North America Point of Care Diagnostics Market Analysis and Forecast by Size, Share, Growth, Trends 2031

Coverage: By Product (Glucose Monitoring, Infectious Disease Testing, Cardio metabolic Testing, Pregnancy and Fertility Testing, Coagulation Testing, Tumor or Cancer Marker Testing, Cholesterol Testing, Urinalysis Testing, Hematology Testing, Thyroid Testing, and Others), Glucose Monitoring (Blood Glucose Meter, Lancet, and Strips), Infectious Disease Testing (HIV Testing, Influenza Testing, Sexually Transmitted Diseases Testing, Hepatitis C Virus Testing, Tropical Diseases Testing, Respiratory Infection Testing, Hospital Acquired Infections, and Others), Cardio Metabolic Testing (Cardiac Troponin (cTn) Test, Myoglobin Test, and Others), Purchase Mode (OTC and Prescription), Sample (Blood, Urine, and Others), End User (Healthcare Facilities, Homecare, and Others), and Healthcare Facilities (Hospitals and Clinics, Diagnostic Centers, and Others)

- Status : Published

- Report Code : TIPRE00023729

- Category : Life Sciences

- No. of Pages : 180

- Available Report Formats :

- Last update date : March 24, 2026

2024 Market Size

US$ 15,289.0 Mn

Base year value

2031 Forecast

US$ 34,026.8 Mn

Projected by 2031

CAGR 2025-2031

12.2 %

Growth rate

Addressable Market

US$ 174,138.69 Mn

(2025-2031)

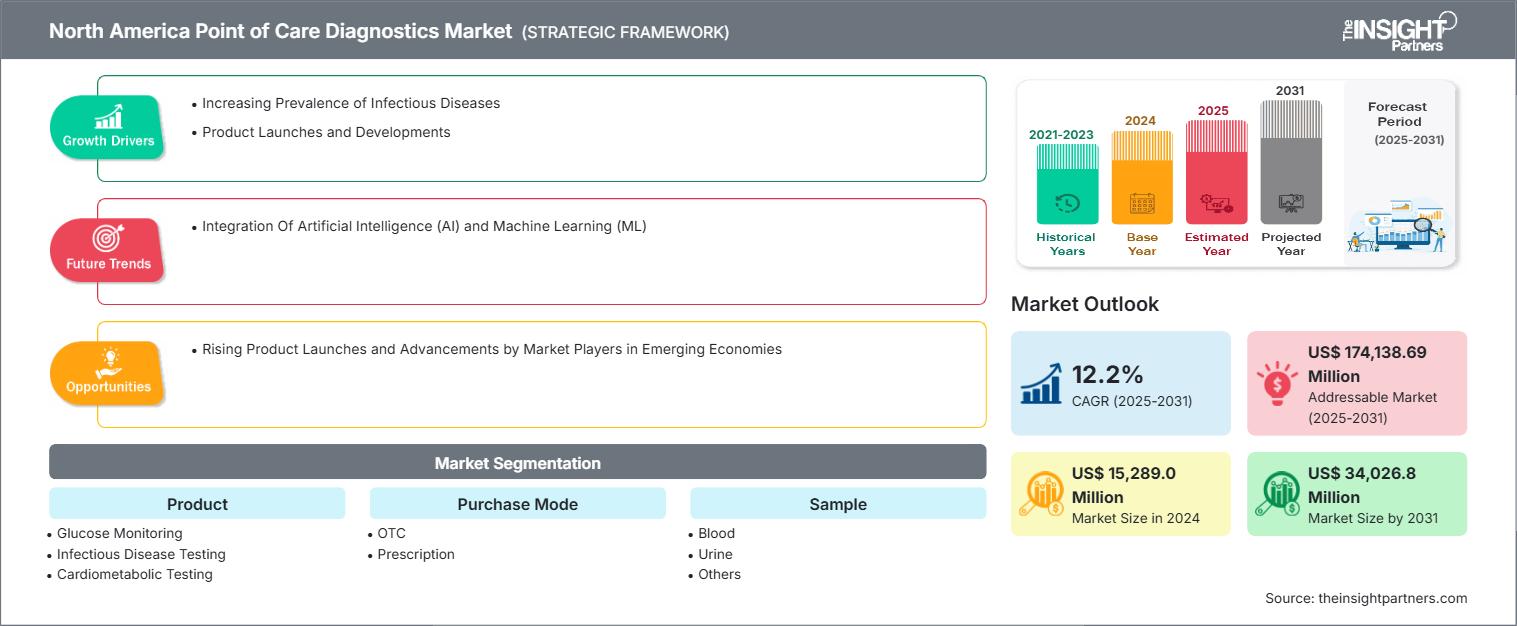

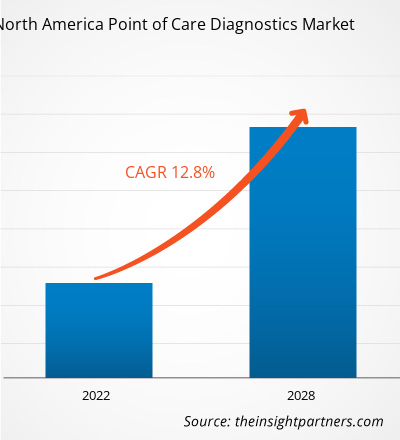

The North America Point of Care Diagnostics Market size is expected to reach US$ 34,026.8 Million by 2031 from US$ 15,289.0 Million in 2024. The market is estimated to record a CAGR of 12.2% from 2025 to 2031.

Executive Summary and North America Point of Care Diagnostics Market Analysis:

The North American POC diagnostics market is segmented into the US, Canada, and Mexico. The North American market is poised for significant growth during the forecast period due to an upsurge in the prevalence of infectious and chronic diseases, which largely calls for rapid, accurate, and easy diagnosis. Strong government support in terms of healthcare initiatives and funding for developing advanced diagnostic kits and instruments is further fueling the market's growth. Additionally, ongoing R&D by leading players results in the launch of innovative and highly effective POC testing devices. Advancing technologies, including digital health tool integrations, miniaturized biosensors, and connectivity solutions, improve the accuracy and accessibility of diagnoses. Due to a well-established infrastructure of healthcare, a high adoption rate of innovative technologies, and an established presence of companies, North America continues to hold its leading position in the POC diagnostics market globally.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

North America Point of Care Diagnostics Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

North America Point of Care Diagnostics Market Segmentation Analysis:

- By Product, the North America Point of Care Diagnostics Market is segmented into Glucose Monitoring, Infectious Disease Testing, Cardio metabolic Testing, Pregnancy and Fertility Testing, Coagulation Testing, Tumor or Cancer Marker Testing, Cholesterol Testing, Urinalysis Testing, Hematology Testing, Thyroid Testing, and Others. Glucose Monitoring held the largest share of the market in 2024.

- By Glucose Monitoring, the North America Point of Care Diagnostics Market is segmented into Blood Glucose Meter, Lancet, and Strips. Strips held the largest share of the market in 2024.

- By Infectious Disease Testing, the North America Point of Care Diagnostics Market is segmented into HIV Testing, Influenza Testing, Sexually Transmitted Diseases Testing, Hepatitis C Virus Testing, Tropical Diseases Testing, Respiratory Infection Testing, Hospital Acquired Infections, and Others. Respiratory Infection Testing held the largest share of the market in 2024.

- By Cardio Metabolic Testing, the North America Point of Care Diagnostics Market is segmented into Cardiac Troponin (cTn) Test, Myoglobin Test, and Others. Cardiac Troponin (cTn) Test held the largest share of the market in 2024.

- By Purchase Mode, the North America Point of Care Diagnostics Market is segmented into OTC and Prescription. Prescription held the largest share of the market in 2024.

- By Sample, the North America Point of Care Diagnostics Market is segmented into Blood, Urine, and Others. Blood held the largest share of the market in 2024.

- By End User, the North America Point of Care Diagnostics Market is segmented into Healthcare Facilities, Homecare, and Others. Healthcare Facilities held the largest share of the market in 2024.

- By Healthcare Facilities, the North America Point of Care Diagnostics Market is segmented into Hospitals and Clinics, Diagnostic Centers, and Others. Diagnostic Centers held the largest share of the market in 2024.

North America Point of Care Diagnostics Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 15,289.0 Million |

| Market Size by 2031 | US$ 34,026.8 Million |

| CAGR (2025 - 2031) | 12.2% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Product

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

North America Point of Care Diagnostics Market Players Density: Understanding Its Impact on Business Dynamics

The North America Point of Care Diagnostics Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

North America Point of Care Diagnostics Market Outlook

The surge in infectious diseases globally fuels demand for point-of-care diagnostics. As outbreaks spread rapidly, quick, on-the-spot testing becomes essential to control transmission. This trend drives innovation in compact, user-friendly diagnostic devices. Immediate results enable faster clinical decisions and reduce reliance on centralized labs. Ultimately, the growing disease burden accelerates the shift toward decentralized healthcare solutions. Point-of-care testing (POCT) is critical for the diagnosis, treatment, and prevention of infectious diseases. It can be used to detect major pathogens, including human immunodeficiency virus (HIV), malarial parasites, human papillomavirus (HPV), Ebola, dengue, and Zika viruses, and Mycobacterium tuberculosis (TB bacteria). According to the World Health Organization (WHO) data, 1.3 million people (including 214,000 individuals affected by HIV) succumbed to TB in 2022. Its estimates also indicate that 10.6 million individuals in the world will have TB in 2022, including 3.5 million women, 1.3 million children, and 5.8 million men. As per the WHO, HIV has infected over 39.9 million people worldwide. In 2023, people were diagnosed with HIV, out of which 1.3 million people were newly diagnosed, including 77% adults and 57% children. According to a study published by Joint United Nations Programme on HIV/AIDS (UNAIDS) in 2023, ~630,000 people died due to HIV and associated conditions. Healthcare-associated infections (HAIs), including central line-associated bloodstream infections and catheter-associated urinary tract infections (UTIs), might affect patients in hospitals and other healthcare facilities. As per the Office of Disease Prevention and Health Promotion, 1 out of 31 hospitalizations in the US suffer from HAI at any given time. The rising prevalence of infectious diseases and healthcare-associated infections is intensifying the need for rapid, accurate point-of-care diagnostics. These tools enable early detection, timely treatment, and effective disease management, reducing the strain on healthcare systems. By providing immediate results outside traditional labs, point-of-care testing enhances patient outcomes and helps curb the spread of infections. As infectious disease burdens continue to grow, the adoption of decentralized diagnostic solutions becomes increasingly vital for global health

North America Point of Care Diagnostics Market Country Insights

By country, the North America Point of Care Diagnostics Market is segmented into the United States, Canada, and Mexico. The United States held the largest share in 2024.

The growth of the US point of care diagnostics market is attributed to the rapidly increasing incidence of chronic diseases in the country. As per the National Institute of Health, an estimated 2.04 million new cases and 611,720 cancer deaths were reported in the country in 2024. Breast cancer, lung and bronchus cancer, prostate cancer, colon and rectum cancer, melanoma cancer, and liver cancer are a few common types of cancer. In addition, according to a study published by the Centers of Disease Control and Prevention in 2021, ~38.4 million people are living with diabetes, which is 11.6% of the total population. Moreover, according to the same study, a higher incidence of diabetes is observed in American youth, and the prevalence of such health conditions will ultimately boost the demand for point-of-care diagnostics in the country. Moreover, medical technologies are significantly growing, and researchers are coming up with the latest innovations. This growth resulted in the development of advanced medical devices and catalyzed developments and advancements in the healthcare industry. Moreover, the US is home to various companies developing advanced products for point of care diagnosis. For instance, in August 2021, Mylab Discovery Solutions collaborated with the US-based Hemex Health for the development of next-generation diagnostic solutions for the Point-of-Care (POC) testing of coronavirus and other diseases. Under the technology partnership, Mylab develop test assays, and Hemex will provide its Gazelle POC testing platform and expertise.

North America Point of Care Diagnostics Market Company Profiles

Some of the key players operating in the market include Siemens AG, Abbott Laboratories, F. Hoffmann-La Roche Ltd, bioMerieux SA, Bio-Rad Laboratories Inc, QIAGEN NV, Nova Biomedical Corporation, Polymer Technology Systems, Inc. (PTS), and Danaher Corp.

These players are adopting various strategies such as expansion, product innovation, and mergers and acquisitions to provide innovative products to their consumers and increase their market share.

North America Point of Care Diagnostics Market Research Methodology

The following methodology has been followed for the collection and analysis of data presented in this report:

Secondary Research

The research process begins with comprehensive secondary research, utilizing internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

- Company websites, annual reports, financial statements, broker analyses, and investor presentations

- Industry trade journals and other relevant publications

- Government documents, statistical databases, and market reports

- News articles, press releases, and webcasts specific to companies operating in the market

Note:

All financial data included in the Company Profiles section has been standardized to US$. For companies reporting in other currencies, figures have been converted to US$ using the relevant exchange rates for the corresponding year.Primary Research

The Insight Partners conducts a significant number of primary interviews each year with industry stakeholders and experts to validate its data analysis and gain valuable insights. These research interviews are designed to:

- Validate and refine findings from secondary research

- Enhance the expertise and market understanding of the analysis team

- Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects

Primary research is conducted via email interactions and telephone interviews, encompassing various markets, categories, segments, and sub-segments across different regions. Participants typically include:

- Industry stakeholders: Vice Presidents, Business Development Managers, Market Intelligence Managers, and National Sales Managers

- External experts: Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends