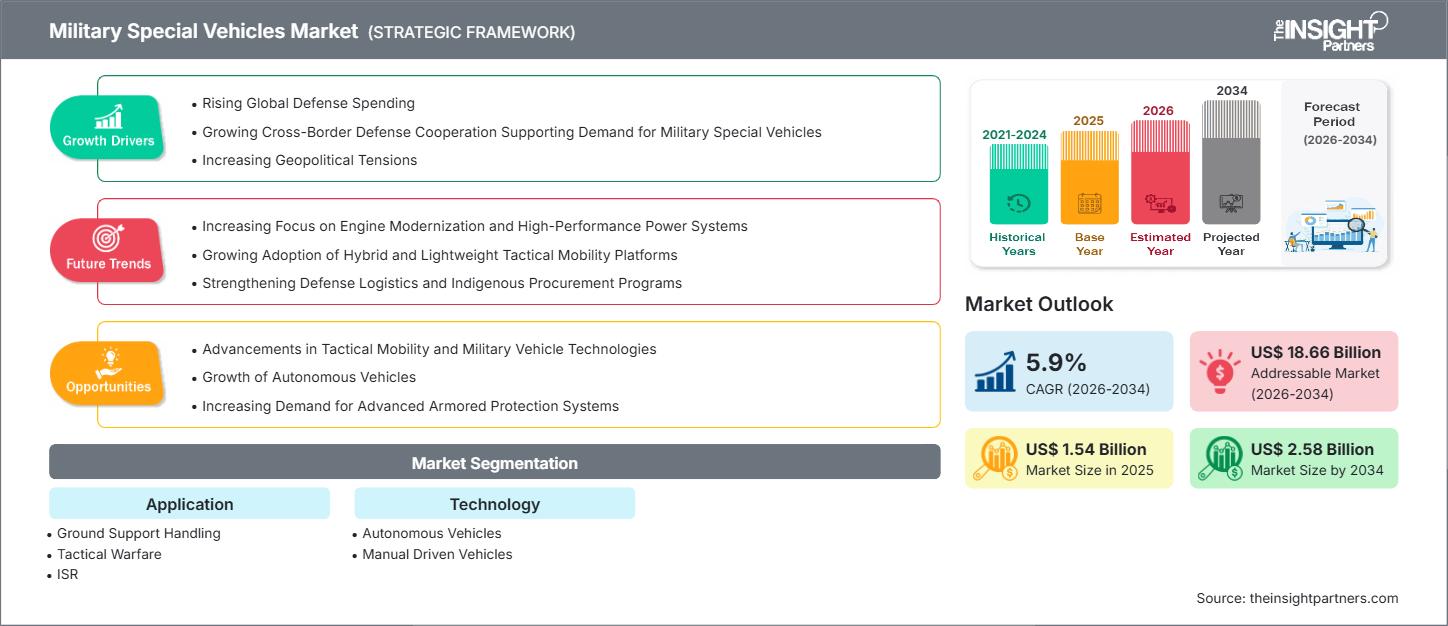

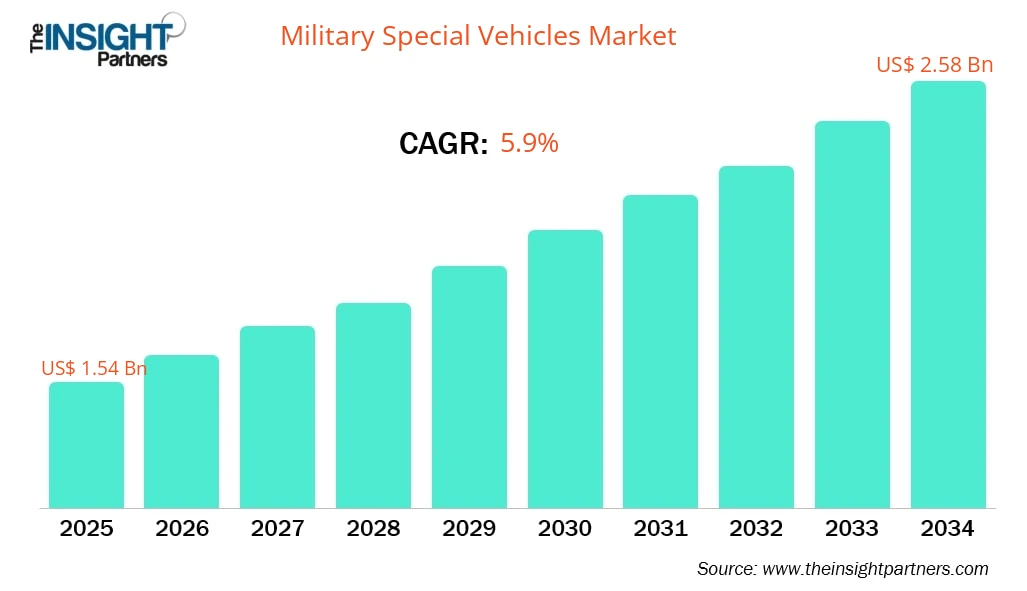

The military special vehicles market size is projected to reach US$ 2.58 billion by 2034, from US$ 1.54 billion in 2025. The market is expected to register a CAGR of 5.9% during 2026–2034.

Military Special Vehicles Market Analysis

The military special vehicles market is driven by an increase in geopolitical tensions, increased defense budgets, and an increase in modernization of land forces, coupled with a greater focus on developing multidomain warfare capability. Nations are investing large amounts of money into developing new methods to improve their mobility to improve border security, conduct internal stability operations, be ready for rapid deployment, and be able to support expeditionary operations. There has been a strong acceleration in market growth because of the increased demand for improved off-road mobility, efficient, lighter-weight composite materials, better protection, and integrated digital battlefield technology.

Because of a growing emphasis on the need for increased counter-terrorism capabilities, enhancing urban warfare readiness, and increasing assistance capabilities, global demand for military special vehicles is expected to grow significantly in the future. The market may be limited by several factors, including the high costs of acquiring and maintaining military special vehicles, the need for sophisticated engineering, and extended product development and acquisition cycles.

Military Special Vehicles Market Overview

The military special vehicle market develops, produces, and deploys highly specialized military vehicles that can operate on diverse lands and multiterrain environments. The vehicles serve many functions, including providing tactical mobility, armored combat support, reconnaissance, transporting troops, logistics support, border security, internal security operations, and disaster relief missions. Technology such as advanced mobility systems, armored protection, surveillance technologies, and communications suites is utilized to provide a wide array of capabilities to support operational effectiveness in complex environments.

The principal vehicle types produced in this market include: Armored Personnel Carriers (APCs); Infantry Fighting Vehicles (IFVs); Light Tactical Vehicles; Mine Resistant Ambush Protected (MRAP) Vehicles; Logistic and Support Vehicles; and Multi-Role Tactical Mobility Platforms. These products are used by military forces, domestic law enforcement agencies, peacekeeping units, and special operations forces to enhance their operational missions by providing flexibility, survivability, and deployment speed in a variety of terrain types. Recent advancements in technology, including autonomous mobility systems, hybrid and electric propulsion systems, AI-enabled command and control systems, and advanced battlefield network solutions, have widened the market scope.

Market Research Highlights

- North America dominated the market with 41.5% share in 2025.

- Asia Pacific is poised to grow at a CAGR of 6.9% over the forecast period.

- United States market is projected to grow at a CAGR of 6.3% over the forecast period.

- By Application, the Military Transportation segment accounted for the largest market share of 36.6% in 2025.

- By Technology, the Autonomous Vehicles segment is anticipated to witness the fastest growth, registering a CAGR of 6.8% over the forecast period

- The report profiles key industry players such as BAE Systems Plc, General Dynamics Corp, Thales SA, Lockheed Martin Corp, Rheinmetall AG, Tata Motors Ltd, Ashok Leyland Ltd, Oshkosh Corp, KMW+NEXTER Defense Systems NV, Patria Oyj, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Military Special Vehicles Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Military Special Vehicles Market Drivers and Opportunities

Market Drivers:

- Rise in Global Defense Spending: As military organizations increasingly focus on rapid deployment, multidomain operations, and defense modernization initiatives, rising defense expenditure is expected to significantly support the long-term growth of the military special vehicles market.

- Cross-Border Defense Cooperation Supporting Demand for Military Special Vehicles: Increasing cross-border defense cooperation, military assistance programs, growing international defense collaboration, and military aid initiatives are anticipated to drive long-term demand for military special vehicles globally.

- Increased Geopolitical Tensions: Geopolitical tensions such as the Russia-Ukraine conflict, Israel-Hamas conflict, territorial disputes in the South China Sea, and rising border tensions between India and China are significantly driving the demand for military special vehicles.

- Investments in Electric Battlefield Special Vehicles: Rising investments in electric battlefield special vehicles enhance operational efficiency, reduce fuel dependency, improve stealth capabilities, and accelerate military modernization initiatives globally.

- Military Modernization Programs: Military modernization programs increase demand for advanced armored vehicles, surveillance systems, and tactical transport solutions, significantly driving military special vehicles market growth.

Market Opportunities:

- Advancements in Tactical Mobility and Military Vehicle Technologies: The growing need for rapid deployment capabilities, enhanced battlefield support, and multimission operational performance is accelerating the adoption of technologically advanced military special vehicles.

- Growth of Autonomous Vehicles: Defense organizations worldwide are investing in advanced vehicle automation systems to improve operational efficiency, reduce human risk, enhance battlefield intelligence, and strengthen mission effectiveness in complex combat environments.

- Demand for Advanced Armored Protection Systems: Military special vehicles are increasingly being integrated with advanced armor systems, blast-resistant hull structures, active protection systems, electronic warfare technologies, and improved situational awareness solutions to ensure troop safety during combat operations.

- Integration of Advanced Communication Systems: Integration of advanced communication systems enhances real-time coordination, situational awareness, and mission efficiency, driving demand for technologically advanced military special vehicles globally.

- Adoption of Hybrid and Electric Propulsion: Adoption of hybrid and electric propulsion enhances fuel efficiency, reduces emissions, improves operational performance, and creates significant opportunities in the military special vehicles market.

Military Special Vehicles Market Report Segmentation Analysis

The military special vehicles market is segmented into distinct categories to provide a detailed understanding of its material type and end user:

By Application:

- Ground Support Handling: Military special vehicles used for ground support handling are designed to assist armed forces in logistics coordination, equipment movement, recovery missions, and operational support across land-based and multiterrain environments.

- Tactical Warfare: The tactical warfare segment represents a major application area for military special vehicles, primarily focused on combat operations, troop engagement, and battlefield dominance across diverse terrain environments, including deserts, mountains, forests, urban zones, and border regions.

- ISR: The ISR segment represents a critical application area for military special vehicles, focused on real-time intelligence gathering, battlefield awareness, and mission support.

- Military Transportation: The military transportation segment represents a key application area for military special vehicles, focused on the movement of troops, weapons, supplies, and mission-critical equipment across land-based and multiterrain environments.

- Others: The ‘other’ category includes vehicles that are designed to perform mission-specific roles while ensuring personnel safety, operational efficiency, and adaptability in complex and high-risk operational zones.

By Technology:

- Autonomous Vehicles

- Manual Driven Vehicles

By Geography:

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Military Special Vehicles Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 1.54 Billion |

| Market Size by 2034 | US$ 2.58 Billion |

| Global CAGR (2026 - 2034) | 5.9% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Application

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Military Special Vehicles Market Players Density: Understanding Its Impact on Business Dynamics

The Military Special Vehicles Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Military Special Vehicles Market Share Analysis by Geography

Asia Pacific is witnessing the fastest growth, driven by its expanding construction industry and demand for smart homes. Emerging markets in Latin America and the MEA offer untapped opportunities for military special vehicles providers.

The military special vehicles market experiences varying growth rates across different regions. Below is a summary of market share and trends by region:

1. North America

- The Canadian and US defense sectors are prioritizing rapid upgrades of advanced military vehicles for next-generation active and reserve units.

- The adoption of bi-directionally connected and autonomous systems, supported by autonomous navigation and AI-based surveillance technologies, is expected to accelerate military operational capabilities.

2. Europe

- As NATO continues to modify its capabilities, countries in Europe are developing multinational defense projects, which will allow them to share costs associated with quickly deploying military forces and the procurement of new vehicles.

- The OEMs in EU countries are currently building battery-powered vehicles, utilizing smart manufacturing practices, and developing multinational procurement projects that will provide sustainability and operational efficiency to their respective armed forces.

3. Asia Pacific

- Demand for advanced military special vehicles and local defense manufacturing is increasing across Asia Pacific due to geopolitical tensions, border conflicts, and rising military spending by countries such as China, India, Japan, and South Korea.

- Countries in Asia Pacific are increasing domestic defense production, adopting modular vehicle platforms, and deploying advanced tactical fleets with surveillance, communication, and mobility capabilities to strengthen long-term military self-reliance and operational preparedness.

4. South and Central America

- Internal security issues, organized crime, border monitoring requirements, and modernization of law enforcement fleets are driving gradual demand for armored patrol, transport, and tactical special-purpose vehicles, while constrained defense spending continues to act as a limiting factor.

- Governments are increasingly favoring cost-effective, rugged, multipurpose military vehicles procured through phased tender processes, with emphasis on operational durability, maintenance efficiency, and integration with domestic security and defense operations.

5. Middle East and Africa

- Regional conflict, counter-terrorism operations, border security requirements, and increasing military expenditure are driving strong demand for protected military special-purpose vehicles that can operate safely and effectively in high-risk and harsh environments.

- Defense modernization programs continue to emphasize drone-integrated operations and rugged tactical mobility platforms. Partnerships with domestic defense manufacturers are enabling regional states to enhance collective security capabilities and reduce dependence on foreign suppliers, thereby supporting market growth.

High Market Density and Competition

Competition is strong due to the presence of established players such as BAE Systems Plc (UK), Thales SA (France), and Lockheed Martin Corp (US). Regional and niche providers such as Rheinmetall AG (Germany) and General Dynamics Corp (US) add to the competitive landscape across different regions.

A highly competitive environment drives companies to offer unique products and services, including:

- Vertical integration and scale

- Technological partnerships

- Geographic footprint

Opportunities and Strategic Moves

- Consolidation through mergers and acquisitions

- Investment in automation

- Diversifying into high-growth verticals

- Sustainability and eco-friendly solutions

Major Companies operating in the Military Special Vehicles Market are:

- Ashok Leyland Ltd (India)

- BAE Systems Plc (UK)

- General Dynamics Corp (US)

- Rheinmetall AG (Germany)

- Tata Motors Ltd (India)

- Thales SA (France)

- Lockheed Martin Corp (US)

- Oshkosh Corp (US)

- Patria Oyj (Finland)

- KMW+NEXTER Defense Systems NV (Netherlands)

Other companies analyzed during the course of research:

- Arquus SAS

- Otokar Otomotiv ve Savunma Sanayi A.Ş.

- IVECO Defence Vehicles S.p.A.

- Singapore Technologies Engineering Ltd

- Navistar Defense LLC

- Mahindra Defence Systems Ltd

- NIMR Automotive LLC

- Paramount Group Ltd

- SC Group Global Ltd (Supacat brand)

- Force Protection Industries Inc.

- EXCALIBUR ARMY spol. s r.o.

- Denel Land Systems SOC Ltd

- Hyundai Rotem Company

- Hanwha Aerospace Co., Ltd.

- China North Industries Group Corporation Limited

- FNSS Savunma Sistemleri A.Ş.

- BMC Otomotiv Sanayi ve Ticaret A.Ş.

- Armoured Vehicles Nigam Limited (AVNL)

- Tatra Defence Vehicle a.s.

- John Cockerill Defense SA

- JSC Research and Production Corporation UralVagonZavod

- GAZ Group LLC

- Dongfeng Motor Corporation

- JCBL Limited

- INKAS Armored Vehicle Manufacturing Ltd.

Disclaimer: The companies listed above are not ranked in any particular order.

Military Special Vehicles Market News and Recent Developments

- Düsseldorf-based Rheinmetall AG and the Spanish Technology Group Indra sign an MoU for the Production of Military Vehicle Systems: In March 2026, Düsseldorf-based Rheinmetall AG and the Spanish technology Group Indra signed a memorandum of understanding to further deepen their strategic cooperation, particularly in the production of military vehicle systems for European and Latin American Armed Forces.

- Oshkosh Defense LLC Introduces Multi-Mission Autonomous Vehicles: In October 2025, Oshkosh Defense introduced its Family of Multi-Mission Autonomous Vehicles (FMAV) at the Association of the United States Army Annual Meeting & Exposition. The FMAV platforms demonstrated support for modernization priorities, including long-range precision fires, resilient formations, and scalable autonomy, providing production-based solutions aimed at reducing risk and enhancing capabilities for soldiers in contested environments.

Military Special Vehicles Market Report Coverage and Deliverables

The "Military Special Vehicles Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering below areas:

- Military special vehicles market size and forecast at global, regional, and country levels for all the segments covered under the scope

- Military special vehicles market trends, as well as dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Military special vehicles market analysis covering key trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the military special vehicles market

- Detailed company profiles

Frequently Asked Questions

2. Long Procurement Cycles

3. Supply Chain Disruptions

1. Autonomous Vehicles

2. Manual Driven Vehicles

1. Advancements in tactical mobility and military vehicle technologies

2. Growth of autonomous vehicles

3. Increasing demand for advanced armored protection systems

1. Ground Support Handling

2. Tactical Warfare

3. ISR

4. Military Transportation

5. Others

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends