North America Telecom Cloud Market Analysis and Forecast by Size, Share, Growth, Trends 2031

Coverage: By Component (Solution and Services), Deployment (Public Cloud, Private Cloud, and Hybrid Cloud), Service Model (Software-as-a-Service, Infrastructure-as-a-Service, and Platform-as-a-Service), and End User (SMEs and Large Enterprises)

- Status : Published

- Report Code : TIPRE00042009

- Category : Technology, Media and Telecommunications

- No. of Pages : 195

- Available Report Formats :

- Last update date : March 11, 2026

2024 Market Size

US$ 8,689.3 Mn

Base year value

2031 Forecast

US$ 34,976.0 Mn

Projected by 2031

CAGR 2025-2031

22.1 %

Growth rate

Addressable Market

US$ 146,223.28 Mn

(2025-2031)

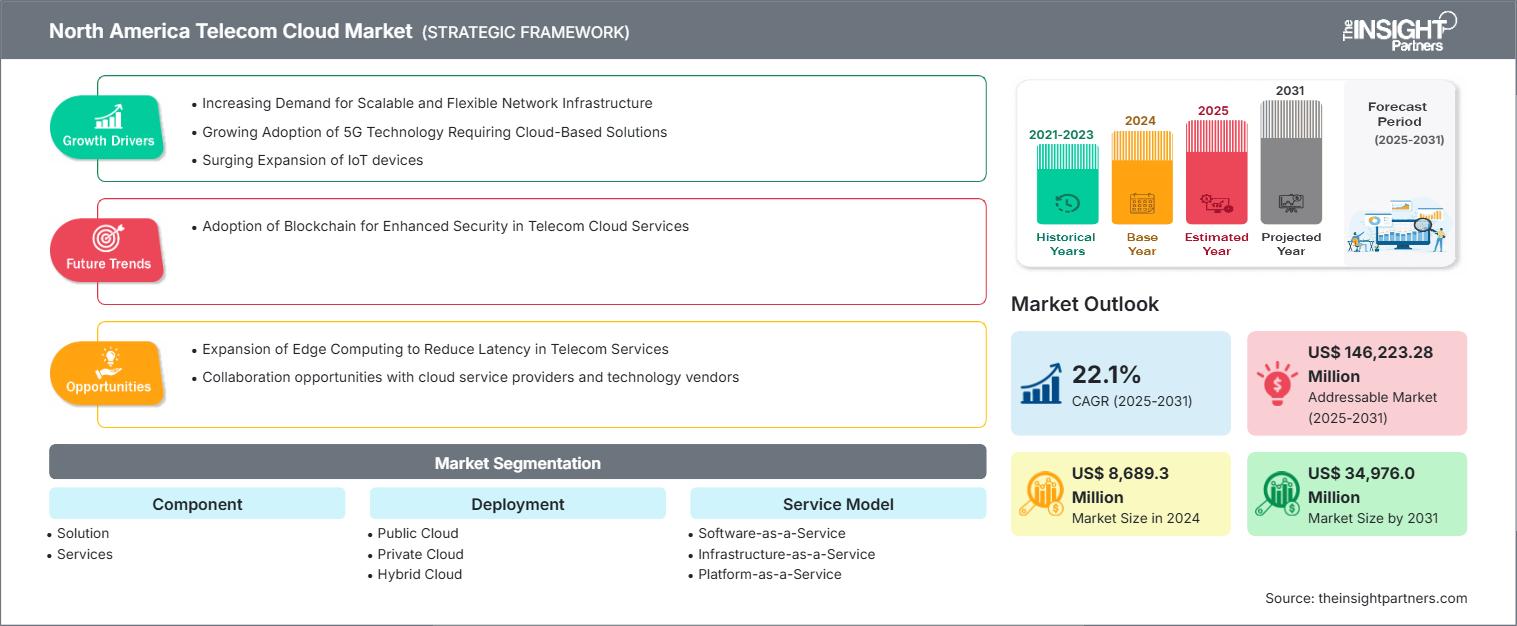

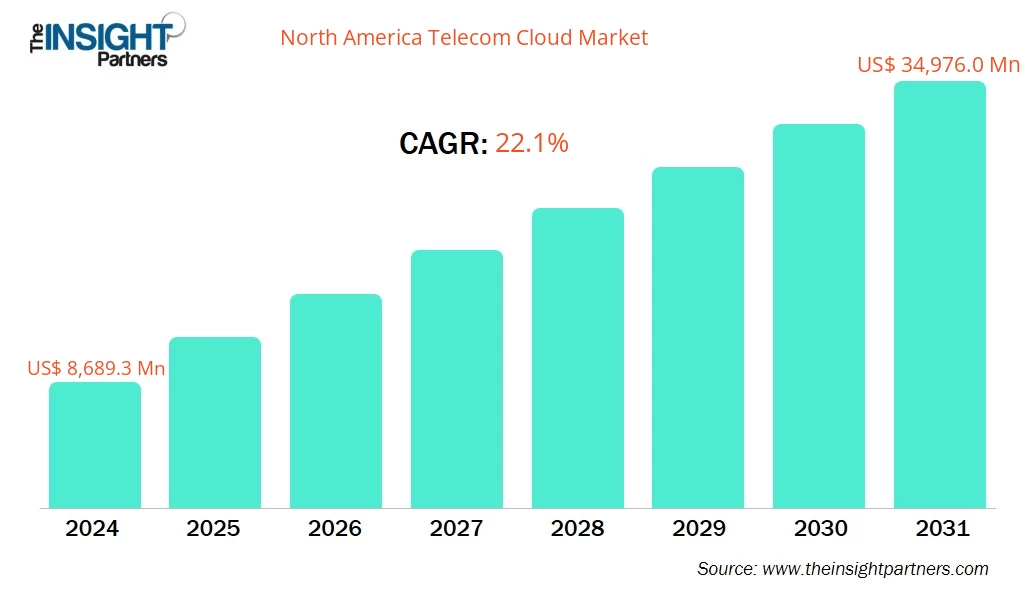

The North America Telecom Cloud Market size is expected to reach US$ 34,976.0 Million by 2031 from US$ 8,689.3 Million in 2024. The market is estimated to record a CAGR of 22.1% from 2025 to 2031.

Executive Summary and North America Telecom Cloud Market Analysis:

The North America telecom cloud market is segmented into the US, Canada, and Mexico. As mobile devices, IoT applications, and 5G deployment continue to rise, telecom operators are increasingly compelled to upgrade their networks. Cloud-based solutions provide the agility and efficiency needed to support these evolving requirements. The presence of a robust ecosystem of cloud providers and technology innovators, along with substantial investments in cloud-native network functions and edge computing, is propelling adoption. Regulatory backing for network virtualization and adherence to data sovereignty requirements further drive adoption. Regulatory oversight intensified in 2025 following AT&T's agreement to a US$177 million settlement related to data breaches that exposed the personal information of tens of millions of customers. These breaches resulted from unauthorized access to customer data hosted on Snowflake's cloud platform, causing substantial financial and reputational impact for the company.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

North America Telecom Cloud Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

North America Telecom Cloud Market Segmentation Analysis:

- By Component, the North America Telecom Cloud Market is segmented into Solution and Services. Solution held the largest share of the market in 2024.

- By Deployment, the North America Telecom Cloud Market is segmented into Public Cloud, Private Cloud, and Hybrid Cloud. Public Cloud held the largest share of the market in 2024.

- By Service Model, the North America Telecom Cloud Market is segmented into Software-as-a-Service, Infrastructure-as-a-Service, and Platform-as-a-Service. Software-as-a-Service held the largest share of the market in 2024.

- By End User, the North America Telecom Cloud Market is segmented into SMEs and Large Enterprises. Large Enterprises held the largest share of the market in 2024.

North America Telecom Cloud Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 8,689.3 Million |

| Market Size by 2031 | US$ 34,976.0 Million |

| CAGR (2025 - 2031) | 22.1% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Component

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

North America Telecom Cloud Market Players Density: Understanding Its Impact on Business Dynamics

The North America Telecom Cloud Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

North America Telecom Cloud Market Outlook

User demands are changing rapidly due to evolving technologies and increasing data consumption, as well as the proliferation of connected devices. Traditional network infrastructures, often reliant on fixed hardware, struggle to keep pace with these dynamic requirements. In contrast, cloud technology offers telecom companies scalable resources that can be adjusted on demand, allowing them to efficiently manage sudden traffic spikes and seamlessly expand services without substantial upfront hardware investments.

Scalability in cloud-based networks enables operators to dynamically allocate computing power, storage, and bandwidth as needed. This helps during high network traffic or while launching new services. This flexibility enhances network performance and reduces operational costs, as telecom providers can avoid over-provisioning and pay only for the resources they use. Moreover, cloud infrastructures facilitate faster deployment of new applications and services, enabling telecom companies to respond swiftly to market changes and customer expectations.

On May 22, 2025, Tata Consultancy Services (TCS) announced a partnership with DNA and has committed to a five-year collaboration to accelerate DNA's cloud transformation. As part of this agreement, TCS will lead the migration of up to 80% of DNA's enterprise applications to the public cloud by 2030. This move builds on a successful 17-year relationship and aims to enhance customer experience, improve operational efficiency, and achieve significant cost optimization. This partnership exemplifies how telecom companies are leveraging cloud technology to build flexible, scalable networks that can quickly adapt to changing demands. By embracing cloud migration and modernization, telecom operators stay competitive in a fast-evolving industry while delivering improved services.

Therefore, the growing shift toward scalable and flexible network infrastructure powered by cloud technology for meeting the future needs of the telecom sector drives telecom cloud market growth.

North America Telecom Cloud Market Country Insights

By country, the North America Telecom Cloud Market is segmented into the United States, Canada, and Mexico. The United States held the largest share in 2024.

In 2023, the US telecom industry continued its shift toward cloud technologies, with major players such as AT&T, Verizon, and T-Mobile investing in cloud infrastructure to enhance network agility and scalability. The adoption of Network Functions Virtualization (NFV) and Software-Defined Networking (SDN) became more prevalent, enabling telecom operators to deliver more flexible and cost-effective services. Technological innovations remain a key driver in the industry's evolution. In 2025, major players such as AWS and Microsoft revealed significant investments in AI-powered data centers. AWS committed US$11 billion toward expansion in Georgia, and Microsoft allocated US$80 billion to AI infrastructure. These investments highlight the increasing integration of cloud computing and artificial intelligence in revolutionizing telecom operations.

North America Telecom Cloud Market Company Profiles

Some of the key players operating in the market include Amazon Web Services Inc., International Business Machines Corp, Microsoft Corp, Google LLC, Verizon Communications Inc., Telefonaktiebolaget LM Ericsson, Broadcom Inc., Cisco Systems Inc., Telstra Corp. Ltd., and AT&T Inc.

These players are adopting various strategies such as expansion, product innovation, and mergers and acquisitions to provide innovative products to their consumers and increase their market share.

North America Telecom Cloud Market Research Methodology

The following methodology has been followed for the collection and analysis of data presented in this report:

Secondary Research

The research process begins with comprehensive secondary research, utilizing internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

- Company websites, annual reports, financial statements, broker analyses, and investor presentations

- Industry trade journals and other relevant publications

- Government documents, statistical databases, and market reports

- News articles, press releases, and webcasts specific to companies operating in the market

Note:

All financial data included in the Company Profiles section has been standardized to US$. For companies reporting in other currencies, figures have been converted to US$ using the relevant exchange rates for the corresponding year.Primary Research

The Insight Partners conducts a significant number of primary interviews each year with industry stakeholders and experts to validate its data analysis and gain valuable insights. These research interviews are designed to:

- Validate and refine findings from secondary research

- Enhance the expertise and market understanding of the analysis team

- Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects

Primary research is conducted via email interactions and telephone interviews, encompassing various markets, categories, segments, and sub-segments across different regions. Participants typically include:

- Industry stakeholders: Vice Presidents, Business Development Managers, Market Intelligence Managers, and National Sales Managers

- External experts: Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends