Phosphoric Acid Market Share, Growth & Demand by 2034

Coverage: by Process Type (Thermal Process, Wet Process, Others); Grade Type (Agricultural Grade, Food Grade, Industrial Grade); Application (Fertilizers, Food Additives, Animal Feed, Others) , and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00012559

- Category : Chemicals and Materials

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 08, 2026

2025 Market Size

US$ 115.98 Bn

Base year value

2034 Forecast

US$ 141.43 Bn

Projected by 2034

CAGR 2026-2034

2.51 %

Growth rate

Addressable Market

US$ 1,183.98 Bn

(2026-2034)

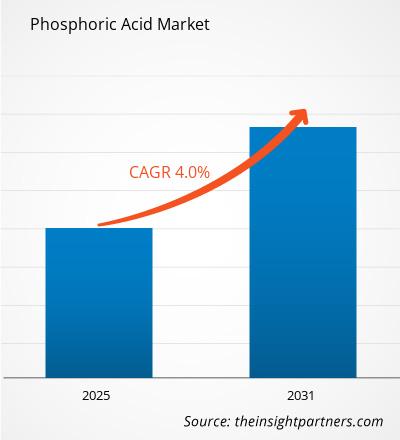

The Phosphoric Acid Market remains a fundamental component of the global phosphate value chain, supporting fertilizer production, industrial processing, food-grade applications, and advanced electronics manufacturing. The market was valued at US$ 115.98 Billion in 2025 and is projected to reach US$ 141.43 Billion by 2034, expanding at a CAGR of 2.51% during 2026–2034. Growth is closely linked to agricultural productivity requirements, phosphate-based chemical demand, and investments in downstream specialty applications.

North America represents a mature yet strategically important Phosphoric Acid market, expected to expand at an estimated CAGR of around 2.2% through 2034. Demand is supported by fertilizer consumption, water treatment investments, and food processing applications. Growing interest in battery materials, semiconductor-grade chemicals, and supply-chain localization initiatives is creating additional opportunities for high-purity phosphoric acid producers across the region.

Phosphoric Acid Market Assessment and Insights

- North America: North America accounted for 24–28% market share in 2025 and is projected to expand at a CAGR of 2.0%–2.6% during 2026–2034. Growth is driven by a strong fertilizer manufacturing base, advanced agricultural productivity, and sustained demand for phosphate-based products across the region.

- U.S.: The U.S. represented 78–82% of the North American market in 2025 and is anticipated to register a CAGR of 2.1%–2.7% during 2026–2034, supported by extensive fertilizer production, high agricultural output, and consistent consumption of phosphoric acid across industrial applications.

- Europe: Europe held 18–22% market share in 2025 and is expected to grow at a CAGR of 1.8%–2.4% during 2026–2034. Germany, France, and Spain remain the leading regional markets, supported by industrial processing activities and steady demand for phosphate-based applications.

- Asia Pacific: Asia Pacific accounted for 38–42% of the Phosphoric Acid market share in 2025 and is forecast to expand at a CAGR of 3.0%–3.6% during 2026–2034. China, India, and Japan drive regional growth through expanding agricultural production, industrial manufacturing, and increasing phosphate consumption.

- Largest Segment – Fertilizers: The fertilizers segment represented the largest market share and is expected to grow at a CAGR of 2.4%–3.0% during 2026–2034, driven by extensive demand for phosphate nutrients across commercial agriculture and crop production.

- High Growth Segment – Electronics: The electronics segment is projected to register the fastest growth with a CAGR of 4.2%–4.8% during 2026–2034, supported by expanding semiconductor manufacturing and increasing demand for high-purity phosphoric acid formulations.

- Key companies analyzed in detail: Arkema S.A.; J.R. Simplot Company; Nutrien Ltd.; OCP S.A.; PJSC PhosAgro; Prayon S.A.; Solvay SA; Spectrum Chemical Manufacturing Corp.; The Mosaic Company; Yara International ASA.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

The Phosphoric Acid Market has evolved beyond its traditional role in fertilizer manufacturing. While agriculture continues to account for the majority of demand, increasing utilization in food additives, industrial chemicals, metal treatment, water purification, and semiconductor processing has broadened the market’s revenue base. Producers are increasingly focusing on downstream integration and value-added phosphate derivatives.

Over the coming decade, industry participants are expected to emphasize operational efficiency, sustainability, and specialty product development. Investments in purified phosphoric acid, electronic-grade materials, and circular resource utilization are likely to reshape competitive positioning. Companies such as Arkema Group, Nutrien Ltd., OCP Group, PJSC PhosAgro, Prayon Group, The Mosaic Company, and Yara International continue strengthening integrated phosphate ecosystems.

Phosphoric Acid Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 115.98 Billion |

| Market Size by 2034 | US$ 141.43 Billion |

| Global CAGR (2026 - 2034) | 2.51% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Phosphoric Acid Market Analysis

Demand fundamentals remain strongly tied to global food security requirements. Phosphoric acid serves as the primary intermediate for phosphate fertilizers, making agricultural production trends a major determinant of market performance. Population growth, shrinking arable land availability, and pressure to improve crop yields continue supporting phosphate fertilizer consumption across emerging and developed economies.

The value chain begins with phosphate rock extraction and proceeds through beneficiation, sulfuric acid processing, phosphoric acid production, and downstream conversion into fertilizers and specialty phosphates. Integrated operators benefit from cost efficiencies, raw material security, and greater resilience against feedstock price volatility.

Competition is characterized by vertically integrated producers controlling phosphate reserves, processing infrastructure, and fertilizer distribution networks. OCP Group, The Mosaic Company, Nutrien Ltd., PJSC PhosAgro, and Yara International maintain strong positions through scale advantages and international supply networks. Specialty manufacturers such as Prayon Group and Spectrum Chemical Manufacturing Corporation focus on high-purity applications.

In terms of investment trends, downstream diversification is being prioritized over simple volume growth for the Phosphoric Acid market size. Investments are being made in purified phosphoric acid, electronic-grade products, sustainable technology, and efficient water usage. It becomes increasingly important to be technologically distinct and able to meet industrial needs.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Phosphoric Acid Market: Strategic Insights

Regional Insights

North America Phosphoric Acid Market

North America is expected to register a CAGR of approximately 2.2% throughout the Phosphoric Acid market forecast period. The region benefits from established fertilizer industries, advanced food processing infrastructure, and significant water treatment investments. Environmental regulations continue encouraging efficient nutrient management and the adoption of higher-quality phosphate products.

Industrial diversification is another factor contributing to the growth in demand. Expanding semiconductors production industry, investment in electronics industry’s logistics and raw materials for batteries have opened up new opportunities for companies supplying purified phosphoric acid. Regional producers remain focused on supply security, sustainability projects, and modernizing operations.

U.S. Phosphoric Acid Market

The U.S. accounts for roughly 75–80% of North American demand and is projected to grow at a CAGR near 2.1% through 2034. The country's strong agricultural sector remains the primary consumption center, while food-grade and industrial applications provide additional stability. Domestic phosphate reserves and integrated production assets support supply security.

Major industry participants, including The Mosaic Company and Nutrien Ltd., maintain substantial operational footprints. Demand for water treatment chemicals, food phosphates, and electronics-grade materials is increasing steadily. Continued investments in semiconductor manufacturing and advanced industrial production are expected to support incremental demand for high-purity phosphoric acid products over the forecast period.

Europe Phosphoric Acid Market

Europe represents approximately 18–22% of global market revenue and is anticipated to expand at a CAGR of around 2.0% through 2034. Demand is shaped by agricultural efficiency requirements, stringent environmental regulations, and growing consumption of specialty phosphates. Sustainability considerations increasingly influence production technologies and sourcing strategies.

The United Kingdom continues to demonstrate steady demand from food processing, water treatment, and industrial chemical sectors. Investment in wastewater infrastructure and food-grade phosphate applications supports market stability despite modest agricultural growth rates.

Germany, the leading European Phosphoric Acid market, benefits from its extensive industrial manufacturing base. Demand from chemicals, specialty materials, and advanced manufacturing sectors complements fertilizer consumption. The country's emphasis on industrial innovation encourages adoption of high-purity phosphate products.

France, Italy, and Spain collectively contribute significant regional consumption through agricultural activity and food production industries. Growing focus on nutrient efficiency, sustainable farming practices, and specialty chemical applications supports long-term market development across these countries.

APAC Phosphoric Acid Market

Asia Pacific accounts for approximately 40–45% of global revenue, making it the largest regional market. The region is projected to expand at a CAGR of nearly 3.0% through 2034. Agricultural intensity, population growth, industrialization, and rising food demand collectively underpin phosphoric acid consumption.

China remains the leading Phosphoric Acid market due to its substantial fertilizer industry, phosphate processing capacity, and industrial chemical production base. Government initiatives supporting agricultural productivity and industrial modernization continue influencing demand patterns.

Japan and South Korea contribute through advanced manufacturing and electronics industries, where high-purity phosphoric acid is increasingly important. Meanwhile, India benefits from rising fertilizer requirements, agricultural development programs, and investments in phosphate processing infrastructure. Australia supports regional demand through mining, agriculture, and industrial applications.

Middle East & Africa Phosphoric Acid Market

The Middle East & Africa region is anticipated to be the fastest-growing market, advancing at an estimated CAGR of 3.4% through 2034. Expansion is supported by phosphate resource availability, fertilizer production investments, and increasing agricultural modernization efforts.

Saudi Arabia leads regional growth through integrated phosphate projects and industrial diversification initiatives. Large-scale investments in mining, chemicals, and downstream fertilizer manufacturing continue strengthening the phosphoric acid ecosystem.

The UAE is expanding its role in specialty chemicals and industrial processing, while South Africa remains an important consumer due to agricultural and industrial requirements. Across the broader region, infrastructure development, food security programs, and energy-linked industrial projects continue creating new demand opportunities.

Segmentation Analysis

Process Type

- Wet Process: Dominates global production due to lower manufacturing costs, large-scale fertilizer integration, and widespread availability of phosphate rock feedstock. It remains the preferred route for agricultural and industrial phosphoric acid production worldwide.

- Thermal Process: Primarily utilized for high-purity and specialty-grade phosphoric acid applications requiring superior quality standards. Demand is supported by food processing, pharmaceuticals, electronics manufacturing, and specialized industrial applications.

Application

- Fertilizers: Represents the largest application segment, driven by crop yield optimization, nutrient management requirements, and increasing global food demand across both developed and emerging agricultural economies.

- Food and Feed Phosphate: Supports food preservation, beverage processing, animal nutrition, and dietary supplementation. Growing processed food consumption and livestock production contribute to sustained demand growth.

- Detergents: Utilized in cleaning formulations requiring phosphate-based performance enhancement. Demand is influenced by industrial cleaning requirements and specialized detergent applications despite regulatory constraints in some markets.

- Water Treatment Chemicals: Benefits from increasing wastewater treatment investments, municipal infrastructure upgrades, and industrial water management requirements across rapidly urbanizing regions.

- Industrial: Includes metal treatment, catalysts, chemical intermediates, and surface finishing applications. Broad industrial utilization provides diversification beyond agriculture-dependent demand cycles.

- Electronics: Emerging high-value segment supported by semiconductor manufacturing, precision cleaning requirements, and growing demand for ultra-high-purity phosphoric acid products.

Opportunity Snapshot

| Application | Revenue Contribution | Trend Tag | Adoption Stage |

| Fertilizers | High | Crop Nutrition | Mature |

| Food and Feed Phosphate | Medium | Food Processing | Mature |

| Detergents | Low | Industrial Cleaning | Mature |

| Water Treatment Chemicals | Medium | Water Security | Scaling |

| Industrial | Medium | Process Chemicals | Scaling |

| Electronics | Low | Semiconductor Demand | Emerging |

Phosphoric Acid Market Growth Drivers and Impact Analysis

Rising Global Demand for Phosphate Fertilizers

Agriculture remains the cornerstone of phosphoric acid consumption. Growing population levels, changing dietary preferences, and increasing pressure on agricultural productivity continue to support phosphate fertilizer demand globally. Farmers increasingly depend on balanced nutrient application to maximize yields while maintaining soil health. Phosphoric acid serves as a critical precursor for diammonium phosphate, monoammonium phosphate, and other phosphate fertilizers widely used across major crop systems.

The market impact extends across the value chain of phosphate. For producers with both mining and fertilizer plants, there is more assured demand and a guaranteed supply of their raw materials. Countries that want to increase food security are now producing and importing fertilizers. This market effect continues to give market stability even during times of industrial insecurity.

Expansion of High-Purity and Electronic-Grade Applications

The rise in demand for pure phosphoric acid is due to the growth of advanced manufacturing firms. These include semiconductors manufacturing, electronics manufacturing, specialized chemical manufacturing, and precise industrial processing, which require high standards of purity. These sectors provide much greater profits than the ordinary fertilizer industry. This encourages manufacturers to focus on specialization in such products.

This brings about significant changes in the structure of the Phosphoric Acid market. There will be investments made in purification technology, quality control systems, and specialization in the manufacture of specialty products. The development of electronics-grade phosphoric acid, used for making semiconductors, brings about changes in the direction of investments.

Growing Investments in Water Treatment Infrastructure

As a result of urbanization, industrialization, and water scarcity, the demand for municipal and industrial water treatment plants is growing. Phosphate-based compounds remain key ingredients in applications such as corrosion inhibition, scale formation prevention, and water conditioning. Many governments have realized the importance of investing in infrastructure that can help achieve high-quality water.

This trend supports stable demand from non-agricultural sectors and broadens the market's application base. Producers capable of serving water treatment customers benefit from greater revenue diversification. As environmental standards become more stringent, demand for specialized phosphate-based treatment chemicals is expected to strengthen, creating additional opportunities for value-added product development.

Phosphoric Acid Market Future Trends

Shift Toward Specialty and Purified Phosphate Products

Current Phosphoric Acid market trends indicate that market players are moving towards specialty phosphates, which provide higher profit margins and reduce their exposure to market price fluctuations. Pure phosphoric acid is now being increasingly utilized in applications such as food products, pharmaceuticals, electronics, and sophisticated industries. The trend reflects broader industry efforts to create value through methods other than the manufacturing of fertilizers.

In the future, trends in investments indicate that there will be a shift to more specialty products. Companies that have purification technology along with sound knowledge and customers in high-end areas will have a competitive edge over others. There will be a shift towards specialty phosphates, which may affect capacity plans and alliances in the industry.

Integration of Sustainability and Resource Efficiency Strategies

Environmental concerns have started gaining relevance in phosphate mining enterprises. Investments are being made in recycling water, renewable energy, emission reduction techniques, and resource optimization processes. The notion of sustainability is changing from an obligation into a strategic factor.

Future success in the industry is expected to be determined by efficiency and environmental performance. Firms that manage to decrease their energy consumption and optimize water use and circular resource management are expected to gain competitive advantages. In addition, sustainability investments could help in obtaining financing opportunities.

Phosphoric Acid Market Opportunities

Emergence of Battery Material Supply Chains

The rapid expansion of lithium iron phosphate battery production is creating new opportunities for purified phosphoric acid suppliers. Although battery-related demand remains relatively small compared with fertilizer consumption, it represents a high-growth and strategically significant market segment. Manufacturers are exploring opportunities to develop battery-grade phosphate materials for energy storage and electric vehicle applications.

Investment opportunities abound in purification techniques, specialty processing facilities, and the entire supply chain related to battery materials. Firms that can satisfy high-quality standards can form long-term partnerships with battery manufacturers and developers of technology. Being positioned early in this emerging market can create considerable competitive advantages in the coming years.

Expansion of Semiconductor Manufacturing Capacity

Global programs aimed at investment in the production of semiconductors have been driving up the need for chemicals with extremely high purity, such as electronic-grade phosphoric acid. Fabrication of semiconductors demands strict contamination control and uniformity of chemical quality, making it an appealing market for specialists. Capacity expansion plans in North America, Europe, and Asia are likely to drive future growth in demand.

Those who are able to invest in facilities for purification, quality control, and logistics will be able to take advantage of this trend. Collaborations with the producers of semiconductors and technology platforms can result in access to premium markets with strong profitability and high barriers to entry and favorable profitability profiles.

Recent Developments

- June, 2026: Arianne Phosphate Inc a development-stage phosphate mining company advancing its Lac à Paul project in Quebec’s Saguenay-Lac-Saint-Jean region, announced that it has completed the production of purified phosphoric acid (“PPA”) with its partner Travertine Technologies. As announced in November of 2025, the companies partnered by way of an MoU to test the ability of producing PPA by combining Travertine’s proprietary process with Arianne’s high-purity phosphate concentrate and, subsequently, signed the joint-venture framework agreement earlier this month.

- July 2025: OCP Group launched ChemTechxAI, an open innovation program focused on deep-tech and sustainable specialty chemistry through its Specialty Products & Solutions business unit. The initiative supports innovation in advanced phosphate derivatives, specialty chemicals, and industrial applications, reinforcing the company's downstream diversification strategy.

- February, 2025: Prayon announced the construction of a new electronic-grade phosphoric acid production unit in Bex, Switzerland. This investment will double production capacity to meet the growing demand for ultrapure phosphoric acid, notably linked to the reshoring of the fast-growing semiconductor market in Europe and the United States.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends