Traction Inverter Market Developments and Forecast by 2031

Coverage: By Propulsion (BEV, HEV, PHEV, and Others), Voltage (Up to 200V, 201 to 900V, and 901v and above), Technology (IGBT, MOSFET, and Others), Vehicle Type (Passenger Cars, Commercial Vehicles, and Others), and Geography

- Status : Data Released

- Report Code : TIPRE00014595

- Category : Automotive and Transportation

- No. of Pages : 150

- Available Report Formats :

- Last update date : February 15, 2025

2023 Market Size

US$ 18.13 Bn

Base year value

2031 Forecast

US$ 65.80 Bn

Projected by 2031

CAGR 2023-2031

17.5 %

Growth rate

Addressable Market

US$ 320.55 Bn

(2023-2031)

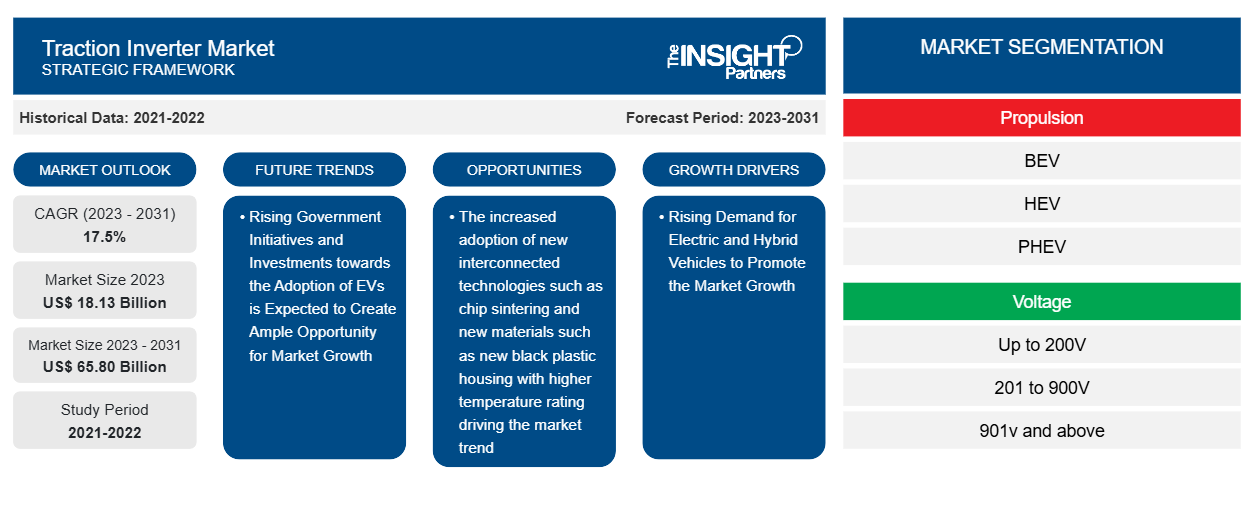

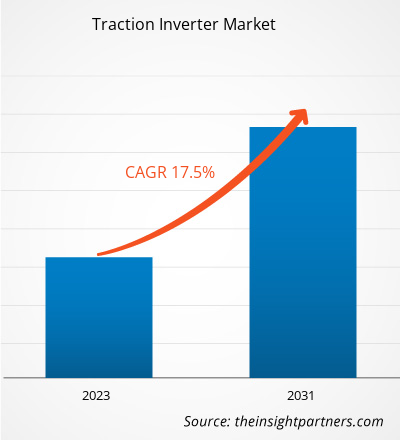

The traction inverter market size is projected to reach US$ 65.80 billion by 2031 from US$ 18.13 billion in 2023. The market is expected to register a CAGR of 17.5% during 2023–2031. The increased adoption of new interconnected technologies, such as chip sintering, and new materials, such as new black plastic housing with higher temperature ratings, are driving the market trend. The increasing adoption and sale of electric vehicles are major trends that are expected to likely drive market growth.

Traction Inverter Market Analysis

The major stakeholders in the traction inverter market ecosystem include raw material suppliers/component suppliers, traction inverter manufacturers, and end-users. The raw material supplier is a crucial stakeholder in the ecosystem of the Traction inverter market. The major raw materials are semiconductors, IGBTs, MOSFETs, gate drivers, power supply ICs, and others. The major raw material suppliers include Arrow Electronics, Power Integrations, STMicroelectronics, Infineon Technologies AG, and Danfoss, among other players. For instance, in July 2022, Danfoss supplied completely electric drivetrains to Shin Bus Group, the national bus operator of Taiwan, helping them to achieve their net-zero targets by building their electric buses. In March 2022, Infineon Technologies launched EDT2 IGBTs in a TO247PLUS package, devices that are optimized for automotive discrete traction inverters. The devices have the potential to improve the performance of inverter systems. Thus, such growing initiatives from the raw material suppliers are strengthening the production of broaching machines, which is propelling the market growth.

Traction Inverter Market Overview

The traction inverter is located between the high-voltage system battery and the electric motor in the high-voltage electrical system of a car, truck, or bus. The motor is driven by converting the DC power from the HV system into three AC output phases. A vital part of an EV, the inverter and motor work together to determine the dynamics, performance, and driving experience. The effectiveness of the motor and traction under all driving conditions, including acceleration, steady state, and energy recovery into the battery through regenerative braking, directly affects a vehicle’s range. Power integrations provide gate drivers and power supply ICs for the traction inverter that are automotive-qualified, which increases efficiency while reducing cost and space requirements and ensuring functional safety. Packages meet the most recent criteria for vehicles upgrading to 800 V designs with reinforced isolation and longer creepage distance.

Market Research Highlights

- Global market for Traction Inverter was valued at US$ 18.13 Billion in 2023

- Annual market size is expected to reach US$ 65.80 Billion by 2031

- Total addressable market (TAM) during 2023-2031 is projected to reach approximately US$ 320.55 Billion

- Market is anticipated to register a CAGR of 17.5% during the forecast period

- The United States represents a key market, supported by Rising Demand for Electric and Hybrid Vehicles to Promote the Market Growth, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as The increased adoption of new interconnected technologies such as chip sintering and new materials such as new black plastic housing with higher temperature rating driving the market trend are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Infineon Technologies AG, Continental AG, Delphi Technologies Plc, Hitachi, Ltd., Mitsubishi Electric Corporation, Siemens AG, Toshiba Corporation, Voith GmbH & Co. KGaA, Curtiss-Wright Industrial Group, Dana Incorporated, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Traction Inverter Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Traction Inverter Market Drivers and Opportunities

Rising Demand for Electric and Hybrid Vehicles to Promote the Market Growth

One of the main causes fostering an optimistic view of the industry is the notable increase in the demand for electric and hybrid electric vehicles worldwide. Due to the rise in demand for higher levels of integration and increased power density across electric vehicles, automotive manufacturers and suppliers are increasing their production. Accordingly, the market is expected to increase due to the rising demand for lithium-ion batteries. The majority of plug-in hybrids and electric vehicles make use of lithium-ion batteries. The production of automotive lithium-ion batteries has increased by 33% in the year 2020. Additionally, several technical developments, like the WBG devices, primarily SiC and GaN, are boosting market expansion.

The Si-IGBT is preferably used across the automotive industry owing to its affordability, efficiency, and short circuit capacity. In addition, the sincere measures taken by the government and market players show lucrative opportunities for the growth in demand for tractive inverters with regard to the rising production of electric cars. The market is expected to develop due to additional factors, such as rising awareness among consumers, OEMs, and numerous suppliers brought with government stringent laws will further encourage the growth of the market.

Rising Government Initiatives and Investments toward the Adoption of EVs are Expected to Create Ample Opportunities for Market Growth

In North America, initiatives by the government, federal policies, and programs for various industries are expected to drive electric vehicles, resulting in higher growth of the traction inverters market. The US, Canada, and Mexico signed the trade deal NAFTA. The trade deal helped automakers with the increased number of manufacturing facilities and enhanced supply chain of auto parts. The Saudi Vision 2030 is an initiative that aims to diversify the Saudi economy away from oil and is encouraging the adoption of electric vehicles (EVs) to increase energy efficiency in its transportation sector. Dubai is promoting its long-term goal of electrification. Smart city projects and the rise in foreign direct investments are boosting the adoption of advanced technologies in the MEA region.

Traction Inverter Market Report Segmentation Analysis

Key segments that contributed to the derivation of the traction inverter market analysis are propulsion, voltage, technology, vehicle type, and geography.

- Based on propulsion, the market is divided into BEV, HEV, PHEV, and Others. Among these, BEV has the largest share in 2023, owing to increased sales of electric vehicles. According to the International Energy Agency, electric vehicle sales reached 14 million in 2023 and are projected to reach 17 million in 2024. Such growth in electric vehicle sales has created a massive demand for the traction inverter market during the forecast period.

- Depending upon the voltage, the market is divided into Up to 200V, 201 to 900V, and Above 901 V. Among these, 201 to 900 V has the largest share in 2023. This is owing to the increasing demand for commercial vehicles.

- Based on technology, the market is divided into IGBT, MOSFET, and others. Among these, MOSFET had the largest share in 2023. This is owing to high reliability and adoption among commercial vehicles.

- Based on vehicle type, the market is divided into passenger cars, commercial vehicles, and others. Among these, commercial vehicles have the largest share in 2023, owing to increased demand for the increased commercial vehicle sales across the globe.

Traction Inverter Market Share Analysis by Geography

The geographic scope of the traction inverter market report is mainly divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South America.

Asia Pacific is considered to be the fastest growing economic region, with China as the largest market for high-performance electric vehicles, followed by Japan, giving an opportunity for the development of the electric bus market. The establishment of new production facilities for electric buses in Vietnam and The Philippines is also supporting the market growth in the region. Additionally, The macroeconomic outlook for India is encouraging, and initiatives like the OROP law and the seventh pay commission will increase spending.

Traction Inverter Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2023 | US$ 18.13 Billion |

| Market Size by 2031 | US$ 65.80 Billion |

| Global CAGR (2023 - 2031) | 17.5% |

| Historical Data | 2021-2022 |

| Forecast period | 2023-2031 |

| Segments Covered |

By Propulsion

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Traction Inverter Market Players Density: Understanding Its Impact on Business Dynamics

The Traction Inverter Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Traction Inverter Market News and Recent Developments

The traction inverter market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the developments in the traction inverter market are listed below:

- LEM, a leading global company in electrical measurement for industrial and automotive applications, has launched the HAH3DR S07/SP42, a new compact current sensor designed for 800V three-phase power modules. Developers of automotive traction inverters are increasingly using three-phase power modules such as the popular and widely proven Hybridpack Drive from Infineon. These modules are now adopting the more efficient SiC MOSFET technology, allowing vehicles to use 800V battery systems that offer faster charging and longer driving range. (Source: News Letter, November 2023)

- Infineon Technologies AG launched a new automotive power module, HybridPACK Drive G2, for traction inverters in electric vehicles. It builds on the well-established HybridPACK Drive G1 concept of an integrated B6 package, offering scalability within the same footprint and extending it to higher power and ease of use. The HybridPACK Drive G2 will be available with different current ratings, voltage levels (750V and 1200V), and Infineon’s next-generation chip technologies EDT3 (Si IGBT) and CoolSiC G2 MOSFET. (Source: Company Website News, April 2023)

Traction Inverter Market Report Coverage and Deliverables

The “Traction Inverter Market Size and Forecast (2021–2031)” report provides a detailed analysis of the market covering below areas:

- Traction inverter market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Traction inverter market trends as well as market dynamics such as drivers, restraints, and key opportunities.

- Detailed PEST and SWOT analysis

- Traction inverter market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the traction inverter market

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends